BLZE - Backblaze Guides To Lower Revenue Growth Amid Worsening Operating Losses

2023-05-24 11:00:00 ET

Summary

- Backblaze recently reported its Q1 2023 financial results.

- The firm provides an array of storage and recovery solutions worldwide.

- BLZE has guided to lower revenue growth rate and is generating increasing operating losses.

- My outlook on BLZE stock is Bearish [Sell].

A Quick Take On Backblaze

Backblaze ( BLZE ) went public in November 2021, raising approximately $100 million in gross proceeds from an IPO priced at $16.00 per share.

The firm provides cloud-based storage and recovery software to businesses and individuals.

I previously wrote about Backblaze here .

However, given the company's lower forward revenue growth outlook and its increasing operating losses, I’m not optimistic about Backblaze, so my outlook is Bearish [Sell].

Backblaze Overview

San Mateo, California-based Backblaze was founded to develop a cloud-based SaaS storage service suite for businesses and consumers wishing to easily back up and store their critical data.

Management is headed by co-founder, Chairperson and CEO Gleb Budman, who has been with the firm since its inception and was previously in various senior positions at SonicWall, MailFrontier and Kendara.

The company’s primary offerings include:

-

B2 Cloud Storage

-

Computer Backup

The firm seeks customers primarily through online marketing, social media, partnerships and word of mouth.

BLZE operates a self-serve website that enables users to sign up for a free trial and convert to a paid subscription.

Backblaze’s Market & Competition

According to a 2023 market research report by MarketsAndMarkets, the global market for cloud storage services was an estimated $78.6 billion in 2022 and is forecast to reach $184 billion by 2027.

This represents a forecast CAGR of 18.5% from 2022 to 2027.

The main drivers for this expected growth are the growing demand for enterprises for ever larger amounts of data and a rising number of remote-located employees and contractors needing access to relevant data stores.

Also, a key challenge for the industry is to effectively defend against security threats and improve data privacy for corporate and personal data.

Major competitive or other industry participants include:

-

Amazon

-

Alphabet

-

Microsoft

-

Dell EMC

-

iDrive

-

pCloud

-

Dropbox

-

Icedrive

-

NordLocker

-

Others

Backblaze’s Recent Financial Trends

-

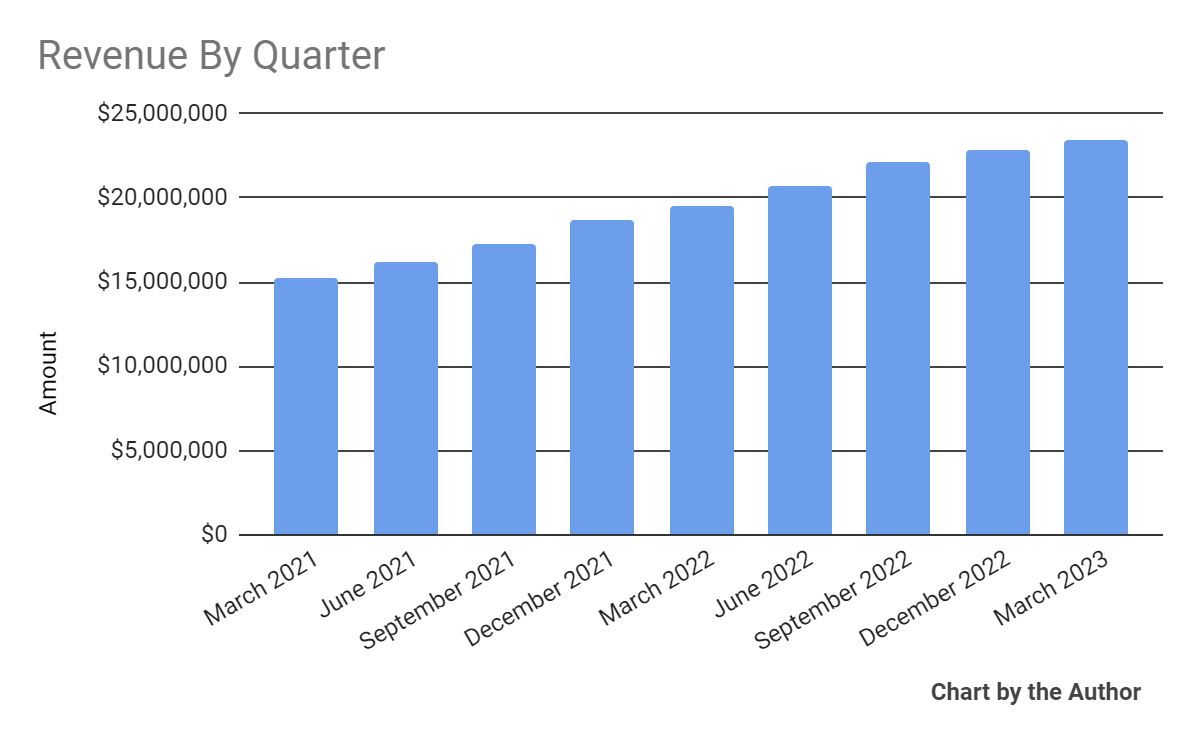

Total revenue by quarter has grown steadily, as the chart shows below:

