ZION - Banking Crisis: A Buying Opportunity

2023-03-31 06:31:01 ET

Summary

- The collapse of Silicon Valley Bank and Signature Bank has caused a fallout in the stock price of other regional banks.

- There are buying opportunities in the midst of the fallout.

- ZION and SCHW are two stocks that I am buying.

The banking crisis has caused some jitters in the market. The market as a whole seemed to recover from these worries and pulled through with a gain last week. The effects of the banking failures and concerns on the broader economy are worthy of an article in and of itself. Could it help push the economy into a recession? Will lenders pull back on lending potentially causing a recession, or help inflation drop? How will the Fed react to the changes in the market? A lot can be unpacked from what we have seen over the last two weeks. But, that is not the topic of my discussion today. Today I want to focus on what I think are potential buying opportunities that have presented themselves in the market. The particular winner to me is Zions Bancorp, National Association ( ZION ). The runner up being The Charles Schwab Corporation ( SCHW ).

Rather obvious, but the stocks that dropped the most recently were regional banks. These stocks are the most at risk to a similar end result as Silicon Valley Bank and Signature Bank. Credit Suisse also collapsed, or excuse me, was purchased. Although I believe the reasons behind Credit Suisse failure are not the same as the regional banks in the US. While duration issues affected Credit Suisse, it was probably more likely the straw that broke the camel's back. I don't want to do a deep dive into the issues around the collapse of those banks and why, how, or the many reasons that it happened. There are many articles and discussions as to why and how it happened. My focus is on the stocks that saw a collapse in their stock prices due to the collapse in the other banks. Which ones, if any, are a good buy due to the drop in price. While not diving into it in depth here, I am not discrediting understanding the why and how of the bank failures we saw. This is important to know if a particular stock is more at risk or is potentially undervalued/overvalued. I will discuss at a high level to help you understand why I think certain stocks are a buy following the drop in price.

Run on Regional Banks

Regional banks do not have as much available capital as larger banks. When customers pull large sums from a regional bank it is noticed much more than from a larger bank. A run on smaller regional banks can happen fast, fast enough that Usain Bolt himself might be impressed. We saw this with Silicon Valley Bank and Signature Bank. In brief, the main cause of their demise was a duration issue on their holdings (there are other reasons that I will discuss more) The Fed has raised rates at a historically fast rate. This has caused treasury holdings and mortgage bonds to lose a lot of value. Banks are sitting on those paper losses. Now there is not necessarily a problem with that theoretical loss if the banks do not have to sell those positions. Sure they are not getting as much interest as they could be getting, but liquidity wise they will not be in trouble. The issues come when customers want their money at a large enough clip that banks have to sell those positions and realize that loss. All of a sudden the bank is going to be crunched for cash.

Side note, but the psychology behind bank runs is very interesting. Bank runs are really a self-fulfilling prophecy. People hear a bank is in trouble and go to pull their money out. The very fact of them pulling their money out causes the bank to be in trouble.

Back to the meat and potatoes. People (or at least I am going to say a high percentage) know that their money is protected by FDIC up to $250,000. If you have less than that in your account then there is no need to run on the bank. You have the insurance and don't need to be concerned as you have the backing of Uncle Sam. I think far fewer people with less than the insured amount in their account are pulling their money from the bank. At least they are not withdrawing in large enough amounts to cause serious problems. I think the much larger concern for these regional banks are the deposits that are not insured. Banks with higher uninsured deposits are at higher risk of a run on the bank.

The other factor playing into the withdrawals is that you can get so much more for your money elsewhere. You can keep your money in your savings account or put it in a money market account and earn twice as much as that savings account. This is causing a lot of people to rethink where they are parking their money. This is also causing outflows from a lot of savings accounts. Another factor not helping the liquidity crunch on banks.

Zions Bancorporation

ZION is a regional bank that saw a large drop following the collapse of Silicon Valley Bank. On March 8th, the stock price for ZION closed at $46.68 a share. In a matter of days the stock price tanked on fears that ZION would be next on the list of banks to fail. The stock most recently closed at $28.25 a share. That is a decline of nearly 40%. With two banks already failed and Zions Bank being closely correlated in terms of size and market, many have thought that Zions is at risk of failure as well. While this is to some extent true, I think the risk to Zions Bank has been overdone. It is not as closely correlated with either of the two banks that already failed as it may seem.

The first reason that I like the stock is that the price decline has been exaggerated. At a decline of 40% people are in essence placing their bet that it goes bust. If it does not go bust then it has to be a great buying opportunity. Sure there may have been withdrawals from the bank. Their deposits may have decreased and they may be slowing their pace on loans. These could have a negative effect on earnings. But to say that the value of the company has dropped 40% is not because the business has slowed and there might be some negative effects on earnings. That large of a drop is not justified on that basis. It is because people are concerned it fails. If you do not think the bank is going to fail then the price has fallen too much and you have a buying opportunity.

