BAYZF - Bayer: Improving Business And Still Undervalued

Summary

- Bayer reported great results for fiscal 2022 with sales growing in the double digits, core EPS growing 22% and all three segments contributing to growth.

- And although Bayer is a little cautious for fiscal 2023 and expecting EBITDA and core EPS to decline, we can be optimistic about its long-term growth potential.

- Management also increased the dividend by 20% to an annual dividend of €2.40.

- The stock remains deeply undervalued and even when calculating with rather cautious assumptions, the stock should be worth between €80 and €90.

Germany is probably not the most interesting market when talking about new technologies or artificial intelligence and clearly lagging in these sectors. But Germany might be interesting to invest as many stocks are trading for more reasonable valuation levels than peers in the United States. While the United States was trading at a CAPE ratio of 25.6, Germany was trading at a CAPE ratio of 13.4 as of January 2023.

And while Germany is lagging in some sectors, we have several businesses dominating the “old industry” and one of them is the pharmaceutical and life science company Bayer AG ( BAYZF ). Despite the terrible performance in the last few years and the criticism about the Monsanto acquisition and the discussion if glyphosate is causing cancer, Bayer is a well-performing business and after a new CEO was appointed and Bayer reported strong annual results for fiscal 2022, the stock might finally move higher in the years to come.

New CEO

One of the major news stories in the last few weeks was the retirement of CEO Werner Baumann. And although Baumann’s performance was not great – at least when measured by looking at the stock price – I don’t know if the criticism he had to endure was justified. Of course, under Baumann Monsanto was acquired which led to the declining stock price, caused a series of multi-billion-dollar litigations against Bayer (which are still not resolved) and damaged the reputation of Bayer a bit. As a result, many investors seemed to question Bayer’s management.

The new CEO will be Bill Anderson, who will join the company on April 1, 2023, and is the former head of Roche’s (RHHBY) Pharmaceutical Division. Baumann, who has worked 35 years for Bayer, is set to retire at the end of May 2023 to ensure a smooth transition between the two CEOs.

Annual Results

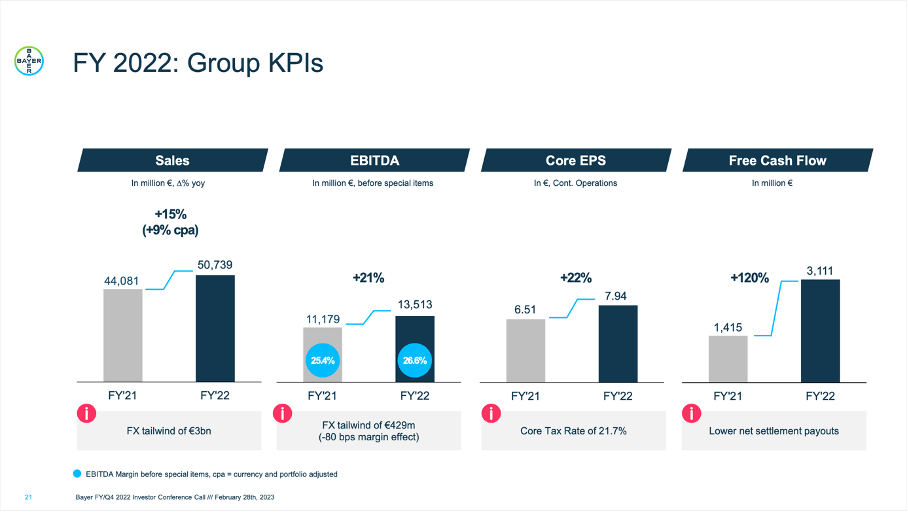

Aside from announcing a new CEO, the annual results Bayer reported on Tuesday was the second major story. In fiscal 2022, Bayer generated €50,739 million in sales and compared to €44,081 million in fiscal 2021 this resulted in 15.1% year-over-year growth (with organic sales growth still being 8.7%). EBITDA more than doubled from €6,409 million in fiscal 2021 to €13,515 million in fiscal 2022 and when looking at EBITDA before special items, we saw an increase from €11,179 million in fiscal 2021 to €13,513 million in fiscal 2022 – an increase of 20.9% year-over-year. And diluted earnings per share increased from €1.02 in fiscal 2021 to €4.22 in fiscal 2022 and when looking at the more important core earnings per share, Bayer reported 22.0% year-over-year growth from €6.51 in the previous year to €7.94 in fiscal 2022. Finally, free cash flow also improved from €1,415 million in fiscal 2021 to €3,111 million in fiscal 2022.