{kind=link}

-

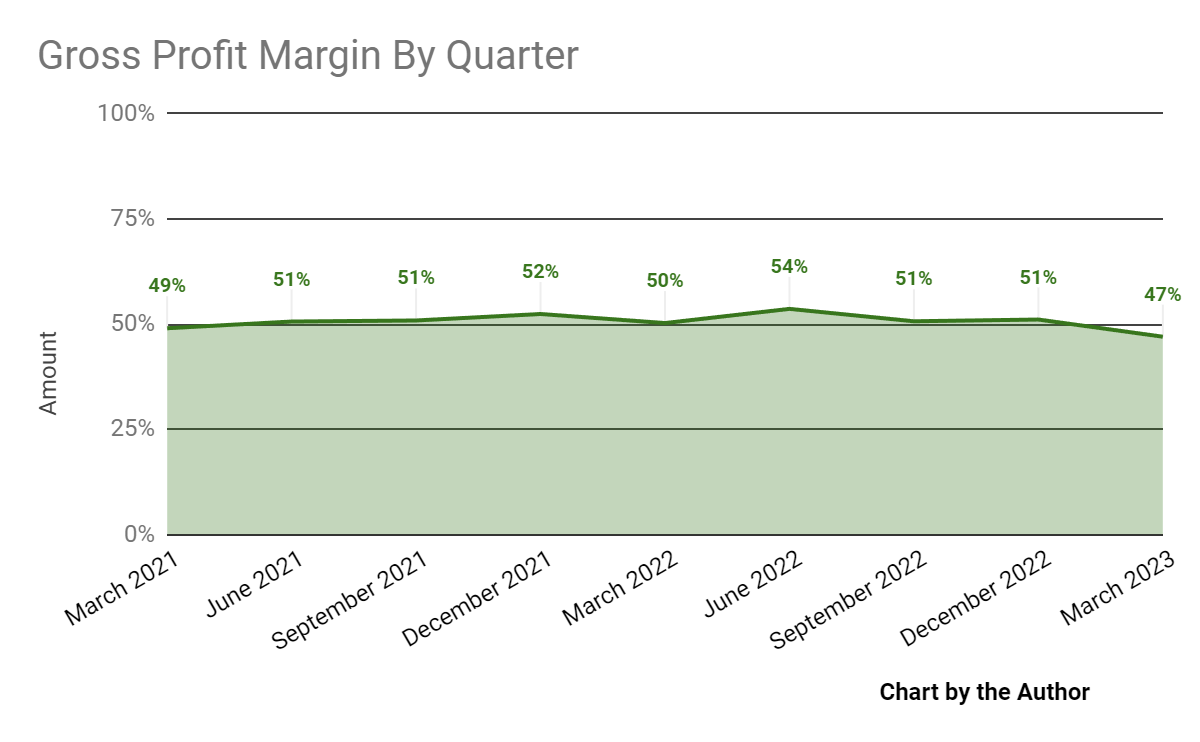

Gross profit margin by quarter has dropped in recent quarters:

Gross Profit Margin (Seeking Alpha)

