AMZN - BCAT: Deeply Discounted As Saba Builds Larger Position

2023-11-09 11:49:49 ET

Summary

- BlackRock Capital Allocation Term Trust provides exposure to an actively managed portfolio split between equities and fixed-income.

- The fund continues to operate without leveraging up from borrowings, which I view as a positive in the current environment.

- BCAT's performance has been respectable, with the potential for further discount narrowing, and improved results could come from discount contraction from activist pressure.

Written by Nick Ackerman, co-produced by Stanford Chemist.

BlackRock Capital Allocation Term Trust (BCAT) provides investors exposure to an actively managed portfolio with managers that have the flexibility to invest in whatever, wherever and whenever. Currently, the fund is split fairly evenly between equities and fixed-income.

The fund also has the capacity to utilize leverage in an attempt to enhance returns; however, the fund remains unleveraged. I view that as a positive in the current environment.

Since our prior coverage , shares have been under pressure, but the market hasn't been particularly rosy either, as Treasury Rates started to soar. Treasury Rates surpassed the highs we saw last October when the broader market bottomed out.

BCAT Performance Since Prior Update (Seeking Alpha)

The Basics

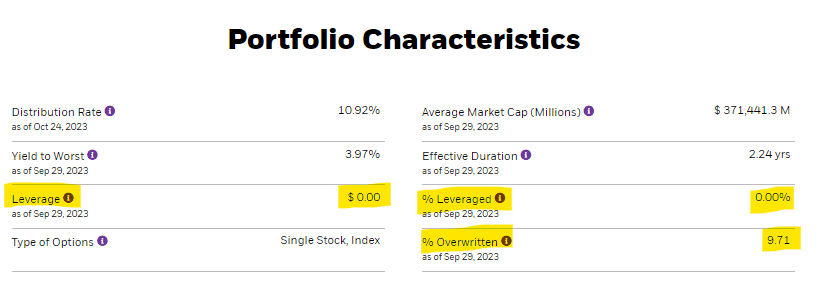

- 1-Year Z-score: -0.02

- Discount: -13.63%

- Distribution Yield: 10.92%

- Expense Ratio: 1.41%

- Leverage: 0%

- Managed Assets: $1.743 billion

- Structure: Term (anticipated liquidation date of September 25, 2032)

BCAT's investment objective is "to provide total return and income through a combination of current income, current gains and long-term capital appreciation."

To meet their objective, they simply "invest in a portfolio of equity and debt securities." They add a bit more color with, "the Trust may emphasize either debt securities or equity securities." Along with this, they will "utilize an option writing strategy in an effort to generate gains from options premiums and to enhance the Trust's risk-adjusted returns."

The fund is overwritten by 9.71% currently, which could indicate that the managers are bullish. This is an indication of being bullish because, in a covered call strategy, the upside can be limited due to essentially putting a cap on what gains to the upside can be participated in. This is only down a touch from the overwritten percentage of our prior update.

The fund also continues to run with zero leverage at this time; this was the same as our prior update. In fact, through most of the last year, leverage was either at 0% from borrowings or quite minimal. Our update from last September 2022 shows us that leverage was mid-single digits.

{kind=link}

I view this as a positive, as borrowings are based on OBFR plus 0.75% . Given where rates are, this would push the borrowing costs over 6%. That limits the universe of what makes sense to invest in, especially during a more uncertain period going forward with the Fed holding rates higher to slow down the economy.

Performance - Deepening Discount

Saba Capital Management has been getting aggressive with BlackRock and taking positions in a number of different funds. For BCAT, they hadn't been as aggressive as a few others, but that could be looking to change as the activist firm just crossed the 10% ownership threshold.

I believe in an effort to thwart activist pressure, BCAT boosted its distribution payout earlier this year. This was along with its ESG-focused sister fund, BlackRock ESG Capital Allocation Term Trust ( ECAT ).

