META - Baron Durable Advantage Fund Q2 2023 Shareholder Letter

2023-08-16 11:00:00 ET

Summary

- Baron is an asset management firm focused on delivering growth equity investment solutions known for a long-term, fundamental, active approach to growth investing.

- Baron Durable Advantage Fund gained 10.7% during Q2, which compared favorably to the gain of 8.7% for the S&P 500 Index, the Fund’s benchmark.

- From our perspective, not much has changed from our comments three months ago.

- Consensus expectations call for one or two more hikes this year followed by rate cuts as we get into 2024.

Performance

We had another good quarter and a strong first half of the year.

Baron Durable Advantage Fund® (the Fund) gained 10.7% (Institutional Shares) during the second quarter, which compared favorably to the gain of 8.7% for the S&P 500 Index (the Index), the Fund's benchmark. Year-to-date, the Fund is up 28.4% compared to 16.9% for the Index.

{kind=link}

Performance listed in the table above is net of annual operating expenses. The gross annual expense ratio for the Retail and Institutional Shares as of September 30, 2022 was 1.49% and 1.10%, respectively, but the net annual expense ratio was 0.95% and 0.70% (net of the Adviser's fee waivers), respectively. The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor's shares, when redeemed, may be worth more or less than their original cost. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund's transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month end, visit www.BaronFunds.com or call 1-800-99BARON.

More of the same.

From our perspective, not much has changed from our comments three months ago. The bears continue to argue that the unprecedented pace of interest rate hikes will cause the U.S. economy to enter a prolonged recession, which will cause a sustained deterioration in corporate earnings. They further argue that even if the economy proves to be more resilient, then inflation will prove to be stickier, which means that the Fed will continue to raise rates until both break, which in turn, means earnings will still need to be revised lower and stock prices will follow. The bulls continue to argue that the tightening cycle is mostly behind us, that inflation has clearly peaked and is on its way down, that the economy has proven to be resilient, and that after earnings reset in 2023, companies will resume their growth trajectories in 2024. They further argue that even if the economy does falter and slip into a recession, the Fed will start lowering rates, which is good for intrinsic values. This logic is of course circular with each argument leading into and supporting the other enabling both sides to stand their ground. While we expect this debate to continue, the market's wisdom of crowds, as well as the Fed, clearly suggest that we are much closer to the end of this rate hike cycle than to its beginning.

Consensus expectations call for one or two more hikes this year followed by rate cuts as we get into 2024. It is also clear that investor sentiment that was heavily tilted to the downside just six months ago has changed, as the Index is now officially in bull market territory. The rally has been largely driven by technology stocks that had their strongest half-year performance in more than 20 years, not entirely surprising after the steep correction of last year. The Magnificent Seven - NVIDIA ( NVDA ) +190%, Tesla ( TSLA ) +113%, Meta ( META ) +138%, Apple ( AAPL ) +50%, Amazon ( AMZN ) +55%, Microsoft ( MSFT ) +43%, and Alphabet ( GOOG ) ( GOOGL ) +36% were responsible for 73.9% of the Index's year-to-date return. Five of these companies accounted for 33% of the Fund's net assets at the end of this quarter. Selling our entire position in Apple some years ago was a costly mistake. We were completely right about investors' overestimation of Apple's growth prospects but misjudged that the market's recognition of the quality of Apple's business would eventually lead to a dramatically higher multiple. Tesla made it to the very top of our "new idea" list in January. We were going to start buying it below $100 per share. It bottomed out at $101.81 and closed the June quarter at $261.77. Oh well… in this business, we'll take five out of seven - every time!

In terms of performance attribution for the second quarter, strong stock selection in Communication Services attributable to Meta and Alphabet combined with our overweight to the sector accounted for most of the excess returns. Stock selection in Consumer Discretionary (Amazon) and lack of investments in Energy, Utilities, Real Estate, and Materials also contributed positively to relative returns. Poor stock selection in Health Care (due mostly to our overweight to the life sciences tools & services sub-industry) and a sizable overweight to Financials were the two detractors of note.