{kind=link}

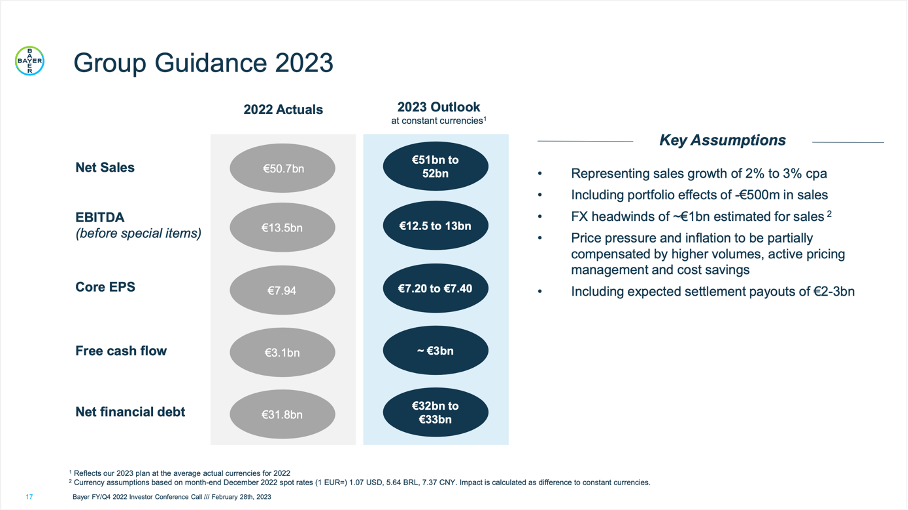

And while Bayer reported strong results for fiscal 2022, the guidance for fiscal 2023 can rather be seen as a disappointment. Net sales are expected to grow slightly to about €51 billion to €52 billion while EBITDA and core earnings per share are expected to decline in the single digits.

{kind=link}

Dividend

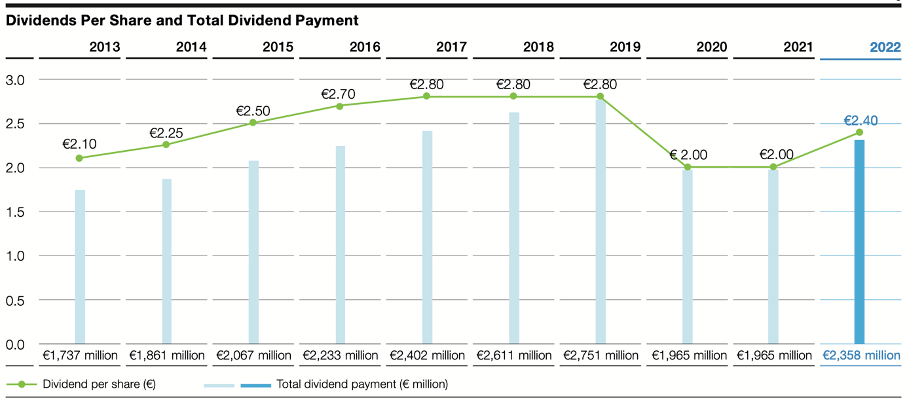

While the guidance was rather underwhelming, investors might be pleased with the dividend raise. After Bayer cut its dividend for fiscal 2020 from previously €2.80 to only €2.00 it is now increasing the dividend again by 20% to €2.40. This is resulting in a payout ratio of 57% when using diluted earnings per share. However, when using Bayer’s core EPS of €7.94, the payout ratio is only 30%. And with a share price around €56 at the time of writing, we get a dividend yield of 4.3% for Bayer.

{kind=link}

Pharmaceutical Business

Sales for the pharmaceutical segment increased with a solid pace from €18,349 million in fiscal 2021 to €19,252 million in fiscal 2022 – an increase of 4.9% year-over-year. EBITDA before special items also increased slightly (1.6% year-over-year) from €5,779 million in the previous year to €5,873 million in fiscal 2022. Growth was especially driven by Eylea growing 9% with all regions contributing to growth, however it was offset by Xarelto declining due to pricing pressures in the UK and loss of exclusivity in Brazil.

