FLJP - Bank of Japan Policy Normalization Comes Slowly Under New Leadership

2023-04-25 10:56:14 ET

Summary

- The Bank of Japan has been alone among the major developed country central banks in continuing Quantitative Easing despite above target inflation.

- New Governor Kazuo Ueda is to lead his first BOJ policy meeting on April 28th under pressure to make changes to monetary policy.

- High inflation, a weak yen, poor JGB market liquidity and wide global yield differentials all suggest that a change is warranted from monetary policies implemented during a different era.

- According to Reuters 89% of polled economists predict that the BOJ won't make a policy change at the upcoming meeting.

Haruhiko Kuroda recently stepped down after serving for ten years as the Governor of the Bank of Japan (BOJ) Kuroda was tasked with eliminating the deflationary environment he faced when he began his management of the central bank.

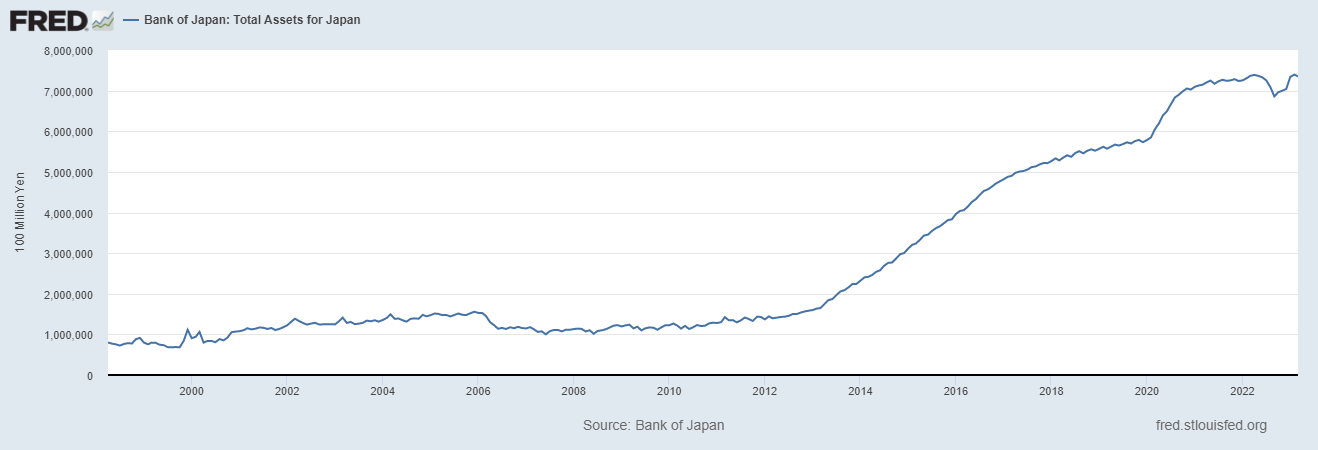

Japan was the first adopter of Quantitative Easing (QE,) having begun the program in 1999, but Kuroda was instrumental in kicking it into a higher gear. Under his leadership the BOJ balance sheet quadrupled to 740 trillion yen, mainly through heavy buying of Japanese Government Bonds (JGBs)

Bank of Japan Total Assets Chart

{kind=link}

Kuroda was known for taking rates negative in 2016 and soon thereafter implementing the Yield Curve Control Policy ((YCC)). YCC was designed to stabilize long rates around zero percent with short rates remaining negative.

The strategy was to bring inflation up to the long term goal of 2%.

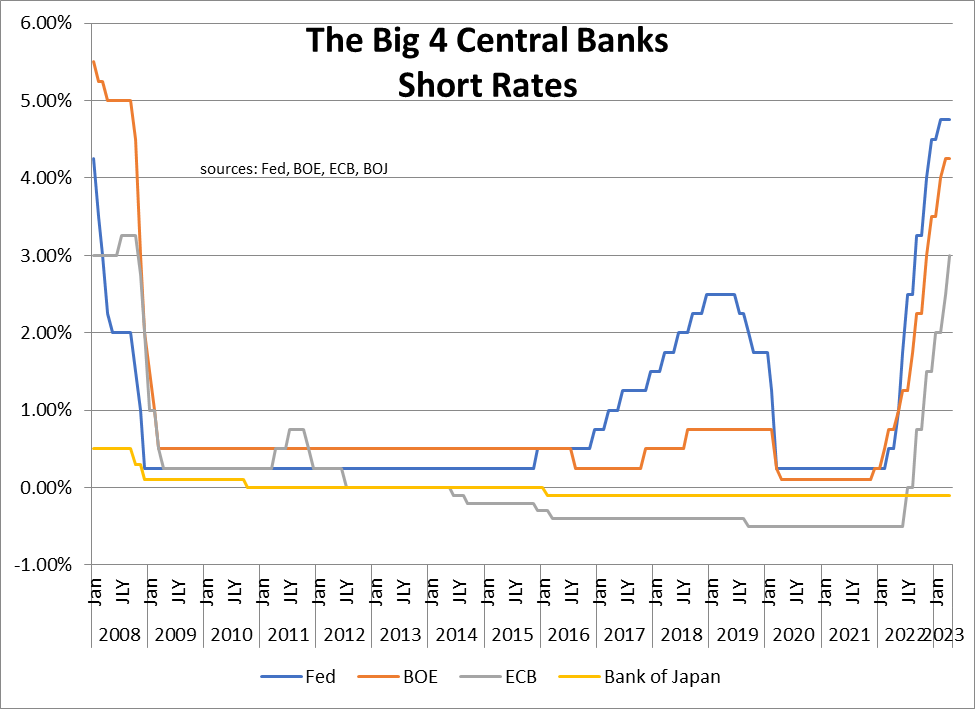

Like the economies of the other major developed countries, inflation spiked above the 2% target beginning last year. But unlike the other countries which began reversing their QE policies of the prior decade by raising interest rates aggressively and implementing Quantitative Tightening, Kuroda was determined to maintain an easy monetary policy.

