PACB - Assessing Pacific Biosciences And Their Revio Launch

2023-04-21 18:34:12 ET

Summary

- Pacific Biosciences of California, Inc.'s Revio long-read sequencing system is poised to enable large-scale research projects with increased efficiency.

- The commercial launch of the Revio platform, alongside the ongoing beta testing of the Onso benchtop short-read DNA sequencing platform, puts Pacific Biosciences on track for significant revenue growth.

- Despite potential risks, PacBio's progress in execution suggests that the company remains on a solid growth trajectory and well-aligned with its projections.

In a previous analysis, I discussed Pacific Biosciences of California, Inc. ( PACB , "PacBio"), a company that has recently introduced new products aimed at driving strong growth and improving gross margins over the next several years. Their core technology, single molecule, real-time ((SMRT)) technology, has a wide range of applications in genomics, epigenomics, transcriptomics, and metagenomics. With the launch of their Revio long-read sequencing system and the initiation of external beta testing for the Onso benchtop short-read DNA sequencing platform, PacBio aims to start ramping up revenue. Given Revio's launch and the release of the 2022 financials, it seems a good time to review the company.

Pacific Biosciences Catalysts: Revio

In the recent 4Q22 earnings call , we gleaned a few intriguing insights about PacBio. The enterprise is on the cusp of unveiling Revio, anticipated to be its most groundbreaking long-read sequencer to date. This system is poised to be a step forward in the field by markedly enhancing the efficacy of sequencing projects. As a result, researchers will be able to tackle large-scale endeavors with reduced time and expense, while gaining a more comprehensive and precise understanding on structural variations, epigenetic profiles, and single nucleotide variants.

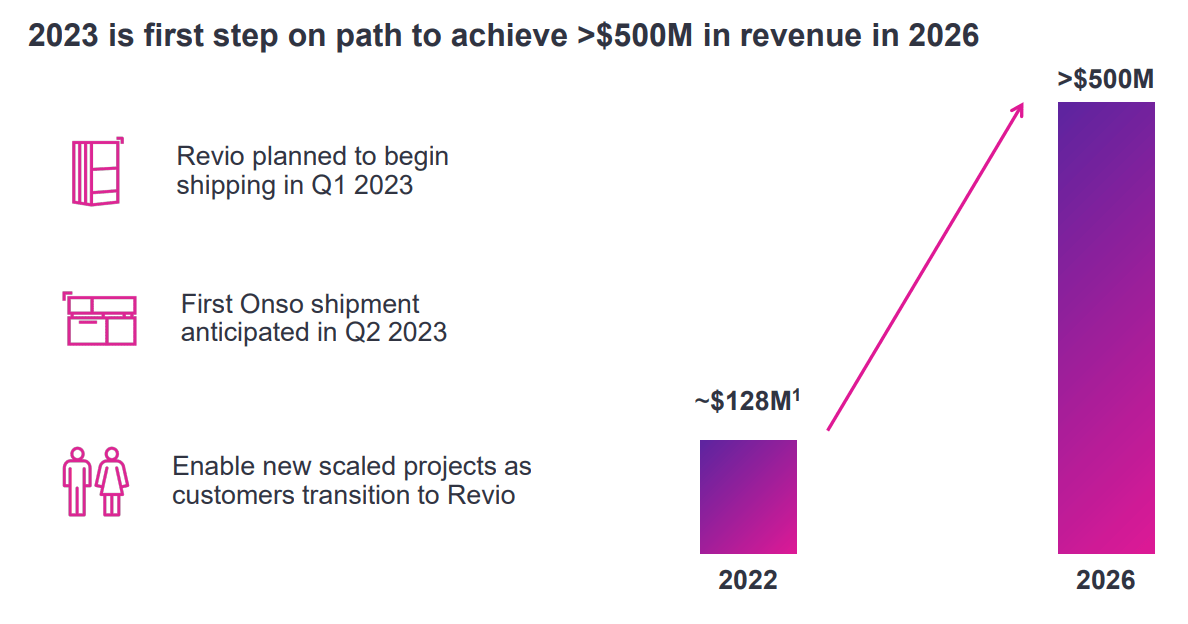

The widespread commercial availability of Revio is just around the corner, with a minimum of 25 units slated for delivery to clients before the quarter's conclusion. Preference will likely be given to customers with higher throughput. The firm intends to ramp up manufacturing during the second quarter, culminating in the target production rate for 2023 by the close of Q2. Furthermore, the objective is to attain a compound annual growth rate of 40% to 50% through 2026, fueled by the promise of the Revio platform.

Consequently, 2023 is projected to be a transitional year for product offerings, as numerous Sequel II and IIe users switch to the Revio platform. This may result in some temporary fluctuations in consumable revenue. Throughout the year, revenue momentum is expected to stem primarily from Revio, supplemented by modest Sequel IIe system placements and the commercial release of the short-read sequencer in Q2 of 2023.

