ULTA - Bath & Body Works: A Compelling Growth Story

Summary

- After the Victoria's Secret spin-off, Bath & Body Works shows a compelling growth story.

- Over the last decade, the growth story has been shrouded in a holding company.

- The company has a loyal customer base and expects modest growth with a high ROIC.

Bath & Body Works ( BBWI ) is an American specialty retailer focused on Home Fragrance and Body Care products. The company used to be known as L Brands up until March 2021. Under the L Brands umbrella, the company had its struggling Victoria's Secret ( VSCO ) brand dragging down results. Now as a standalone company, BBWI could offer an enticing investment opportunity. In this article, I'll go through the business and why it could be an attractive buying opportunity in this market.

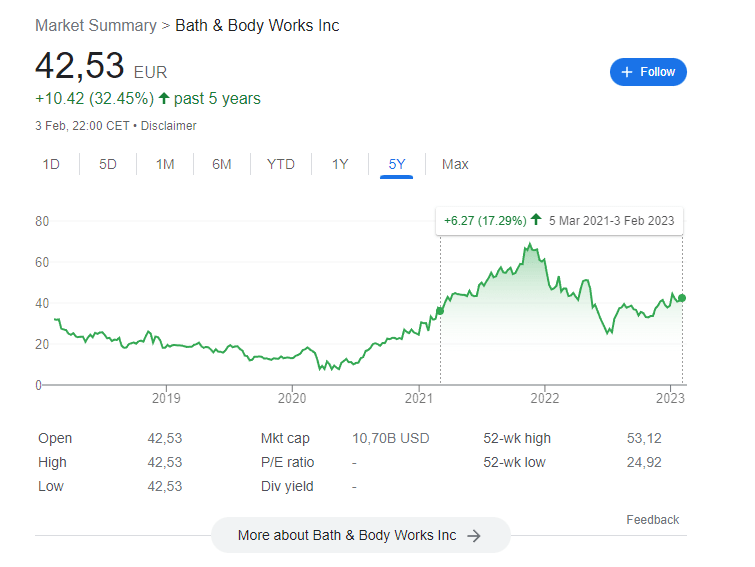

BBWI past performance (Google)

{kind=link}

The Victoria's Secret Spin-off

In February 2020, L Brands announced a sale of 55% of its ownership in Victoria's Secret to private equity firm Sycamore Partners. After the deal fell through, the company eventually decided to spin off Victoria's Secret as a standalone public company and rename L Brands to Bath & Body Works. This is where we are now: A focused company on its top brand.

