BBBY - Bed Bath & Beyond Headed Toward Liquidation In Chapter 11 Bankruptcy

2023-04-23 22:28:39 ET

Summary

- Bed Bath & Beyond finally filed for Chapter 11 bankruptcy in New Jersey on April 23.

- Shareholders are expected to receive no recovery.

- The retailer appears to be completely liquidating and is expected to raise $718 million from inventory sales.

- There's going to be a bidding process for all assets, such as store leases and trade names.

- $40 million in DIP financing is needed to help during the liquidation process.

Bed Bath & Beyond ( BBBY ) filed for Chapter 11 bankruptcy in Newark, N.J., on April 23. They're not even going to try to reorganize - they appear to be completely liquidating. Shareholders are expected to receive no recovery because there are too many priority claims that are likely to get less than full recovery. Vendors basically put them into this situation because they were extremely reluctant to deal with BBBY. With much less merchandise on the shelves, customers did not even bother going to BBBY stores. Their various programs to raise cash by selling additional stock were not enough to cover their extreme negative cash flow from operations.

It's amazing that a company that had $1.5 billion in cash and $1.2 billion in debt in November 2020 just filed for bankruptcy and appears to be completely liquidating. Bed Bath & Beyond used cash to repurchase $1.0 billion BBBY stock the last few years and because their cash flow from operations decreased sharply, they were no longer able to stock their shelves.

Ch.11 Bankruptcy Filing

Bed Bath & Beyond filed for Ch.11 bankruptcy in New Jersey on April 23 ( docket 1) . It's liquidating in Ch.11 and not in Ch.7. In Ch.7 an independent trustee is appointed to manage the liquidation, but Ch.11 allows current management to oversee the liquidation. Some assert that a Ch.11 process is more orderly and more likely to raise a greater amount of cash from the process to pay creditors. Others assert that a Ch.11 process almost always means more legal/professional fees are incurred than in Ch.7 and have to be paid before other creditors. According to their CFO "a full chain wind-down is necessitated by economic realities" (docket 10). The liquidation process is expected to raise $718 million in sales and close all the remaining 473 stores (docket 28). They are retaining an outside liquidator, Hilco Merchant Resources, to help with the process. Often these liquidators bring in other merchandise to help stimulate foot traffic, especially when the inventory level gets very low.

This statement by their CFO basically sums up their position:

The Debtors’ cash burn continued while sales further declined due to lack of incoming merchandise, thus, preventing the Debtors from implementing their anticipated long-term operational restructuring while satisfying their restrictive debt obligations. As such, the Debtors once again find themselves in an untenable liquidity position, necessitating the commencement of these Chapter 11 Cases.

They're also having a bidding process (docket 29) to sell all their assets. This would include store leases, trade names, and other assets. All bids must be received by May 28. The value of these assets is a real wild card. You almost have to go store by store lease to determine if there is some value for each lease and then sum them up. Plus, it's very uncertain how much the other assets are actually worth.

Even after selling additional BBBY stock the last few weeks, they were so broke that on April 21 they got an "emergency overadvance of $54 million" to make timely payments of payroll and taxes. They're trying to get court approval for a 40 million DIP financing to raise new cash and rolling up $200 million of FILO loans with the same terms as the DIP (docket 25). They clearly were very broke before the filing.

At the time of their filing there were 739,056,836 BBBY shares outstanding, which is a huge increase from only 80,362,695 shares outstanding on August 27, 2022. Using the latest BBBY stock price of $0.28 on Friday, the total equity capitalization was $207 million, which is rather high for a company just prior to a bankruptcy filing. They sold a massive number of new shares over the last few weeks to raise cash, but they were constrained by the total number of currently authorized shares outstanding. (Note: Docket 25 stated a different number of shares outstanding, but the wording "As of the Petition Date, approximately 428,120,000 shares of voting common shares were outstanding" implies, in my opinion, that was how many shares were outstanding on the record date to vote on the reverse stock proposal.)

Why Bankruptcy?

There seems to be two reasons why Bed Bath & Beyond, in my opinion, had to file for bankruptcy now.

First, was a legal technical reason. According to their original preliminary proxy statement for voting on the reverse stock split proposal stated that:

The Company expects that the Reverse Split Proposal and the Adjournment Proposal will each be treated as a routine matter, which means that your broker or other nominee will have discretionary authority to vote your shares held in street name on this matter."

