CA - Avino Silver & Gold Mines Q1 Earnings: A Slow Start To The Year

2023-05-14 04:28:52 ET

Summary

- Avino Silver & Gold Mines has been one of the worst-performing silver stocks in Q4, down 14% quarter-to-date vs. a 5% decline for the Silver Miners Index.

- The poor performance is likely attributed to the stock getting ahead of itself in March and a softer Q1 report financially, impacted by a delayed concentrate shipment.

- The good news is that Avino should see a stronger Q2 and recently received encouraging metallurgical results from its Oxide Tailings Project, with a PFS due by Q1 2024.

- That said, I continue to see Avino as a relatively marginal producer in a jurisdiction that continues to get less attractive, so I see better reward/risk bets elsewhere.

Just over three months ago, I wrote on Avino Silver & Gold ( ASM ), noting that while the stock had a better year ahead with work continuing on pillars for future growth (La Preciosa community engagement, bringing Oxide Tailings Project to PFS level), there was elevated risk to paying up for the stock above US$0.85. The stock immediately suffered a 24% drawdown and while it briefly traded above its January highs, any gains have been fleeting. The underperformance may be attributed to what was a slow start to the year, with ASM being one of the worst-performing silver miners year-to-date, and Mexico's investment attractiveness not getting any better following recent mining law reforms . Let's dig into the quarter closer below:

