BCV - BCV: Stay On The Sidelines Until The Right Market Conditions

2023-11-12 07:04:46 ET

Summary

- The Bancroft Fund is a closed-end fund that focuses on convertible securities for current income and capital appreciation.

- BCV's distribution appears aggressive relative to the fund's long-term historical returns.

- Current market conditions are not conducive for convertible bonds as both equity and fixed income markets remain in bear markets.

The Bancroft Fund ( BCV ) is a convertibles-focused CEF paying an attractive 8.9% distribution yield. However, the convertibles asset class has had a rough few years due to the twin bear markets in both bonds and equities.

Until small-cap companies return to positive returns, I believe convertible bond funds like BCV will continue to struggle. I am staying on the sidelines for now.

Fund Overview

The Bancroft Fund is a closed-end fund ("CEF") that seeks to provide current income and capital appreciation, primarily from a portfolio of convertible securities.

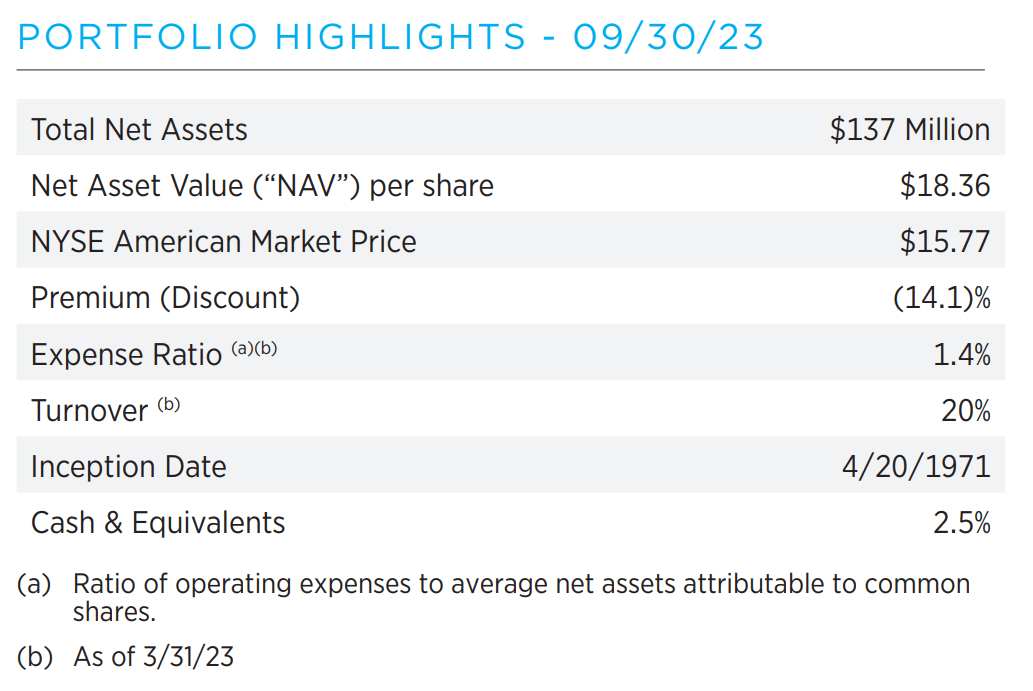

The Bancroft Fund has been in operation since the 1970s with an inception date of April 19, 1971. Currently, the fund has $137 million in managed assets and $30 million in preferred shares for a 21.9% effective leverage ratio (Figure 1). The BCV fund charges a modest 1.4% total expense ratio.

Figure 1 - BCV overview (gabelli.com)

{kind=link}

Refresher On Convertible Securities

For readers that do not deal with financial jargon all day, convertible securities are investments that can change from its initial form into another form after certain conditions are met. Most commonly, they appear as convertible bonds and convertible preferred shares that can be converted into common stock at a given conversion price.

Compared to traditional bonds, convertible bonds typically carry lower interest rates. This is because investors assign a value to the 'optionality' embedded in the security. For the issuer, convertible securities allow them to raise capital at a lower fixed carrying cost than traditional bonds, although the tradeoff is potential share dilution. Investors are willing to accept a lower interest coupon because they can participate in the 'equity upside' if the company does well.