{kind=link}

This policy decision has become controversial, as the yield gap between the BOJ and the other major central banks has widened dramatically.

Kuroda’s replacement, Kazuo Ueda, takes over at a crucial time, with pressure from many quarters to normalize policy. Ueda chairs his first rate review meeting later this week, and all indications suggest that during his first opportunity for change, he will do nothing.

According to Reuters, 89% of economists polled say there will be no policy change at the upcoming April 28 th meeting.

Ueda has suggested that he will undertake a comprehensive assessment of the BOJ’s monetary moves since 1999. This review will help him understand how the unconventional policy decisions over the past twenty-five years have worked. Baby steps.

Inflation

The main driver of global monetary policy tightening has been the surge in inflation as a result of the easy money policies of the past. Japan has not been immune from this inflation resurgence.

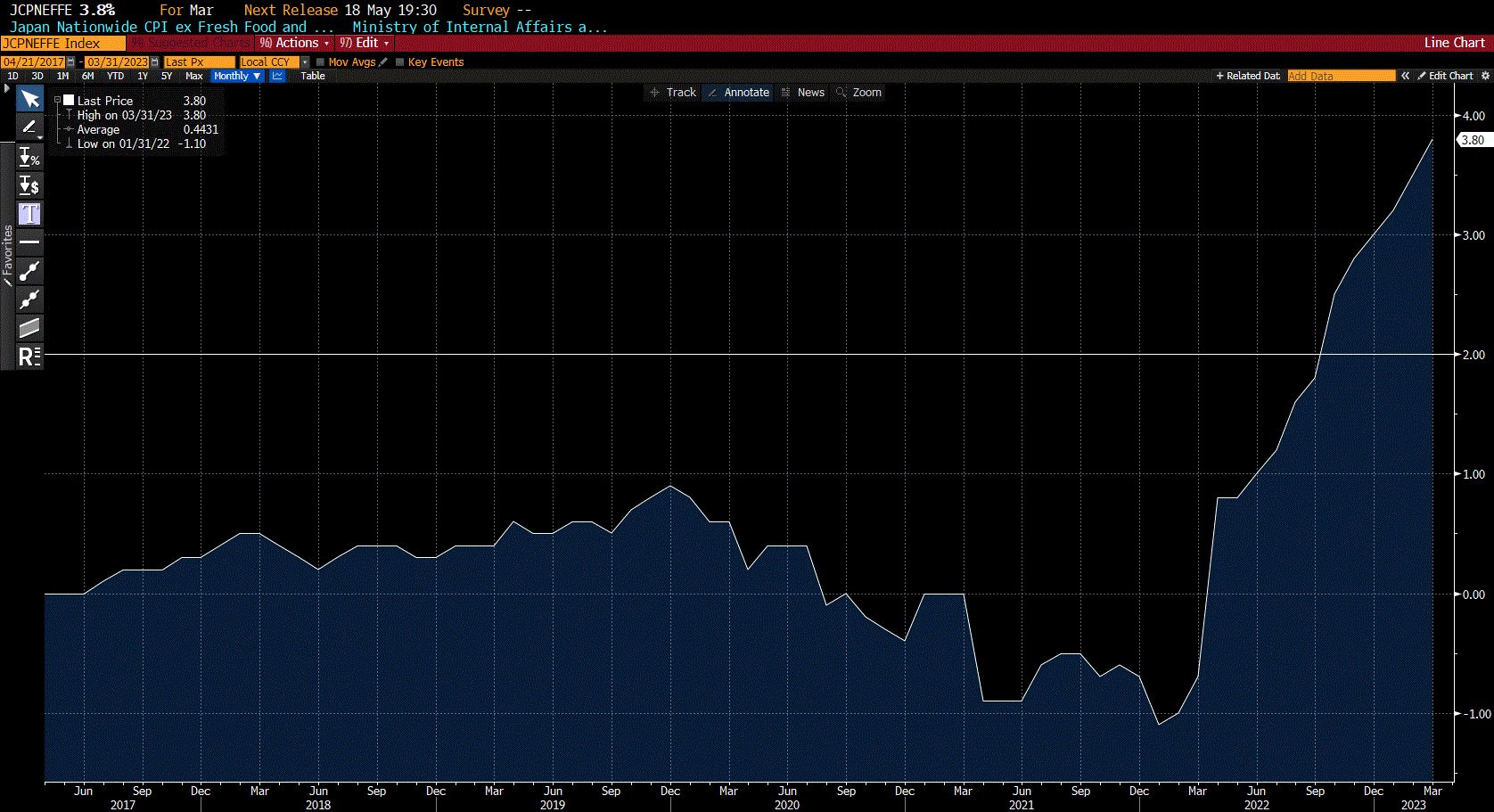

The most recent headline CPI for March came in at 3.2% y/y. While this is down from the January peak of 4.3% y/y, it is still above the target rate of 2%.

Scrutinizing the numbers more thoroughly, the closely watched Core Core CPI continues to rise. The Core Core rate measures CPI excluding the volatile components of fresh food and energy. This rate climbed to 3.8% y/y in March, its highest level in over forty years.

Core Core CPI Chart

{kind=link}

This week’s policy meeting will provide BOJ’s inflation forecasts.

Ueda has commented that “The BOJ’s forecasts of trend inflation for half a year, one year and one-and-a-half years ahead must be quite strong and close to 2%. We also need to judge that the likelihood of the forecasts materializing is high.”

Controlling the Yield Curve

When YCC was implemented, Japan was in a deflationary period and 0.0% long interest rates were appropriate. Since then, however, inflation has increased significantly and there has been substantial pressure to alter the policy.

