BBBY - Bed Bath & Beyond: The Last Nail In The Coffin

2023-04-24 01:01:26 ET

Summary

- The management team at Bed Bath & Beyond announced that the firm had voluntarily entered into Chapter 11 Bankruptcy protection.

- Instead of restructuring, the business looks slated to wind down substantially all of its operations.

- Some remnants may survive, but they will likely be small and will leave common shareholders wiped out.

April 23 proved to be a really awful day for shareholders of beleaguered retailer Bed Bath & Beyond ( BBBY ). Although the market was closed for the day because it was Sunday, the management team issued a press release on the company's website in which it announced that the company had "voluntarily" filed a Chapter 11 bankruptcy petition. Shares of the enterprise already were trading well under $1, so investors had essentially already been wiped out by this point. But this serves as the final nail in the coffin for the firm. At this point, the best thing that investors can do is salvage what little capital they might by selling their stock. Due to these circumstances, the company certainly warrants a "strong sell" rating at this time.

The end of an era

Understanding the history of Bed Bath & Beyond up to this point paints a rather interesting and sadly poetic picture for shareholders. I say this because the company's origins can be traced back to the collapse of another retailer, called Arlan's. At that time, Warren Eisenberg and Leonard Feinstein were employed at Arlan's in management positions. But believing that the chain was likely to collapse (it did in 1973), they struck out on their own in 1971 to create the first Bed Bath & Beyond, then called Bed 'n Bath. From these humble origins, the company grew to become a major retailer that employed tens of thousands of people at any given time and that generated billions of dollars in revenue per year. But alas, changing market conditions, combined with poor management decisions, ultimately led to its own collapse this year.

