BAYZF - Bayer: Still A Strong Buy Despite Lowered Guidance

2023-08-22 00:06:59 ET

Summary

- Bayer reporting disappointing second quarter results with declining sales and lowered the guidance for fiscal 2023.

- The company is continuing to struggle and total debt increased again and management is now expecting no free cash flow in 2023.

- But over the long run, Bayer should profit from several headwinds and is operating in three segments with huge addressable markets.

- And in my opinion, the stock is still deeply undervalued.

Bayer Aktiengesellschaft ( BAYZF ) is an interesting company – more interesting than an investor likes to see. As investor I actually like a boring company that is not really in the news, that is constantly growing with a solid pace and is not constantly generating headlines. I also don’t look for a business that is constantly hyped or constantly in troubles.

And Bayer, which was once a solid, well-performing business, seems to be in constant trouble since 2015 and not really fitting the description of a boring, well-run company. I have been bullish about Bayer for a long time, and I remain bullish, but the problems seem to continue, and Bayer does not seem to be able to return to its previous performance.

I have covered Bayer several times in the last few years. And as Bayer recently disappointed again with its second quarter results, I will look at the positive and negative aspects once again. Bayer seems to be caught between being an established, high-quality business that has growth potential and should profit from several tailwinds and megatrends on the one side and still struggling, reporting declining sales, low free cash flow and having high debt levels on the other side.

The Bears

And as Bayer recently reported rather bearish second quarter results, I start with the negative aspects about Bayer.

Disappointing Results

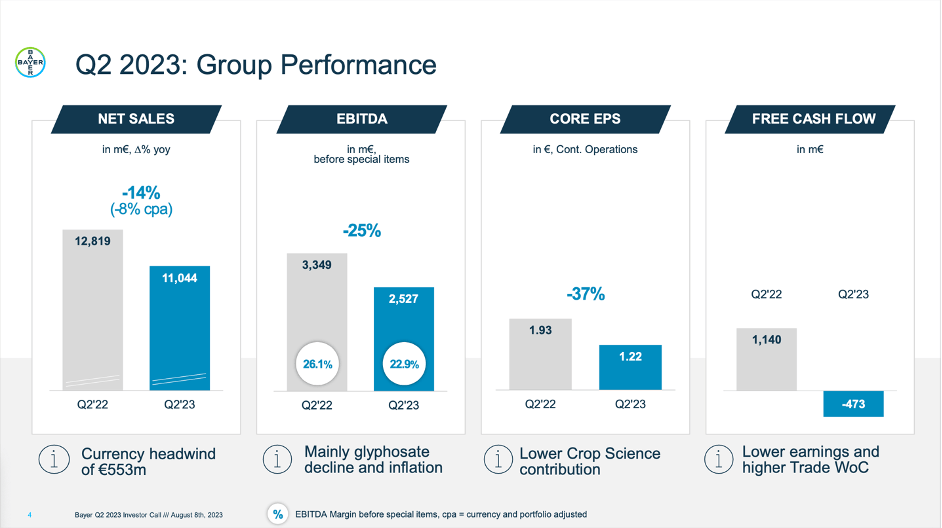

After Bayer reported great results for fiscal 2022 – I have written about the results in my last article – second quarter results -Q2 2023-were a disappointment once again. Sales declined 13.8% year-over-year from €12,819 million in Q2/22 to €11,044 million in Q2/23. And although currency tailwinds had a negative impact, FX- and portfolio-adjusted sales declined 8.2% year-over-year.

{kind=link}

When looking at EBITDA before special items (an adjusted metric) it declined from €3,349 million in the same quarter last year to €2,527 million this quarter – resulting in 24.5% year-over-year decline. And EBIT “switched” even from a positive €169 million in Q2/22 to a loss of €956 million in Q2/23. Free cash flow also switched from a positive FCF of €1,140 million in the same quarter last year to a negative free cash flow of €473 million this quarter. And core earnings per share declined from €1.93 in the same quarter last year to €1.22 this quarter.

