AZN - AstraZeneca: Think Medium-To-Long Term

2023-05-25 11:02:29 ET

Summary

- AstraZeneca's price has moved sideways in the past month, after showing good progress for some time.

- A look at its numbers reveals that it is going strong, and will continue to do so in the foreseeable future. However, it is fairly valued at this time.

- There might be limited upside for short-term investors, but it is still a buy from a medium to long-term perspective.

If there's one stock I've had an almost consistent Buy rating for over the years, it is the oncology treatment provider AstraZeneca ( AZNCF )(AZN). For good reasons. The most direct of them being the predictably good returns it gives investors, more often than not. Since the time I first covered it at Seeking Alpha, in September last year, it is up by 22% and by another 8% since my last update in February this year as I write.

However, in the past month, its price has only moved sideways. It is hard to overlook the fact that it coincides with the time since which it has released its first quarter results (Q1 2023) in April 2023. Here I take a closer look at it to see if there are any fundamental reasons that this is happening and based on that, what is next for it.

Sustained revenue growth ex-COVID-19 vaccine sales

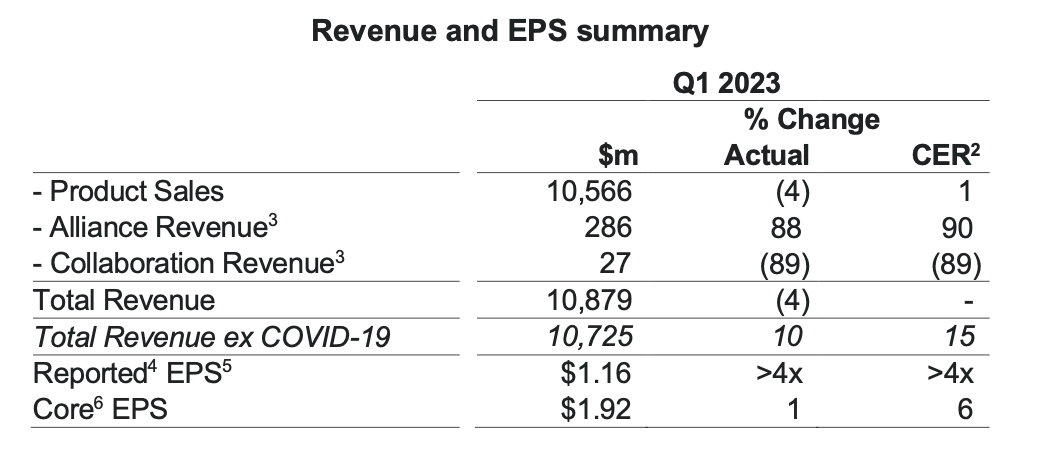

At first glance, its revenue itself looks disappointing. The actual revenue declined by 4% year-on-year (YoY), while at constant exchange rates [CER] it slowed to a 1% growth. For context, in FY22 (which is also the calendar year 2022), the company showed a 19% growth at actual rates and 25% growth at CER. There is a good basis for the latest softening. There was a sharp drop in vaccine sales since the pandemic is all but over. The company's Q1 2023 revenue ex-COVID-19 vaccine sales actually grew by a healthy 10% at actual rates and at 15% at CER.

{kind=link}

Mixed earnings growth picture

Interestingly, though, while revenue growth has softened overall, the company has seen over 4x increase in its reported earnings per share [EPS]. Some of this was expected purely due to the reduced sales of its COVID-19 vaccine, which is a lower margin segment. This is visible in the significant bump up in gross margin to 82% from 68% in Q1 2022.

But it is also down to a base effect. Q1 2022 saw a dramatic shrinking in the EPS during the quarter to USD 0.25 on account of inventory fair value adjustments on the Alexion acquisition. For context, for the full year 2022, reported EPS was at USD 2.12, indicating proportionally higher EPS for the rest of the quarters. Unsurprisingly, Core EPS, which was not impacted by the said adjustment, was strong last year too, consequently, it has risen by just 1% in Q1 2023 at actual rates.

EPS growth expected

The Core EPS figure is expected to gain ground over the rest of 2023, though. In its guidance, AstraZeneca says that it will rise by "a high single-digit to low double-digit percentage". The inventory value adjustment continues even now, but the company expects it to "be minimal in future quarters". This suggests that the difference between reported and core EPS should narrow, in fact it already has in Q1 2023. This in turn implies the potential for continued further increase in reported EPS figures.

Market multiples indicate fair valuation

Analysts are optimistic about the company's EPS figures for 2023, expecting it to come in at the upper end of the range, with an almost 11% growth. This yields a forward core or non-GAAP price-to-earnings (P/E) ratio of 20.1x, which is just a shade higher than that for the healthcare sector at 19.5x.

The trailing twelve months [TTM] GAAAP P/E ratio might still look like a source of concern at almost 50x, compared to 26x for the sector. However, since the reported EPS was significantly lower than the core EPS last year, as discussed earlier, the resulting P/E ratio looks far more inflated than the corresponding non-GAAP P/E ratio at 22.1x compared to 18.3x for the sector. And this is the ratio I would take into account for now as the gap between the two metrics is set to reduce in the coming quarters. It does however indicate that AstraZeneca is fairly priced in any case.

Progress in new treatments

That said, this analysis takes into account the company's performance only over the next year or so. There are enough signs that suggest that the company can continue to perform well in the years to come. In its latest earnings presentation it points to 10 blockbuster opportunities (see page 7 of link). Since then, it has reported good results from phase three trials for Tagrisso in treating non-small cell lung cancer, which is the most common form of lung cancer. Cancer treatment is already the strongest segment for AstraZeneca, accounting for 38% of its revenues in 2022.