{kind=link}

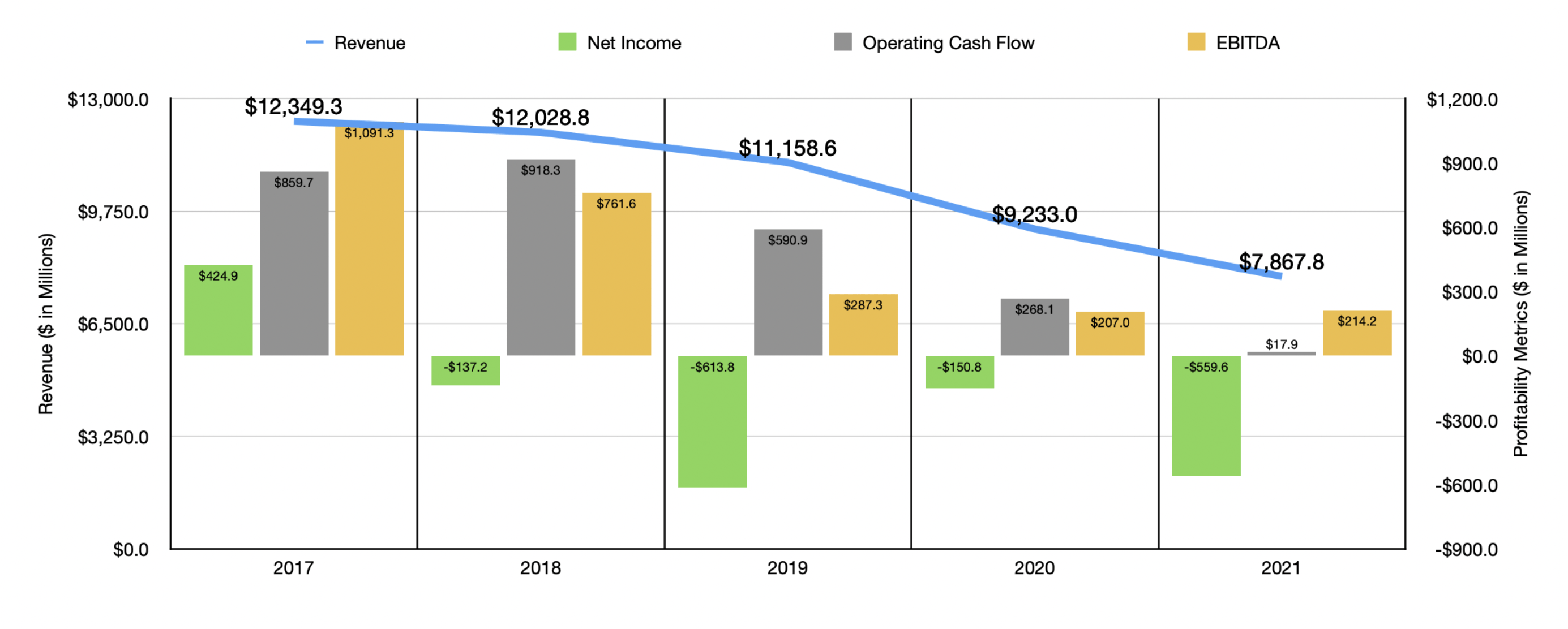

As I detailed in an article published late last year, the retail chain's decline has been years in the making. Back in 2017, for instance, the company generated revenue of $12.35 billion. By 2021, that number had fallen to $7.87 billion. 2017 was actually the last year that the firm generated a net profit. And every year between then and now has been worse than the year before. Although the COVID-19 pandemic certainly took a chunk out of the enterprise, asset sales in the years leading up to that had a major impact as well. Competitive market conditions caused a reduction in traffic at the company's stores and management made some rather awful moves when it came to capital allocation. The most significant involved the firm's decision to buy back $574.9 million worth of shares in 2021. This was followed up by $40.4 million worth of share buybacks in the first nine months of 2022. In fact, from December of 2004 through the present day, the company allocated $11.73 billion toward buying back 265 million shares on the market. Looking back, that was a monumental waste of capital.

This is not to say that every decision made by management was a bad one. In 2019, recognizing that something had to change, the company began selling off certain non-core assets. They used some of these proceeds to reduce debt. The company also focused on building out brand name offerings of its own. Conceptually, this is a wise move since it tends to result in stronger profit margins for the retailers that can pull it off. But when coupled with the share buybacks that the company engaged in, these maneuvers were too little and too late. In my initial article on the company last year, I left open the possibility that the company could experience some nice upside if its major initiatives resulted in success. But I was skeptical of these maneuvers succeeding and, as a result, I ended up rating the company a 'sell'. Since then, shares have plunged 87.8% at a time when the S&P 500 is up 8.6%.

True financial distress

I don't think any reasonable person would have disagreed that the company was experiencing financial distress. But I do think it's surprising that the company entered into Chapter 11 bankruptcy protection when it did. Earlier this month, management was pushing the recommendations from companies like Glass Lewis and ISS all of the proposals that were to be voted on at the next shareholders meeting. One of these proposals involved a reverse split of the company's stock aimed at ensuring compliance with the exchanges and, ideally, aimed at reducing market volatility in a bid to calm the nerves of investors. Also this month, management even announced the launch of a vendor consignment program under a third party agreement whereby its partner would purchase up to $120 million, on a revolving basis, of pre-arranged merchandise from Bed Bath & Beyond's primary suppliers. This kind of strategy would help the company increase its inventory without technically having to acquire that inventory itself. This is the kind of strategy that a company makes when it is still trying to survive, not planning for bankruptcy.