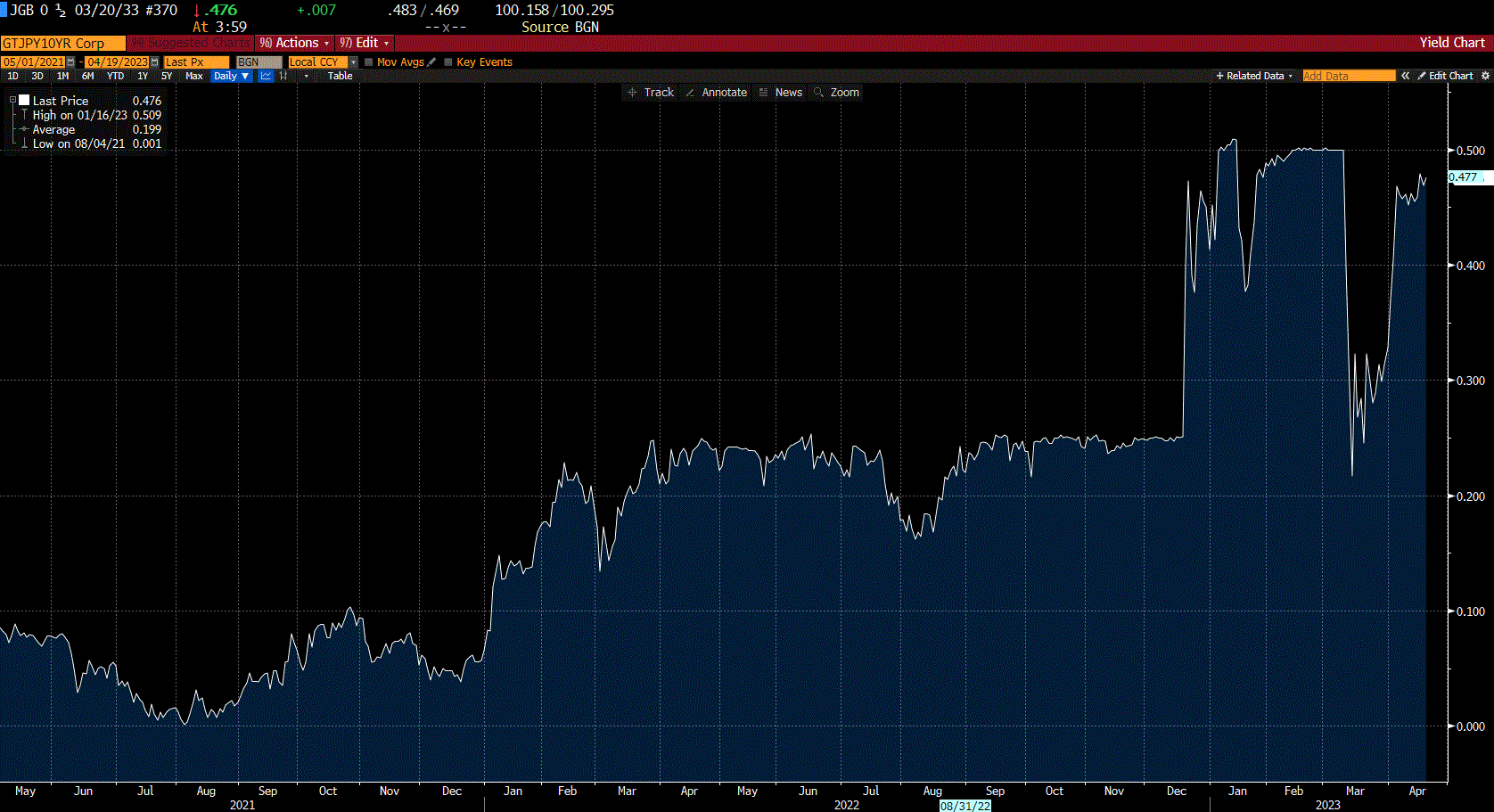

Part of the YCC policy was that the BOJ committed to buy as many JGBs as necessary to keep the 10-year yield near zero.

As pressure mounted the BOJ modified their policy. First, in 2018 they created a band of +/- 20 basis points around 0.0% on the 10-year yield. Then in 2021 the band was widened to +/- 25 basis points. Finally, in a surprise move last December Kuroda adjusted the band again by doubling it to +/- 50 basis points.

As can be seen in the yield chart of the 10-yr JGB below, at each change market speculators pushed the yield to the top end of the band.

10-year JGB Yield Chart

{kind=link}

Kuroda rightly noticed that the functioning of the yield curve has been impaired by YCC. YCC is committed to only 10-yr JGBs, consequently yields at other maturities move more freely. With upward pressure across the entire yield curve, it has attained an artificial shape with a kink at the suppressed 10-year maturity.

Part of the fine-tuning with December’s announcement was to try to smooth the curve out. Unfortunately, it didn’t work.

