BBBY - Bed Bath & Beyond Is Most Likely Headed Into Bankruptcy Given The Latest SEC Filings

2023-03-31 10:30:00 ET

Summary

- Bed Bath & Beyond is trying to raise more cash by selling even more shares, which dilute current shareholders, to stay out of bankruptcy.

- The recent filing stated that if the stock offer is not successful, they will file for bankruptcy, which will wipe out shareholders.

- The latest preliminary results were terrible, with comparable sales down 40-50%.

- It appears that avoiding bankruptcy also depends on shareholders needing to approve a reverse stock split proposal.

- Meme trading is one thing that could save this retailer, and possibly the only thing.

Even after issuing a massive number of additional new shares to raise cash, Bed Bath & Beyond ( BBBY ) seems fairly likely to be headed into bankruptcy court based on various filings on March 30. Their amended credit agreement is much stricter and their preliminary results for 4Q'22 were terrible. The only way, in my opinion, that BBBY can be saved is if irrational meme traders push the stock price significantly higher - again.

Incorrect Reported Metrics on Financial Websites

First, we need clarification of some reported metrics. It is important that investors have up-to-date data when determining appropriate values for securities. There are some financial metrics reported on various financial websites that are currently incorrect. The capitalization number of $93.5 million reported seems to be using the 117,321,914 shares outstanding as of November 26, 2022 and the last BBBY trading price on March 29. There were actually 428,098,624 shares outstanding as of March 27 using the latest figures filed with the SEC. That would imply a capitalization of $346.8 million - not $93.4 million. That is a very significant difference that was the result of the new financing transactions in February and March. (Note: The March 27 number most likely is already "old".)

Another incorrect metric is the reported 72.33% short interest. Using the 82,349,518 shares sold short as of March 15 and the March 27 shares outstanding, the short interest is "only" 19.2%. One still needs to look at the ability to actually borrow shares and the borrowing rate, but it is much less likely there will be a short squeeze than the incorrect 72.33% short interest would imply.

Selling Even More New Stock to Raise Cash

On March 30 Bed Bath & Beyond filed an updated prospectus to issue up to an additional $300 million worth of BBBY stock. The contents of this update were very disturbing and caused the stock to plunge. According to the filing, they can currently issue up to 295,411,477 shares. For the sake of discussion, I am using the average of the high price ($0.81) and low price ($0.59) on March 30, which is $0.70, to estimate the maximum amount of money that could be raised using the 295,411,477 figure. That estimate of only $207 million is far below the $300 million amount.

They need to complete this sale of stock fairly quickly. As stated in the amended prospectus: "Upon filing our annual report on Form 10-K, which is due by April 26, 2023, we will lose S-3 eligibility, and therefore, we expect all sales made pursuant to the sales agreement will cease by April 26, 2023."

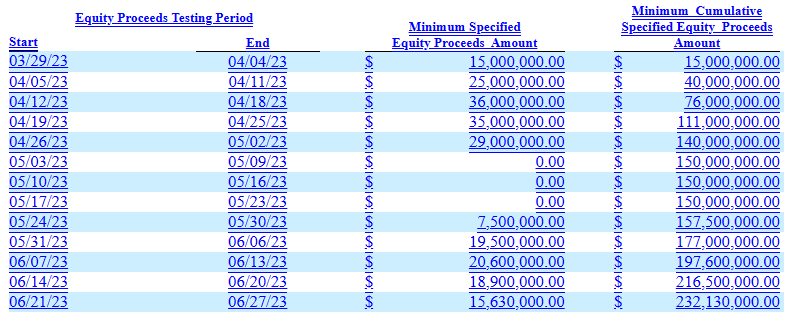

There is also a minimum amount of new equity that needs to be raised within certain time periods under the newly amended credit agreement .

{kind=link}

To get to that $140 million minimum by May 2 implies that the average price of BBBY shares sold via the offer needs to be greater than $0.474, using the 295,411,477 share number. That may seem very easy, but the last price for BBBY was only $0.59 on March 30. If the stock price continues to plunge, this minimum could, in theory, be difficult to achieve.

Besides the $300 million offer, Bed Bath & Beyond negotiated with B. Riley Securities up to a $1.0 billion equity purchase deal over the next 24 months. Oddly, B. Riley could sell BBBY shares up to 30 days past a bankruptcy filing to raise cash, subject to certain conditions, under the terms of the deal. This reminds me of what Hertz Global did in 2020 when they sold new shares even when they were Ch.11.

Shareholder Voting on Reverse Stock Split

There are currently 900 million shares authorized. There is a very clever way to get around that cap without actually getting shareholder approval to increase the authorized number of shares. The company filed a preliminary proxy on March 17 to have a vote on a reverse stock split of either 1 for 5 or 1 for 10. Assuming that the 1 for 10 is approved, many investors think that the 900 million share authorization cap would be adjusted to 90 million - wrong! The 900 million remains the cap even if there is a reverse split. Indirectly, therefore, shareholders would allow for an additional 810 million post reverse split shares to be issued or 8.10 billion shares based on current pre-reverse stock split numbers.