{kind=link}

-

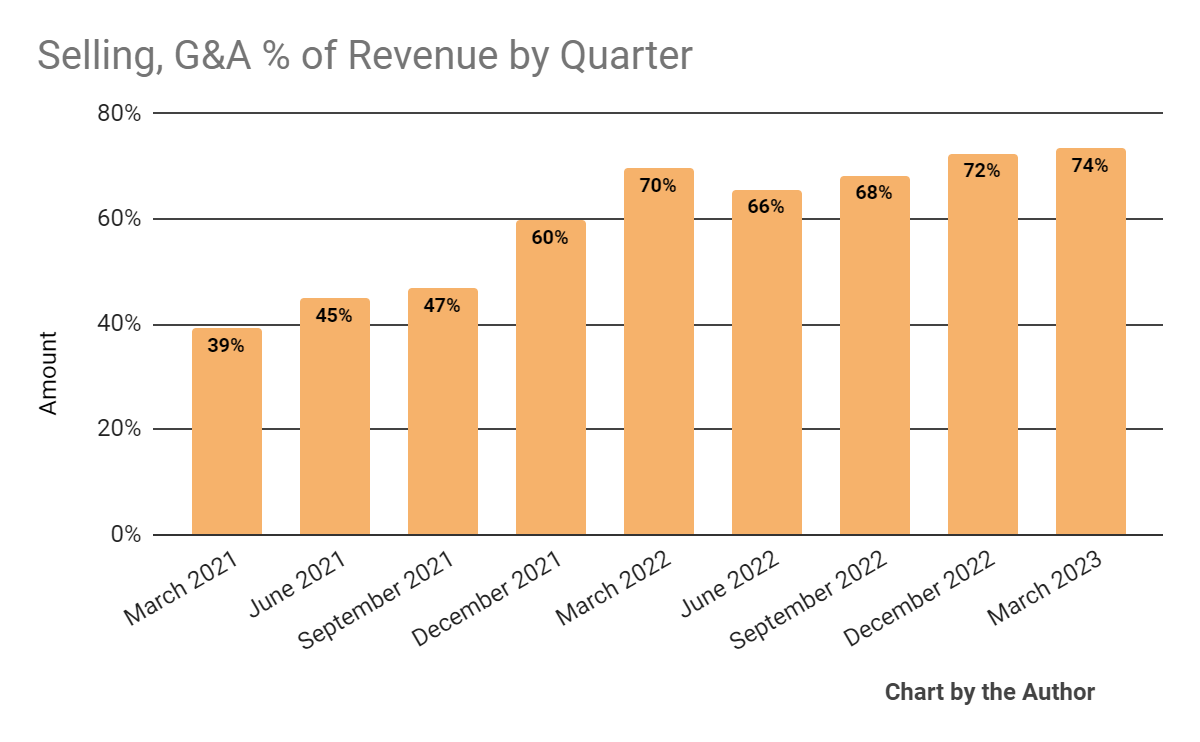

Selling, G&A expenses as a percentage of total revenue by quarter have risen in recent quarters, indicating a rising cost structure for generating incremental revenue:

Selling, G&A % Of Revenue (Seeking Alpha)

{kind=link}

-

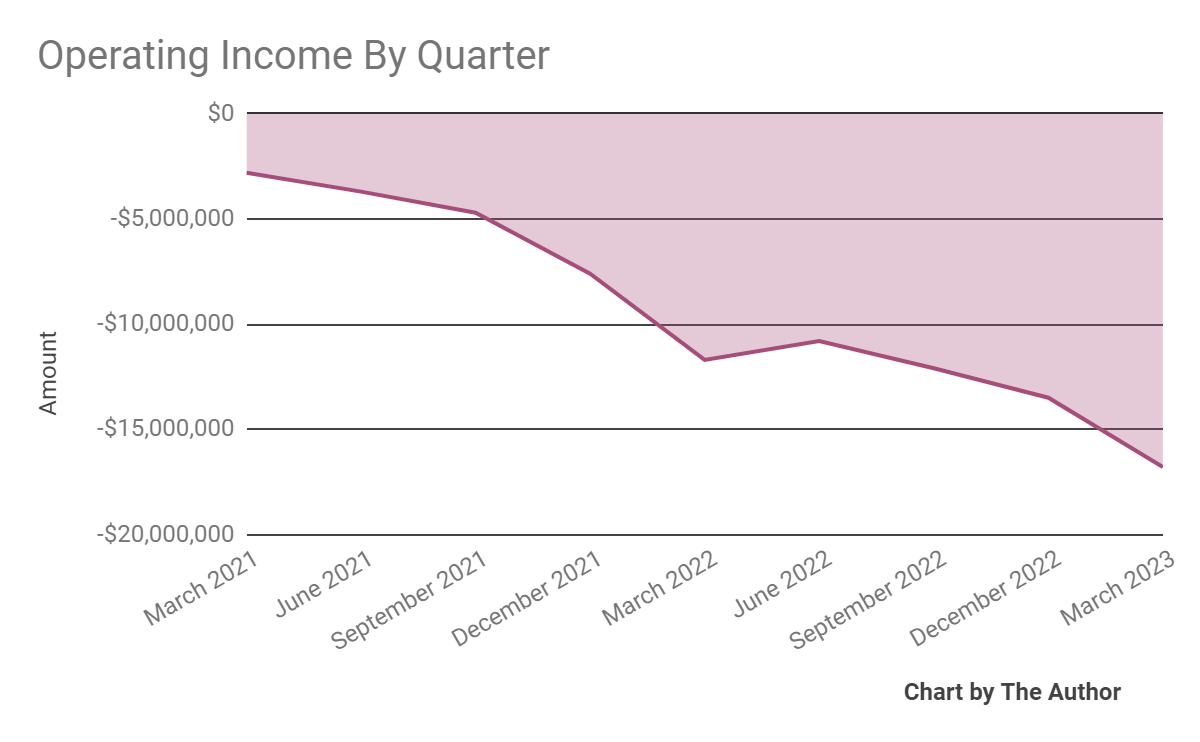

Operating losses by quarter have worsened, as shown below:

Operating Income (Seeking Alpha)

{kind=link}

-

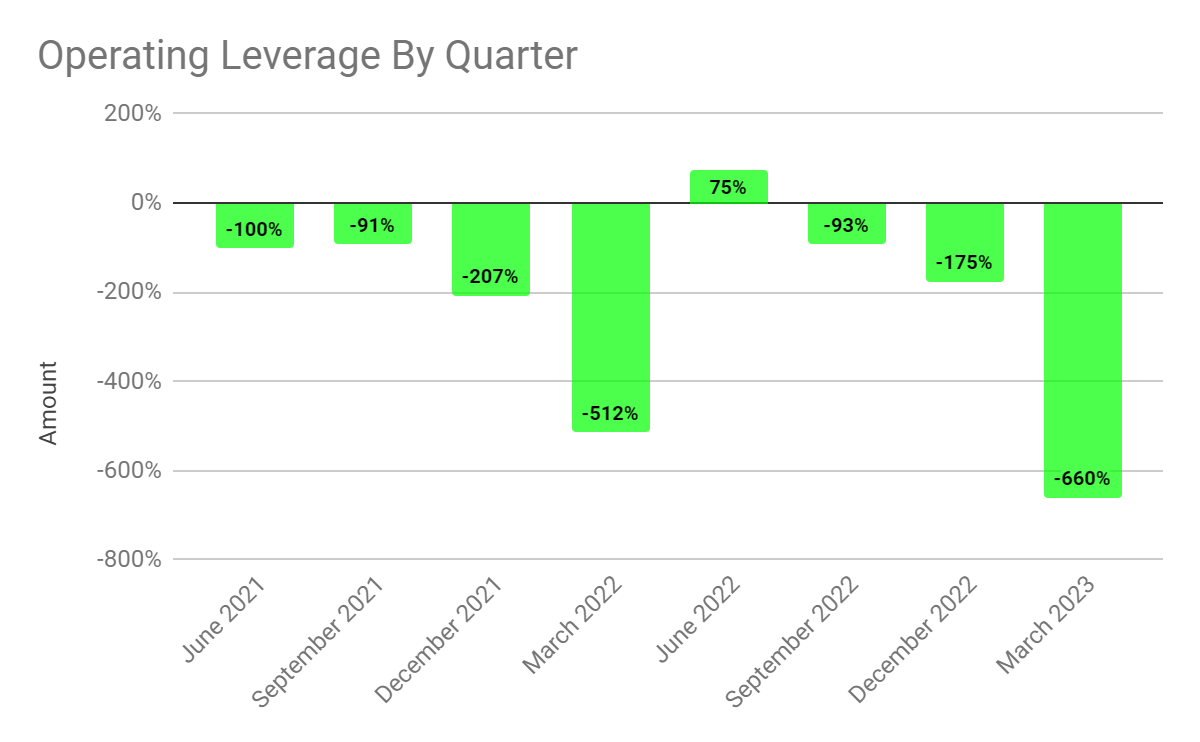

Operating leverage by quarter has also deteriorated recently:

Operating Leverage (Seeking Alpha)