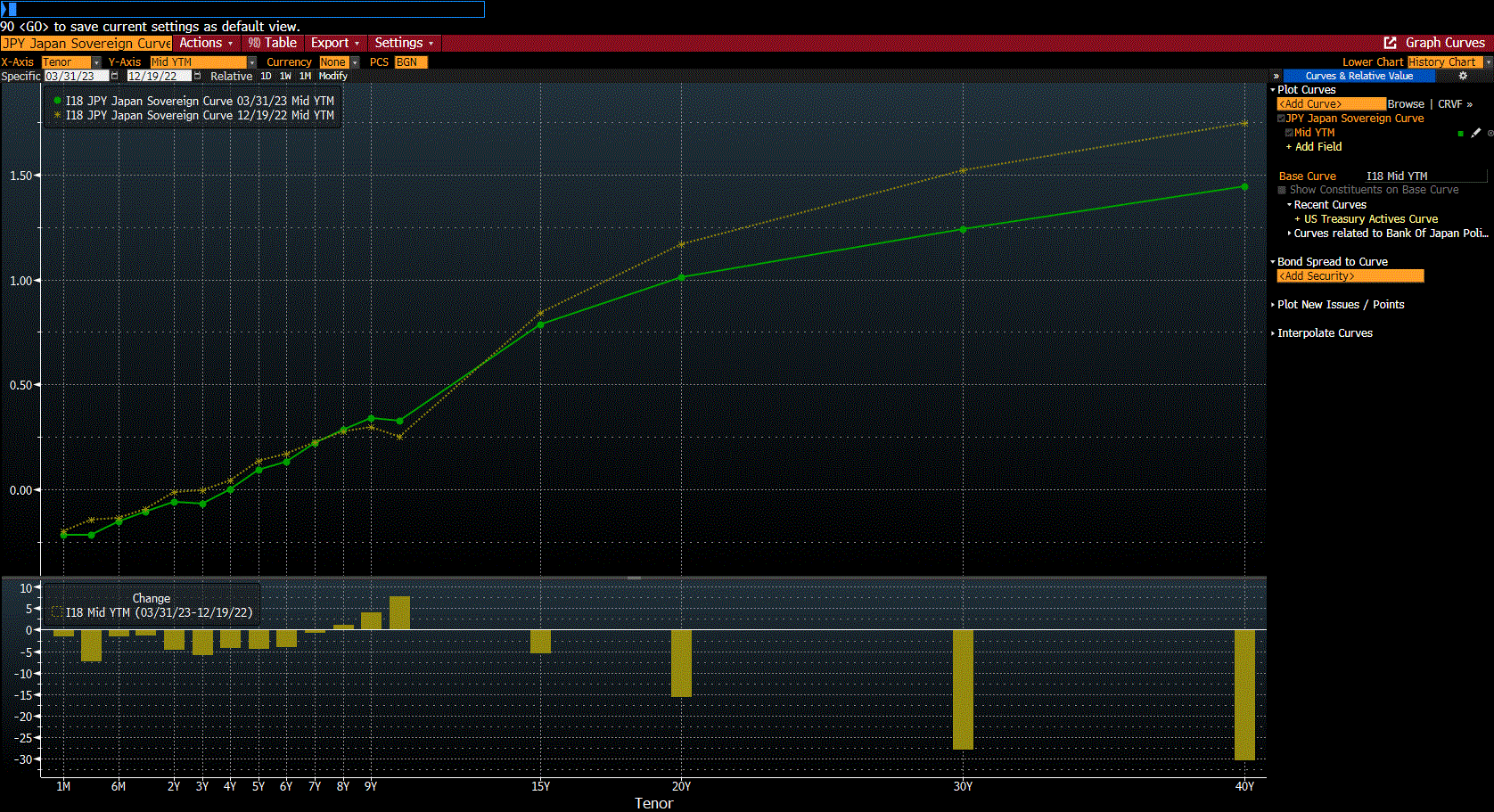

The below chart shows the yield curve at two points. The yellow line represents December 19, 2022, immediately before December’s band widening announcement, while the green line shows the curve on March 31, 2023, the BOJ’s fiscal year-end and the final days of Kuroda’s tenure.

Yield Curves on 12/19/22 and 3/31/23

{kind=link}

Despite the band expansion to improve market functioning, both curves still show the kink remaining.