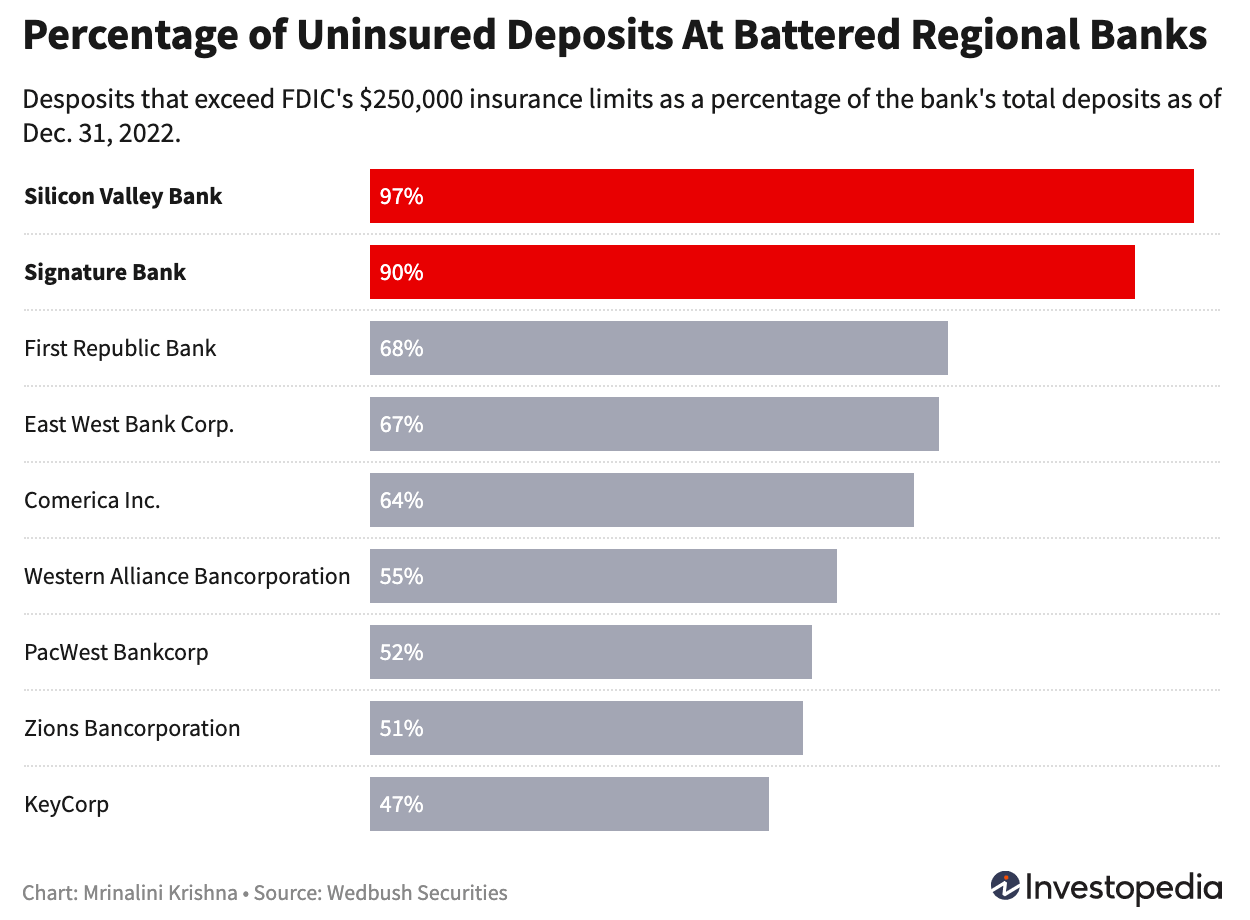

The next question is do you think the bank will fail. I do not believe the bank will fail. There are few factors that differ Zions Bank from Silicon Valley and Signature Bank. The first is that Zions Bank is in a much less risky position in terms of liquidity and susceptible to a bank run. As I mentioned before I don't think accounts that are insured are as likely to pull their money. As you can see in the chart below, Zions Bank has a much lower percentage of uninsured deposits than many of the other regional banks. In my opinion, this makes it much less susceptible to a run on the bank.

{kind=link}

Silicon Valley Bank and Signature Bank had extremely high percentages of uninsured deposits. Drastically higher than most other regional banks. This caused them to be at higher risk for a run.

The other reason is that I believe the markets and industries that bank with Zions Bank are different from the two failed banks. Silicon Valley Bank was extremely focused on the tech sector and startups. Signature Bank is very connected with the real estate market in New York and also cryptocurrency. We know that the tech sector has been battered as of late. There have been massive layoffs in the tech sector. Funding for startups has been drying up. Due to the downturn these companies have needed to pull more money from their accounts. They still have to meet payroll and pay rent. Expenses don't just stop even if less money is coming in the door. I think this put extra strain on Silicon Valley Bank specifically. It was in the wrong part of the market. In a similar vein, Signature Bank was connected to an industry that was not doing well at the moment. These two banks were tied into the wrong industries and were running at a much higher level or risk. When things turned negative in these industries they got into trouble. Not to say that other banks are not at risk, I just don't think the risk is as concentrated and in the wrong industries at the wrong time.