{kind=link}

-

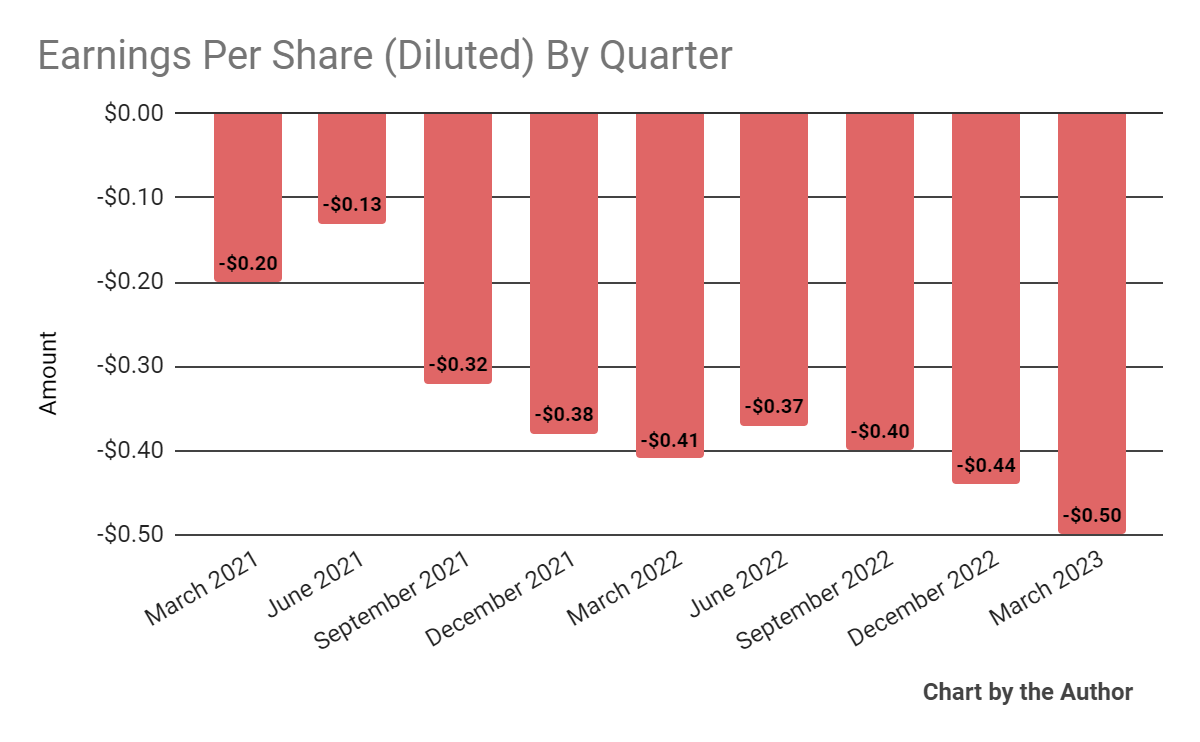

Earnings per share (Diluted) have worsened markedly recently:

Earnings Per Share (Seeking Alpha)

{kind=link}

(All data in the above charts is GAAP)