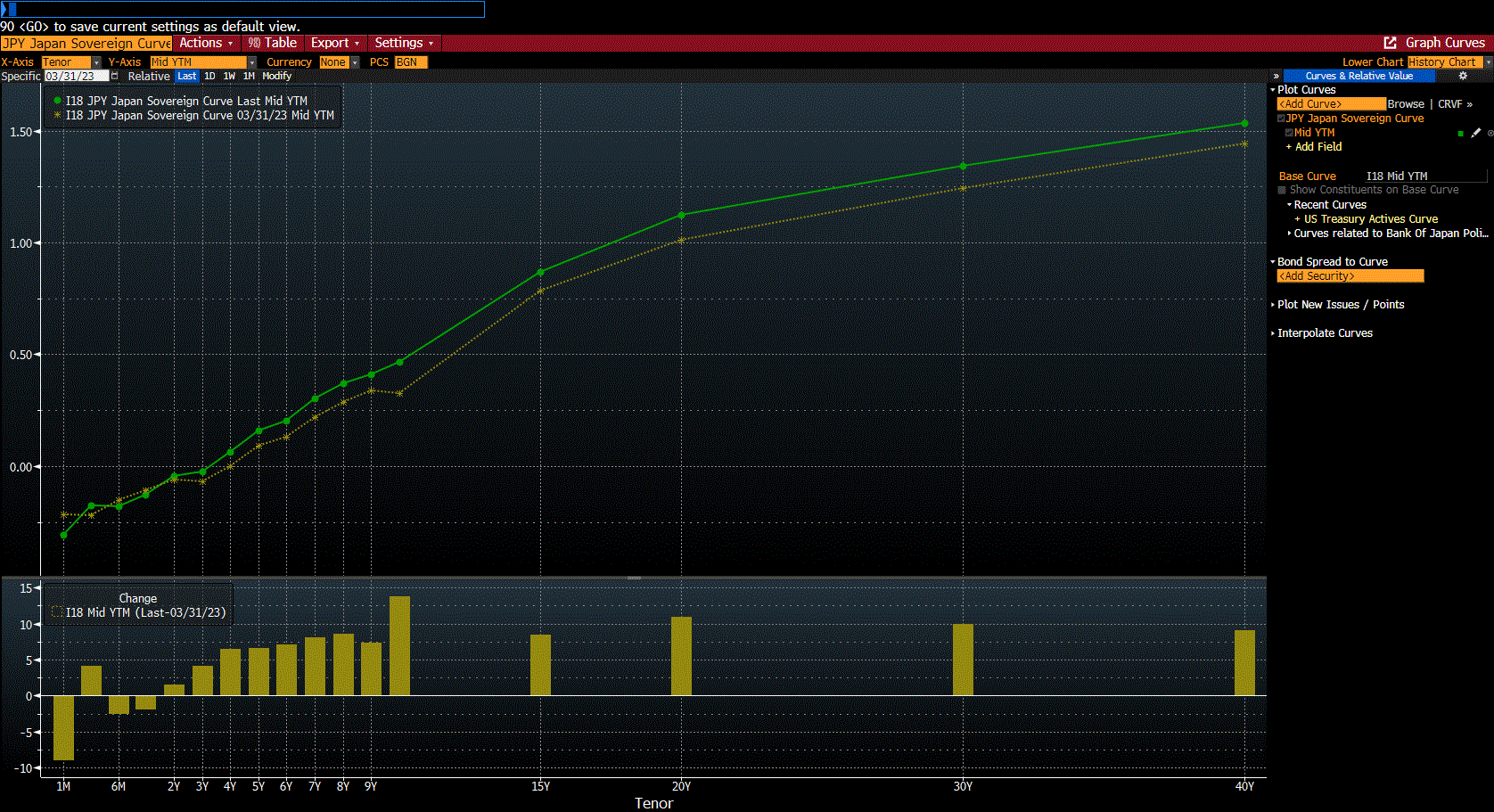

Since fiscal year end, with Ueda now at the helm, there has been modest improvement. The below chart again shows two curves with yellow representing fiscal year end and green showing the current curve. As can be seen in the chart, the kink in the 10-year is now gone.

Yield Curve on 3/31/23 and 4/21/23

{kind=link}

Liquidity

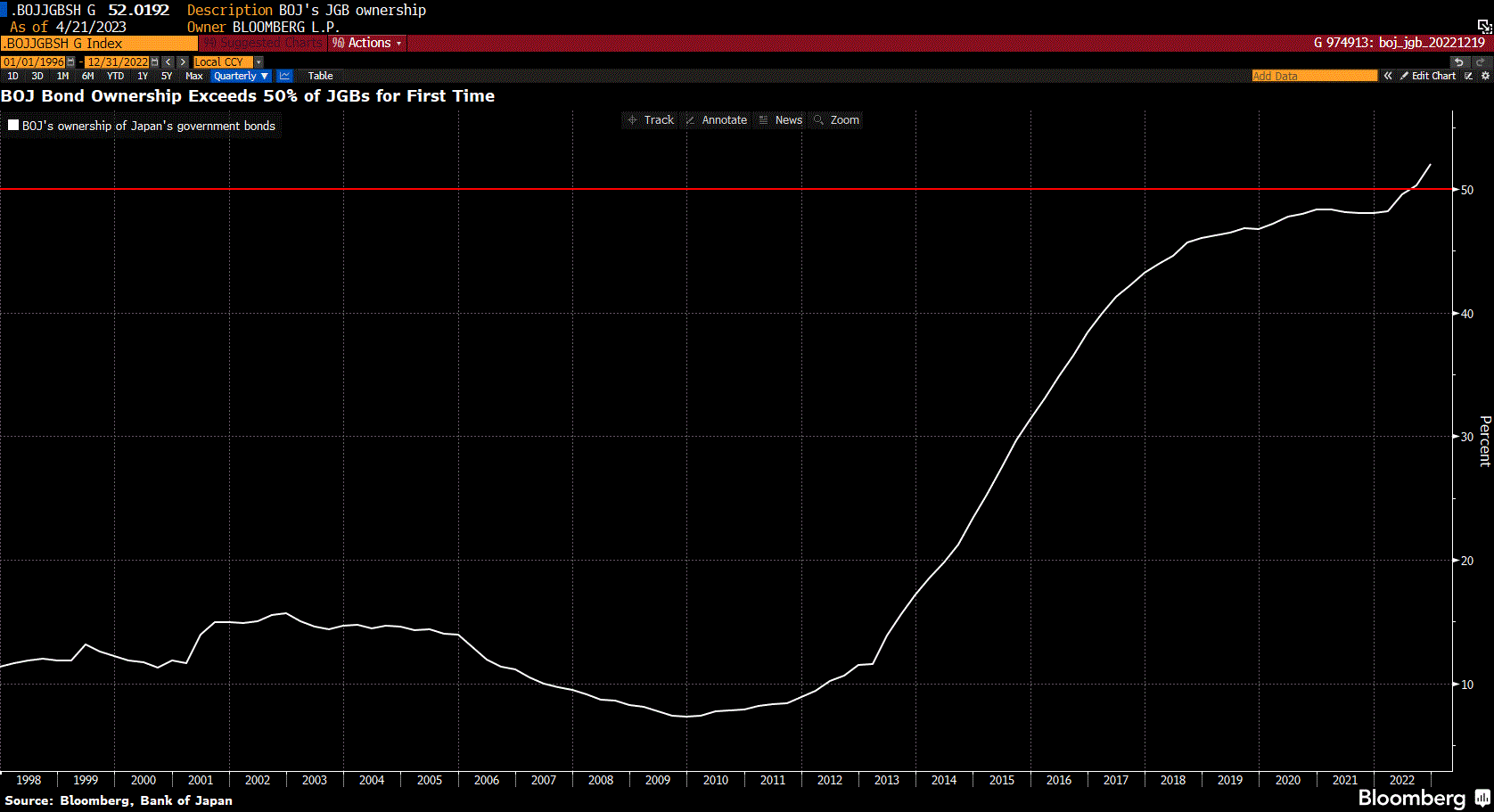

Liquidity was another reason for the BOJ’s surprise December modification. Liquidity, or lack thereof, has been a problem for quite some time. The reason for this is that the BOJ owns so much government debt and the tradeable market float is limited.

As of December 31,2022 the BOJ owned more that 52% of the entire JGB market. When Kuroda instituted YCC the BOJ only held 11% of the JGB market.

BOJ ownership of JGB market

{kind=link}

With their heavy new purchases this year, that percentage has only grown.

As other central banks are currently shrinking their balance sheets with Quantitative Tightening, the BOJ is moving in the opposite direction by greatly expanding their balance sheet. During the past year the BOJ’s holdings increased by 10.6%.

And this isn’t by design.