Bath & Body Works

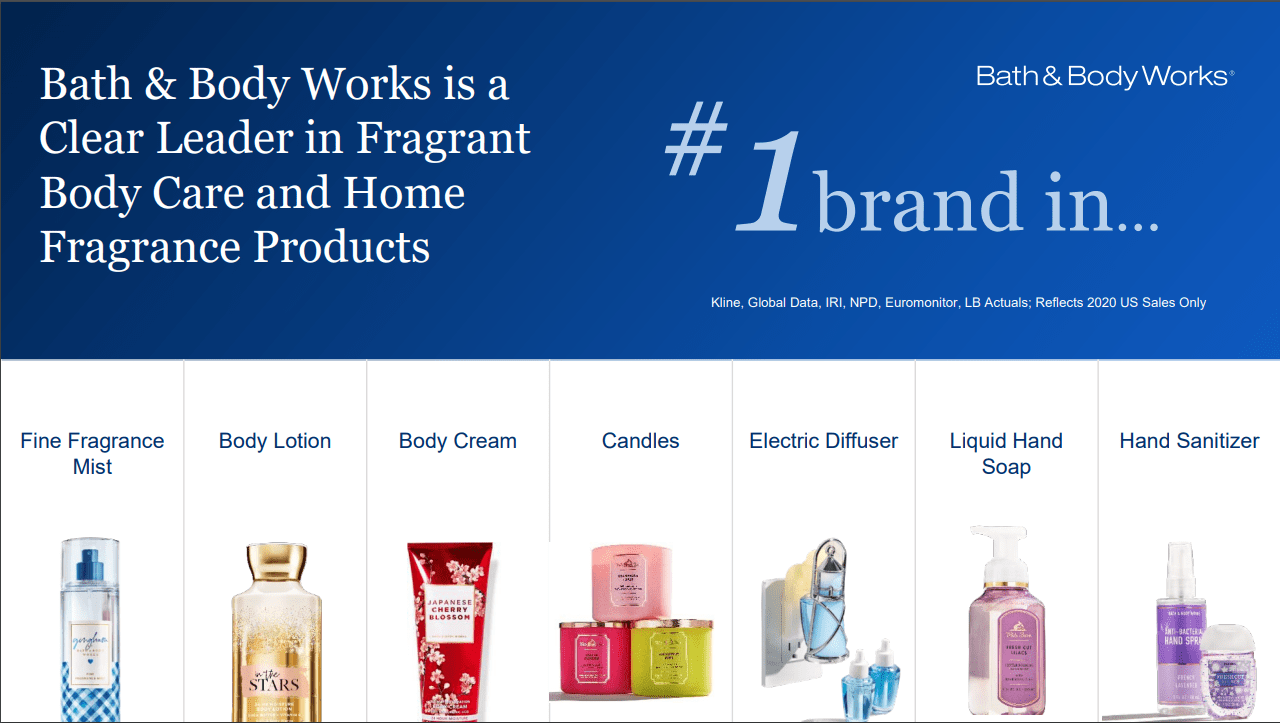

BBWI is America's #1 Specialty retailer for Home Fragrances and Fragrant Body Care. The company generates around $7.7 billion in sales driven by 45% Home Fragrances, 35% Body Care & Fragrances, 15% Soaps & Sanitizers and the remaining 5% from other items. BBWI has created a strong brand over the years and is the #1 US brand for several of its markets. The company operates in attractive markets focused on beauty and well-being. Focused companies in this industry with high customer loyalty can have long runways of growth, as evidenced by the success story of Ulta Beauty ( ULTA ) for example.

BBWI brand overview (BBWI Investor Handout)

{kind=link}

A loyal customer group

The company managed to create a loyal customer base with 80% brand awareness for Women aged 18-59 and 60% for men in the same cohort. That translates to 60 million customers that transact on average three times a year at one of their stores, purchasing seven items at an average spend per visit of $41.

To increase the annual spend per customer and increase retention, the company also rolled out a national loyalty program, my Bath & Body Works . In the latest earnings report(pages 2-3) , the company shared some very encouraging early findings from the rollout:

According to BBWI's loyalty partner Bond Brand Loyalty, the Bath & Body Works rollout shows world-class loyalty to the brand and program, leading to an unprecedented enrollment rate. In just a few months, the program had 21 million members enroll (remember the 60 million customer base), representing more than 1/3 of customers and 2/3 of US sales. This is already a strong indicator that the loyalty program manages to capture the high-value customers for BBWI, increase their experience, and convince them for more visits and purchases. This should lead to positive same-store sales (SSS) developments.

