SPY - AVK: Getting Closer To A More Attractive Valuation

2023-05-30 18:09:45 ET

Summary

- Advent Convertible & Income Fund's discount has widened, making it more appealing, but it remains above its longer-term average.

- The fund's distribution yield is high at 12.69%, but the NAV rate is also elevated, which could be hard to earn.

- The environment for convertibles is becoming more attractive, with higher rates leading to higher yields being required when issued.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 29th, 2023.

In our previous update of Advent Convertible & Income Fund ( AVK ), I mentioned that the discount was getting quite attractive. However, I was still looking for an even larger discount. We've since seen the fund move to a larger discount, and that can make it more appealing at this time. Still, it's staying stubbornly above its longer-term average - that's even despite the added volatility we've been experiencing with bank failures and debt ceiling negotiations.

Additionally, I still believe that the fund's distribution yield is a bit too high, which could mean a cut. Historically speaking, they don't generally make many adjustments. Since the fund's launch, there has been a cut in the GFC and a raise around 2017. Those were the only two adjustments. But paying out the same distribution and actually being able to earn it for a closed-end fund are two different things.

The Basics

- 1-Year Z-score: -0.91

- Discount: -7.90%

- Distribution Yield: 12.69%

- Expense Ratio: 1.56%

- Leverage: 45.61%

- Managed Assets: $765.163 million

- Structure: Perpetual

AVK's investment objective is "to provide total return, through a combination of capital appreciation and current income." They will attempt to achieve this by "investing at least 80% of its managed assets in a diversified portfolio of convertibles securities and non-convertible income securities." They will also invest "at least 30% of its managed assets in convertible securities and up to 70% of its managed assets in lower-grade, non-convertible income securities, although the portion of the Fund's assets invested in convertible securities and non-convertible income securities will vary from time to time."

The fund is highly leveraged. When including leverage expenses, the fund's last expense ratio was reported at 3.54% in its annual report for the year 2022. This was an increase in the fund's expense ratio that came from both an increase in borrowings and the rate of borrowings increasing. Seeing leverage increase in 2022 was a bit unusual because most other funds were deleveraging.

In total, they list leverage outstanding at $349 million. This is comprised of sources of both a credit facility and reverse repurchase agreements. At the end of 2022, here is what the interest rates and maturities looked like for their reverse repo agreements.

{kind=link}

Here is a look at the borrowing costs of their credit facility.

{kind=link}

Interestingly, credit facilities are generally overwhelmingly based on a variable rate. AVK has most of the borrowings here tied up in fixed rates. That would have helped hedge them against the full brunt of higher rates.

Performance - Discount Needs To Go A Bit Wider Yet

Since our prior update , the fund has performed quite poorly as well. However, this isn't really my main concern as it's performing about as expected.

AVK Performance Since Prior Update (Seeking Alpha)

Some of this was due to discount widening, but also due to portfolio positioning. While the broader equity 'market' seems to be enjoying a strong rebound from last year, most other investments are not. Our last update of AVK was at the end of January 2023. To start off the year, the participation in upside was more widespread. Since then, it's basically come down to a handful of mega-cap tech names driving up the results we are seeing.

This can be better represented by looking at the YTD performance of various benchmarks to provide some context. As we can see, the SPDR S&P 500 ( SPY ) is the lone soldier powering higher to the upside. We see a more sobering picture if we look at the equal-weighted version of SPY through Invesco S&P 500 Equal Weight ETF ( RSP ).

Ycharts

In fact, that's mostly where fixed-income investments and preferreds are, much closer to the performance of RSP than SPY. One of the exceptions here would be the iShares Convertible Bond ETF ( ICVT ) is making a valiant attempt at some upside movement. It's worth noting that two convertible issues from Palo Alto ( PANW ) make up the first and second largest position of ICVT. With a YTD performance on the common at nearly 53%, that's certainly helped provide some upside for ICVT. AVK carried a small position in PANW's 0.375% convertible at the end of January . It's not known if the fund still has that position at this time.

That's helped out AVK, which carries most of its exposure to convertibles. It also mixes in a healthy dose of high yield, followed by a more negligible sleeve of equities. As we can see, it was right about when that last AVK update was published that the declines began. It wasn't only AVK that experienced this but ICVT and HYG during this period too.