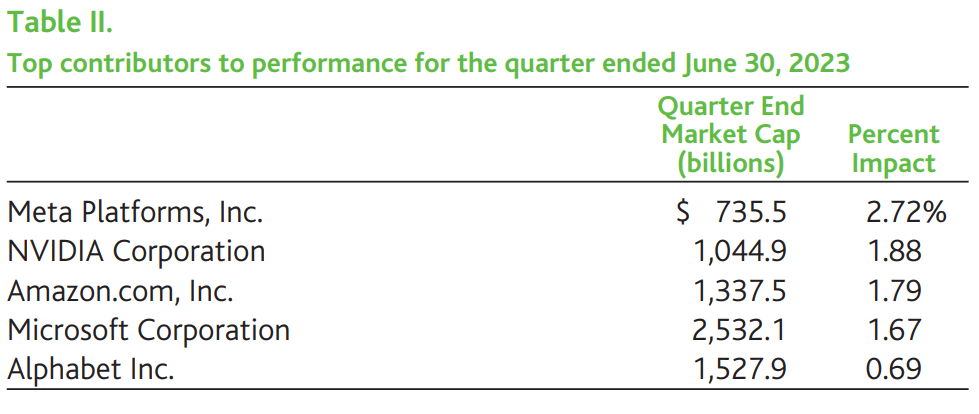

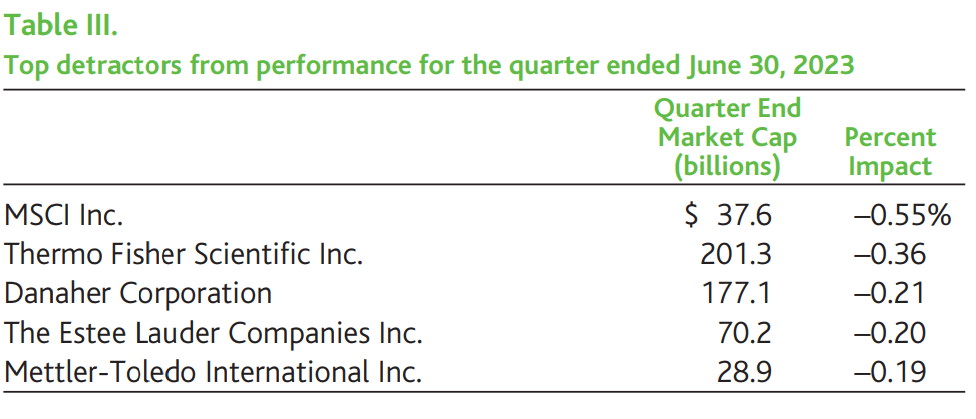

Turning to absolute returns, we had 22 contributors and 8 detractors. Not as good as the prior quarter's 27 and 4, but about what one could expect in a generally rising and recovering stock market. In addition to this solid batting average, we also enjoyed a good slugging percentage as our four largest contributors - Meta, NVIDIA, Amazon, and Microsoft - were also our four largest investments, contributing over 160bps each with gains of between 18% and 52% during the second quarter. Alphabet , S&P Global ( SPGI ) , Adobe ( ADBE ) , Arch ( ARCH ) , Moody's ( MCO ) , and Accenture ( ACN ) rounded out the top 10 contributors adding at least 30bps each to absolute returns. Among the Fund's 8 detractors, only MSCI and Thermo Fisher Scientific cost us more than 30bps, detracting55bps and 36bps, respectively.

Since the inception of the Fund five-and-a-half years ago we have experienced two severe bear markets, a global pandemic, the fastest interest rate hiking cycle in U.S. history, and a war in Europe. If that wasn't enough, the political landscape in the U.S. and the world over gave us outcomes that were well outside most prognosticators' ranges, in some cases, even our own. Through it all, we argued that investors should not equate market volatility and stock price volatility to risk. We argued that risk should be evaluated in the context of probability of permanent loss of capital and that market volatility is an opportunity for investors with a long-term ownership mindset.