Looking at the sales in more detail, we see the top line declining due to several reasons. As already mentioned above, currency effects had a negative impact and led to a 4.3% decline YoY. Additionally, prices also declined 0.8% YoY and especially volume declined 7.4% being therefore the biggest negative contributor to declining sales.

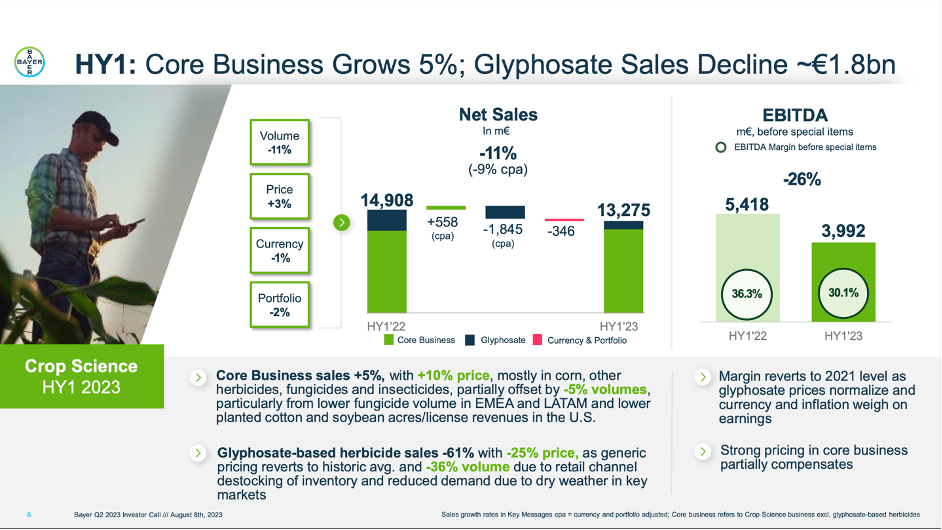

Among the three different segments, it was especially “Crop Sciences” that contributed to the declining sales. In the second quarter, sales dropped 23.8% year-over-year to only €4,924 million. And here especially volume declined 15.1% year-over-year, which is not a good sign. When looking at the first half of 2023, the picture is still a little better with sales declining 11% year-over-year. But EBITDA in H1/23 already declined 26% compared to the same timeframe last year.

{kind=link}

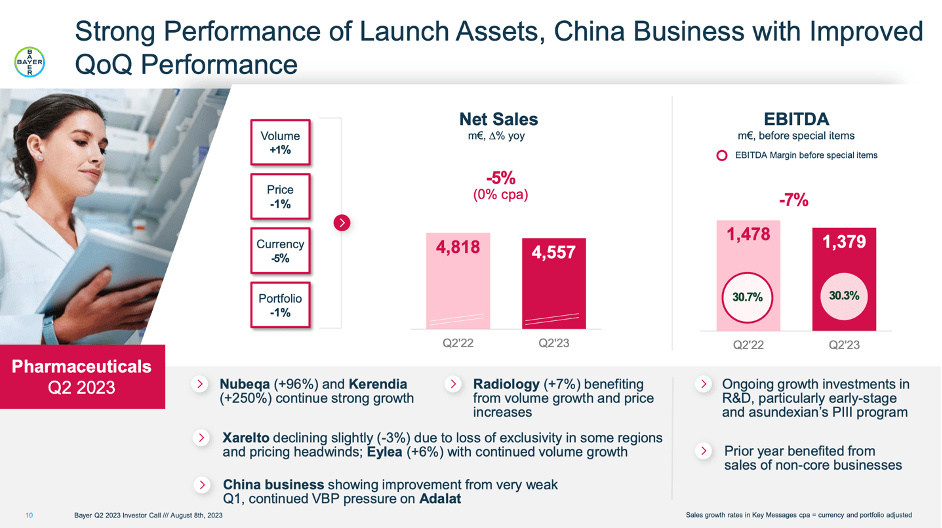

While “Crop Sciences” is certainly the most important segment for Bayer when looking at sales, “Pharmaceuticals” is similar important for the bottom line. Sales for the segment declined from €4,818 million in Q2/22 to €4,557 million in Q2/23 – resulting in 5.4% YoY decline. And in case of “Pharmaceuticals” it was mostly currency effects that contributed to the decline (4.8% decline), while volume increased slightly (0.9%) and prices declined slightly (-0.7%).