Q1 Production

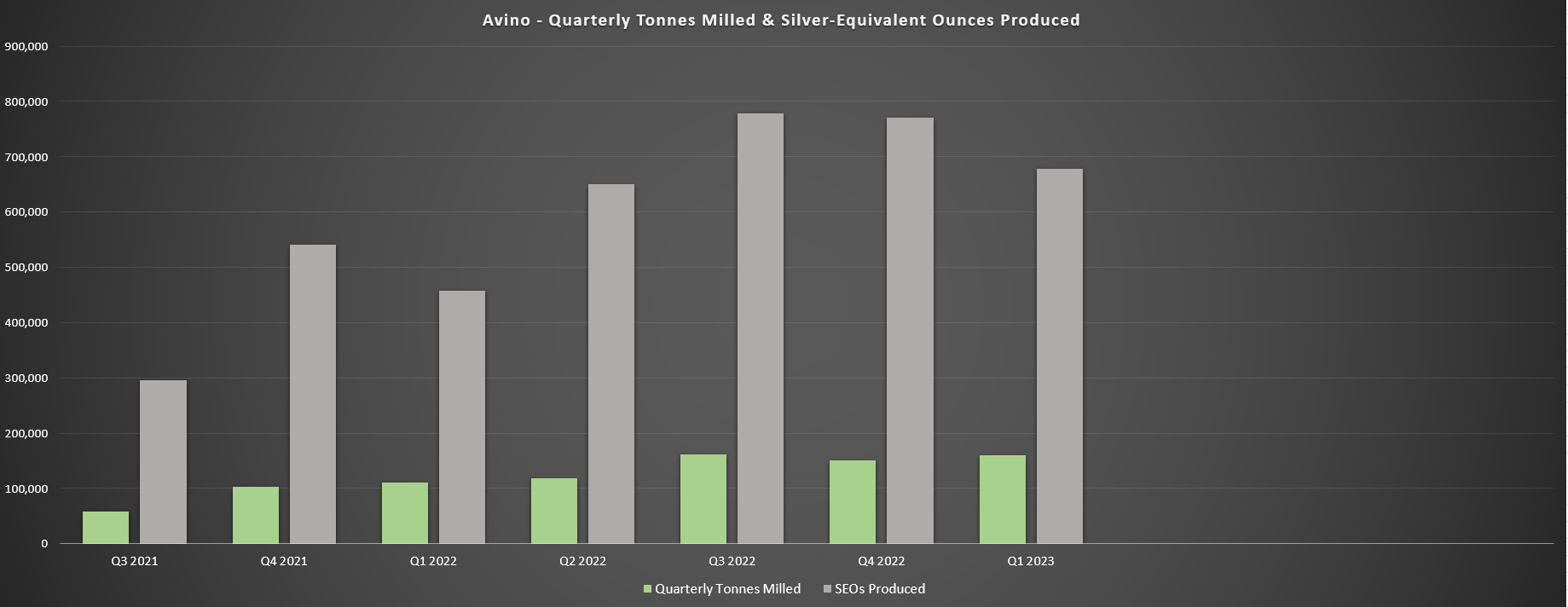

Avino Silver & Gold Mines ("Avino") released its Q1 results last week, reporting quarterly production of ~678,200 silver-equivalent ounces [SEOs], a 48% increase from the year ago period. The sharp increase in output was related to being up against easy comparisons in the year-ago period, as the asset was ramping back up towards full production levels after a temporary shutdown of operations until August 2021. Unfortunately, the higher production did not translate to an increase in revenue for Avino, with a concentrate shipment planned for Q1 being pushed into Q2. The result was just ~506,700 SEOs sold in Q1, well below its quarterly production figures.

Avino - Quarterly Tonnes Milled & SEOs Produced (Company Filings, Author's Chart)