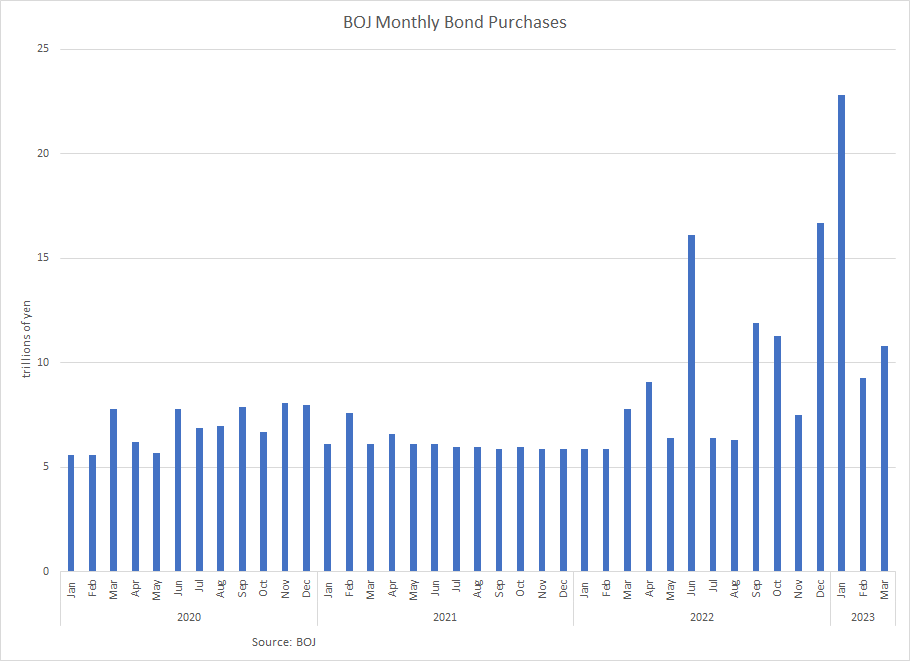

The BOJ’s stated goal was to buy up to 7.3 trillion yen of JGB’s per month in 2022. They generally followed this path until June 2022 when speculators stepped in.

As other central banks were tightening and interest rates around the world were rising, investors started betting that the BOJ would be forced to alter, or abandon, its interest rate target. They began shorting JGBs.

To defend the band, the BOJ adhered to their commitment to buy whatever was necessary to maintain their target, and wound up purchasing a then record 16.1 trillion yen of JGBs for the month. This was more than double their stated goal. Volatility calmed for a bit and they resumed their scheduled JGB purchases.

{kind=link}

The speculators returned in September with their bets against the BOJ, and the BOJ purchased 11.9 trillion yen of JGBs in September, and another 11.3 billion yen of JGBs in October. The band held.

But the pressure was growing on BOJ. They couldn’t continue buying JGBs at this pace. This is why in December there was a surprise announcement and the band was expanded from +/-25 basis points to +/- 50 basis points. The BOJ said the move was a “tweaking” and was aimed at smoothing out the distortions of the yield curve, and not a policy move or abandonment of YCC. The BOJ also announced that they would increase their JGB purchases to 9.0 trillion yen per month.

The yield on the 10-year JGB immediately spiked to near the top of the new band and the BOJ was forced to respond with more purchases. In December they bought a record 16.6 trillion yen of JGBs and then in January they had to buy a new record 22.8 trillion of JGBs.

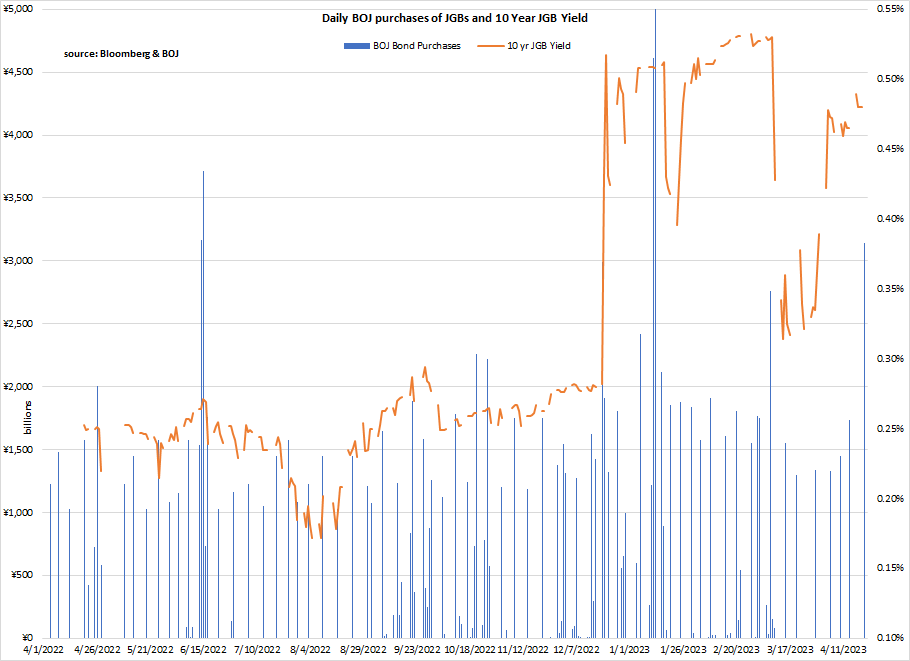

On a more granular level, the following chart shows the daily JGB purchases of the BOJ with the corresponding changes in the yields. You can clearly see the above mentioned BOJ interventions with the spikes in June 2022 and December 2022 and January 2023.

{kind=link}

The BOJ has had in place a Securities Lending Facility ((SLF)) for quite some time as a means to create more liquidity in the market due to their heavy ownership of JGBs.

One unusual twist to this situation is that the BOJ was actually lending JGBs that they owned to speculators so they could short them. These short sellers who bet on a change in monetary policy are making the BOJ’s YCC more difficult by putting upward pressure on yields.