The price of a stock has two components to it: we think of the first one as the health of the business or its fundamentals. It can be measured by cash flows, earnings per share or in some cases, revenues. The second component is the multiple that investors are willing to pay for those fundamentals. The performance or returns of stocks are driven by the changes in these two components. The fundamentals of a high-quality business, while not immune to external shocks and macro pressures, tend to be far more stable and resilient than the investor psychology that shifts dramatically with the environment and drives multiple expansions or compressions. Over long periods of time, high-quality businesses' fundamentals often compound exponentially, while the change in multiples is always linear. Hence, for long-term investors, stock price declines of high-quality businesses driven primarily by changes in the investor psychology have historically been shown to be great opportunities to buy those businesses at good discounts to their intrinsic values. This is exactly why Meta (-64%), NVIDIA (-50%), Amazon (-50%), Microsoft (-29%), and Alphabet (-39%) were some of our largest purchases in 2022.

Speaking of 2022, it was obviously a challenging year for equity investors, and the Fund declined 24.8%. We recovered all of that decline in the first six months of this year. Interestingly, last year's loss was driven entirely by multiple contraction as the weighted average multiple for our investments was down 26%. However, our recovery year-to-date has been driven by a combination of multiple expansion1 (+18%) as well as growth in earnings (i.e., fundamentals). Despite the complex macro environment, many of our companies have begun reporting improving business trends during their recent quarterly results, leading to upward estimate revisions over the last three months.

Last year's drawdown notwithstanding, we continue to believe that we have put together the right collection of competitively advantaged companies with durable growth characteristics and great management teams. We have a lot of confidence in our process. If executed well, we should be able to outperform the Index over the long term while minimizing the risk of permanent loss of capital. The 24.8% decline was painful. But in the context of a 28.4% gain year-to-date, 27.7% gain over the last 12 months, 14.4% annualized gain over the last 3 years, and 14.3% annualized gain over the last 5 years, we think it is not unreasonable.

{kind=link}

Shares of Meta Platforms, Inc. , the world's largest social network continued their upward trajectory, rising by 35.4% due to stabilizing revenues and ongoing improvements in margins. Meta reported continued growth in Instagram Reels adoption and other new advertising products. In addition, the company's advancements in artificial intelligence ((AI)) continue contributing to its targeting and measurement capabilities, while generative AI (GenAI) innovation presents an opportunity for new products and incremental monetization. The company also achieved a significant milestone of 3 billion daily active users across its family of apps, representing a 5% year-over-year increase. User engagement remains robust, with video content and Instagram Reels playing a significant role in user time on the platform. The monetization gap between Reels and other ad formats is steadily narrowing, and Meta anticipates it will reach revenue neutrality by late 2023 or early 2024. Meta has also reported an increase in its speed and agility of execution following the recent organizational changes and cost cuts. Longer term, we believe Meta will benefit from its leadership in mobile advertising, massive user base, innovative culture, leading GenAI research and potential distribution, and technological scale, with further monetization opportunities ahead.

NVIDIA Corporation is a fabless semiconductor company designing chips and software for gaming and accelerated computing. Shares continued their torrid first quarter rise, increasing 52.3% in the second quarter, after the company reported a meaningful acceleration in demand for its data center Graphics Processing Units, which drove a material guidance beat with revenues expected to increase from $7.2 billion to approximately $11 billion sequentially. This unprecedented acceleration is driven by growing demand for GenAI. We are at the tipping point of a new computing era with NVIDIA at its epicenter. While the opportunity within the data center installed base is already large at approximately $1 trillion, the pace of innovation in AI in general, and GenAI in particular, should drive a significant expansion in the market, as AI creates a new way for human-computer interaction through language, and as companies are better able to utilize their data for decision- making. We remain shareholders as we believe NVIDIA's end-to-end AI platform and the ecosystem it has cultivated over the last 15 years will benefit the company for years to come.