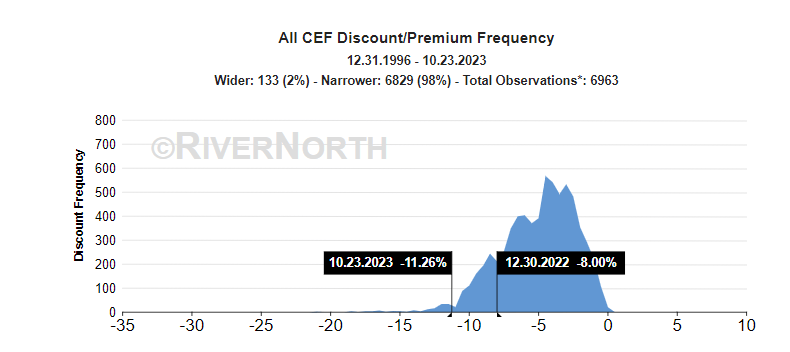

That effort seemed to help narrow the discount as it was at a much deeper double-digit discount. Through mid-2023, the discount was heading toward almost touching a single-digit discount; however, with volatility heating back up in the market, that seemed to be a driving factor in pushing it back out to a wider discount.

Ycharts

I suspect this provides Saba with a better argument that the fund needs to do more for its shareholders. On the other hand, to be fair, closed-end fund discounts are at some of the deepest discounts we've seen historically .

CEF Discount/Premium Relative to History (RiverNorth (as of 10/25/2023))

{kind=link}

With a dynamically changing allocation allowed to invest anywhere in the market, the performance, being good or bad, is going to be subjective. In my opinion, the fund has performed respectably.

Overall, I don't really like the 'broader equity' market this year that's usually represented by the S&P 500 Index. The results we are seeing in SPDR S&P 500 ETF ( SPY ) - have been driven by just a handful of mega-cap tech names. This can be reflected when we look at the Invesco S&P 500 Equal Weight ETF ( RSP ) on a YTD basis. The fund is slightly negative, while SPY is running hot on a total return basis. To me, this all means that SPY isn't really a great representation of what most equity positions are feeling today.

Ycharts

Where BCAT comes in is right in the middle on a total NAV return basis. Coming off of the ~18% discount at the start of the year really drove BCAT's total share price results. If Saba is successful in whatever they may be trying to do here, we could see results similarly impressive going forward.

Actually, looking back at the total NAV return results, the performance has been suspiciously close to that of the iShares iBoxx $ High Yield Corporate Bond ETF (HYG), interestingly enough. Junk bonds are performing better than their investment-grade counterparts, as represented by the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) and even outperforming RSP. Junk bonds are less interest rate sensitive, so this makes sense.

BCAT is a split between about a 50% allocation to equities, and then the other 50% is divided against investment-grade, non-investment-grade, and not-rated offerings.

So, no doubt, an investor can look at the above performance and come up with a conclusion for or against BCAT in terms of results and why they are bad or why they were good. I'll stay neutral and say they were decent and quite respectable with the opportunity to drive further discount narrowing that could really provide even better results.

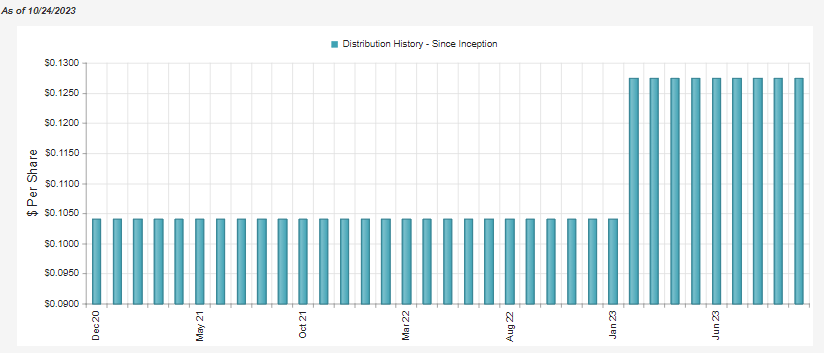

Distribution - Approaching ~11%

As mentioned, the fund bumped up its payout earlier this year and, at the time, it worked out to a 9% NAV distribution rate. Performance has come down since then, and the NAV rate is now sitting closer to 9.5%.

{kind=link}

Now, as everyone knows, just because a fund can pay a distribution rate doesn't mean it can earn it. In this case, it brings up the strong argument that earning it or not could have led to some discount contraction, and that means it was a positive move for shareholders regardless.