One common way to treat convertible bonds is to consider them as a combination of a traditional bond plus a call option on the underlying stock. Since convertible securities have an embedded call option, they typically do very well in equity bull markets as the option provides upside convexity. If the company's stock price rallies beyond the conversion price, the convertible bond can even trade like the underlying stock due to the embedded option. Conversely, in an equity bear market, convertible bonds can perform very poorly, as the option component can lose value very quickly.

Portfolio Holdings

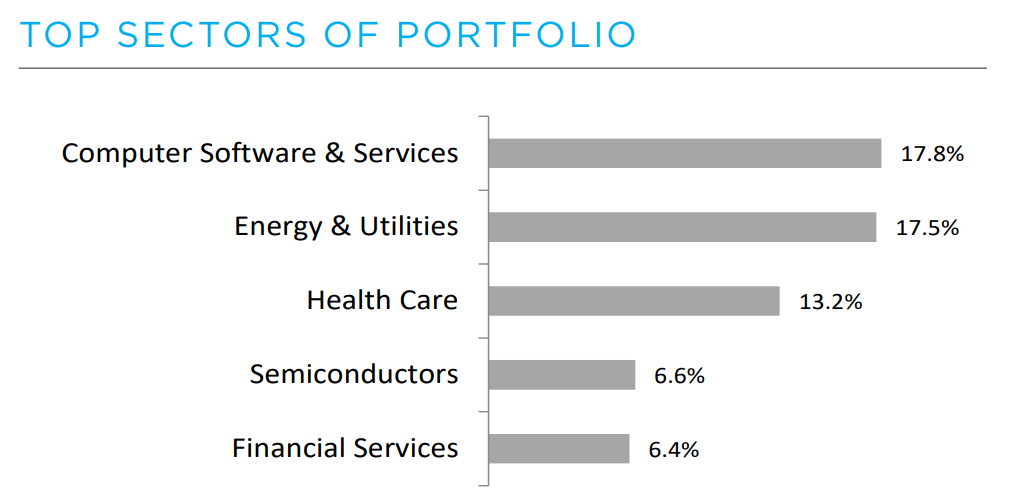

Figure 2 shows BCV's sector allocation. 17.8% of the portfolio is invested in the Computer Software & Services sector, 17.5% in Energy & Utilities, and 13.2% in Health Care.

Figure 2 - BCV sector allocation (BCV factsheet)

{kind=link}

This sector allocation is quite common for convertible securities funds, since convertible issuers tend to be younger, small-cap 'high-growth' companies with less robust cash flows that like to take advantage of the lower cash coupons of convertible securities. Investors are also enamoured with the 'upside potential' of these high growth companies.

Figure 3 shows the top 10 holdings of the BCV fund, which account for 21.2% of the fund's assets.

Figure 3 - BCV top 10 holdings (gabelli.com)