Amazon.com, Inc. is the world's largest retailer and cloud services provider. During the quarter, Amazon's shares increased 25.9% as a result of improving investor perception regarding the company's advancements in AI, as well as an anticipated slowdown in customer cloud optimization initiatives, which is expected to pave the way for the reacceleration of growth in Amazon Web Services (AWS) in the latter part of 2023. We are also optimistic about Amazon's ability to significantly enhance the profitability of its core North American retail segment in the short to medium term. This optimism stems from the company's transition to a new regionalized fulfillment network, the rightsizing of its infrastructure from the increased spend levels during the early stages of the pandemic, and its rapidly growing advertising business, which is margin accretive. Looking further ahead, Amazon's potential for growth in e-commerce remains substantial, considering it currently captures less than 15% of its total addressable market. Amazon also remains the clear leader in the vast and growing cloud infrastructure market, with large opportunities in application software, including enabling GenAI workloads.

{kind=link}

Shares of MSCI Inc. ( MSCI ) , a leading provider of investment decision support tools, detracted from performance after declining 16.0% in the second quarter despite reporting steady first quarter earnings results and reiterating its outlook for 2023. The stock's move down was driven by in part by weaker new sales activity in ESG due to the political environment in the U.S. and some regulatory updates in the EU around classifying ESG funds. In addition, broader macro uncertainty starting in late March led to a tightening of client budgets, lengthening of sales cycles (though the pipeline remains healthy), and increasing cancellations with smaller clients (though overall retention rates remain strong at approximately 95%). While there is some near-term uncertainty, we believe that the impact of the slowdown in the ESG segment would not be meaningful (we estimate that ESG overall represents around 10% of revenues and less than 5% of profits), while broader business fundamentals remain sound. We retain long-term conviction as MSCI owns strong, all weather franchises that should enable the company to compound earnings at a double-digit rate for many years.

Thermo Fisher Scientific Inc. ( TMO ) is the world's largest life sciences tools company. Thermo Fisher provides analytical instruments, laboratory equipment, software, services, consumables, and reagents for life sciences research, manufacturing, analysis, discovery, and diagnostics. Shares fell 9.4% during the quarter along with other life sciences tools stocks because of several headwinds, including a slowdown in capital spending among pharmaceutical customers, slower growth in China, lack of funding and spending among pre-commercial biotechnology companies, and inventory destocking among bioprocessing customers. We view these headwinds as temporary and believe management can achieve its long-term goal of solid mid- to high single-digit organic revenue growth with an even faster profit growth, driven by long-term end-market tailwinds in the life sciences industry, including favorable demographics, scientific advances, new technology, and increased regulations.

Danaher Corporation ( DHR ) is a life sciences and diagnostics company. For life sciences, Danaher supplies instruments for lab research, genomics services, and bioproduction tools. For the diagnostics business, Danaher offers instruments to run clinical tests in large core labs, hospitals, and pathology labs and at the point of care. Shares declined 4.7% during the quarter after the company cut its fiscal year 2023 guidance due to headwinds within its bioprocessing segment, as biopharmaceutical customers burned through existing inventory and smaller biotechnology firms faced funding constraints. We remain positive on Danaher's long-term trajectory. Danaher benefits from a market-leading position and broad portfolio within bioprocessing, which addresses a biologics market that is growing by double digits, and which we expect to benefit in the near and medium term from a wave of biosimilars entering the market after key patents expire. Danaher has a collection of high-quality assets, with targets of high single- digit core revenue growth and double-digit EPS growth.

Portfolio Structure

The portfolio is constructed on a bottom-up basis with the quality of ideas and conviction level, rather than benchmark composition and weights, determining the size of each individual investment. Sector weights tend to be an outcome of the stock selection process and are not meant to indicate a positive or a negative view.