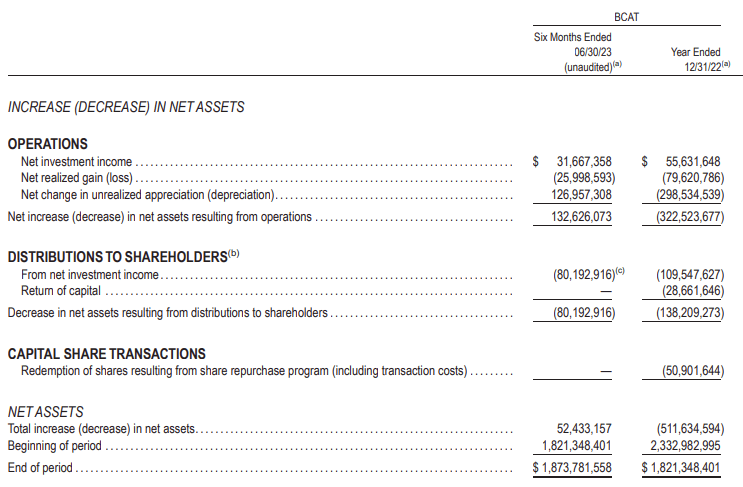

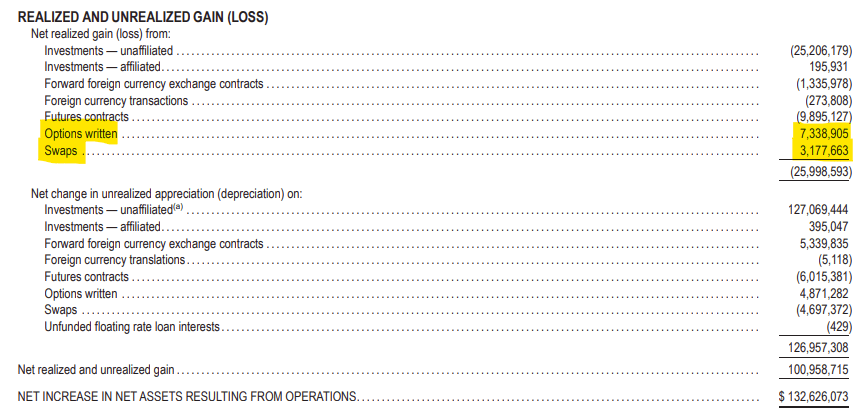

In terms of coverage of the distribution, the fund, in the first half of the year, earned a net investment income of $0.29. If annualized, that is on pace to surpass last year's $0.50 NII per share. Of course, at an annualized distribution rate of $1.53, that means they'll have to generate capital gains for the shortfall if it is to be covered.

For the first half of the year, that was starting to look good as well, as they had unrealized capital gains of $0.94 per share, which saw the total increase from NII and capital appreciation/depreciation come in at $1.23. This was largely driven by the unrealized appreciation in the underlying portfolio as the fund realized losses in the first half.

{kind=link}

Swaps and options written contributed to offsetting some of these realized losses; however, the underlying portfolio and foreign currency transactions were detractors.

BCAT Unrealized/Realized Gains/Losses (BlackRock (highlights from author))

{kind=link}

Still, the earnings here in the first half were enough to nearly cover the entire year. However, a lot of this was coming from a rebound of last year, where the fund's portfolio took a significant hit.

However, since then, equities and fixed-income have come under pressure once again with higher Treasury Rates. So some of those gains have come down, and now NAV has moved down into the negative for the year.