Bayer Investment Case 11/22 Presentation

{kind=link}

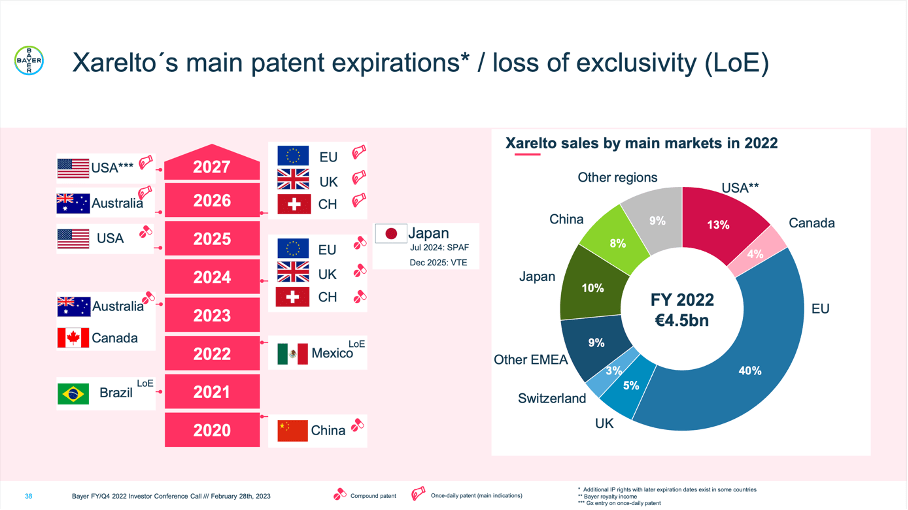

And Xarelto will continue to have a negative effect on pharmaceutical sales as it is the most important product for Bayer (in fiscal 2022 it generated €4,516 million and is responsible for almost 10% of Bayer’s total revenue and for 28% of the revenue of the pharmaceutical segment). In 2023, patent losses will only occur in Canada (responsible for 4% of sales) and Australia, but in 2024 and 2025 Bayer will lose patents in key markets probably leading to steeply declining sales.

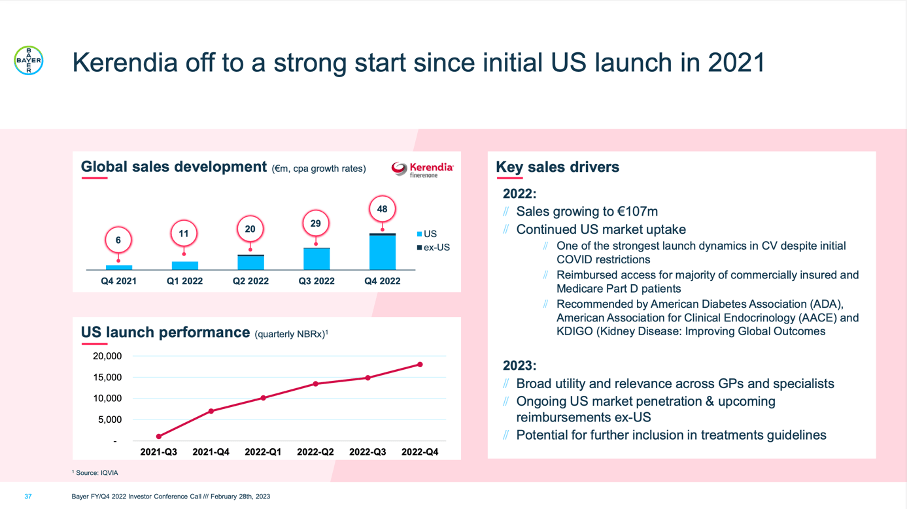

However, Bayer is confident it can compensate the decline by launching new products. During the 41 st J.P. Morgan Healthcare Conference , Stefan Oelrich – the head of Bayer’s pharmaceutical division – was quite optimistic. Bayer announced it is raising the combined new sales forecast for key growth drivers in its pharmaceutical portfolio to over €12 billion. These key growth drivers include Kerendia, which reported €108 million in sales in fiscal 2022. In Q4/22, sales increased 700% compared to the same quarter last year and 66% growth quarter-over-quarter. Peak sales are expected to be above €3 billion.