They need a majority of shares "entitled" to vote to approve the proposal - not the majority of shares voted at the meeting. The shareholder record date is March 27. The company asserted in their proxy statement that they feel this will be considered a "routine" matter, which means a broker can vote if their customer has not voted. Since brokers almost always vote according to management's recommendations, this should pass.

There is an SEC minimum requirement of at least 10 days between filing a preliminary proxy statement and filing a definitive proxy statement, so I would expect a definitive proxy statement should be filed soon because the preliminary proxy statement was filed on March 17.

A 1 for 10 reverse stock split would most likely also cure the problem of BBBY selling below $1.00 per share for 30 consecutive business days that could cause a NASDQ delisting under Rule 5550(a)(2) . BBBY has traded under $1.00 since March 20. They need to file a definitive proxy statement, vote to approve, and have the reverse split become effective quickly before the 30 days run out or the stock needs to trade over $1.00.

Amended Credit Agreement

Another filing on March 30 included an amended credit agreement. The total lending commitment was reduced to $300 million from $565 million. There were a number of new restrictions added to the agreement, and some waivers were granted. Currently, they have $101.5 million borrowed under the agreement plus $105.6 million in letters of credit. They only have $11.5 million currently available to borrow because certain metrics determine the actual amount available.

I just do not see how Bed Bath & Beyond can get past the "minefield" of requirements/restrictions contained in this agreement without blowing up and ending up in bankruptcy court.

Potential Defaults and Potential Bankruptcy

While not all defaults automatically trigger a bankruptcy filing, there is a significant risk that it could. Besides the long list of typical items that trigger a default and/or bankruptcy filing, there are some interesting ones that investors need to pay attention to that could result in default and/or bankruptcy:

*Trading of the common stock on The Nasdaq Stock Market or another national securities market shall have been suspended for a period of at least 3 consecutive Business Days.

*Common stock shall not be listed for trading on The Nasdaq Stock Market or another national securities market.

*Termination or even suspension of the Sales Agreement with B. Riley Securities.

*If they are unable to receive shareholder approval for the reverse stock split.

This is the reality as stated in the prospectus :

If the Company does not receive the proceeds from the offering covered by this prospectus supplement, the Company would not have the financial resources to satisfy its payment obligations under the Credit Facilities, and the Company expects that it will likely file for bankruptcy protection and that its assets will likely be liquidated. The Company has engaged advisors to explore strategic alternatives, including, if needed, filing for bankruptcy protection. Holders of our common stock would not receive any recovery at all in a bankruptcy scenario.

Latest Preliminary Results

4Q period ending February 25 :

*Net Sales of approximately $1.2 billion

*Comparable Sales decline in the 40% to 50% range

*Continuation of negative operating losses

*Modest free cash flow usage

Considering they closed a large number of stores, one would have thought that selling a large amount of inventory would have generated a significant amount of cash. Interesting that they did not actually state the amount of operating losses.

(A note of caution regarding future earnings/loss per share. As the average number of shares outstanding for a specific reporting period increases, the loss per share will decline. Do not be fooled into thinking operations are improving by looking at just the per share numbers.)

Unsecured Notes

While dilution has a negative impact on BBBY shareholders, noteholders do not care about shareholder dilution. They just want cash to be raised, so the company stays out of bankruptcy.

Since there have been a number of comments about the 3.749% 8/1/2024 unsecured notes (CUSIP 075896AA8) I am including this chart. This chart is also an indicator of a potential bankruptcy filing.

If Bed Bath & Beyond files for Ch.11 bankruptcy and reorganizes under a typical reorganization plan, the noteholders might get some token recovery, such as the right to participate in some rights offer. If they, however, file for Ch.7 or liquidate in Ch.11, it is fairly unlikely that noteholder will get much, if any, recovery.

3.749% 8/1/2024 Unsecured Notes Price

finra-markets.morningstar.com

Conclusion

Even after raising a ton of new cash via stock offers, Bed Bath & Beyond's operating business model is imploding. I am assuming that vendors are demanding very strict terms when dealing with this potential bankrupt retailer, which puts even more pressure on the company's cash position. When stores are low on product to sell, they will also be low on customers shopping.

There are a number of details in the latest filings that I did not include in order to make this article understandable with a wide range of readers. These details, however, did impact my analysis of BBBY stock.

I originally thought that after they made the new financing announcement earlier this year, they might be able to avoid bankruptcy. Given the terrible latest operating results and the much more restrictive amended credit agreement, I think Bed Bath & Beyond will enter bankruptcy court. Now the only thing to debate is it going to be Ch.7 or Ch.11 bankruptcy. At this point, only irrational meme trading, in my opinion, can save this retailer. I continue to rate BBBY a sell.

For further details see:

Bed Bath & Beyond Is Most Likely Headed Into Bankruptcy Given The Latest SEC Filings