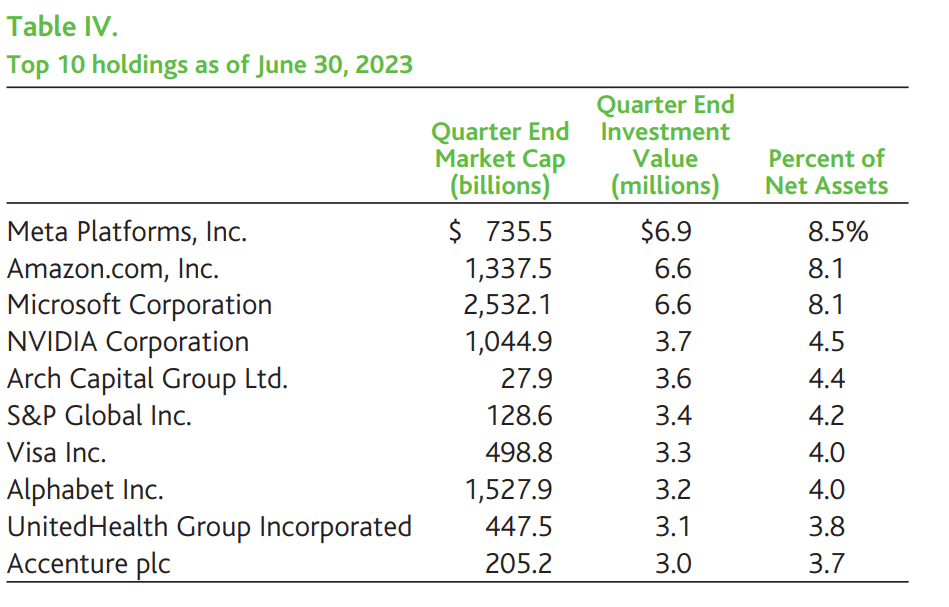

As of June 30, 2023, our top 10 positions represented 53.3% of the Fund, the top 20 represented 81.6%, and we exited the second quarter with 30 investments, unchanged from the first quarter. IT and Financials represented 61.0% of the Fund, while Communication Services, Health Care, Consumer Discretionary, Consumer Staples, and Industrials represented another 37.7%, with the remainder in cash.

{kind=link}

Recent Activity

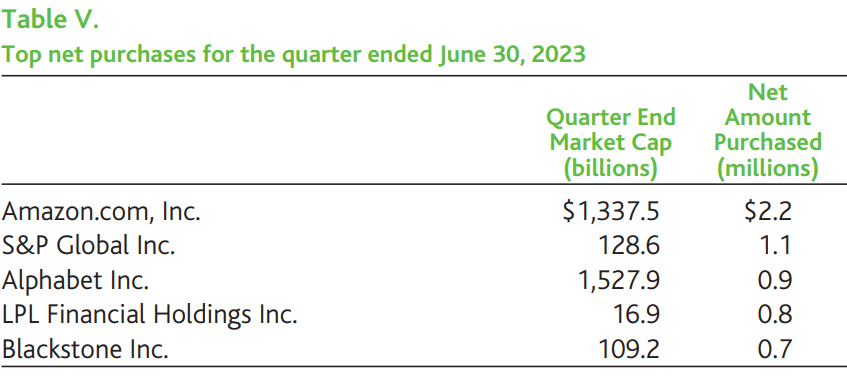

During the second quarter, we added to 25 of our holdings as we put the Fund's inflows to work.

{kind=link}

Amazon.com, Inc. was our largest addition during the second quarter. We believe that Amazon's core retail profitability is still masked due to its increased spending in the early days of COVID-19 and profitability should become more visible over the next several quarters as the company right sizes its infrastructure and regionalizes its fulfillment network, which simultaneously reduces delivery times costs. In addition, as customers start lapping their cloud optimization efforts, we expect AWS business to reaccelerate.

We continue to believe that Amazon holds sustainable competitive advantages with a leadership position in multiple trillion dollar markets that exhibit durable growth characteristics. According to the U.S. Census Bureau domestic e-commerce still accounts for only 15.1% of retail sales (as of the first quarter of 20232). Internationally, the upside is also significant as Amazon has less than 5% market share of international retail sales. Amazon's advertising market share is still below 5%, even though it continues outgrowing other digital advertising companies. For example, Amazon's advertising revenues were up 21% year-over-year in the first quarter of 2023, compared to revenue growth rates of 3% for both Meta and Alphabet. This is driven by Amazon's structural advantages in advertising thanks to its closed loop between advertisers and transactions, which enables accurate targeting and measurement. AWS remains the leading cloud provider, while cloud computing still represents only 11% of the $4.4 trillion spending on global IT products and services according to Gartner in 20223. Areas such as logistics and health care present additional optionality.

