BAYZF - Bayer AG: Potential To Double Over 12-18 Months

Summary

- Bayer AG is a $50-billion multinational life sciences conglomerate based in Germany.

- The company is trading at a discount of at least 20% compared to its peers as well as to its historical multiples.

- 3 catalysts could reinvigorate the stock and unlock value: new management, a group restructuring, and finally more clarity on the Monsanto litigations.

- We estimate the potential best-case returns 130% vs. current share price. We rate Bayer AG a "Strong buy".

Investment Thesis

Bayer AG (BAYZF) (BAYRY) is undervalued by "Mr. Market" - shares in Bayer trade at a discount of at least 20% to its peers and the historically low trading multiples further present an attractive entry point for opportune investors. Bayer has been a target of investor activism lately, which forced the removal of the distrusted CEO Baumann. Investors are further pushing for a breakup of the company to unlock value from what is a typical conglomerate-discount-situation.

About Bayer

Bayer AG is a $50 billion multinational pharmaceutical and life sciences company headquartered in Leverkusen, Germany. The company was founded in 1863 and has grown to become one of the largest pharmaceutical companies in the world.

Bayer operates in three main business segments: pharmaceuticals, consumer health, and crop science. The pharmaceuticals segment focuses on developing and manufacturing prescription drugs, while the consumer health segment produces over-the-counter products for consumers. The crop science segment provides agricultural products and services to farmers and other agricultural businesses.

Bayer has a long history of innovation, with notable contributions to the development of aspirin, the world's first mass-produced synthetic dye, and the first oral contraceptive pill. The company's R&D efforts continue to focus on addressing some of the world's most pressing health challenges, such as cancer, cardiovascular disease, and infectious diseases.

The company is a stable, profitable and cash-generative business with operating margins between 16-17% over the last 3 years despite all the global turbulences. Its gross profits stayed stable at around 62% during last year even after the run up in input prices, which shows evidence of pricing power.

The toxic Monsanto takeover

Bayer took over US-based crop science competitor Monsanto for $60 billion in 2017 in what has turned out to be a literally toxic deal. The acquisition was forced upon Bayer by its then-new CEO Werner Baumann. The takeover led to a series of multi-billion-dollar litigations against Bayer because of Monsanto's Roundup product allegedly causing cancer. The takeover and its subsequent problems severely impaired the trust in Bayer's management. Shareholders voted at the 2019 shareholder meeting against the board and Singapore's sovereign wealth fund Temasek called in 2022 for the removal of CEO Baumann .

The share price has been receiving a beating since the takeover and Bayer's share price fell by 50%. However, BAYZF stock seems to be bottoming out, having traded sideways since mid-2020.

A Restructuring of Bayer Is In The Cards

Bayer's undervaluation has also caught the attention of activist shareholders such as Jeff Uben's Inclusive Capital, Bluebell Capital Partners or Elliott Management . Their initiatives recently culminated in the early termination of Baumann's contract and nomination of Bill Anderson (56) as the new CEO.

Bill Anderson is an outsider, joining Bayer from Roche ( RHHBY ), where he was CEO of Roche's pharma business and previously CEO of Genentech. The change should instill long-lost trust in the management of Bayer, attract new investors and open up the company for a shake-up. Capital markets reacted positively to Anderson's appointment: the share price jumped 6% as investors pin high hopes on Anderson .

Anderson's nomination is just a first step, however. Bluebell as well as traditional German fund managers such as Union Investment or Deka have been voicing concerns about the stock and calling for a re-think of the group's structure, which would have been unthinkable under Baumann who resisted a breakup. With Baumann removed and Anderson at the helm, nothing is off the table anymore.

The key rationale behind a restructuring is Bayer's conglomerate discount, which we estimate very conservatively at a minimum of 20%. JPMorgan puts the discount at around 25% and Credit Suisse at around 40%.