{kind=link}

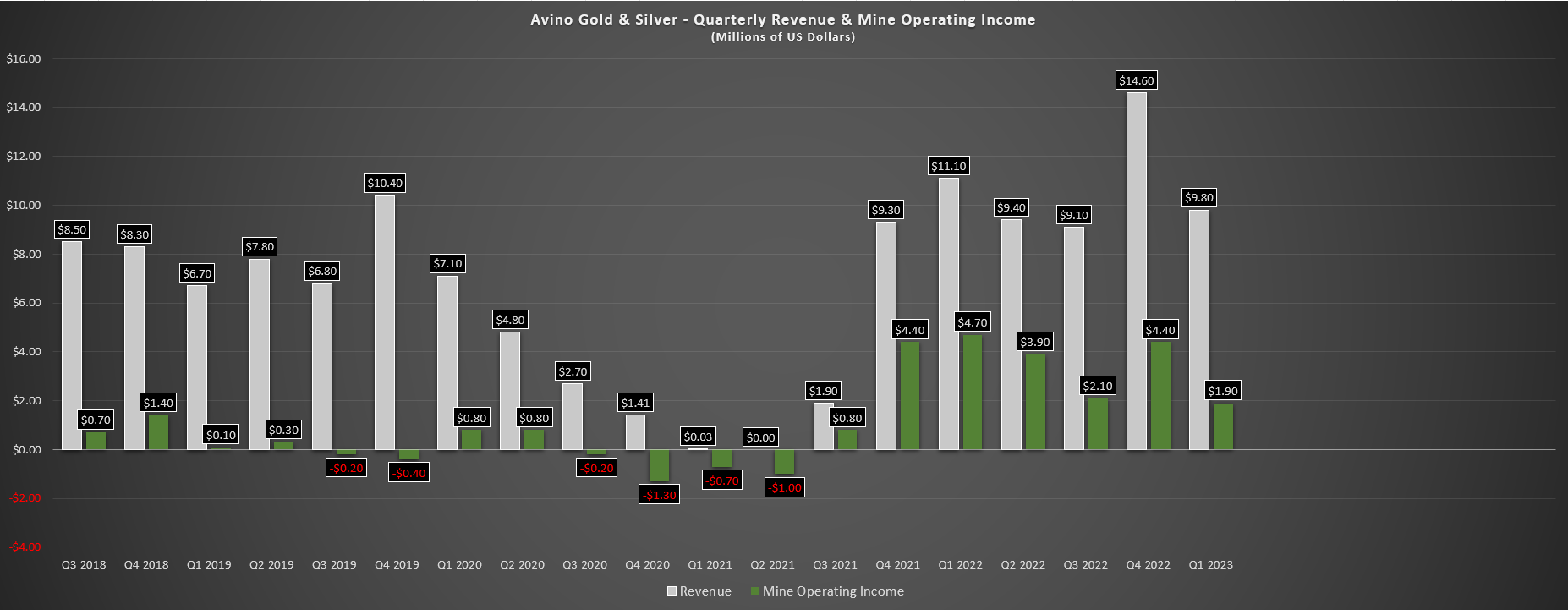

The silver lining is that mill performance was solid in the period, with ~159,800 tonnes processed at grades of 51 grams per tonne of silver, 0.58 grams per tonne of gold, and 0.47% copper, respectively. This was an improvement from the year-ago period and most recent quarter from a throughput standpoint, though grades fell vs. Q4 2022 levels. The result of the lower sales was that revenue declined to just $9.8 million, mine operating income slid to $1.9 million, and operating cash flow came in at just $0.4 million, down from $3.5 million in the year-ago period. This left Avino with just $2.7 million in cash at quarter-end despite proceeds from share sales under its ATM that led to minor dilution (~253,700 shares sold in Q1 2023).

Avino - Quarterly Revenue & Mine Operating Income (Company Filings, Author's Chart)