{kind=link}

The third segment, “Consumer Health” also had to report declining sales, but only 2.0% year-over-year decline to €1,466 million. For “Consumer Health” the negative currency effects had a huge negative impact on the business (-7.0% YoY) and volume also declined 4.4% YoY. These negative effects were offset by 9.8% YoY price increases.

Disappointing Guidance

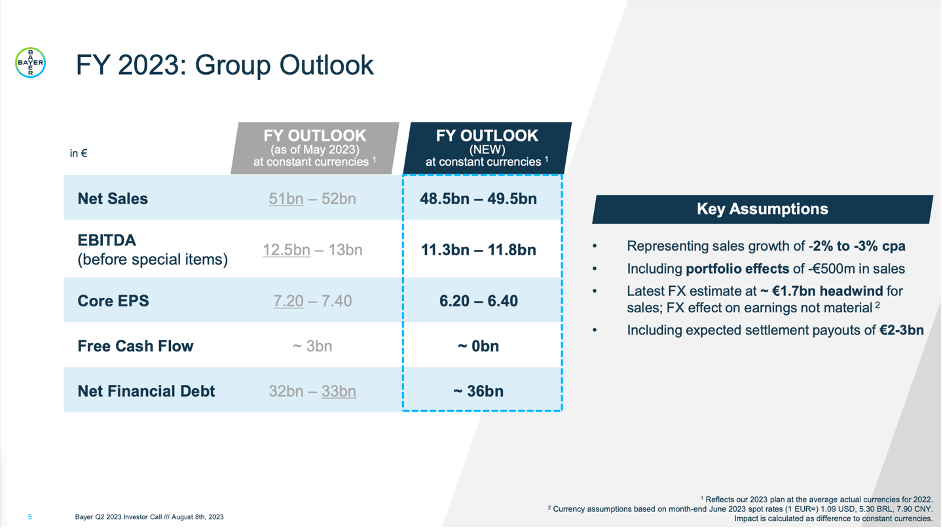

Not only were second quarter results disappointing, but Bayer also had to lower its guidance for the full year 2023. Instead of $51 billion to $52 billion in sales, management is now expecting only €48.5 billion to €49.5 billion in 2023. And these numbers are FX-adjusted – reported revenue is expected to be between €46.8 billion and €47.8 billion. The core EPS – another adjusted metric – is now expected to be between €6.20 and €6.40 – one Euro lower than in the previous guidance. And finally, free cash flow is expected to be zero – compared to €3 billion in a previous guidance.

{kind=link}

The man reason for the low free cash flow are included expectations for settlement payouts between €2 billion and €3 billion, but these negative impacts were already included in the previous guidance.

Still high debt levels

Another problem of Bayer are the still high debt levels. In its previous guidance, management was expecting debt to decline to a range of €32 billion to €33 billion at the end of fiscal 2023, but now management is seeing debt at around €36 billion.

And when looking at Bayer’s statement of financial positions (the balance sheet) on June 30, 2023, we see total assets as well as equity attributable to Bayer AG shareholders declining over the last few quarters – which is not a good sign. While Bayer has €36,557 million in non-current financial liabilities, the company also has €9,960 million in current financial liabilities. And in my opinion, management is quite optimistic when it assumes to repay about €10 billion in debt in the next 12 months. Of course, the company has €4,481 million in cash and cash equivalents on its balance sheet it can use to reduce debt levels.