Platform Advantages

Researchers emphasize the significance of long read sequencing, particularly HiFi reads , in achieving comprehensive and precise variant calls. PacBio stands out as a leader in this field, excelling at variant calling even with lower coverage, which translates to increased cost-effectiveness and efficiency for numerous research endeavors.

Pacific Biosciences

As the need for high-precision reads grows, PacBio's long reads are gaining recognition and being employed in various groundbreaking studies and initiatives. PacBio's Revio holds promise in propelling further discoveries due to its enhanced throughput and cost-efficiency for large-scale research projects and broader applications. The Corteva Agriscience partnership is a positive sign about Revio's potential to scale research and explore the genome.

The first early access Revio system is slated to be sent to the Broad Institute. To expand long-read sequencing capabilities for initiatives like the NIH's All of Us program, the Broad Institute has ordered 10 Revio systems.

However, their success is not solely dependent on Revio. The Onso beta program has been advancing at a steady pace with institutions such as the Broad Institute, Corteva Agriscience, and Weill Cornell, and the feedback gathered thus far emphasizes the potential for this technology to revolutionize numerous genomic applications.

As we anticipate the commercial launch of Onso in the forthcoming quarter, it is worth noting that it will include enhanced sensitivity in detecting variant allele frequencies and possible utility in single-cell workflows.

During the 4Q22 earnings call , the management team candidly discussed areas where further improvement is necessary before Onso can reach its full potential. These areas include scaling up instrument production, refining the chemistry, ensuring consistent flow cell production, and enhancing software capabilities. Additionally, the company is committed to incorporating feedback from beta customers into the final product, all while carefully managing the launch of Onso without creating any disruptions to the Revio introduction.

Nevertheless, it is essential to maintain some balance, as the management team has acknowledged that Onso is not expected to significantly influence the company's financial performance in 2023. This recognition is reflected in their guidance for the year, which the management argues bears little impact from Onso.

Valuation for Pacific Biosciences

In 2023, the firm anticipates generating revenues in the range of $165 million to $180 million, reflecting a 29% to 40% increase. During the fourth quarter, 76 orders were placed for the Revio systems. The business plans to seize this opportunity by promoting the widespread use of the Revio sequencer, converting existing clientele and enticing newcomers to appreciate the merits of its comprehensive capabilities.

Taking this into consideration, the organization remains steadfast in its aim to reach $500 million in revenue by 2026. In an effort to attain this goal, the firm issued additional shares at the start of the year, successfully raising $201 million through the issuance of 20.1 million shares at a price of $10 each. This move is expected to fortify their financial position and help navigate potential challenges stemming from the prevailing interest rate environment.

My estimations point to a cash-burn of approximately $240 million in 2022. Given the current burn rate and accounting for the influx of new capital, the company's cash reserves should suffice until the close of 2026. Should they manage their resources effectively, they could potentially avoid the need for additional fundraising until they achieve operational cash-flow break-even.

With respect to the future outlook for this stock, I will maintain the majority of assumptions from my previous analysis while making adjustments to the diluted shares and updating the annual returns to account for the increased stock price. In the "bull" scenario, I foresee Pacific Biosciences generating $500 million in sales and nearing break-even cash flow. On the other hand, the "bear" scenario may see the company attaining only $200 million in sales and struggling to achieve positive cash flow. I base these projections on a 10% annual increase in diluted shares, in line with historical trends.

{kind=link}

In the event of a favorable market climate, one might foresee PacBio being valued at a generous 20 times revenue per share, a testament to its strong performance and swift revenue growth. On the other hand, should the market take a more pessimistic turn, a more conservative valuation of 10 times revenue per share might be in order.

Author's computations

Since my previous missive regarding PacBio, the stock has seen growth, which is mirrored in the more balanced annualized returns that still display a somewhat asymmetrical positive potential. Nevertheless, there are risks to consider. Predicting the effects of the announced Revio launch on the Sequel II platform is an uncertain task, and it might lead to a sort of Osborne effect, resulting in a dismal quarter and a plummeting stock price.

Another concern is the company's reliance on an ambitious growth rate of nearly 45% annually through 2026, a challenging feat to accomplish. Evidently, anything less than a 45% annualized growth rate would not justify a 20 times valuation.

From a technological standpoint, PacBio's single-molecule, real-time ((SMRT)) technology might have certain drawbacks. For instance, the substantial cost of this technology could limit its appeal to some researchers and institutions. Moreover, the vast data produced by PacBio's SMRT technology might necessitate specialized software and computational resources for analysis, potentially restricting its usage among researchers. Furthermore, SMRT technology may not be the best fit for all genetic analysis scenarios, and in some cases, alternative technologies might be more suitable. On a wider macroeconomic scale, there exists the risk that PacBio might fail to quench its cash-burning operations, and given the current credit market conditions, the company could struggle to secure refinancing.

Despite these risks, we observe favorable progress on the execution front, indicating that Pacific Biosciences of California, Inc. remains on a growth trajectory and on track with its projections.

For further details see:

Assessing Pacific Biosciences And Their Revio Launch