{kind=link}

Operating Costs & Recent Developments

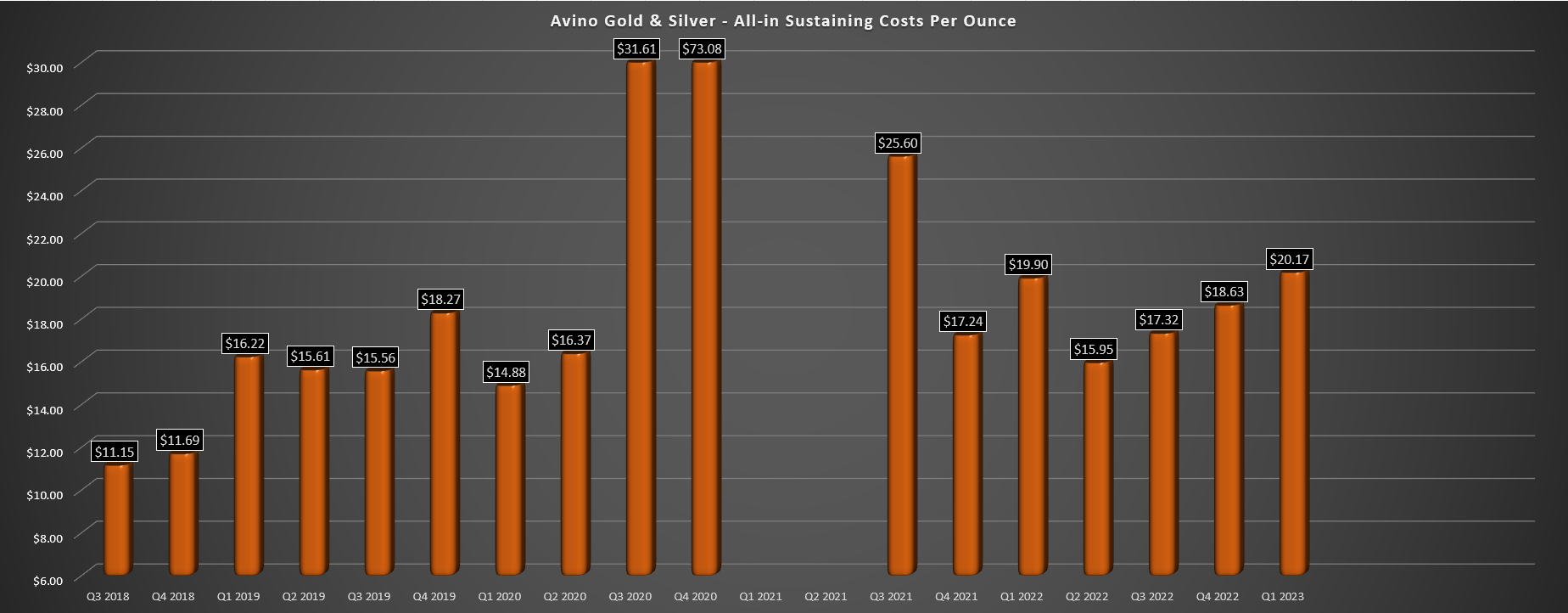

Moving over to costs and margins, Avino saw a material increase in cash costs in the period, with cash costs increasing to $14.22/oz and all-in sustaining costs increasing to $20.17/oz despite the 2nd lowest cost quarter from a sustaining capital standpoint in two years. This has continued a long trend of rising costs at the Avino Mine, with AISC consistently coming in above $17.00/oz vs. sub $17.00/oz pre-inflationary pressures. One potential impact on costs is the stronger Mexican Peso we've seen year-to-date, and the strength of the Peso has persisted into Q2, with the USD/MXN exchange rate at its lowest levels in five years. This could continue to affect Avino's unit costs, though Q1 saw an impact from lower sales volumes because of the Q1 planned shipment shifting into Q2.

Avino - All-in Sustaining Costs Per Ounce (Company Filings, Author's Chart)

{kind=link}

From a positive standpoint, Avino reported encouraging metallurgical results from its Oxide Tailings Project in April, which is home to a ~5.7 million tonne resource at an average silver-equivalent grade of 95 grams per tonne of silver. According to recent metallurgical work, gold and silver recoveries were estimated at 88.2% and 86.0% using agitation leaching and 75.5% and 76.2% using heap-leaching on its lower-grade 'ancient oxides' samples. Meanwhile, recoveries were estimated at 85.7% and 78.6% on gold and silver for agitation leaching and 76.0% and 63.7% for gold and silver using heap leaching on its slightly higher-grade recent oxides sample. These are solid results and will be implemented into a PFS expected by Q1 2024.

Meanwhile, Avino is confident in its ability to grow production through the nearby La Preciosa Project, with community engagement ongoing ahead of planned development work, with plans to mine at the Gloria Vein first, followed by the Abundancia and Martha veins. The company noted in its prepared remarks it expects the first ore to be available in early 2024 from La Preciosa, and while its growth should translate to lower unit costs, I would be surprised if the company can deliver this growth without additional share dilution with study work ongoing at the Oxide Tailings Project and mine development required at La Preciosa and very limited free cash flow generation even at current silver prices.

{kind=link}

Valuation & Technical Picture

Based on ~134 million fully diluted shares and a share price of US$0.78, Avino trades at a market cap of US$114 million. This leaves the stock trading at just $0.42/oz on a measured & indicated resource basis, which is one of the cheapest valuations sector-wide. That said, Mexico does not appear to be getting any more attractive from an investment standpoint, and while I expect the recent changes to impact developers more than current producers, I believe that much of this discount is justified given that Avino is a low-margin producer today with all of its operations in a Tier-2 ranked jurisdiction.

And while Avino should see a re-rating if can grow into a larger producer at lower costs, several Mexican producers are in similar positions with better margins, but the market hasn't rewarded them for growth. Some examples include MAG Silver ( MAG ) and SilverCrest Metals ( SILV ) which continue to trade well below 2022 levels despite significantly higher production at industry-leading costs, massively underperforming Tier-1 jurisdiction peers like Hecla Mining ( HL ) and Dolly Varden ( OTCQX:DOLLF ). And while this may just be a coincidence, the market appears to be quicker to re-rate producers in more stable jurisdictions, with most Mexican producers/developers continuing to underperform.