Ycharts

A higher expense ratio, portfolio positioning, and leverage would have all been reasons that AVK's performance was below ICVT and HYG on a YTD basis. However, that leverage during the initial January 2023 rebound also shows the upside of being leveraged.

The positioning of AVK makes it a bit more similar to the Calamos twins, Calamos Convertible & High Income Fund ( CHY ) and Calamos Convertible Opportunities & Income Fund ( CHI ). AVK has performed materially worse over the last decade relative to these two funds. The performance here can provide better context than the ETFs above, as these are comparing actively managed and leveraged CEFs.

Ycharts

The fund's discount is now a bit deeper than it was when we last covered the fund. Still, it's ultimately above the fund's longer-term average, and that can mean continuing to be patient for a better opportunity isn't a bad idea.

Ycharts

A double-digit discount isn't too uncommon for this fund, either. We were just at those levels when the broader market bottomed in October. Then right near the end of 2022 and to start off 2023, the fund was also at a double-digit discount. That's why on a YTD basis, the fund's share price performance has been greater than the NAV. That chipped away at what was a deeper discount for the fund to start off the year.

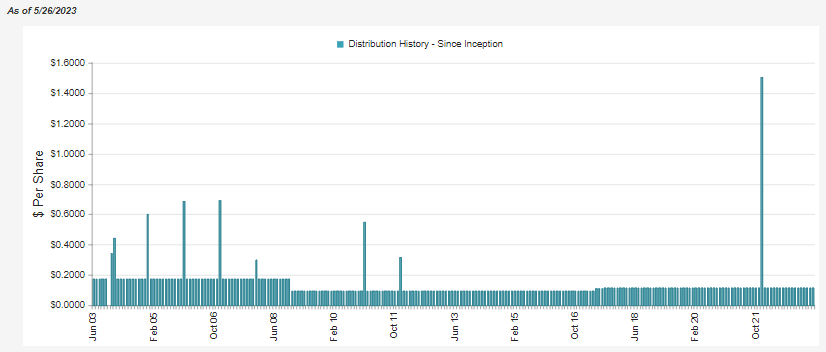

Distribution - Elevated Distribution Rate

The fund's distribution rate comes in at an attractive 12.69%. Thanks to the fund's large discount, the fund actually only has to earn 11.69% to cover the payout to shareholders. That's the NAV distribution yield. As I mentioned, the fund hasn't made many adjustments historically, but the current NAV yield is still fairly elevated.

{kind=link}

It's elevated primarily due to taking such a hit last year. So a swift recovery in the underlying portfolio could see the NAV yield come back down, indicating a better chance of maintaining the rate over the long term.

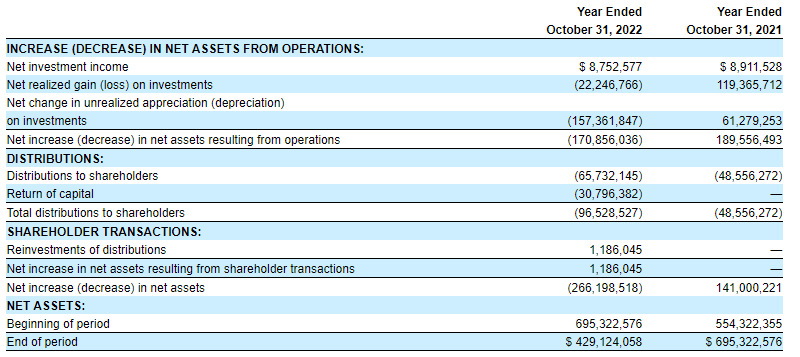

With a net investment income coverage of only just over 9% in the prior fiscal year, they will require significant capital gains to fund their distribution. Therefore, that further adds pressure to maintain the distribution. Capital gains can be more irregular, and this highlights why an appreciating fund in recovery and seeing that NAV yield go down would indicate it's starting to cover the payout.