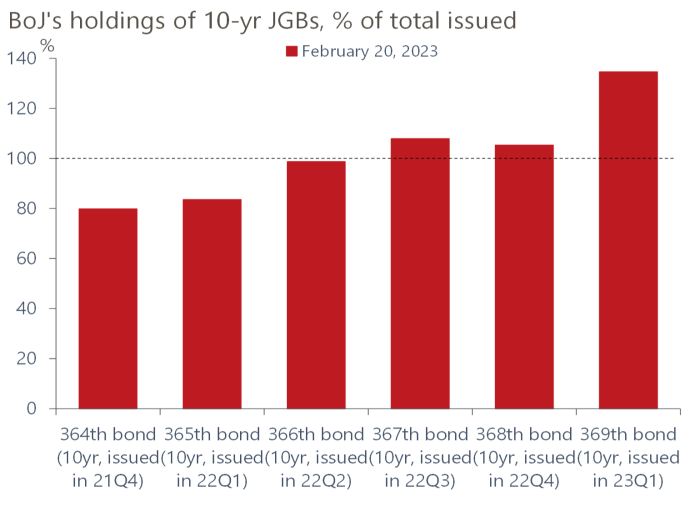

A further complication of the situation is that due to heavy purchases by the BOJ from speculators who are borrowing the BOJ’s bonds utilizing the SLF, the BOJ now own more than 100% of the three current benchmark 10-year JGBs.

According to Oxford Economics, after the assault on higher yields by speculators following the BOJs December band expansion and subsequent purchases by BOJ to defend the band, the BOJ has absorbed all the liquidity of on-the-run 10-year JGBs from the market.

{kind=link}

The BOJ owns 140% of the most recently issued on-the-run 10-year. This creates an odd situation where they could, if they choose, create a short squeeze, to punish the speculators.

However, the BOJ has implemented a plan to reduce speculation in another way. In late February they changed the terms of their SLF by raising fees dramatically. The cost to borrow securities was quadrupled from 25 basis points to 100 basis points. They hope that this will deter the speculators.

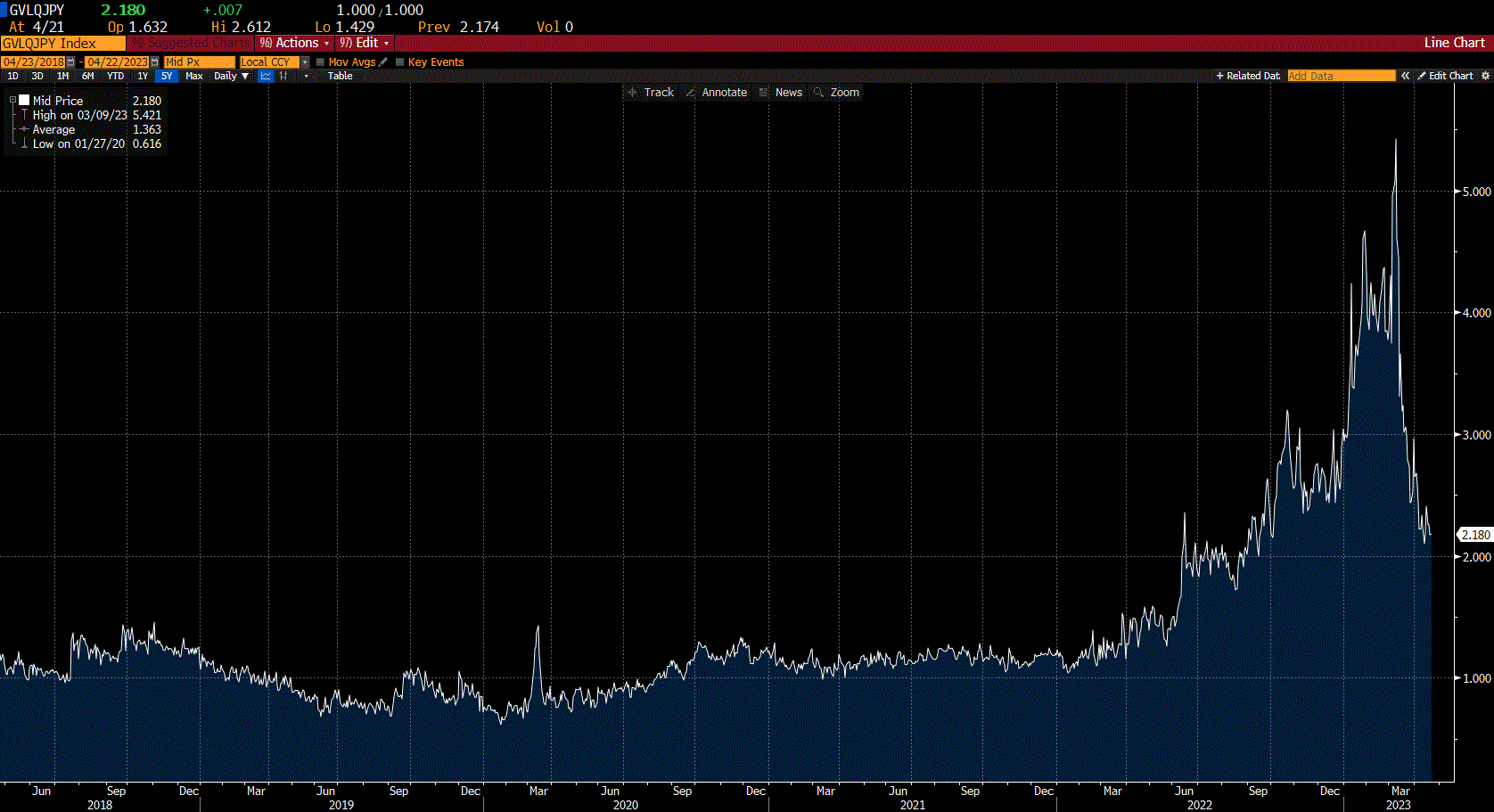

There is one sign that the increase in fees is having a positive effect. According to the Bloomberg JGB liquidity index, there has been some improvement in market liquidity.

Bloomberg JGB Liquidity Index

{kind=link}

This index measures the liquidity of the JGB market. The index displays the average yield error to relative value. When liquidity is favorable yield errors are small. Under stressed conditions, dislocations from fair value can remain, resulting in larger yield errors. In this index a larger number indicates less liquidity.