Ycharts

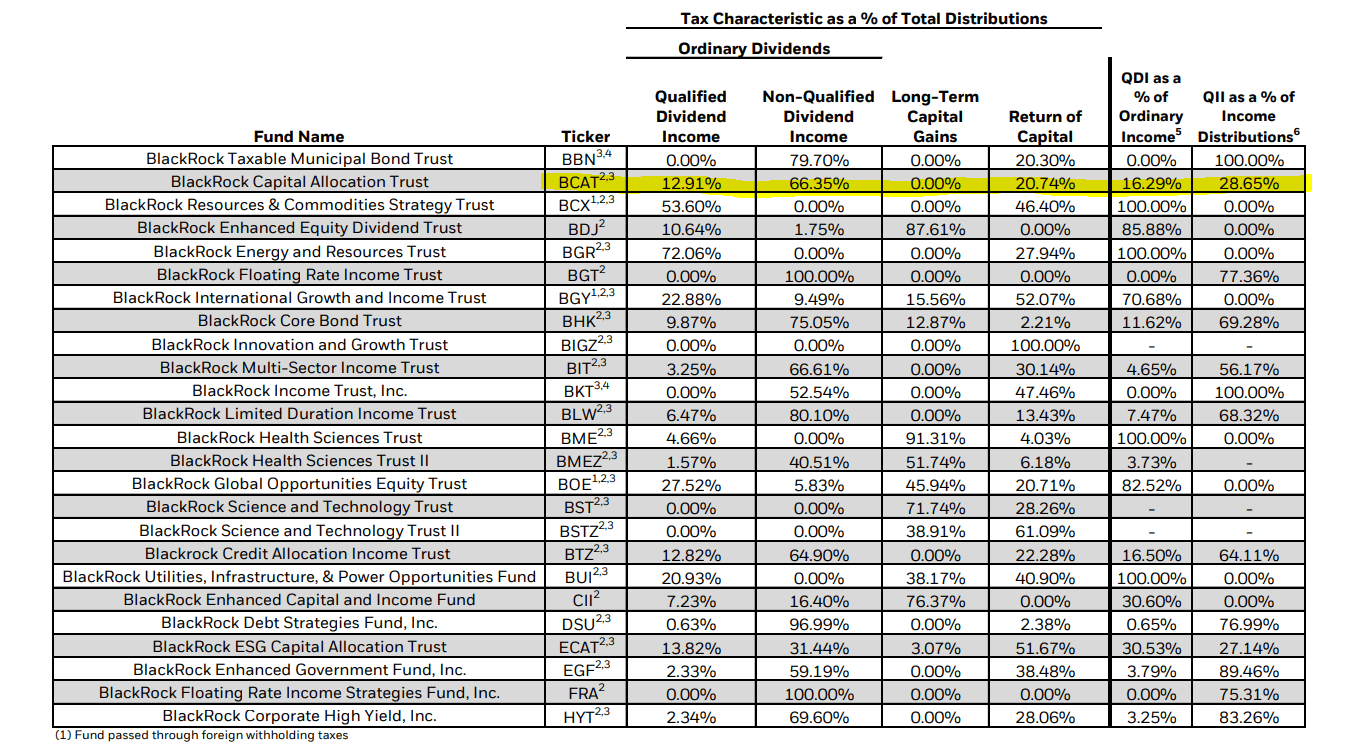

We previously discussed the tax classification for the distribution in our prior update. Here is a recap:

2022 saw the fund's distribution tax classification as mostly non-qualified dividend income. That could indicate the fund isn't so tax-friendly and could be best held in a tax-sheltered account. Given the sizeable exposure to fixed-income investments that pay interest payments, this could be the case going forward. However, we also have ROC identified, which is a way to defer tax obligations as it reduces an investor's cost basis. If the fund is successful, long-term capital gains would likely also show up.

BCAT Distribution Tax Classification (BlackRock (highlights from author))

The breakdown going forward is likely to change materially, and hard to predict year to year for the reasons listed above. Overall, that makes this fund a bit difficult to determine which would be more appropriate in general.

{kind=link}

BCAT's Portfolio

The fund has taken its positioning to about 50/50 between equities and fixed income. It isn't exactly, but it is close enough. This was largely how they were positioned in our previous update as well, which showed the portfolio positioning from the period ended April 28, 2023.

{kind=link}

This might be a bit surprising considering that the fund has some really high turnover. The last six months came in at 122%. That was up from last year, which had a turnover rate of 98%, and that was for a full year.

That said, they also break out the portfolio turnover rate if it wasn't for the mortgage dollar roll transactions. So, this isn't exactly all turning over their equity and bond portfolio. That said, even when excluding the MDR transactions, the portfolio was still pretty active, with a turnover rate of 75% for the prior six-month period. Last year's turnover was still at 88%, meaning they were quite active then, too.

{kind=link}

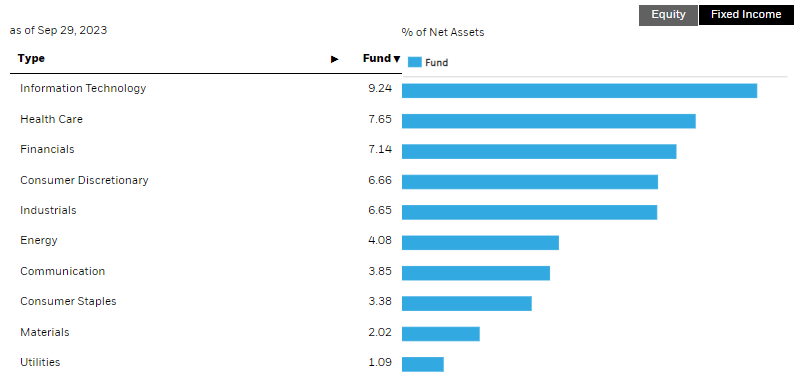

In terms of sector exposure, the fund is fairly diversified, with no sector commanding a significant overweight position. Tech is the largest weighting, but it isn't dominating the fund. This is the breakdown for the equity sleeve of their portfolio, which is generally consistent with how they were positioned previously as well, similar to the overall asset allocation.