{kind=link}

Returns

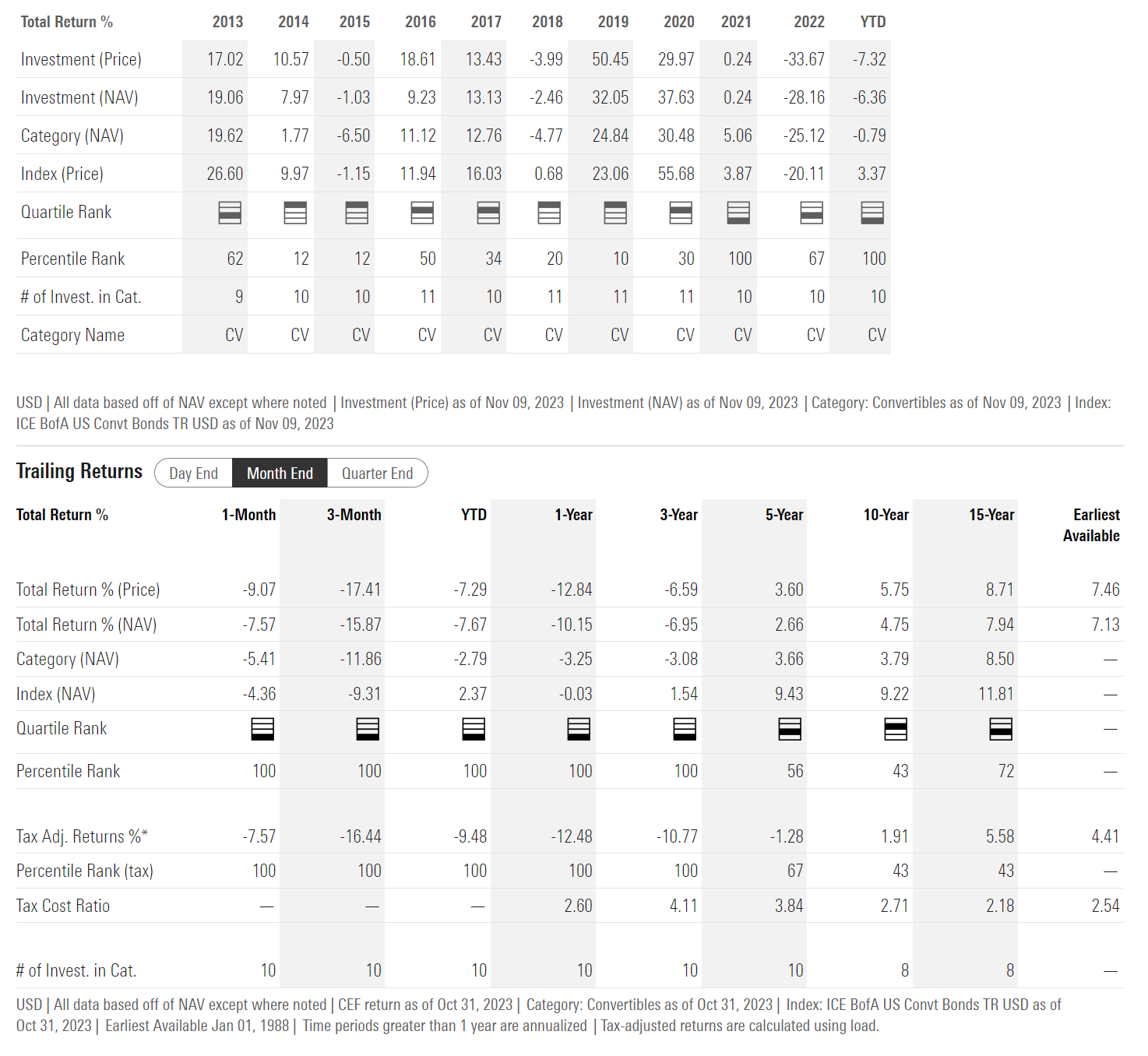

Figure 4 shows BCV's historical returns. The BCV fund has modest returns with 5/10/15Yr average annual returns of 2.7%/4.8%/7.9% respectively to October 31, 2023. Short and medium-term returns were negatively impacted by 2022, when the fund lost 28.2%.

Figure 4 - BCV historical returns (morningstar.com)

{kind=link}

However, the fund's -28.2% return in 2022 fail to give context to how poor returns have been for the past 2 years. BCV's NAV peaked at over $36 / share in early 2021 and have since declined by more than 50% due to the simultaneous equity and fixed income bear market (Figure 5).

Figure 5 - BCV's NAV has crashed more than 50% (morningstar.com)

{kind=link}

Distribution & Yield

The Bancroft Fund pays a quarterly distribution of $0.32, which works out to an attractive 8.9% forward yield. On NAV of $17.21, the BCV fund's distribution is yielding 7.4%. In good years, the BCV fund can also pay a special distribution. For example, in 2021, the ECF fund's fourth quarter distribution was $3.17 instead of the normal $0.32.

The BCV fund's distribution is paid out of net investment income ("NII") and realized gains, although the fund had to dip into return of capital ("ROC") to fund a small part of the distribution last year (Figure 6).

Figure 6 - BCV's distribution mostly funded from NII and realized gains (BCV semi-annual report)

{kind=link}

Unfortunately, relative to the fund's long-term average annual returns of 4.8% over 10 years, I believe the current distribution rate may be too aggressive.