{kind=link}

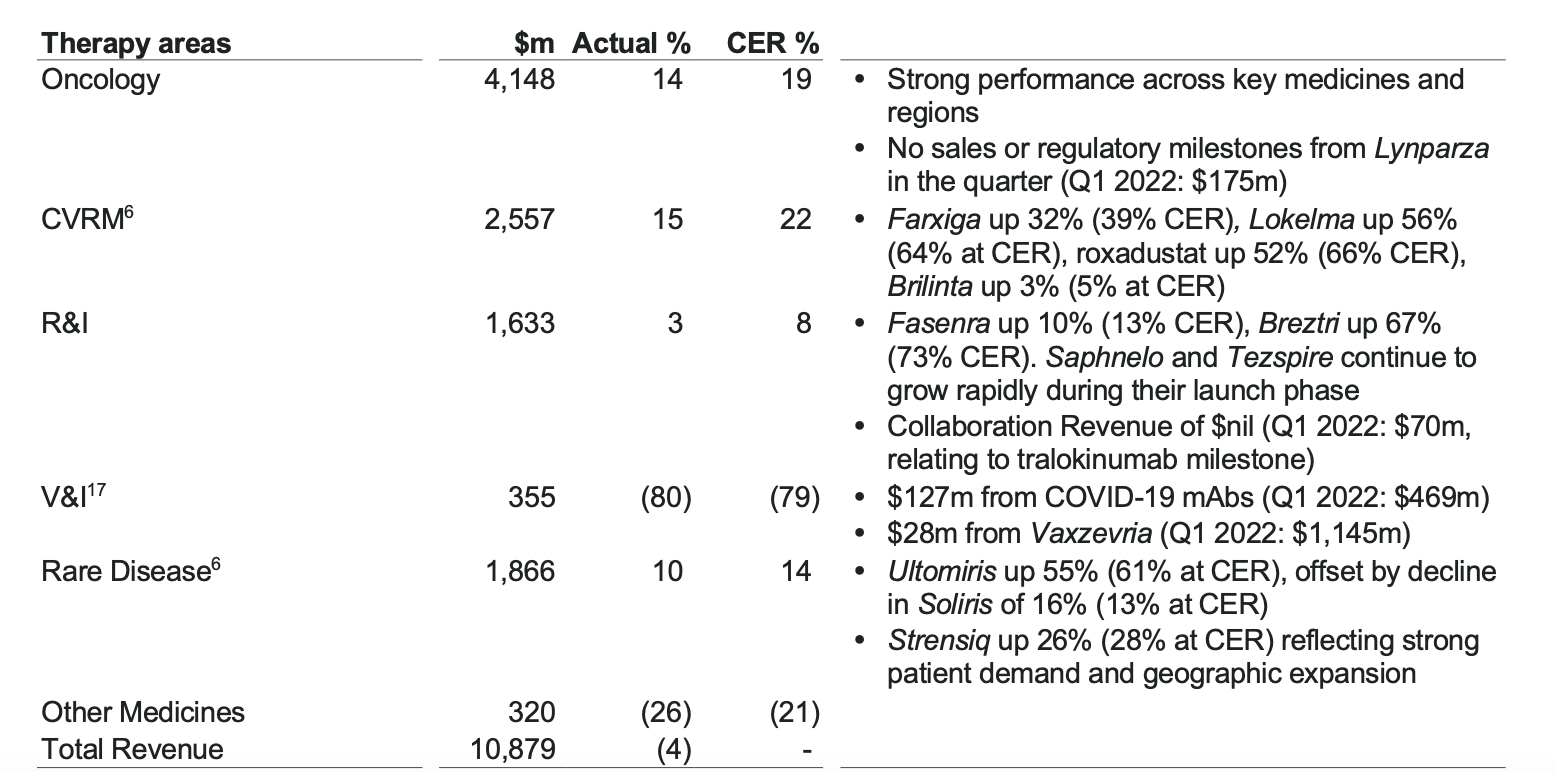

Further, Farxiga, its treatment for heart failure has also been approved in the US . It has already shown robust growth of 32% YoY in Q1 2023, and has managed to improve performance of the cardiovascular, renal and metabolism [CVRM] segment, which is the second biggest contributor to the company's revenues. This bodes well for the company's growth as such, considering that the US is its biggest market, with a 42% share in total sales.

Even otherwise, the company's growth as earlier discussed is strong, with double digit growth in Q1 2023 across oncology, CVRM and rare diseases (see table above). The last one is particularly notable, since the segment is a result of the Alexion acquisition, indicating that all is possibly going well on that front.

What next?

There's no doubt that AstraZeneca remains a leading pharmaceutical company, with growing sales, sustained earnings and a pipeline of treatments that augur well for its future. Its outlook for 2023 further backs this up, with healthy revenue and earnings growth expected.

This indicates that it can continue to hold investors in good stead over time. Its past performance is already proof. Even with all the ups and downs that have happened in between, the company has almost doubled investors' money over the past five years. However, for investors with a time horizon of a year or so, realistically, I see limited upside for now. The market multiples indicate that it is fairly valued. There could be a better opportunity to buy it at a later date. I am tempted to put a Hold rating on it for that reason, but I also believe it is one that should be held for at least the medium term for real gains to come in. For that reason, AstraZeneca stock is still a Buy for me.

For further details see:

AstraZeneca: Think Medium-To-Long Term