This would allow brokers to vote non-voted shares, which would have made the 50%+1 vote of all shares outstanding on the record date easy to get. Their April 5 amended proxy statement completely changed this and stated:

The Company expects that the Reverse Split Proposal and the Adjournment Proposal will each be treated as a non-routine matter, which means that your broker or other nominee will not have discretionary authority to vote your shares held in street name on this matter. Accordingly, in the absence of your voting instructions, your broker or nominee may not vote your shares on the proposals."

This means that brokers can't vote the non-voted proxies. Because retail holders often do not bother to vote, the 50%+1 requirement of shares outstanding to vote to approve the reverse stock split would be very difficult, if not impossible, to get. They would, therefore, be unable to sell more BBBY shares to raise cash. (I covered this in more detail in prior articles.)

Second, vendors refused to ship to the retailer because they were afraid they would not be paid. If the merchandise was received by BBBY more than 20 days before the Ch.11 filing, the vendor's claim for unpaid merchandise would be considered general unsecured claim, which could mean getting little or no actual payment. If merchandise is, however, received within 20 days prior to the bankruptcy filing they are considered priority claims under section 503(b)(9) and should be paid in full under a plan. In addition, some vendors were afraid of the Preference Payment Rule ( section 547) that could mean that BBBY would try to claw back payments to vendors that were paid within the last 90 days prior to the bankruptcy filing. This preference payment action was aggressively used during the Sears Holdings bankruptcy case. I assume that some of their vendors received these preference payment letters from Sears or at least read about this risk of dealing with financially weak retailers.

(Note: If I held unsecured notes, I would try get BBBY management to aggressively begin a claw back of payments to some vendors under section 547.)

Recoveries Under a Chapter 11 Plan

BBBY shareholders should expect to get no recovery because there are just too many claims that have priority. Besides the $1.8614 billion in debt, including the $40 million DIP, there are other unsecured claims and priority claims that must be paid first. There are going to be huge legal/professional fees that must be paid first. Shareholders are at the bottom.

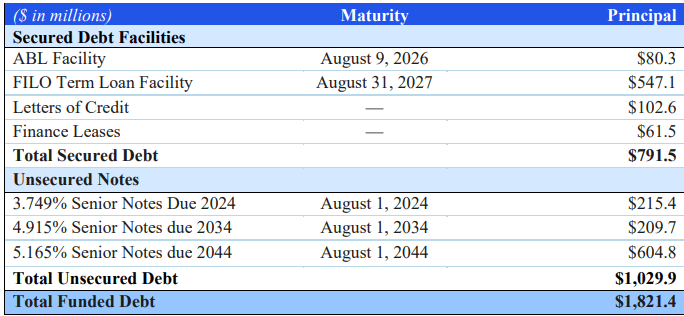

Long-Term Debt Structure

{kind=link}

restructuring.ra.kroll.com/bbby/Home-DocketInfo

(Docket 10 page 27)

The big uncertainty is how much, if any, will unsecured noteholders receive under a plan that must be filed within 90 days after the April 23 filing and confirmed by the court within 120 days under the DIP milestones. Vendors with priority claims must be paid first. Legal/professional fees must be paid first. The $831.5 million secured debt, including the $40 million DIP, has to be paid first. They're expecting $718 million from inventory sales, but too often these expectations are a little too bullish compared to the actual amount. The big wildcard is how much are they going to get under the bidding process. A low bid would most likely mean no recovery for unsecured noteholders, but a very high bid could mean unsecured noteholders could actually get some recovery.

3.749% 8/01/2024 Unsecured Notes

finra.org

Conclusion

It comes as no great surprise that Bed Bath & Beyond filed for Ch.11 bankruptcy since their shelves have been almost empty and it did not seem that they were going to get the needed shareholder approval for their reverse stock split. It still is amazing they went from a very solvent company to bankruptcy so quickly. This is yet another example why I'm absolutely against stock repurchases. It also shows there's something wrong with our legal system that companies can sell securities that will be worthless to the public, but because of issues associated with section 548 , which I covered in prior articles, companies have a very difficult time selling assets to raise cash to avoid bankruptcy.

A hearing has been set for 2pm on April 24 to hear the long list of First Day Motions. It will be interesting to see how smoothly this case proceeds. BBBY shareholders are almost certain to get no recovery. BBBY shares are rated a strong sell. It is uncertain what will happen regarding any recovery for unsecured notes.

For further details see:

Bed Bath & Beyond Headed Toward Liquidation In Chapter 11 Bankruptcy