We also utilized flows to add to our position in the rating agency and data provider, S&P Global Inc . The issuance outlook is improving, driven by non-financial corporate bonds growing by double digits, as issuers have become more adaptive to higher rates leading to narrower spreads and a more open capital market.

The favorable comparison to last year has also contributed to this trend, as debt issuance was significantly impaired in 2022. There is also a significant number of debt maturities approaching that will require refinancing. A rebound in equity markets has further supported asset-based fees, while strong derivative trading has also contributed positively. We are also pleased with the integration progress of IHS Markit, with over 90% of cost synergies already achieved. Over the long term, the company should continue benefiting from the secular trends of increasing bond issuance, growth in passive investing, and demand for data and analytics, while enjoying meaningful and durable competitive advantages that, in our view, are only strengthening following the merger with IHS Markit.

During the quarter, we also added to our Alphabet Inc. position. While there is a wide range of outcomes around the potential implications of the advancements in GenAI on Google's search business, we believe that the risk/reward at the current valuation is skewed to the upside. Alphabet has world class talent in AI between DeepMind, Google Brain, and core Google (note that it was Alphabet's researchers who released the Attention Is All You Need paper, on which the modern large language models are based4). With its Android platform, YouTube, and its advertising assets, the company has data on an unmatched scale with which to train its AI models and has an existing platform on which to distribute them.

Lastly, we also continued building two of our newer positions, the largest independent broker-dealer, LPL Financial Holdings Inc. ( LPLA ), which remains well positioned to win market share in a growing industry as advisors continue shifting to independent broker dealers; and the leading alternative asset manager, Blackstone Inc. ( BX ), which we believe stands to benefit from the continued shift to alternative asset management. Jamie Dimon, JPMorgan's CEO, described how the potential changes in regulatory requirements from banks (such as increasing capital rations to 20%) during the company's most recent earnings could provide an additional boost for alternative asset managers: "This is great news for hedge funds, private equity, private credit, Apollo, Blackstone, and there's dancing in the streets."

{kind=link}

Outlook

Regular readers of this investment letter know our skepticism about outlooks. While we generally have a sense of when our stocks are inexpensive and when they are not, we have never had good insight on the timing of when that might change. No one needed to read our letters to know that a Zero Interest Rate Policy (or ZIRP) was not sustainable but there isn't a single expert we know of who predicted it would last for 13 years and end in 2021. We mentioned earlier how in the five-and-a-half years since the inception of the Fund we have experienced two bear markets, a global pandemic, the fastest rate hiking cycle in U.S. history, a war in Europe, a likely end to globalization, and the geo-political tensions with the wider range of possible outcomes then we could ever imagine. By any measure, the market volatility experienced over this time frame can be described as extreme. And yet… the S&P 500 Index returned 16.9% so far in 2023, 19.6% over the last year, 14.6% annualized over the last three years, and 12.3% annualized over the last five years. We are not suggesting that investors should be expecting these types of returns for the rest of time, but rather that they were entirely unpredictable, especially considering the circumstances in which they were achieved.

The most recent economic reports continue to show that inflation is moderating. The latest CPI reading for the year ended June 2023 came in at 3.0%, the lowest reading in over two years. Interestingly, inflation has declined roughly as rapidly as it has increased. Similarly, the 10-year break-even inflation remains steady in the 2.0% to 2.5% range and real rates (as measured by 10-year TIPS), while moving up from the lows of around 1.1% reached shortly after the collapse of Silicon Valley Bank, are still in favorable territory at approximately 1.5%. While the Fed is expected to raise rates a quarter of a percent once or twice more, it is clear that we are closer to the end of the rate hike cycle. That, coupled with most of our companies reporting stabilizing trends in their businesses and leaner cost structures, creates a favorable backdrop for growth stocks in our view.