When comparing the total debt to the shareholder’s equity we get a D/E ratio of 1.26. Additionally, we can compare total debt to the operating income the business can generate. But here it gets difficult to decide what metric we should use and depending on the metric used as denominator, we get extremely different ratios. When looking at fiscal 2022 numbers, EBITDA was as high as €13,513 million, while EBIT before special items was €9,257 million and EBIT was only €7,012 million. And when looking at the same numbers in previous years or the last four quarters, we see much lower numbers. And hence, it would take only about 3.5 years to repay the outstanding debt – or much longer.

Summing up, I would still see Bayer’s balance sheet as problematic and one of the major issues speaking against an investment. On the other hand, debt levels are still manageable, and Bayer is not facing the risk of bankruptcy or severe liquidity issues.

Free cash flow

Another problem is the rather disappointing free cash flow in the last few years. While Bayer was able to generate close to €5 billion in free cash flow in 2018 and 2019, the years 2020 till 2022 were rather a disappointment. In 2022, Bayer could generate €3,111 million in free cash flow – but in 2021 only €1,415 million and in 2020 only €1,343 million.

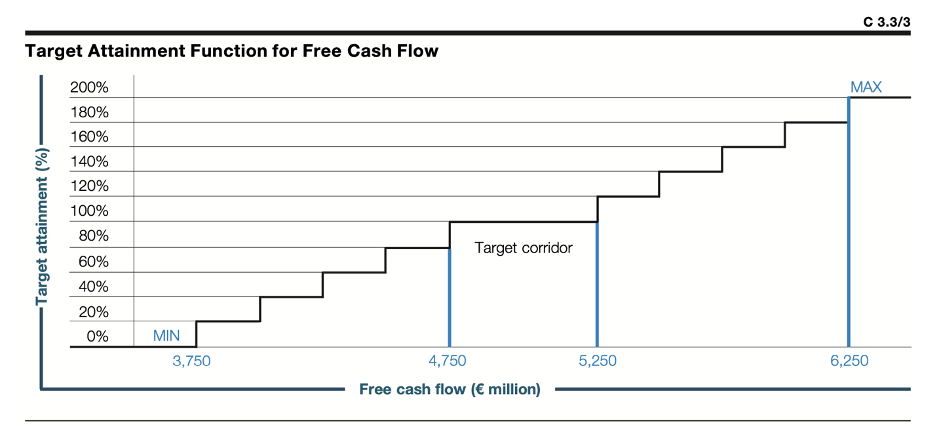

Bayer: FCF Target Range Management Compensation (Bayer Annual Report 2022)

{kind=link}

And in 2023 Bayer is now expecting €0 free cash flow – far away from the company’s target range, which is part of management’s compensation system. The target corridor for free cash flow is between €4,750 million and €5,250 million, but Bayer missed its target for several years in a row.

The Bulls

In an article published in October 2022, I predicted that most parts of the world could be in a recession by now, but Bayer might rather be recession resilient. Now the picture seems to be reverse: Most countries are not in a recession yet (although I still think the recession will come) but Bayer is struggling and doesn’t seem so recession-resilient after all. Nevertheless, the two recession-resilient businesses “Pharmaceuticals” and “Consumer Health” are still keeping up quite well. “Crop Sciences” is struggling, but this business must be seen as rather cyclical and fluctuating sales must be expected in the years to come.

I mentioned above that I was always bullish about Bayer in the last few years – and I still am. Therefore, you are right to expect some bullish arguments about Bayer that off-set the bearish arguments made above.