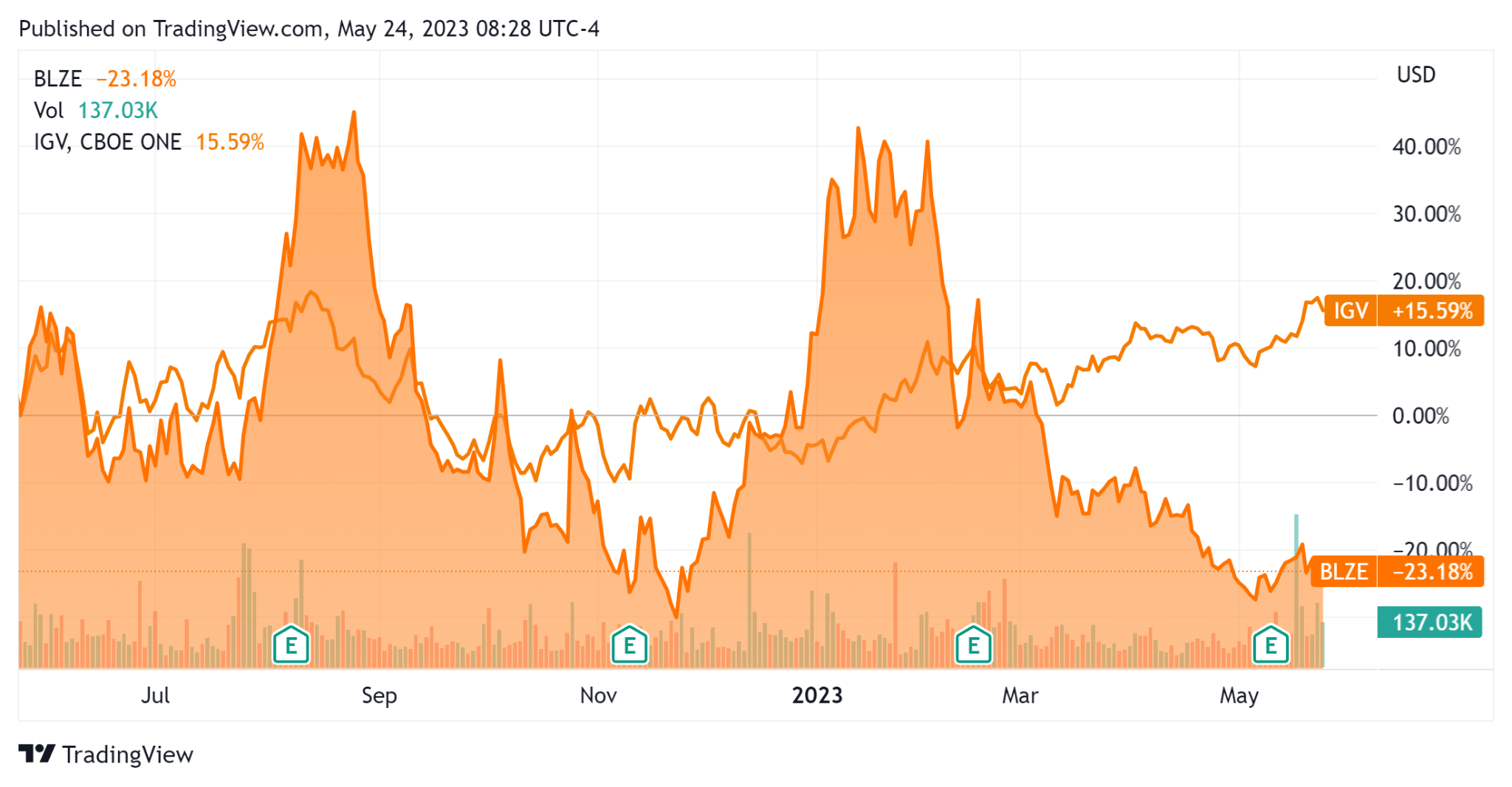

In the past 12 months, BLZE’s stock price has fallen 23.18% during a volatile year vs. that of the iShares Expanded Tech-Software Sector ETF’s ( IGV ) rise of 15.59%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For the balance sheet, the firm ended the quarter with $49.6 million in cash, equivalents and short-term investments and $7.3 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $8.2 million, of which capital expenditures accounted for $9.9 million. The company paid $19.0 million in stock-based compensation in the last four quarters, the highest result in the past eleven-quarter period.

Valuation And Other Metrics For Backblaze

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.6 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.6 |

| Revenue Growth Rate |

| 24.3% |

| Net Income Margin |

| -62.9% |

| EBITDA % |

| -38.6% |

| Market Capitalization |

| $148,460,000 |

| Enterprise Value |

| $144,420,000 |

| Operating Cash Flow |

| -$18,070,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.71 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

Backblaze’s most recent Rule of 40 calculation was negative (14.3%) as of Q1 2023’s results, so the firm has performed poorly in this regard, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| 24.3% |

| EBITDA % |

| -38.6% |

| Total |

| -14.3% |

(Source - Seeking Alpha)

Commentary On Backblaze

In its last earnings call (Source - Seeking Alpha), covering Q1 2023’s results, management highlighted its goal of approaching ‘adjusted EBITDA breakeven in Q4 [2023?].’

Management noted the economic environment headwinds the company faces in the short term and how the company saves customers money by offering a lower-cost service than competitors.

Leadership is seeking to optimize its self-service model to reduce customer acquisition costs while leveraging partnerships to drive customer acquisition.

The company’s net dollar retention rate was 111%, indicating reasonably good product/market fit and sales & marketing efficiency.

Total revenue for Q1 2023 rose 20.0% year-over-year and gross profit margin dropped 3.2 percentage points.

Selling, G&A expenses as a percentage of revenue rose 3.8 percentage points year-over-year, indicating reduced operating efficiency, while operating losses increased a substantial 43.6% as operating leverage worsened dramatically.

Looking ahead, management guided full-year 2023 revenue to be $100 million at the midpoint of the range, or about a 17% growth rate.

This expected growth rate, if achieved, would be significantly lower than 2022’s growth of 26.2% over 2021, so the firm's growth rate is slowing markedly.

The company's financial position is moderately healthy, with ample liquidity, almost no debt and a small amount of positive cash flow.

Regarding valuation, the market is valuing BLZE at an EV/Sales multiple of around 1.6x.