Growing the online sales channel

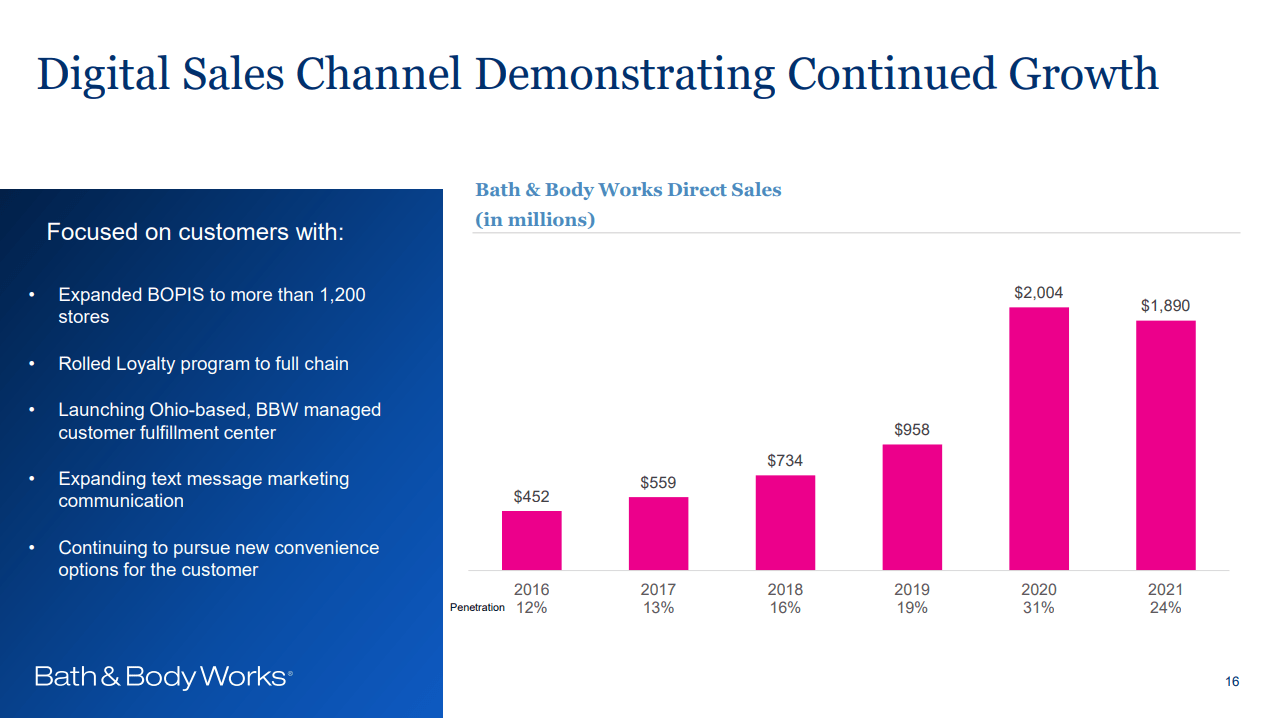

For many years the company has been pushing its Online strategy. Particularly 2020 saw explosive growth due to the pandemic. Online penetration grew from 12% to 24% of sales over the last six years. With a digital distribution channel, the company also has a new way to leverage its Supply chain. The company has five permanent third-party fulfillment centers and an additional 5-6 facilities than can support during peak capacity, like the Christmas season. The company also owns three distribution centers and can leverage its ample store coverage throughout the US. Online sales are a highly profitable channel for BBWI and can also leverage the loyalty app.

Online sales channel growth (BBWI Investor Handout)

{kind=link}

Rationalizing the store footprint

Over the last few years, the company has worked on optimizing its large physical store footprint. With a store count of around 1700, the company has an extensive network and a lot of potential for optimization. Since 2016 the company closed over 150 underperforming stores, particularly in lower-tier mall venues and opened over 240 new stores, primarily in top-tier malls and non-mall venues. This has led the sales per average selling square foot to increase by over 50% from $831 in 2016 to $1220 in 2021, but we have to keep in mind that the majority of the increase happened in 2021 when sales jumped from $916 to $1220 per square foot.

Internationally, the company is also expanding with over 300 locations in over 30 countries. The international business is done via franchising agreements, where BBWI gets paid royalties and the franchisees take care of the rest.

Strong growth track record

Over the last decade, BBWI managed to increase sales from $2.6 billion to $7.8 billion in 2021. For the FY 22 management, however, guides a mid-single-digit decline in sales due to the challenging environment. Profits took a nose-dive as the company hasn't been able to control costs well, with EPS for the first nine months of 2022 coming in at $1.56 versus $2.67 in 2021. This comes from a shrinking gross margin due to inflationary pressures. Given the long-standing track record and the highly unusual year 2021 was, I'll give management the benefit of the doubt and expect to accelerate over the medium to long term, where the company expects mid to high-single-digit sales and earnings growth.

A healthy balance sheet

Due to BWWI's large store count and expansion, we must look at the balance sheet. Like many retailers, the balance sheet is levered, with $6.07 billion in debt versus just $300 million in cash. This is a sizable net debt position at a market cap of just $10.7 billion. Fortunately, the company generates plenty of cash with $1.98 billion in EBITDA, which leaves the company at a 2.4 times net debt/EBITDA ratio, which is okay considering the large store count. Capital Expenditures are relatively low at $280 million and FCF at $831 million is also healthy. Unlike many other retailers, BBWI's inventories didn't bloat up, still at a moderate $1.27 billion. The cash interest payments in the last 12 months accounted for $354 million, well covered by both EBITDA and FCF. The maturity profile also doesn't raise red flags, with the first maturity coming in 2025 at just $300 million.