{kind=link}

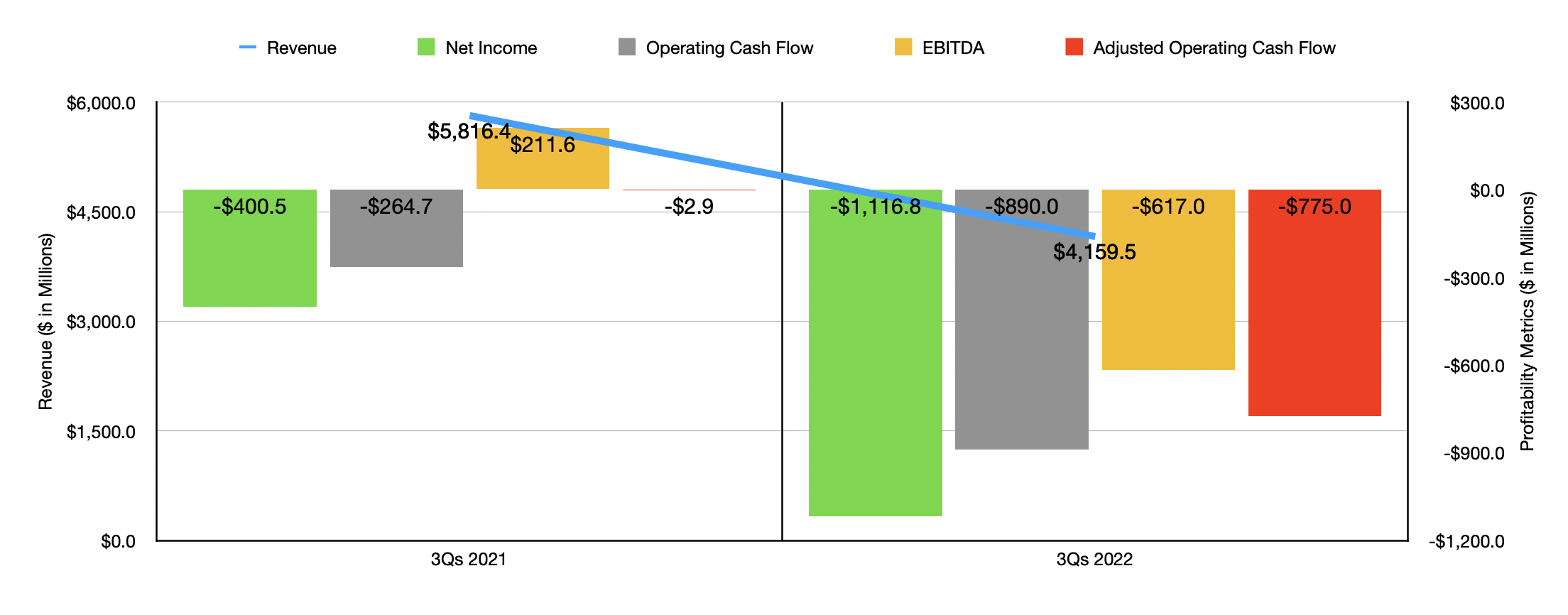

If the consignment strategy seems peculiar, keep in mind that a lot of the company's woes as of late have been caused by a plunge in comparable store sales. During the first nine months of the 2022 fiscal year, for instance, revenue at the business totaled $4.16 billion. This was down substantially from the $5.82 billion that the company reported the same time one year earlier. A big driver behind this drop was a 23% decline in comparable store sales, with the third quarter alone experiencing a 32% plunge. Management did reveal some preliminary results for the fourth quarter. They said that revenue there was about $1.2 billion, with comparable store sales declining by between 40% and 50% year over year. Changes in consumer appetite that have been caused by broader economic conditions are one reason why the business experienced so much weakness on this front. But management also said that a lack of inventory was also to blame.