Bayer Investment Case 11/22 Presentation

{kind=link}

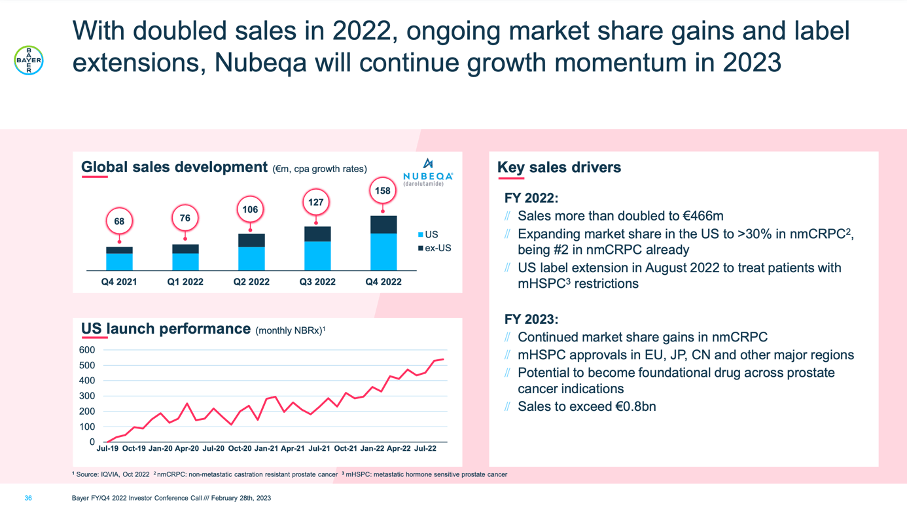

A second growth driver might be Nubeqa, which was able to double sales in 2022 and reported €467 million in revenue in fiscal 2022. In Q4/22, sales increased 132% compared to the same quarter last year and quarter-over-quarter, revenue increased 24%. Peak sales are also expected to be above €3 billion.

Bayer Investment Case 11/22 Presentation

{kind=link}

Aside from the two already launched products, Elinzanetant is expected to launch in 2025 and peak sales are expected to be at least €1 billion. The highest expectations are for its oral factor Xia inhibitor Asundexian for which the Phase III program started recently. The launch is expected for 2026 and for this potential first-in-class, once daily, oral small molecule FXIa inhibitor peak sales are estimated to be above €5 billion. In a statement , Bayer is claiming:

A step-change in growth is expected from oral factor XIa (FXIa) inhibitor asundexian. With the potential to act as distinct option for the prevention of thrombosis and ischemic strokes, asundexian has projected peak sales of more than five billion euros. It is estimated that around 40 percent of eligible patients are either not treated with direct oral anticoagulants or undertreated as these patients assess the bleeding risk to be higher than their need for thrombosis prevention.

Crop Science

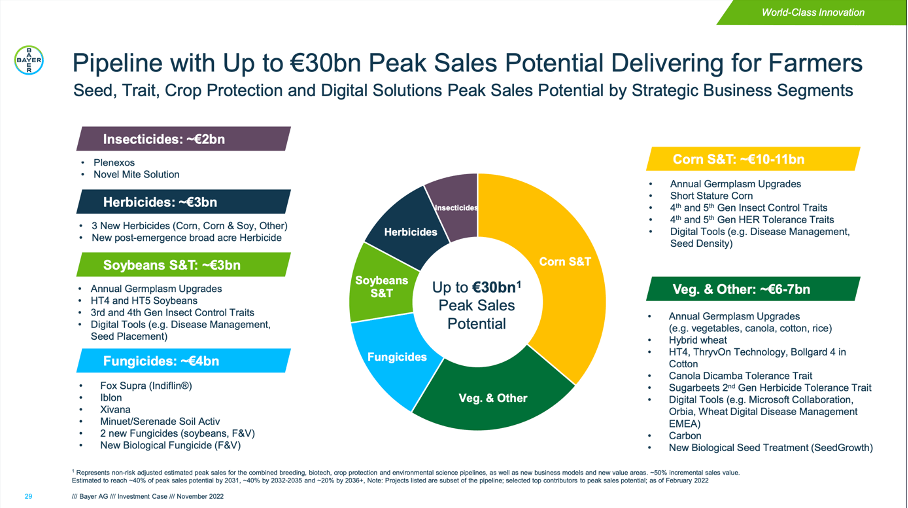

While the pharmaceutical segment certainly had a solid performance, growth in fiscal 2022 was especially driven by the crop science segment. Sales increased from €20,207 million in fiscal 2021 to €25,169 million in fiscal 2022 – resulting in 24.6% year-over-year growth and EBITDA before special items increased 46.2% year-over-year from €4,698 million in the previous year to €6,867 million in fiscal 2022. And especially herbicides were growing with a high pace (44% growth) and this was largely driven by glyphosate pricing due to tight supply.

Bayer Investment Case 11/22 Presentation

{kind=link}

And although management is a little cautious for fiscal 2023 and expecting only 3% organic sales growth as glyphosate-based herbicide sales are expected to decline in the double digits as pricing will most likely normalize, we should expect solid mid-to-long-term growth for the segment as the crop science segment will profit from several megatrends in the coming decades.