{kind=link}

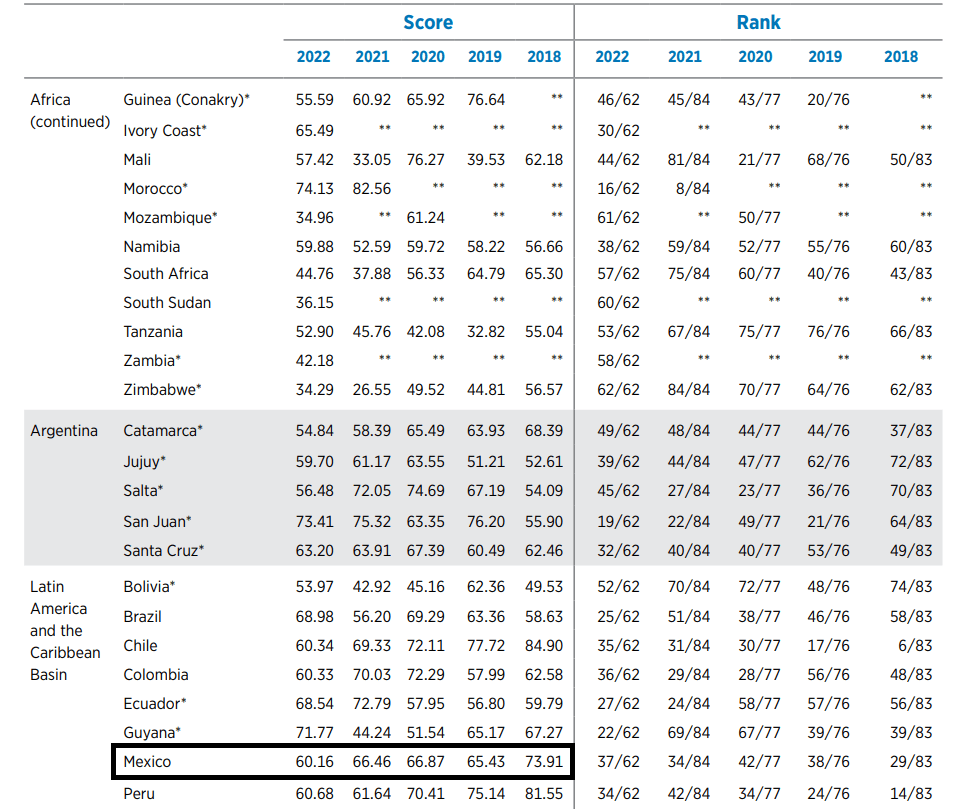

This doesn't mean that Avino won't re-rate higher if it's successful with its growth, but I prefer not to invest in stocks with 100% of their exposure to jurisdictions where the investment attractiveness is trending in the wrong direction. The caveat is if a company has a world-class project with 60%+ AISC margins. However, Avino has a much lower grade profile than its peers, a weaker balance sheet (just $2.7 million in cash at the end of Q1 2023), and Mexico's investment attractiveness rating has plunged from ~74% to ~60% or 37/62 jurisdictions vs. 29/83 jurisdictions since 2018 according to Fraser Mining's 2022 survey.

Hence, without a world-class asset that might justify the elevated risk of investing in Mexico given that producers with world-class assets often outperform their peers due to superior free cash flow generation such as Lundin Gold ( OTCQX:LUGDF ), I see ASM as a swing-trading vehicle only, not an investment.

Mexico - Investment Attractiveness Index (Fraser Institute Annual Survey)