{kind=link}

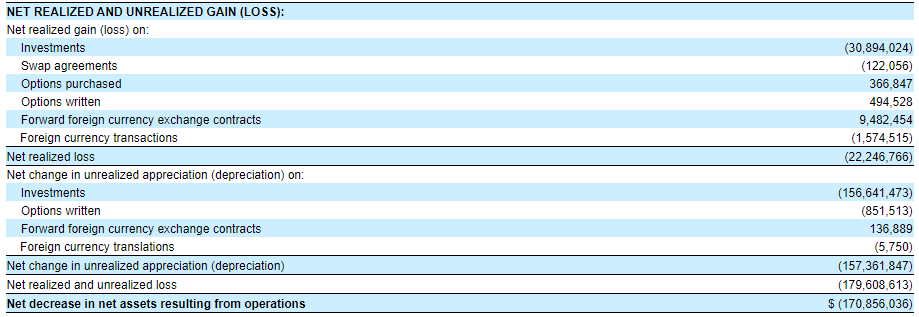

However, they have a couple of tricks to help maintain the distribution - even if their underlying portfolio is falling in value. This is through various derivative contracts. If successful, and it was last year, that helps cover the payout to investors.

The options written and options purchased are ways to generate gains no matter the market direction. The options purchased are a bit harder to make money on because they have to be right in the direction at a specific time. With writing options, you have some leeway to be incorrect.

{kind=link}

Another contribution to the fund's realized gains last year to help stop some of the declines was in their forward foreign currency exchange contracts.

Overall, these derivatives couldn't even come close to reversing what the underlying portfolio lost on a realized and unrealized basis. However, the losses would have been even worse if not for these gains.

On a positive note, Calamos recently noted that convertible bonds are becoming more attractive. Through most of the last few years, really since rates went to zero, companies were getting away with offering 0% rates on their convertible debt with an average conversion premium of 35%. More recently, Calamos noted that the "typical coupon on convertibles now exceeds 4% with conversion premium below 25%."

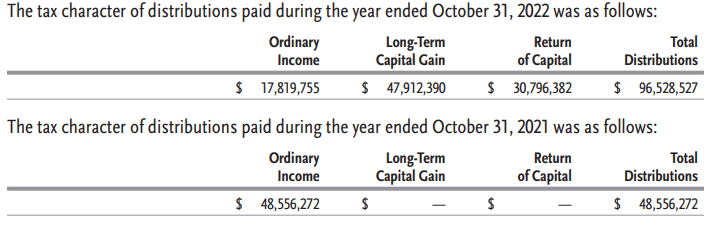

For tax-sensitive investors, holding this fund in a tax-sheltered account could be more appropriate due to the unpredictability of the distribution characterization.

{kind=link}

AVK's Portfolio

Trying to keep up with the fund's portfolio can be more difficult. CEFs don't generally have the most updated reporting. Then when a fund has a high turnover, that means there are generally more changes going on under the hood.

For AVK, the fund last reported a turnover rate of 186% in fiscal 2022. That actually wasn't the highest turnover, as fiscal 2020 had a reported turnover rate of 242%. In the last five years, the lowest turnover was in 2018, at 121%. Suffice it to say the managers in this fund are quite active.

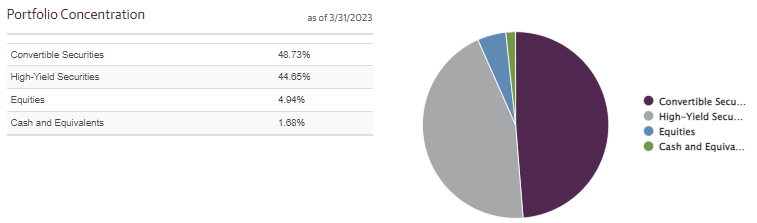

At the end of March, convertibles were the largest allocation of the fund. A sleeve of high-yield bonds closely followed this up. The split between these two allocations is worth pointing out as the spread was wider previously. Near the end of 2022, the fund carried around 52.5% in convertibles and only 38.33% in high yield.

{kind=link}

Another potential positive catalyst that Calamos noted in their article about convertibles becoming more attractive now is the likely issuers with debt coming due. Convertibles are still a relatively attractive way for companies to issue debt because it's generally at a lower coupon compared to just straight debt offerings. The convertible feature might mean future dilution, but having this feature that's the reason for relatively lower coupons.