New CEO

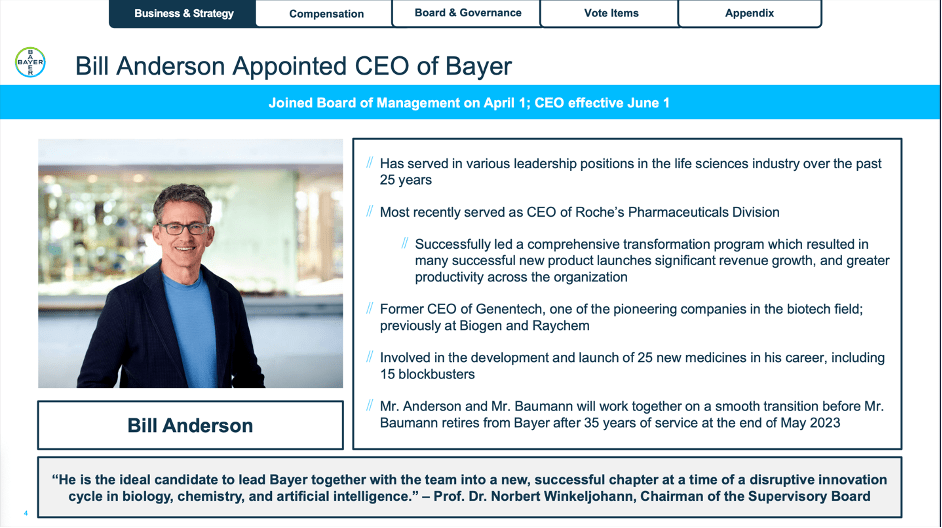

Let’s start with a recent bullish argument – or a piece of information that can be rather bullish. Although Bill Anderson did not have a good start as CEO of Bayer with his first quarterly results, we can still be optimistic. Since June 1, 2023, Bill Anderson succeeded Baumann as CEO of Bayer. And while I don’t want to bash the former CEO, many investors see Baumann as reason for the declining stock price. And one can’t deny that since 2015 Bayer was constantly struggling and mistakes were made.

Bayer Annual Stockholder Meeting 2023

{kind=link}

Bill Anderson, which was most recently the CEO of Roche’s Pharmaceutical Division, might be able to lead Bayer back to its previous glory days. And with more than 25 years industry experience he seems like a great candidate for the position.

Growth Potential

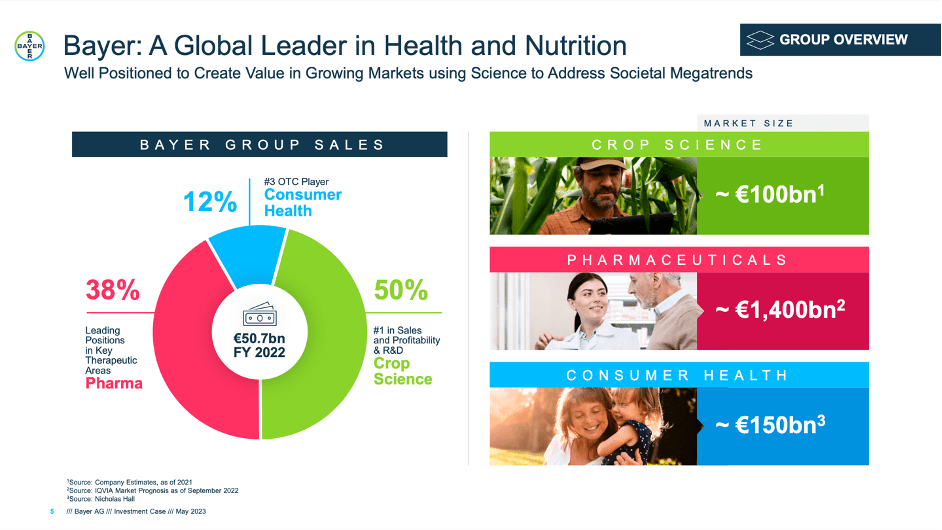

And Bayer also should have growth potential as the three business segments address huge markets. Especially in the Crop Sciences, with a TAM of €100 billion, Bayer is clear market leader and should be able to use its dominant position in the years to come and maybe be able to gain market shares. Consumer Health has a total addressable market of €150 billion and Pharmaceuticals has a huge addressable market of €1.4 trillion which is offering growth potential (at least in theory). For the pharmaceutical industry we also must point out that several companies are battling for market shares.