{kind=link}

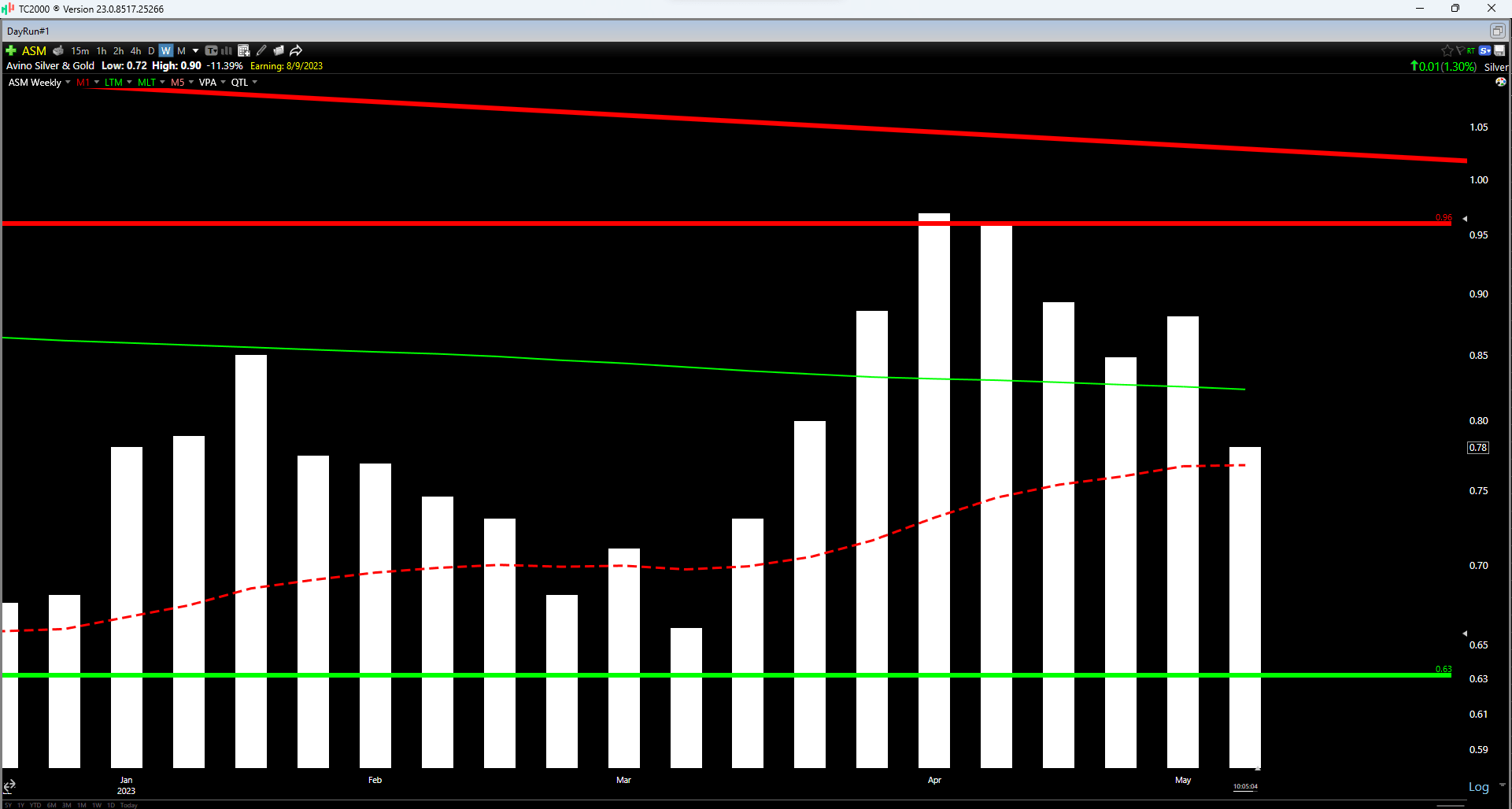

Finally, if we look at the technical picture, Avino remains in the middle portion of its support/resistance range despite its recent correction, with an updated resistance level at US$0.96, and no support until US$0.63. And given that I prefer to buy at or below support for micro-cap names, ASM would need to decline below US$0.63 to become more interesting from a technical standpoint to justify starting a new position. Obviously, I could be wrong and I may be too critical of the recent mining reforms and how they might affect investor sentiment regarding Mexican producers. Still, I think there are more attractive bets elsewhere currently in the sector, and especially when adjusting for the risk of owning a low-margin producer with 100% of its operations in Mexico.

{kind=link}

Summary

Avino Silver & Gold should have a better Q2 report with a boost to sales from the late shipment in Q1, and the Oxide Tailings PFS that's planned to be released by the end of the year should provide more clarity into the economics of this future pillar for growth. And while Avino is cheap at well below $1.00/oz on silver-equivalent resources, I see an elevated risk for investing in single-asset producers in jurisdictions that are becoming less attractive, and I believe Mexico is becoming one of those jurisdictions. So, while I would consider ASM from a trading standpoint below US$0.63, I think there are more attractive bets elsewhere currently.

For further details see:

Avino Silver & Gold Mines Q1 Earnings: A Slow Start To The Year