{kind=link}

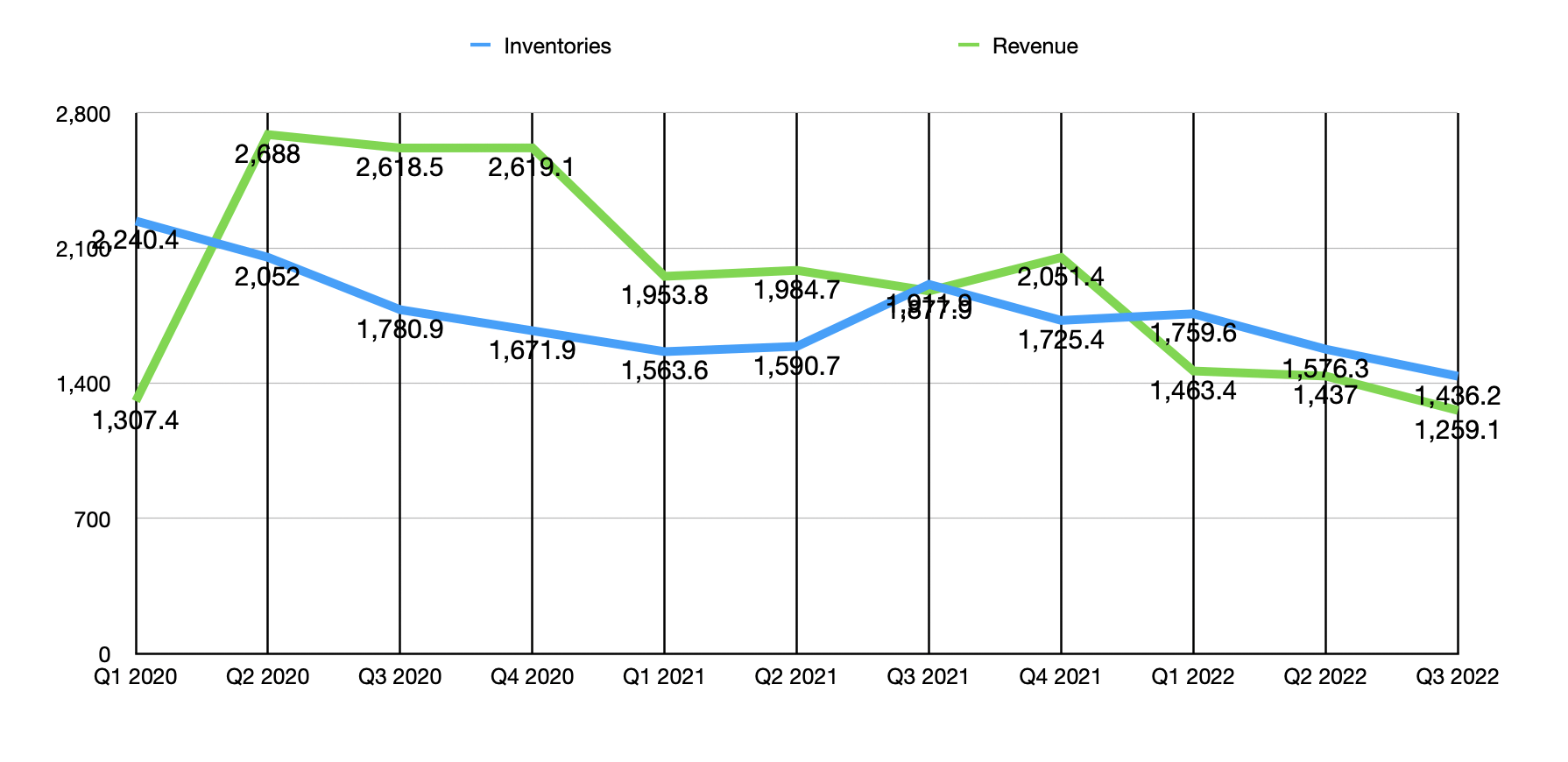

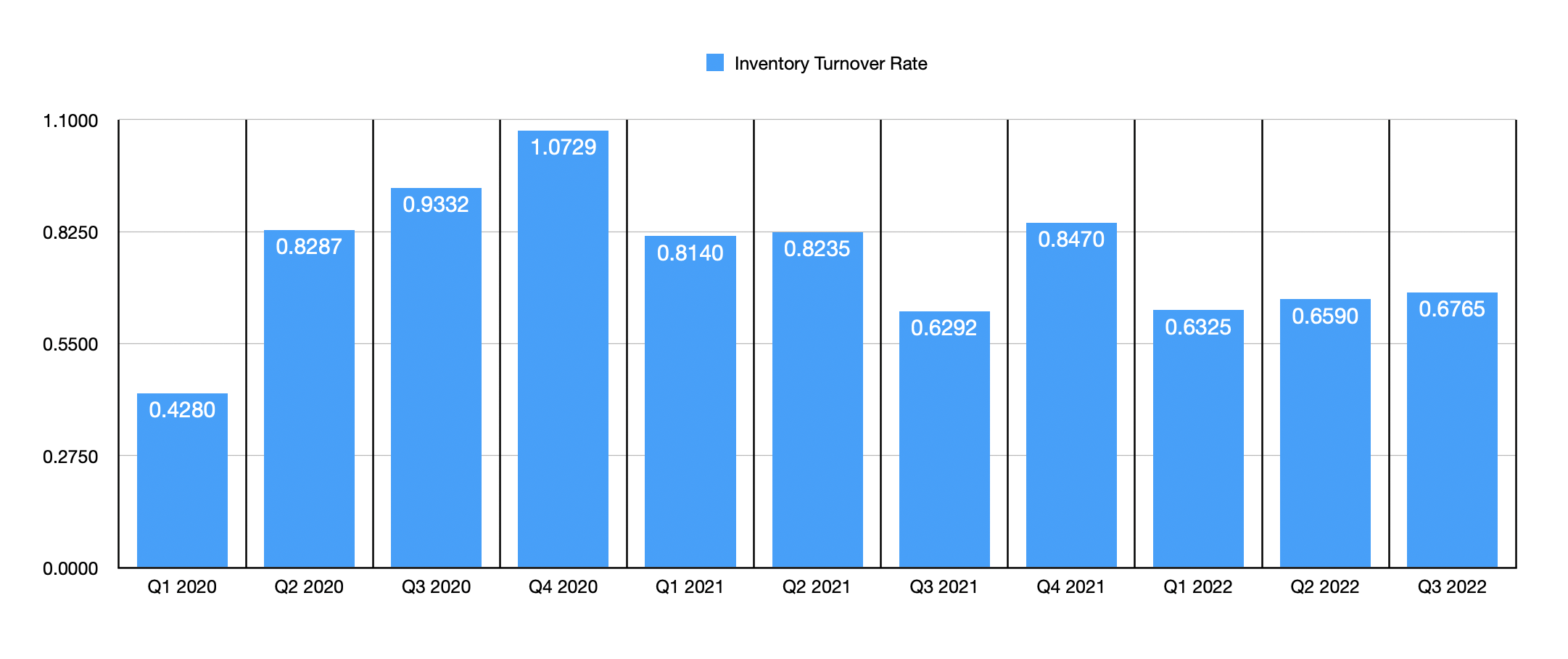

In the broader economy, inventory actually seems to be in excess. But according to management, macro and micro economic challenges that developed since the end of the second quarter of the 2022 fiscal year caused an acceleration of vendor payment terms and credit line constraints. This ultimately led to lower inventory receipts than the company had anticipated for the third quarter. And that's particularly problematic when you consider that the third quarter is supposed to be a build-up to the busiest shopping season of the year. To put this in context, inventory levels at the end of the third quarter last year came out to $1.44 billion. That was down substantially from the $1.91 billion in inventories the company reported one year earlier. In the charts above and below, you can see how the picture has changed since 2020. Both 2021 and 2022 saw a significant deterioration in inventory levels that helped to drive revenue lower. This manifested itself not only in inventory levels, but also in the inventory turnover rate.

{kind=link}

As for the future, nobody knows exactly what will happen. Almost certainly, Shareholders in the company will be wiped out entirely. What I did find out that was interesting, however, was that the business is pursuing a Chapter 11 bankruptcy and yet is still talking about winding down its operations. Normally, a complete wind down would involve a Chapter 7 filing. But I think that the reason for the Chapter 11 stems from the fact that management stated in their press release that they would market some of the assets under both the Bed Bath & Beyond and the buybuy BABY brand names with the hope of salvaging some value during this process. To help fund operations in the meantime, the company did lock down $240 million of DIP (debtor-in-possession) financing from Sixth Street Specialty Lending. This lending will take top priority in the pyramid of who gets paid back first. But it will be incredibly important in ensuring that operations continue as the company goes through this process.