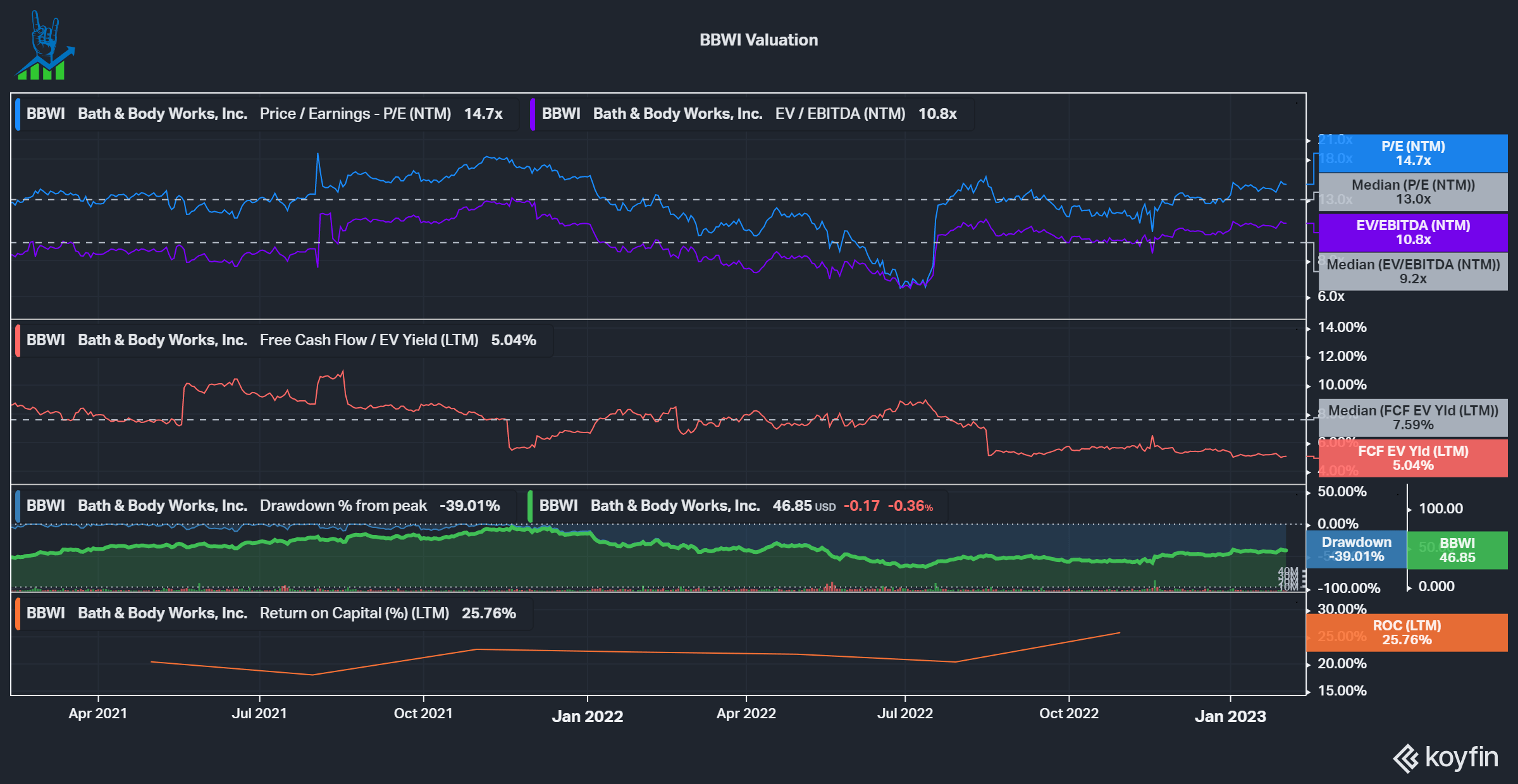

Valuation

For BBWI, we only have a short history as a focused public company. We can see that the company currently trades above its historical short historical averages but still looks attractive at a 10.8x forward EV/EBITDA and a 5% FCF yield. The company also generates a high Return on invested capital of over 20%, well above its 10% WACC . Doing a back-of-the-napkin calculation using FCF + expected FCF growth, we can approximate what returns BBWI stock could give investors. If we believe the three to five-year financial target of mid to high single digits operating income growth, we can estimate that FCF will grow somewhere along those lines. This leaves us with a 5% FCF yield and somewhere around 4-9% FCF growth. This should leave us with returns of around 9-14% roughly. To conclude, BBWI is an interesting business now, after the spin-off, trading at a compelling valuation for a potentially market-beating return and additional upside through growth initiatives like the royalty program.

{kind=link}

For further details see:

Bath & Body Works: A Compelling Growth Story