Bayer AG May 2023 Presentation

{kind=link}

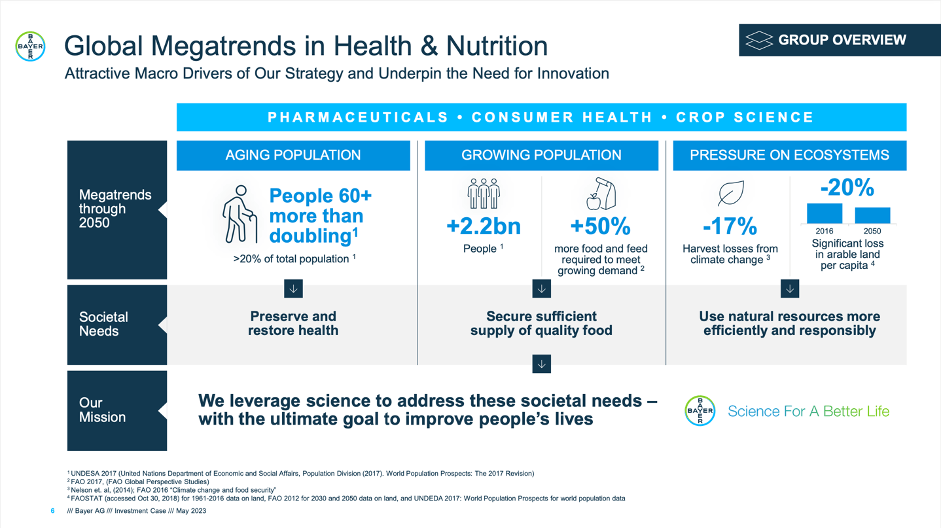

Bayer might also profit from several megatrends that lead to sustained and long-lasting growth over one (or several) decades to come. One megatrend is the aging population with the number of people over 60 more than doubling (and these people will be more than 20% of total population). And especially the pharmaceutical segment will profit here as older people usually have a higher demand for pharmaceuticals. Additionally, the growing population by itself is also a huge megatrend. Bayer is expecting 50% more food and feed required to meet the growing demand and the innovations of crop sciences will be needed. The situation will be worse due to expected pressures on the ecosystem. Bayer is expecting 17% harvest losses from climate change and to keep up with demand for food, crop sciences products will be needed even more.

Bayer AG May 2023 Presentation

{kind=link}

Intrinsic Value Calculation

So far, we talked about the business – the positive and negative aspects of Bayer and the industry the company is operating in. But we all know we can’t just look at the business in isolation – we also must include the price we have to pay for a business in our analysis. And even if Bayer should continue to struggle and not be able to grow again it can be a great investment when it is trading for a lower price.

In past articles I often assumed that Bayer will be able to reach €5 billion in free cash flow again. Management was also optimistic to reach that number again in 2024 (and it is also the target corridor for compensation – see above). But maybe we should be more realistic and use the average free cash flow of the last five years as basis - €2,947 million. Additionally, I would assume that Bayer will be able to grow at least 5% annually. When calculating with these assumptions (and 982.42 million outstanding shares as well as a 10% discount rate) we get an intrinsic value of €59.99.

A more realistic assumption would be to assume €0 free cash flow in 2023 but again €5 billion in fiscal 2024 and 5% growth for the following years. This leads to an intrinsic value of €92.54 for Bayer and in my opinion, this is a realistic intrinsic value as I think Bayer could double in value and the stock would still not be overvalued.

Conclusion

In my opinion, Bayer remains undervalued, and I remain confident that Bayer will return on its path of growth although the debt levels should be carefully monitored. And Bayer – under the new CEO – should try to become the boring but well-run and well-performing business again it was before 2015.

For further details see:

Bayer: Still A Strong Buy Despite Lowered Guidance