Based on my own assessment, the company will likely be able to salvage very little of significant value. I say this because it wasn't even the debt service that was the problem. You see, when you have an enterprise that has a significant amount of leverage on its books, one good way to know if it can be a viable enterprise without the debt is to look at the fundamental performance if interest expense no longer existed. In the first nine months of the 2022 fiscal year, Bed Bath & Beyond had operating cash flow that was negative to the tune of $890 million. Even if we adjust for changes in working capital, it would have been negative in the amount of $774.95 million. By comparison, interest expense during that window of time was a paltry $68.58 million. What this means is that the overall operational structure of the company was far worse than what it could have been in order for a true restructuring to take place.

Takeaway

As a child, I had a number of memories going into Bed Bath & Beyond. Although I never had a strong attachment to the company, it's sad to see it go the way of so many other retail chains over the prior several years. Investors in the company are certainly out of luck. However, this may serve as a learning lesson, not only for investors, but also for other retailers that might one day find themselves in this kind of position. It's important to know when market conditions are changing for the worse and whether those changes are permanent or not. It's important to act quickly when these changes do develop. And it's incredibly important not to make bad decisions like allocating significant amounts of capital to buying back stock or paying dividends when that capital could be put to better use growing the business and optimizing its operations. For Bed Bath & Beyond, these lessons came too late. But hopefully investors who were caught up in this can see the writing on the wall earlier next time as a result of what is now transpiring.

For further details see:

Bed Bath & Beyond: The Last Nail In The Coffin