{kind=link}

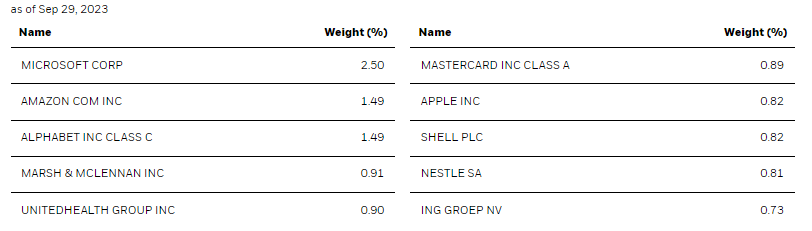

The top position for the fund continues to be Microsoft ( MSFT ), which just recently announced some solid earnings with the return to accelerated growth in Azure , a part of their cloud services. Azure has been providing significant growth for the company, and that hasn't stopped, but the pace was slowing. Seeing a return to an acceleration once again has investors excited.

{kind=link}

Along with MSFT are some of the other Magnificent Seven names, Amazon ( AMZN ), Alphabet ( GOOG ) and Apple ( AAPL ). GOOG also reported their results, but they weren't as rosy and were met with a falling share price as their own cloud revenues didn't grow as fast as expected .

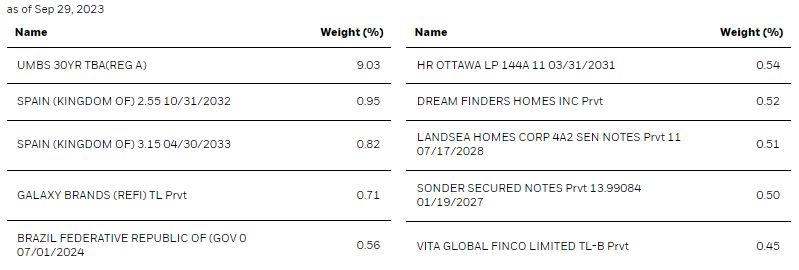

Turning to BCAT's fixed-income sleeve, which contains the fund's largest holding overall. That would be the UMBS 30-year TBA at a 9.03% weight.

{kind=link}

While it is a large part of their portfolio, the UMBS securities fund has exposure to hundreds or thousands of separate mortgages backing the underlying investment. Essentially, a portfolio of loans within itself, so a ~9% weighting isn't dependent upon one person or entity making the payment.

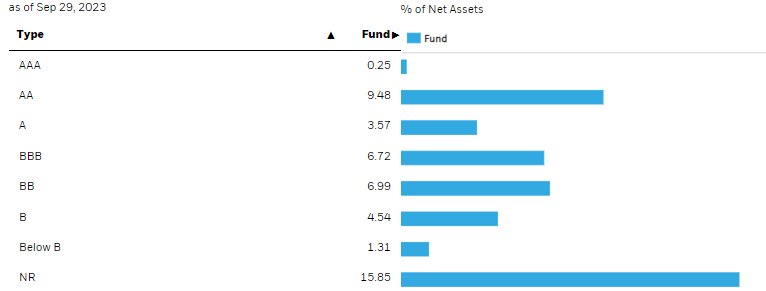

UMBS is also invested in U.S. Government-Sponsored Agency Securities that are issued by Fannie Mae and Freddie Mac. That's primarily where the fund's AA fixed-income credit quality exposure is going to be coming from, as the U.S. Government backs these.

{kind=link}

Conclusion

BCAT provides investors exposure to a wide variety of investments, and that's driven by the highly flexible investment policy that is provided to the investment managers. The fund has put up respectable returns. The move to increase the fund's distribution also was a positive to move the discount. However, more recently, the fund's discount has been widening again, which keeps it an appealing fund. Saba has taken an even larger stake in the fund now at over 10%, which could present further potential opportunity if they are able to shake things up.

For further details see:

BCAT: Deeply Discounted As Saba Builds Larger Position