As we discussed earlier, while investor psychology will likely continue to swing from side to side, we pay more attention to companies' competitive advantages, to the size and durability of their growth opportunities, and to how well management teams are executing against those things. Said another way, we pay much more attention to fundamentals and try to use market/investor psychology as an opportunity to buy stocks at bargain prices or reduce/sell them when we think they are well ahead of the business' intrinsic values.

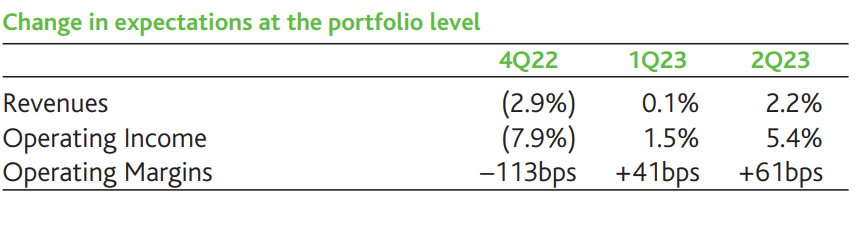

During the second quarter, weighted average 20235 revenue expectations for the portfolio for have increased by 2.2% after rising by 0.1% in the first quarter and declining by 2.9% in the fourth quarter of 2022. Margin expectations have risen by 61bps after rising by 41bps in the first quarter and declining by 113bps in the fourth quarter of 2022, driving an overall 5.4% uplift to operating income expectations for 2023 during the second quarter after a 1.5% increase in the first quarter and 7.9% decline during the fourth quarter of 2022. As of the end of the second quarter, the weighted average revenue growth for the portfolio for 2023 is expected to be 10.1%, while earnings are expected to grow by 18.1%6. The change in expectations for these fundamentals at the portfolio level is summarized in the following table:

{kind=link}

Every day, we live and invest in an uncertain world. Well-known conditions and widely anticipated events, such as Fed rate changes, ongoing trade disputes, government shutdowns, and the unpredictable behavior of important politicians the world over, are shrugged off by the financial markets one day and seem to drive them up or down the next. We often find it difficult to know why market participants do what they do over the short term. The constant challenges we face are real and serious, with clearly uncertain outcomes. History would suggest that most will prove passing or manageable. The business of capital allocation (or investing) is the business of taking risk, managing the uncertainty, and taking advantage of the long-term opportunities that those risks and uncertainties create. We are confident that our process is the right one, and we believe that it will enable us to make good investment decisions over time.

Our goal is to invest in large-cap companies with, in our view, strong and durable competitive advantages, proven track records of successful capital allocation, high returns on invested capital, and high free-cash-flow generation, a significant portion of which is regularly returned to shareholders in the form of dividends or share repurchases. It is our belief that investing in great businesses at attractive valuations will enable us to earn excess risk-adjusted returns for our shareholders over the long term. We are optimistic about the prospects of the companies in which we are invested and continue to search for new ideas and investment opportunities.

Sincerely,

Alex Umansky, Portfolio Manager

Footnotes

- Calculated using weighted average earnings (or equivalent multiples for Financials) based on FactSet consensus estimates for the next 12 months.

- Monthly Retail Trade - Quarterly Retail E-Commerce Sales Report

- Gartner Forecasts Worldwide Public Cloud End-User Spending to Reach Nearly $600 Billion in 2023 Gartner Forecasts Worldwide IT Spending to Grow 5.5% in 2023

- Attention Is All You Need

- Based on weighted average FactSet consensus estimates for our holdings.

- Excluding Amazon, which is expected to shift from negative EPS to positive EPS in 2023, and Brookfield Corporation, which is valued on a sum-of-the-parts basis.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds. You may obtain them from the Funds' distributor, Baron Capital, Inc., by calling 1-800-99BARON or visiting www.BaronFunds.com. Please read them carefully before investing.

Risks: The Fund invests primarily in equity securities, which are subject to price fluctuations in the stock market. In addition, because the Fund invests primarily in large-cap company securities, it may underperform other funds during periods when the Fund's securities are out of favor. The Fund may not achieve its objectives. Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager's views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them.

This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron Fifth Avenue Growth Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA).

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Baron Durable Advantage Fund Q2 2023 Shareholder Letter