The chart shows how liquidity began deteriorating in June 2022, took another spike higher in September 2022, spiked in December 2022, rose again in January 2023, and finally peaked in February 2023 as the new SLF guidelines went into effect. Since then, there has been significant improvement.

Yen

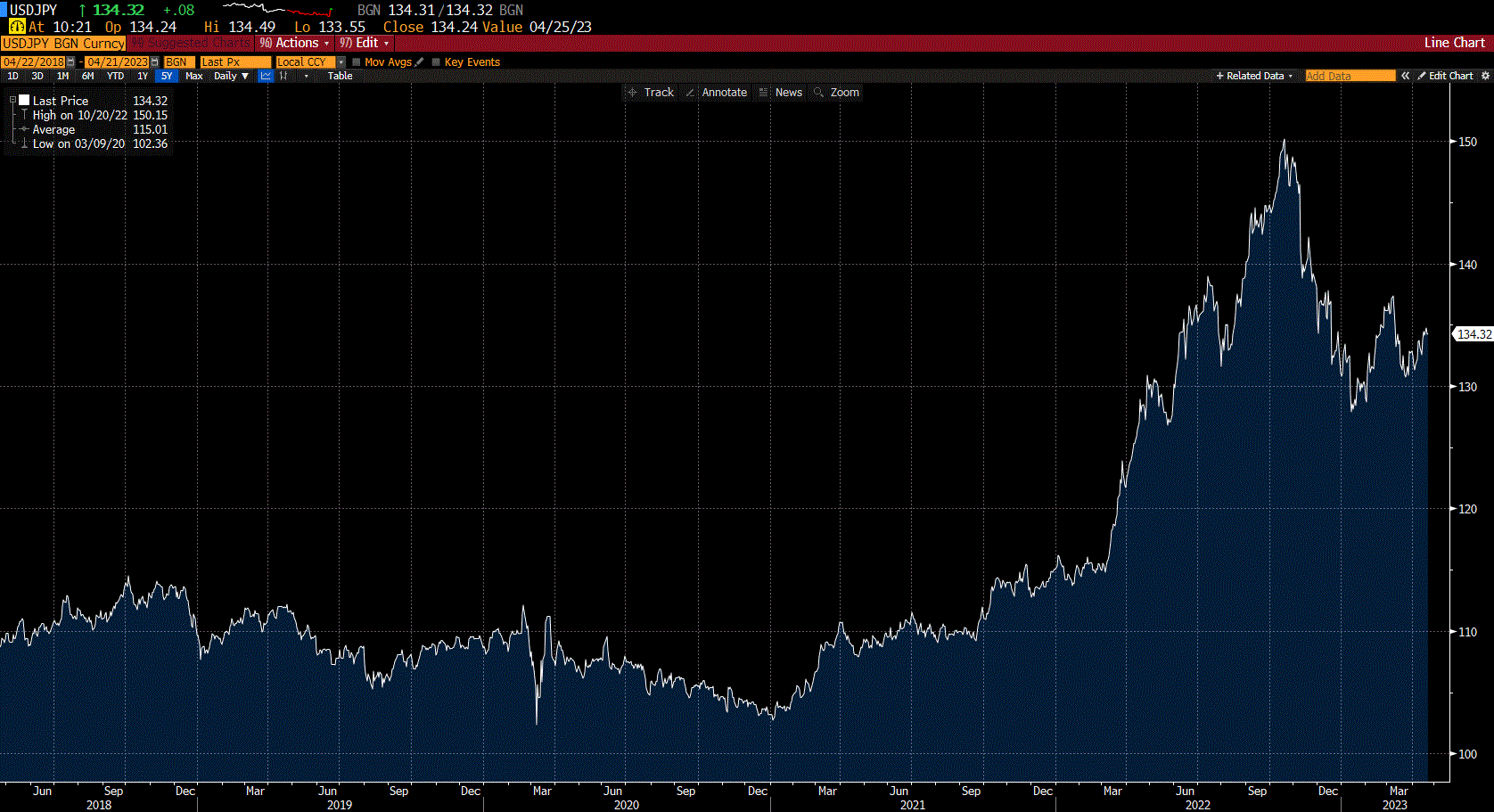

When yield differentials widened relative to other developed countries as they tightened by raising rates, the exchange value of the yen was crushed. The yen spiked to 153 versus the dollar by late fall 2022, a 25% decline from the beginning of the year. While it recovered somewhat following BOJ’s December tweaking of its 10-year JGB band, its future direction is unclear.

Yen Chart

{kind=link}

Unrealized Bond Losses

Most of the above discussion supports that the BOJ should change, or abandon, their easy money policies and tighten to fight inflation like the other central banks of the developed world. This means raising interest rates.

Such a move though, would exacerbate another problem facing the BOJ, which they share with the other major central banks.

The BOJ has a massive bond portfolio that is carried on their balance sheet at amortized cost. Virtually all of these securities were purchased when rates were close to 0.0%. Tightening that would raise interest rates would create a huge unrealized loss on their bond portfolio.

The BOJ as of 12/31/22 already has a 9.5 trillion yen unrealized loss on their bond portfolio of 570 trillion yen. They only have 5 trillion yen in capital, so the current unrealized loss is almost double their capital. Further rate hikes would increase the unrealized loss significantly.

In recent testimony BOJ Deputy Governor Amamiya stated that if the entire yield curve shifted upward by 100 basis points the BOJ’s unrealized loss would increase to 29 trillion yen.

Putting it all together

BOJ Governor Ueda has a big responsibility in his new job. He is inheriting an easy monetary policy that was created for a completely different economic environment. Confronted now with an unacceptable level of inflation, there is much pressure for him to repeal the policies of the past and move to a more appropriate monetary policy. However, in doing so, he will face new challenges that he must measure against current needs.

It appears his first step will be to not act immediately. Hopefully his review of the BOJ policies of the past twenty-five years will guide him down the appropriate path.

For further details see:

Bank of Japan Policy Normalization Comes Slowly Under New Leadership