Bayer Investment Case 11/22 Presentation

{kind=link}

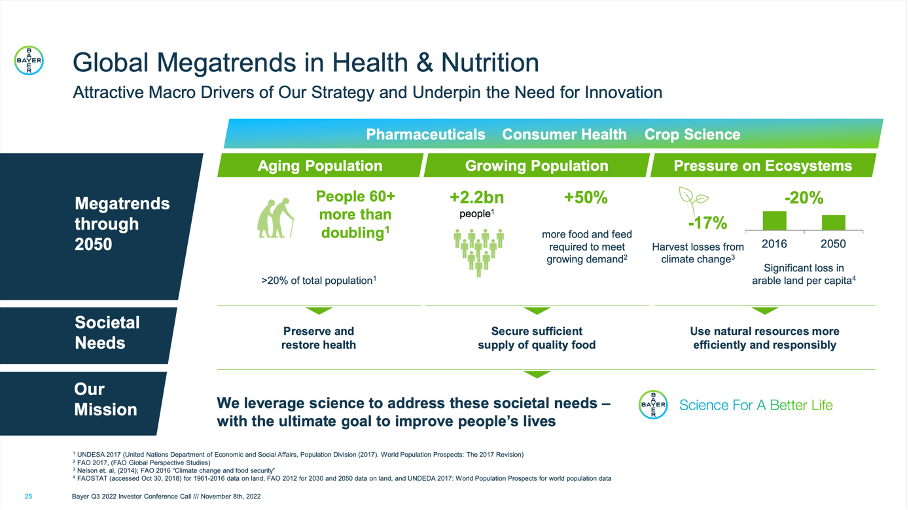

The growing and aging population will lead to higher demand for food and to produce these amounts of food, Bayer’s crop science products are necessary. Until 2050, population is expected to grow by 2.2 billion people and about 50% more food is required to meet the demand. And especially as the pressures on the ecosystem will increase in the years to come (harvest losses from climate change are expected to be around 17% and arable land per capita will decrease about 20% till 2050), the demand for Bayer’s crop science products will increase.

And not only the crop science segment will profit but also the pharmaceutical segment. The number of people above 60 is expected to more than double and in 2050, people above 60 will account for more than 20% of the total population. This will lead to an increased demand for pharmaceuticals in the coming decades.

Consumer Health

The third segment – consumer health – also performed well during fiscal 2022. Not only sales increased 14.9% year-over-year from €5,293 million in fiscal 2021 to €6,080 million in fiscal 2022, but EBITDA before special items also increased 14.9% year-over-year from €1,190 million in the previous year to €1,367 million in fiscal 2022. Growth was broad based across all regions and categories with demand being especially strong in Allergy & Cold (22% YoY growth). And while growth assumptions for 2023 are rather moderate for Bayer, the consumer health segment is expecting sales to grow about 5% in fiscal 2023 and EBITDA margin also to improve slightly.

Bayer Investment Case 11/22 Presentation

{kind=link}

Bayer’s consumer health segment is spending 4% of net sales on research & development with more than 700 scientists and innovators and in 2023 the segment will move further ahead with its Astepro launch in the upcoming US allergy season. During the last earnings call, Heiko Schipper – head of the consumer health division – also announced Bayer is planning to launch an innovative offering in personalized health later this year.

Intrinsic Value Calculation

I have written several times that I see upside potential for Bayer and that the stock is undervalued. And especially when using the core EPS Bayer is reporting, the stock is trading for only 7 times earnings at the time of writing. Even if Bayer should struggle to grow with a solid pace in the years to come, this is a ridiculously low valuation multiple for a high-quality and stable business.

But to get a better picture and determine a clear intrinsic value for Bayer, I can use a discount cash flow calculation. As basis, I often use the free cash flow of the last four quarters (in this case, €3,111 million) but Bayer is offering a free cash flow guidance for fiscal 2023 and is expecting about €3 billion in free cash flow. The main reason for the still low free cash flow is expected settlement payouts between €2 billion and €3 billion, but for fiscal 2024 Bayer is expecting free cash flow to be €5 billion or higher again. When taking these assumptions, Bayer must grow only about 2% after fiscal 2024 in order to be fairly valued right now (assuming 10% discount rate and 982.42 million outstanding shares).

While Bayer was clearly struggling in the last few years, I think we can be a little more optimistic and assume growth in the mid-single digits in the years to come. When calculating with 4% growth following fiscal 2024, we get an intrinsic value of €79.89 and when assuming 5% growth instead, the intrinsic value for Bayer is €95.31. And even when looking at the last five years where Bayer might not have performed at its highest levels, we still see sales increasing with a CAGR of 8.40% since 2018 and core earnings per share increased with a CAGR of 9.12%.

Conclusion

In my opinion, Bayer remains deeply undervalued and the market is still offering us the chance to get a German, high-quality business with an economic moat for a bargain. And even when calculating with rather moderate assumptions (only 4% growth), I see at least 40% upside for the stock.

For further details see:

Bayer: Improving Business And Still Undervalued