ASAN - Asana: Tread Carefully Shares Remain Unattractive

2024-01-03 04:33:22 ET

Summary

- Asana's fundamental outlook remains weak given competitive pressures.

- The company has shown slowing revenue growth and weak margins, especially relative to peers.

- The company's long-term financial targets also appear too optimistic.

Since my initial writeup of Asana ( ASAN ) stock, fundamentals remain challenged with intense competition and the investment thesis is simply uncompelling.

To entertain the bull case, Asana is one of the category leaders in the work management category, has continuously invested into product development for new platform solutions (including AI-driven features), and has created new pricing packages to drive revenue growth. Additionally, Asana boasts its strong customer adoption, its ability to upsell into higher pricing tiers, and of course, its high net retention rates. In October 2023, Asana provides a 110 slide investor presentation that detailed the company's platform, packaging options, long-term outlook, financial targets, etc. Overall, the average investor would conclude that Asana will beat the competition and provide solid long-term returns. However, I remain skeptical that will be the case here.

Now onto the more worrisome elements in the Asana story. On slide 88, management states that the total addressable market ("TAM") will increase from $45 billion in 2023 to $79 billion in 2027. While growth is central to the investment thesis, whenever companies cite enormous TAM figures, investors need to put their skeptical hats on. Let's see how the "collaborative applications" total addressable market is defined. IDC's collaborative applications is described to encompass "team collaboration applications, enterprise community applications, conferencing, virtual events, and email applications." To what extent does Asana provide conferencing, virtual events, and/or email solutions? Asana's core focus is certainly centered around team collaboration applications, while the other categories seem to be less of the target audience. Put another way, are customers going to use Asana for video conferencing or email, like they would use Zoom, Microsoft teams, Microsoft Outlook, etc.? My guess is probably not. Of course Asana can provide integrations, but actually offering the core product to fulfill the business need is an important difference. So investors should consider that when assessing TAM potential here.

My second concern is that management estimates the TAM is expected to grow by 15% CAGR over the next four years. That's an interesting figure because Asana's Q3 2023 earnings reported net revenue growth was 17.7%, which is still above market, but is rapidly decelerating compared to prior quarters. So investors should be mindful of ASAN's quarterly revenue growth and if it slips below that 15% threshold because that's a potential indication it would be underperforming the average growth rate of the industry.

Moreover, for a company that has nearly $700 million in annualized revenue, or 1.5% of its TAM, it's a little surprising to see such a rapid deceleration in revenue growth. Something is happening, and my take is that it's stiff competition. Looking at four direct competitors, all have experienced a significant drop off in revenue growth over the last three years:

Of course, ASAN's existing customer base plus incremental opportunity combined with their new pricing packages affords growth runway, but the rate of growth is a concern relative to the estimated industry average. So either the aforementioned factors are enough to reinvigorate growth, or the company will need to boost sales & marketing, etc. Clearly there are differentiators between work management platforms as Asana has outlined (see slide 55), but Asana is the worst positioned among the four listed above regarding its P&L. It has the smallest annualized revenue base, the weakest margins, and the worst free cash flow profile. Put simply, ASAN is going to have the least capital resources available to push growth relative to its larger peers, and this comes at a time when Asana is trying to be more cost disciplined.

Then turning to the Q3 2024 earnings call , analyst Pat Walravens of JMP Securities drew attention to management's mention of growth headwinds during the period. CFO Tim Wan responded by describing pressure in their net expansion rates and overall weakness being tied to the Americas:

I think we're still seeing pressure on renewals. So, I think there is compression kind of in our net expansion rates, that's one. And I do think we'll lap those by the end of Q1, primarily because we do -- like if you kind of look back at layoffs in tech, there were a number of large companies that were still doing layoffs at the beginning of Q1. And I think once we kind of get through that period, I think we'll have some more tailwinds in our NRR.

The other piece, obviously, is I think like the regions that I spoke about that are performing, EMEA and APAC, those have been nice surprises, but I think we still have more work to do in Americas."

There were lingering technology layoffs, which is valid. However, Mr. Wan seems to suggest that without that drag, then growth should revert. It will be interesting to see if that plays out. Remember, even with those software development layoffs, overall U.S. employment is still trending at all time highs and yet all four companies reported lower growth. It's possible that this could be less of a macroeconomic trend and more of an industry trend. Whatever the case is for the growth weakness, it happened, ASAN's revenue growth trend has been steadily deteriorating.

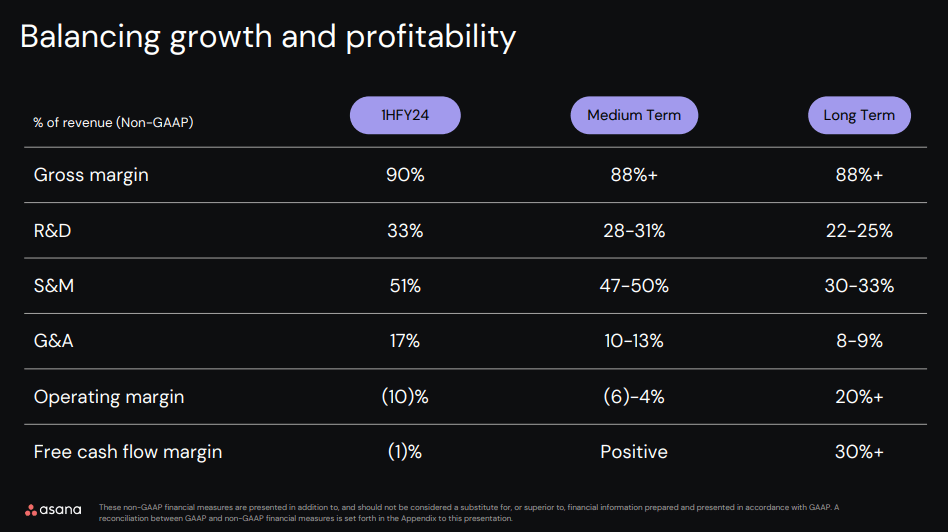

Last and most concerning of all, ASAN has stated that it is targeting long-term operating margins of 20%+ and free cash flow margins of 30%+, as shown below. Quite frankly, I don't even understand how a company can sustainably achieve free cash flow margins in excess of its operating margins when considering taxes. More importantly, ASAN has to work its way up from a -38% operating margin to 20%, which will take a very long time, if it's even achievable. For context, Apple Inc. ( AAPL ), among the most profitable companies in the U.S., sports a TTM operating margin of 30% and free cash flow margin of 26%. So again, for a software platform, that's quite the hurdle.

{kind=link}

Asana Investor Day 2023 Slide 97 (Asana Investor Day 2023 Presentation)

Bottom Line

Asana is experiencing growth challenges driven by intense competition, which is growing faster. Unless the company's growth rate stabilizes, management will have difficulty improving margins without implementing cost cutting measures. Unfortunately, I believe the bull thesis remains weak and investors should still avoid ASAN shares. Thanks for reading and please comment below.

For further details see:

Asana: Tread Carefully, Shares Remain Unattractive