Bayer is no newbie to corporate restructurings - it has spun-off in 2015 its Bayer MaterialScience unit under a separate company called Covestro.

Various scenarios have been put forward with regards to a restructuring. One particular break-up scenario we like is a separation of Crop science and its potential re-listing in the US and sale or spinoff of Consumer health from Pharma. This would provide the company and its investors with several advantages:

- Opening up to a broader shareholders base increasingly focused on pure-play businesses

- Separation of the toxic Monsanto-Bayer Crop science brand from the Pharma & Consumer health segments

- Containment of litigation costs within the Crop science business and ring-fencing from Pharma & Consumer health

- Separation of Crop Science is also potentially relevant with respect to ESG-investing. Some ESG research companies consider the situation around Roundup and glyphosate as a societal, legal and health-related problem. For example, Morningstar's Sustainalytics deems it controversial and rates Bayer's ESG risk as Medium with a rating of 29.6, only 0.4 points from a High-rating (what a coincidence, close but no cigar)

- Depth of US equity markets would favor a high multiple for Crop sciences

Indeed, with Pharma-guy Anderson in the lead, we assume that Bayer 2.0 will be built around Bayer's Pharma business. Also, given Pharma's size, we deem the likelihood of a sale of the unit as unlikely. Megamergers in pharma have become rarer and with a price tag of $60-90 billion, Bayer Pharma would face issues in finding a buyer.

A sale or spinoff of Consumer health, which could fetch an EBITDA multiple in the high teens, seems more plausible. In such a scenario, Bayer would be basically following in GSK's ( GSK ) footsteps, which recently spun-off its Consumer healthcare business into Haleon ( HLN ).

Anderson will join the company on April 1 and it may take time for a shakeup to unfold. We don't expect to see more details or hear more rumors until late Q2 or Q3.

End of Roundup litigations in sight?

As a cherry on top, it looks like investors are having increasingly more clarity about the Monsanto litigations. The company has been able to address 3/4 of the cases brought against it:

[...] of the approximately 138,000 claims in total which have been brought, approximately 107,000 have been settled or are not eligible for various reasons

Source: Bayer

The benefit of an end of the litigations is increased transparency for investors about the total amount of liabilities stemming from the lawsuits, asides from reputational issues. We estimate the litigation provisions at a total of $10 billion.

Valuation

Bayer currently trades at a historically low multiple as well as at a discount to its peers.

Its shares are priced at $63, down around 60% from its pre-Monsanto 2015 highs. The market thus currently values the company at around 7.3x EBITDA and 13.5x earnings (all TTM based).

{kind=link}

With a current multiple of around 7x EBITDA, the stock trades at a historically depressed multiple. Prior to Covid, the shares traded in a range of 9-17x EBITDA (I apologize for the chart but I am unable to scale the y-axis with Seeking Alpha's tool).