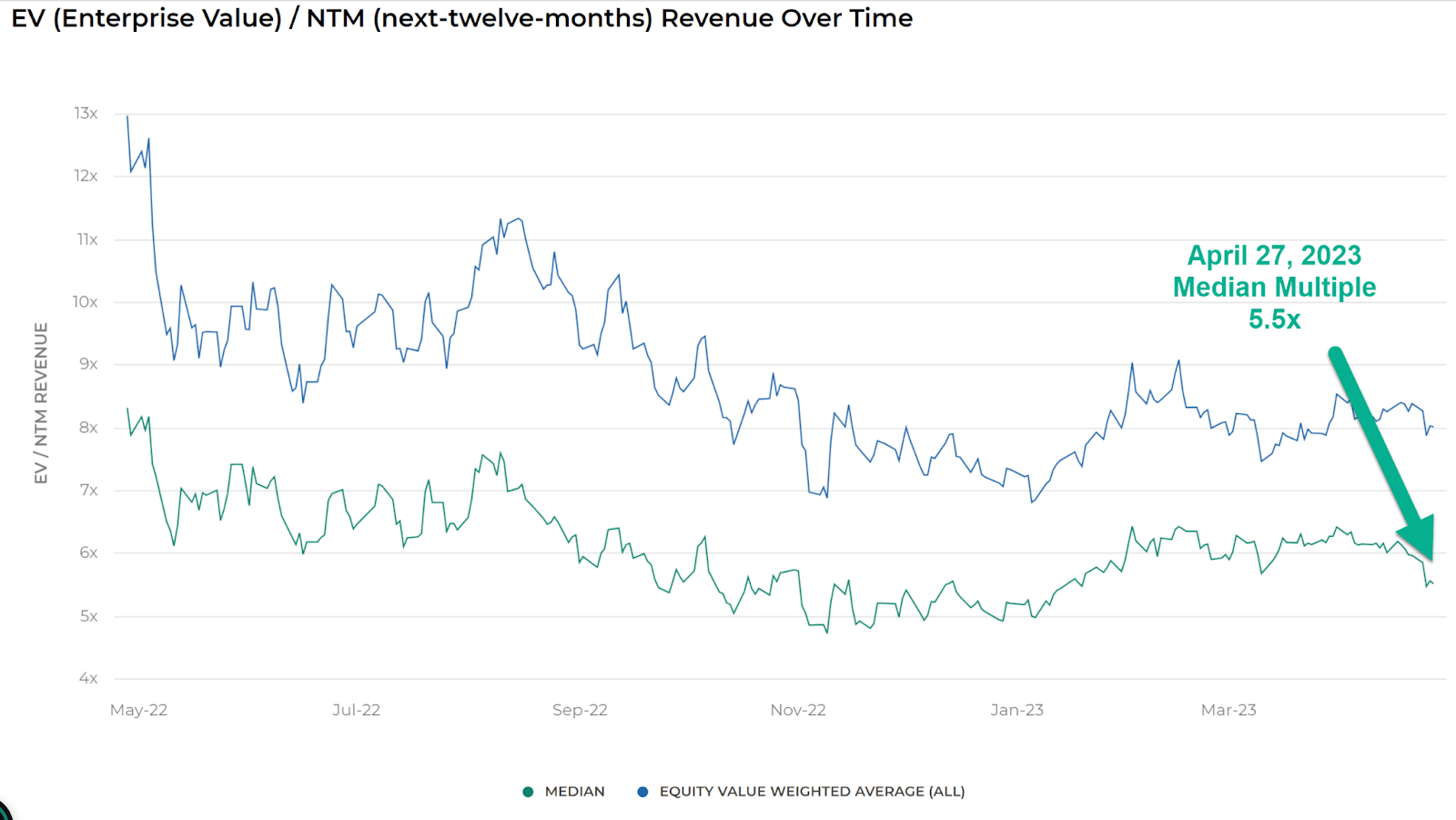

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital)

{kind=link}

So, by comparison, BLZE is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

Risks to the company’s outlook include a macroeconomic slowdown, reduced credit availability which may affect customer/prospect spending plans and lengthening sales cycles.