Explaining BCV's Poor 2022

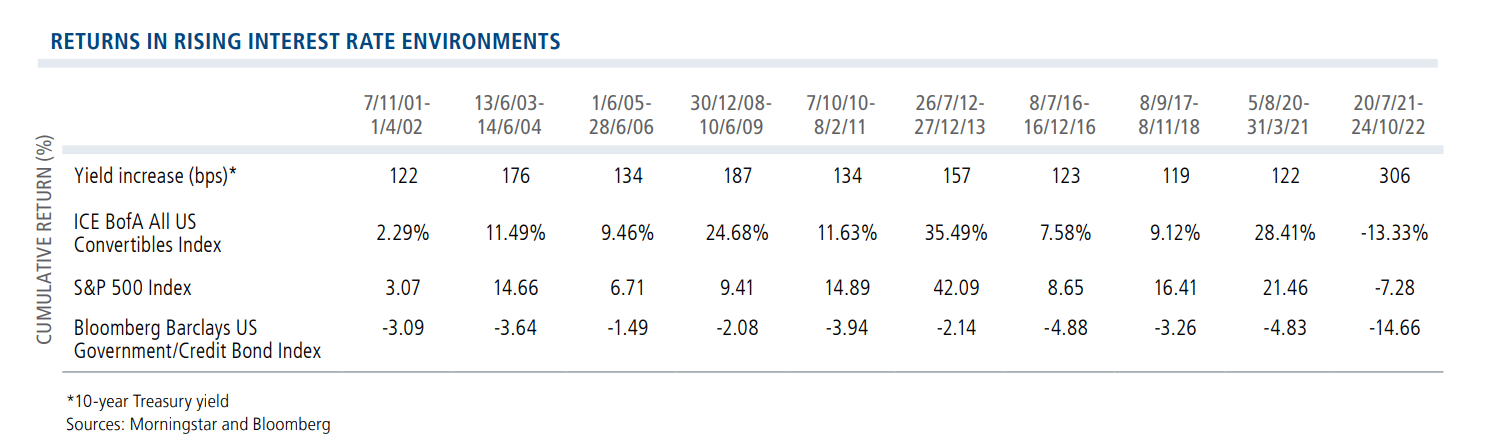

Before last year's annus horribilis for the convertible bond asset class, many analysts and investors were touting convertible bonds as a potential safe haven from rising interest rates. Historically, the convertible bond asset class, as measured by the ICE BofA All US Convertibles Index, had done well in rising interest rate environments (Figure 7).

Figure 7 - Historically, convertibles had done well in rising interest rate environments (calamos.com)

{kind=link}

This is because rising interest rates tend to be associated with an improving economy and a strong jobs market. These economic tailwinds are often accompanied by higher equity prices, which increases the value of convertible securities' embedded call options (Figure 8).

Figure 8 - Due to convertibles' embedded equity options (wellesleyassetmanagement.com)

{kind=link}

However, unlike prior episodes, the interest rate increases in 2022 was driven by the Federal Reserve raising short-term interest rates to combat soaring inflation. This caused both stocks and bonds to decline at the same time, exacerbating BCV's drawdown.

When Might Convertibles Make A Comeback?

As we mentioned earlier in the article, younger small-cap 'growth-oriented' companies tend to be the issuer of convertible securities as they like to take advantage of the lower interest rates paid on the financings.

However, if we look at the equity markets, although the S&P 500 is only a few percent from making new all-time highs, that is mostly driven by a handful of megacap technology companies called the 'Magnificent 7' . Outside of the 'Magnificent 7', the rest of the market has been sideways at best (Figure 9).

Figure 7 - Markets have been poor outside of Magnificent 7 (CNBC)

{kind=link}

In fact, smaller cap companies, as measured by the iShares Russell 2000 ETF ( IWM ) has performed even worse, with a YTD return of -4.5% to October 31, 2023. In my opinion, the convertible securities asset class will need better participation in the equity markets from small-cap companies in order to deliver strong returns.

