BMO:CC - Bank Of Montreal: A Wonderful DGI Stock For The Long Run

Summary

- Bank of Montreal has a long track record of strong shareholder returns.

- It maintains a strong balance sheet and continues its dividend growth track record.

- The shares are reasonably attractive for long-term income and growth.

American banks like JPMorgan Chase ( JPM ) and Bank of America ( BAC ) may be well positioned for a stubbornly high interest rate environment, but there are some Canadian banks with better dividend track records, a higher yield, and lower valuation.

Such I find the case to be with Bank of Montreal ( BMO ), whose dividend track record simply leaves many of its south of the border peers in the dust. As shown below, BMO's total return has outperformed BAC, JPM, and the S&P 500 ( SPY ) over the long term.

BMO Total Return (Seeking Alpha)

{kind=link}

BMO remains well below its 52-week high of $123, and in this article, I highlight why it's an attractive buy for dividend growth investors.

Why BMO?

Bank of Montreal is the fourth largest of the Big 5 Canadian banks and is the 8th largest in North America by assets. It serves more than 12M customers, providing personal and commercial banking, wealth management, and investment services. It also has a presence in the U.S., where it gets about 30% of its revenues, with most of the rest coming from Canada.

BMO differentiates itself from its Canadian peers by having the lowest relative exposure to residential mortgage loans among the Big Six banks, making it less vulnerable to potential headwinds in the housing market as a result of higher interest rates, a risk that was all too familiar during the Great Recession.

Meanwhile, BMO has been building up its commercial lending strength in the U.S. and is seeing solid results amidst economic uncertainty. This is reflected by adjusted EPS rising by 2% YoY to C$13.23 during the full fiscal year 2022, and while adjusted ROE declined by 150 basis points compared to 2021, it still landed at a respectable 15.2%.

This was driven in large part to strong performance in the personal & commercial business, which saw pre-tax earnings growth of 13% and 33% YoY in Canada and the U.S. during the fourth quarter. Also encouraging, consumers are saving more in the current high interest environment, with average customer deposits up 8% YoY and 4% sequentially during Q4, thereby giving BMO more lending firepower.

Nonetheless, management is preparing for potential economic hurdles, with a total provision for credit losses of $226 million, compared with a total recovery of $126 million in the prior year. Plus, while management is less optimistic about consumer loan demand than previously, it sees its high quality consumer base as being overall healthy and in better shape than pre-pandemic times, as noted during the Q&A session of the last conference call :

The clients, both in Canada and the US, are holding up quite well. Their capital bases are strong, probably stronger than pre-pandemic rates have been so far kind of a modest impact. It will impact some more than others. But in many cases, our borrowers have interest rate protection.

We do see a little bit of slowing down in the client base. We do not see a slamming of the brakes. The consequence of that is we come from a pretty healthy position. The book is healthy. The momentum is good. We tend in this business to outperform the market in most environments. And I would expect that we'll do the same going forward next year. You probably won't see the loan growth next year that you saw this year. But you're still going to see loan growth because the customers that we select tend to be the good ones, and they tend to have good performance through time. That's what I think you should expect.

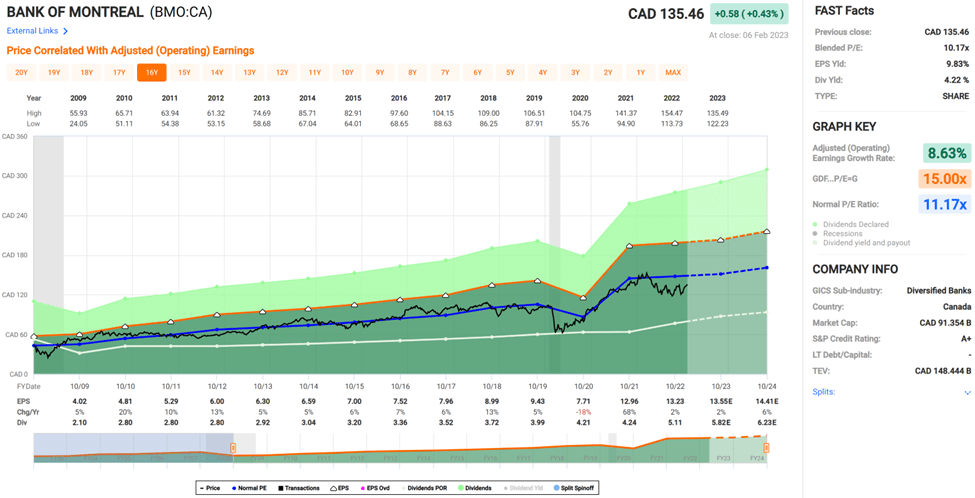

Importantly, BMO is in solid shape financially, with an A+ credit rating and a CET1 ratio of 16.7%, sitting well in excess of the 11% minimum requirement for Canadian banks. Remarkably, BMO hasn't missed a single dividend payment since initiating one in 1829. At present, BMO yields a respectable 4.2% and the dividend is well-protected by a 39% payout ratio and has a 5-year CAGR of 8.3%. This includes the most recent 8% dividend raise during fiscal Q1 to C$1.43.

Lastly, BMO remains attractively valued at the current price of $102 with a forward PE of 10.1, sitting below its long-term normal PE of 11.2 and analysts estimate 7% EPS growth next year. As such, I would estimate that BMO can provide investors with a near term total return at least in the low-teens should it return to its mean valuation.

{kind=link}

Investor Takeaway

BMO is one of the best-positioned banks in Canada when it comes to navigating the current economic headwinds, thanks to its low exposure to residential mortgage loans and strong foothold in commercial lending.

Additionally, BMO has a strong balance sheet and pays an attractive dividend yield, giving investors a steady income base as they navigate through choppy economic waters. As such, I find BMO to be a solid conservative Buy for income and growth investors.

For further details see:

Bank Of Montreal: A Wonderful DGI Stock For The Long Run