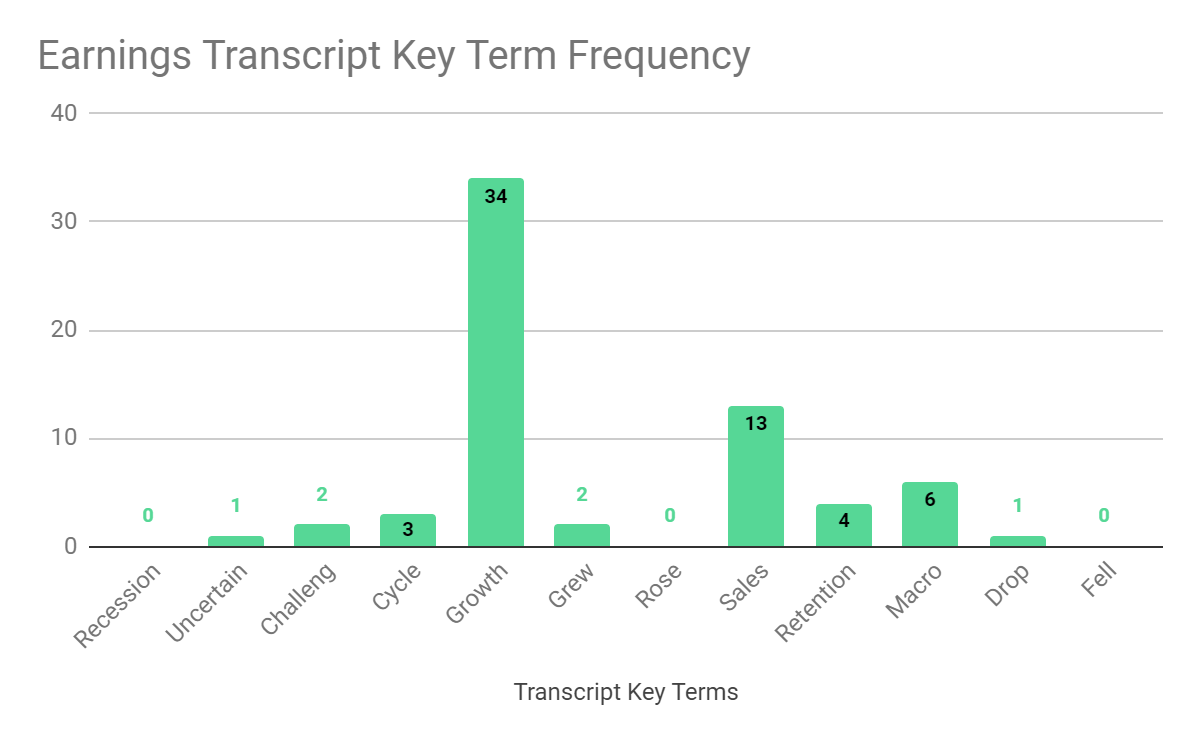

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

{kind=link}

I’m most interested in the frequency of potentially negative terms, so management cited ‘Uncertain’ once, ‘Challeng[es][ing]’ two times, ‘Macro’ six times and ‘Drop’ once.

The negative terms refer to the uncertain macro environment the company and its customers and prospects are facing.

Management believes its cost-effective cloud backup and recovery services will be in demand, even if the macroeconomic environment worsens, as prospects move away from more expensive solutions.

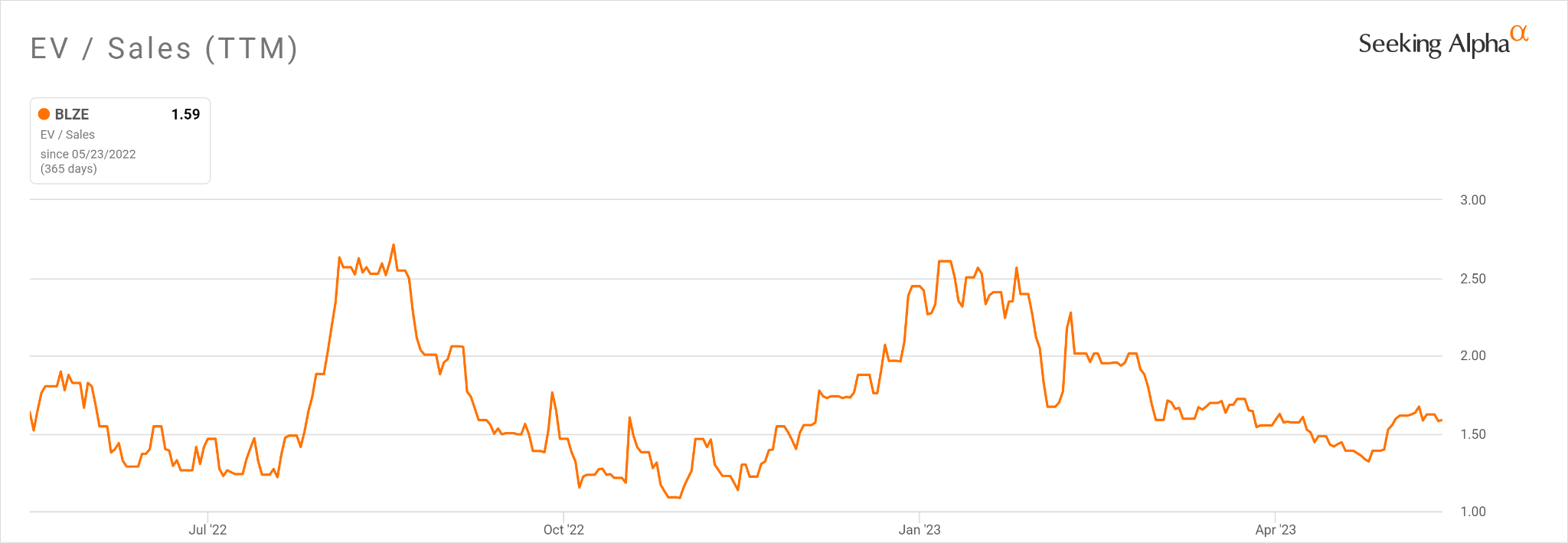

In the past twelve months, the firm's EV/Sales valuation multiple has bounced around with no net change, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

{kind=link}

A potential upside catalyst to the stock could include a cost-of-capital environment that is more favorable for software companies that are generating operating losses.

However, given the company's lower forward revenue growth outlook and its increasing operating losses, I’m not optimistic for Backblaze, so my outlook is Bearish [Sell].

For further details see:

Backblaze Guides To Lower Revenue Growth Amid Worsening Operating Losses