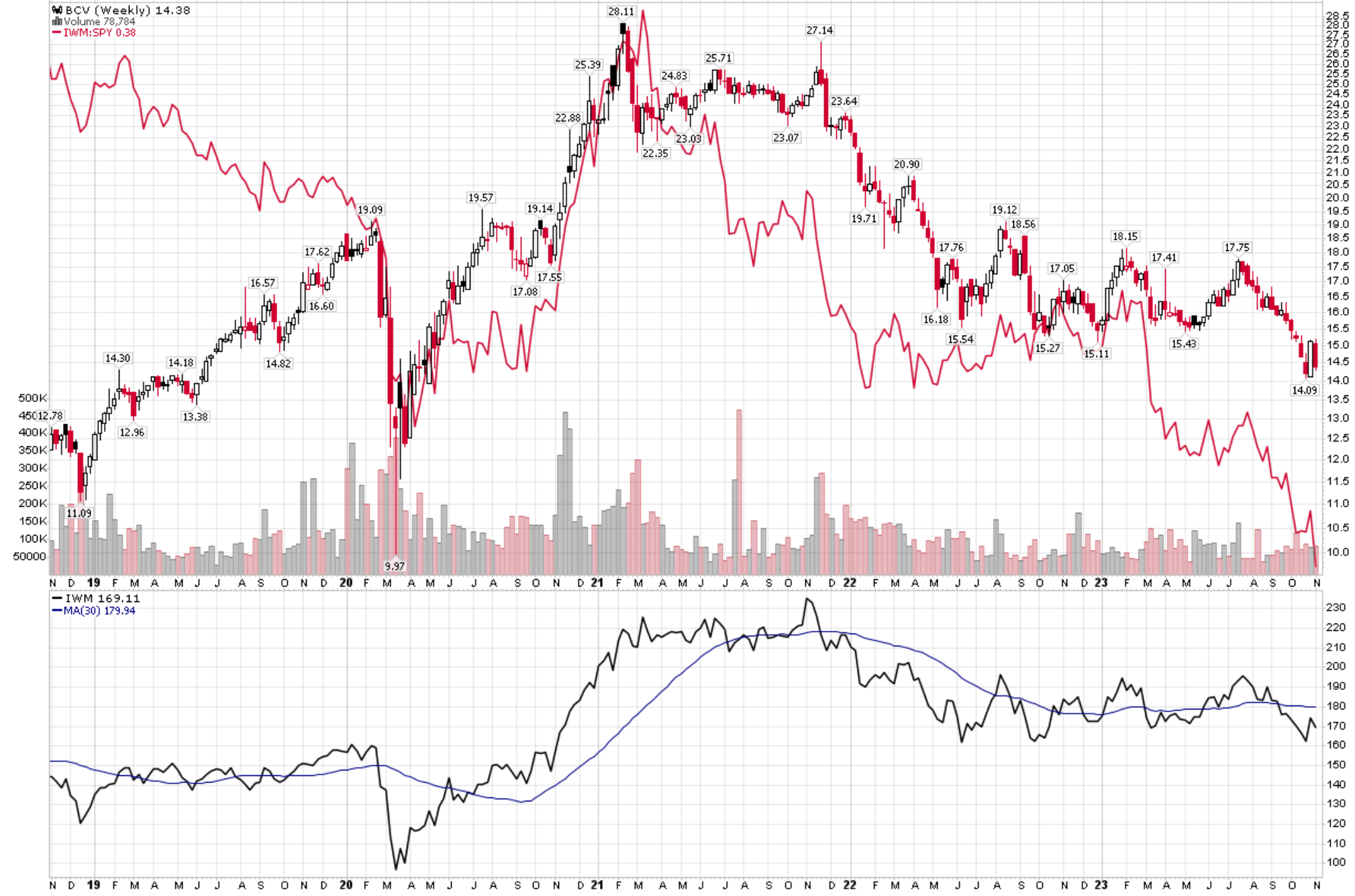

In terms of metrics, what I am looking for is 1) IWM ETF to be in an uptrend (shown in lower panel of Figure 8 below) and 2) the IWM to outperform the SPDR S&P 500 ETF Trust ( SPY ) (shown in the background in the upper panel of Figure 8).

Figure 8 - Better market conditions required for BCV to perform (Author created with price chart from stockcharts.com)

{kind=link}

When the IWM is in an uptrend, the average small-cap company, i.e. the main issuer of convertible securities, have rising equity prices which leads to higher embedded option value. When the IWM outperforms the SPY ETF, that means risk appetite is high and upside optionality is highly valued.

As we can see from Figure 8above, in the right market conditions like in 2020, the BCV fund can deliver extraordinary returns.

Conclusion

The Bancroft Fund is a convertibles-focused CEF offered by Gabelli Asset Management. The BCV fund has been in operation for decades, and has modest long-term historical returns. However, the fund's short-term returns have been negatively impacted by a poor 2022.

I have concerns about BCV's 7.4% of NAV distribution rate, as it appears to be higher than the fund's 4.8% 10 year average annual return.

Convertible funds like the BCV can deliver equity-like returns due to their embedded equity options. However, that requires broad market participation where small-cap companies, the typical convertible security issuer, are generally in uptrends. Until that market condition materializes, convertible bonds may deliver sub-par returns as their yields are lower than similarly rated fixed income securities.

For further details see:

BCV: Stay On The Sidelines Until The Right Market Conditions