With rates rising, Calamos noted that there was a "significant increase in convertibles issued by investment-grade companies." These higher-quality companies can issue convertibles at a lower coupon, so they can avoid borrowing costs climbing too rapidly with the now higher rate environment.

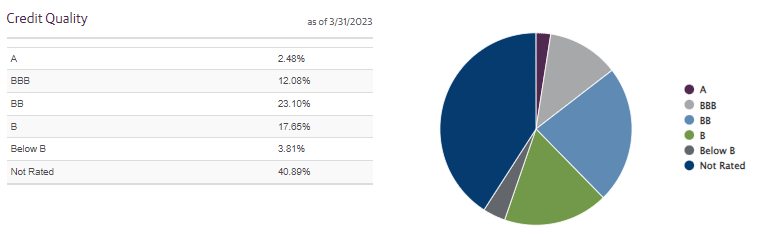

With AVK's allocation to high-yield bonds specifically, the fund will likely carry a material allocation to below-investment-grade debt. The not rated portion of their portfolio is significant, but this is generally the case with convertible debt offerings. When convertibles are issued, they frequently forgo the time and expense of getting rated.

{kind=link}

In fact, the majority of AVK's portfolio is frequently invested in 144A securities. At the end of their last fiscal year, it was 70.7% of their total net assets. 144A securities are those that are privately placed to qualified institutional buyers. This includes not only the fund's convertible debt but also the fund's high-yield bonds.

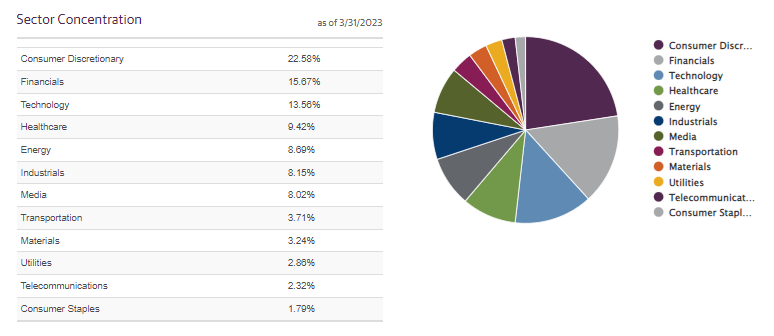

Going back to the fund's underperformance relative to the Calamos twins, it would appear portfolio positioning played quite a role - as would be pretty much expected. AVK seems to emphasize sectors outside of tech, while Calamos funds favoring tech positions. Though in more recent updates for Calamos , we've seen a notable shift in getting tech weightings back to be more in line with the other sector exposures.

{kind=link}

Like peers, AVK doesn't get too concentrated in particular positions. The top ten are only around 11% of the portfolio.

AVK Top Ten Holdings (Guggenheim)

They carry Ford ( F ) at a fairly material weighting relative to the rest of their portfolio, but for the most part, allocations are spread quite thinly. CEFConnect lists the number of holdings at 363. The Ford weighting is also spread across multiple positions, having some convertible but also bonds issued by Ford Motor.

Conclusion

AVK is an interesting convertible and high-yield bond fund. The discount is heading in the right direction. Still, it's not at too attractive of a price yet, even as the fund's discount has started to widen out once again. I'd still be looking to patiently wait for a double-digit discount before getting too excited. The fund's elevated amount of leverage that they employ should be watched closely. This definitely isn't for a risk-averse investor.

Convertibles have been performing fairly well this year compared to other debt investments. However, convertibles and most other asset classes are off from the highs we saw earlier in the year. The lackluster performance of AVK against something like the S&P 500 might be noted, but if it weren't for a handful of mega-cap tech names, not even the S&P 500 would be having too hot of a year. That can be reflected by RSP, which shows a flat YTD performance after an initial jump higher in January.

Simply said, AVK is performing about as expected. Additionally, a comparison to equities, while AVK is a convertible and high-yield fund, isn't necessarily the most appropriate anyway.

For further details see:

AVK: Getting Closer To A More Attractive Valuation