There was obviously concern of bleed over and that these two banks were not isolated in their issues. I do think that this was much more focused on a couple of banks and mismanagement at those banks. In fact there is some question as to whether Signature Bank really needed to be swallowed up by the government. It might have been a case of authorities not wanting to see the contagion effect and jump on it early as they saw it as more risky. We know that most authorities are not really keen on the cryptocurrency industry as well, in which Signature Bank was heavily involved. Overall I do not think the banking crisis will be as widespread as many fear.

The last reason I have for not thinking that Zions Bank will fail is due to government intervention. I will discuss that in a later section of the analysis.

The Charles Schwab Corporation

Charles Schwab did not experience as much of a decline as some regional banks. The main reason being is that Charles Schwab is much larger than many of these banks. I think that Charles Schwab has been lumped in with some of these banks although it does not belong there. It has been a casualty by association in the banking sector.

The other factor for Charles Schwab is that one of the negatives for many banks is looking like a positive for Charles Schwab. I mentioned how many people are withdrawing money from savings accounts because they can make much more in safe investments right now. Luckily for Charles Schwab they run one of the larger trading platforms for purchasing investments. They are currently seeing larger inflows than normal .

That is my simple thesis for my buy on SCHW. It has wrongfully been caught in the fallout from the other bank collapses. It is not in the same position as the regional banks. It manages a large investment arm. It would take an industry wide fallout for SCHW to fail. Not to mention the fact that it manages so many retirement and other accounts. If things were to ever get in a really bad situation for the industry then I think the argument would be that you cannot let SCHW fail. I am not endorsing the government stepping in and saving banks, or the too big to fail thesis. I am merely stating what I believe would happen and make my investments based upon that.

Government Intervention

The last factor that comes into play and this is a big one, government intervention. I think it is pretty clear to see that the government is not going to let the banks fail. It stepped in and guaranteed the deposits for Silicon Valley Bank really quickly. Not to say that it would do that same for all the banks but if they did it for one then it makes it hard to say no to the next bank.

Comments from authorities have been a bit inconsistent. They have said they will support the banks . They have also said they will not provide bank bailouts . They have discussed enacting legislation to provide a guarantee on all deposits. Although this seems unlikely as many are worried that will only encourage risky behavior by banks. Janet Yellen has seemed the most inconsistent with her statements as she toes the line between calming fears and overstepping her authority. Yellen has stated that taxpayers will bear none of the losses incurred by Silicon Valley Bank or Signature Bank. That raises a whole bunch of questions seeing as the government guaranteed the deposits, yet the government's only income is through taxpayers….. Politics will be politics. We don't need to wade too deep into that quagmire.

At the end of the day, they guaranteed the deposits of two banks already. They have provided massive liquidity facility in the form of the Discount Window Lending and the Bank Term Funding Program. I think these actions are enough to show their intentions. Those intentions are to not let more banks fail.

Risks

No investment is without risks. There is obviously risk in the banking sector as a couple of banks have already failed. I have outlined why I think these risks are mitigated for both ZION and SCHW.

The largest risk that I see in this situation is more of a pullback in the economy as a whole. If banks are tighter on liquidity then they are less likely to make loans. Without money moving through the economy we are much more likely to enter a recession. We do not yet know if this credit crunch is occurring or will occur or the size it might be. If it does happen on a large scale then it will be a negative on the economy as a whole. I think the current banking crisis increases the risk of recession as a whole. A recession would obviously have a negative effect on all banks.

The other risk also comes from a positive in my investment thesis. That is government intervention. We could see new regulations come down the chain once everything is sorted out. These regulations could restrict the profit making ability of banks. This would cause a decreased value in banks as a whole.

There is the concern, and it is a real concern, that regional banks will suffer from the fallout. Larger banks are considered "too big to fail". That makes people confident in those banks. The know the government will intervene to protect their money. This does not make the playing field level (government intervention tends to create winners and losers, even if unintended). The withdrawals from small banks will flow to these larger organizations. One catch on this is that regulation may help here. Some statements recently made by Neel Kashkari, president of the Federal Reserve Bank of Minneapolis were interesting in regards to regional banks. "We need regional banks in America. We need community banks in America," he said. "Once we get through this stress period, we have to come up with a regulatory system that both ensures the soundness of our banking system, but is also fair and even so that community banks and regional banks can thrive. We do not have that today."

My Investment Position

I have taken a long position in both ZION and SCHW. I have also sold puts on ZION.

For further details see:

Banking Crisis: A Buying Opportunity