{kind=link}

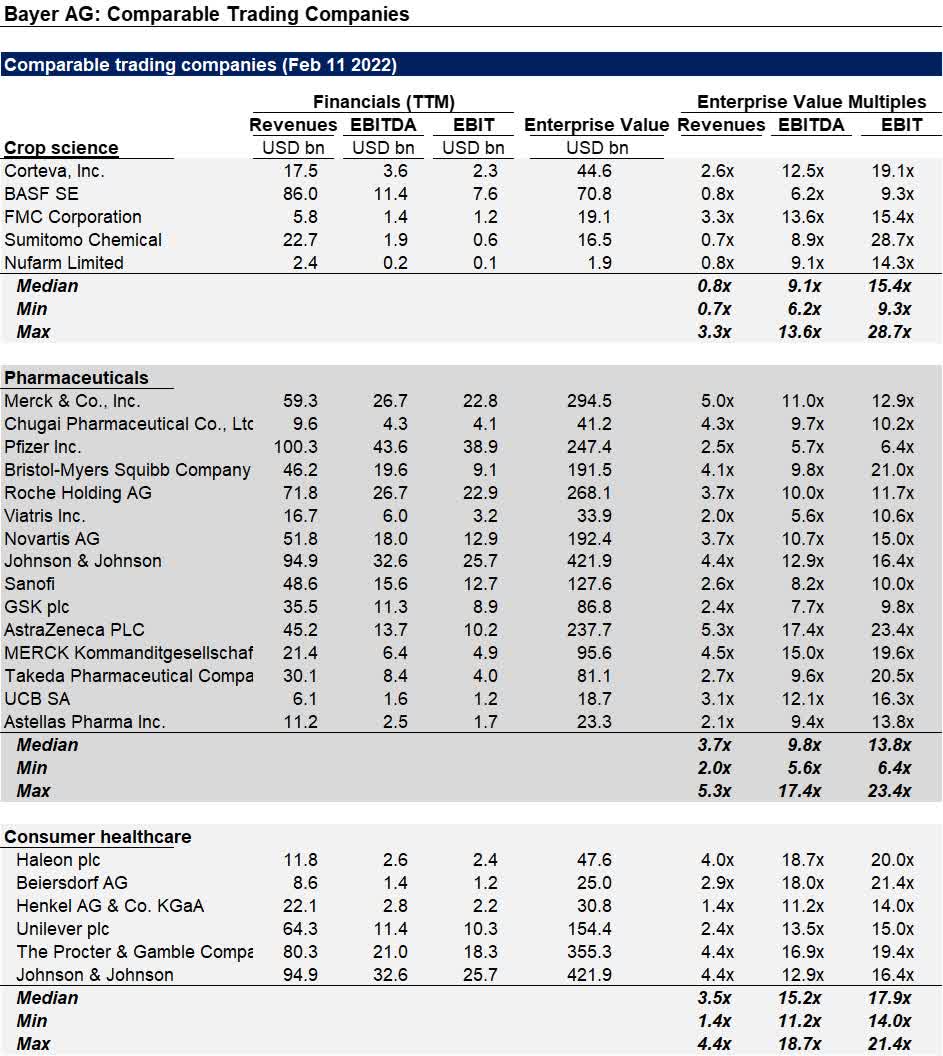

Bayer also trades at a substantial discount to its peers (see detailed table below).

- Pharma peers trade at a median EBITDA multiple of 10x

- Consumer health businesses trade between 11-16x EBITDA

- Crop science / chemical companies trade between 6-14x EBITDA. US crop science company Corteva ( CTVA ), a company similar to Bayer's crop science unit, trades above 12x EBITDA

Bayer AG comparable trading companies valuation ( Seeking Alpha, Author's analysis)

{kind=link}

Why is Bayer undervalued? We assume 4 primary reasons for the discount:

- Distrust of management

- The uncertainty about the total liabilities arising from the Monsanto lawsuits

- Investors preference towards industry-pure-plays

- Listing in Germany, which is traditionally less equity-market focused

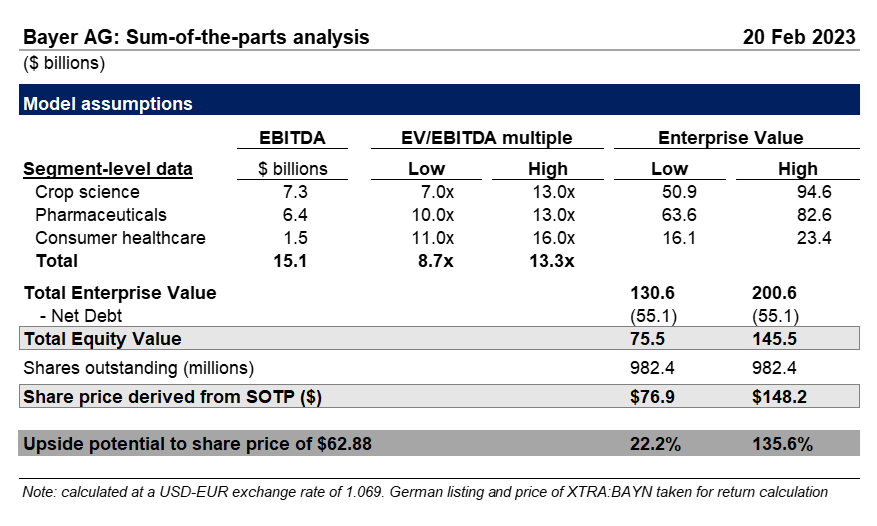

Bayer's SOTP analysis (Sum-of-the-parts)

We believe that Bayer as a whole is being valued less than is the sum of its parts. We believe the company offers enough of a margin of error to be a really attractive investment.

Our bear case arrives at a share price of $77, which represents an upside of around 20% to current levels. The scenario assumes merely the sale of the Consumer Healthcare unit at a very conversative multiple of 11x EBITDA and a re-rating of the Pharma business to 10x while keeping Crop science at today's Group EBITDA multiple of ~7.0x. We believe Anderson's expertise in Pharma may re-invigorate investors' trust in Bayer and result in a better perception of the Pharma business and successively a more attractive valuation of the group overall.

Our Bull case works with the assumption of a complete break-up of the group and a realization of aggressive multiples for the individual segments in the upper range of the peers' multiples. A US listed Bayer Crop science could fetch a valuation of 13x EBITDA, implying a value of $95 billion, which would basically mean that investors are getting the pharma and consumer health units for free! For comparison, US-listed Crop science business Corteva, currently trades between 12-13x EBITDA. The consumer healthcare business could fetch up to 16x EBITDA in a competitive M&A transaction; and we further believe that a standalone Bayer Pharma could be re-rated up to 13x EBITDA. This scenario implies a share price of $149 and thus an upside potential of 137% to today's share price.

All of our calculations assume a conservatively high net-debt of around $55 billion driven by various non-debt adjustments.

Bayer AG investor relations, author's estimates and analysis

{kind=link}

Risks

Our thesis relies on a re-rating of the group or its parts in order to realize capital gains. Everything that could potentially torpedo our proposed shake-up represents key risks for our thesis.

Bill Anderson, as a non-German outsider, may struggle in the fighting that is going to ensue at Bayer because of the potential breakup. He may struggle to re-institute shareholder trust in particular in the Pharma business that may turn out to be a value trap.

German politicians as well as employee unions will clamor against a break-up , especially the separation of Pharma and Consumer health. However, as mentioned earlier, Bayer already spun-off business units in the past (its Material Sciences unit called now Covestro), so we reckon the employee unions current behavior is politically driven and a consensus can be reached.

New, (though unexpected) Monsanto litigation could ensue, dragging down the share price and making a separation of Crop sciences a tough pill to swallow, although the likelihood of such event is impossible to predict precisely.

However, despite all those risks, we still think that Bayer represents great value for money and provides for a comfortable margin of error for investors. The group is stable, profitable, cash-generating and by its nature non-cyclical. Even if none of the breakup phantasies materialize, investors are buying a company for around 13x earnings, which is relatively cheap even for German standards: the German lead index DAX currently trades above 14x earnings .

Wrapping it up

We believe that Bayer is an undervalued stock. The share price has been receiving a beating for the past couple of years, but now that key roadblocks have been removed (more clarity on Roundup litigation costs and a new CEO in place), the stock could significantly gain in value once a restructuring gets under way. We see potential upside of up to 130% for investors over the next 12-18 months. We rate Bayer a Strong Buy.

(If you are considering an investment in Bayer, we would recommend looking into purchasing stock at German stock exchanges (e.g. Xetra, ticker BAYN) because Bayer's ADRs and common stock are traded in the US over the counter and thus suffer from lower liquidity.)

For further details see:

Bayer AG: Potential To Double Over 12-18 Months