COST - BellRing Brands: Great Growth But A Bit Pricey

Summary

- BellRing Brands has been doing really well as of late, with sales and cash flows largely rising over time.

- This has established the company as an important and valuable player in its space.

- But shares of the firm don't look as attractive as I would like them to be to make for quality plays.

If there's one truth that has made itself clear to me over the years, it's that our health is everything. This is a lesson that most people learn at some point or another in their lives. And the realization of that truth can be tied to significant business opportunities for the companies that can best provide the goods and services to help us live the lives that we want to live. One firm in this space that investors should be aware of is BellRing Brands ( BRBR ). The firm has spent years solidifying itself as a fairly sizable player in the nutrition goods space. And the overall trajectory of the company from a fundamental perspective has mostly been positive. But this doesn't mean that it makes for an ideal prospect for investors to consider. Based on how shares are priced at the moment, I think a more appropriate rating for the company would not be a ‘buy’ but would, instead, be a ‘hold’.

A niche player

According to the management team at BellRing Brands, the company operates as a global leader in the convenient nutrition category of products. Their ultimate goal from a mission perspective is to enhance the lives of its consumers by providing them with nutritious, great-tasting products that they can enjoy throughout their day. Today, its two primary brands are Premier Protein and Dymatize. The first of these brands consists of a portfolio of RTD (ready-to-drink) protein shakes, protein beverages, and protein powders. In all, the company’s flagship RTD protein shakes, are available in 14 different flavors and they contain 30 grams of protein and only one gram of sugar, with 160 calories in the mix. The company also has other offerings such as a Premier Protein with Oats shake line that emphasizes additional fiber. Meanwhile, Dymatize is targeted toward fitness enthusiasts, with most of its sales consisting of protein powders. As of the end of its 2022 fiscal year, the Premier Protein portfolio of products accounted for the lion's share of the company's sales, totaling 81% of revenue in all. 15.4% of sales came from its Dymatize brand, with the remaining 3.6% attributable to other products the company sells.

For clarity's sake, it is worth mentioning that the company has a rather complicated operational history. The company was originally spun off from Post Holdings ( POST ) in October of 2021. After a series of transactions over the ensuing months, it became, in March of 2022, a new publicly traded company and the successor to the old spun-off enterprise. Prior to all of this, the company was formed by combining multiple acquired businesses that Post picked up between 2013 and 2015. Due to the size that it was able to grow to as a result of these combinations and the leadership it experienced under Post, the company grew to become a rather sizable player in its market, with sales occurring across club stores, online retailers, specialty retailers, convenience stores, distributors, and more. Today, it even boasts some major players such as Costco Wholesale Corporation ( COST ) and Walmart ( WMT ), entities that collectively accounted for 63.5% of its sales in 2022.

{kind=link}

Author - SEC EDGAR Data

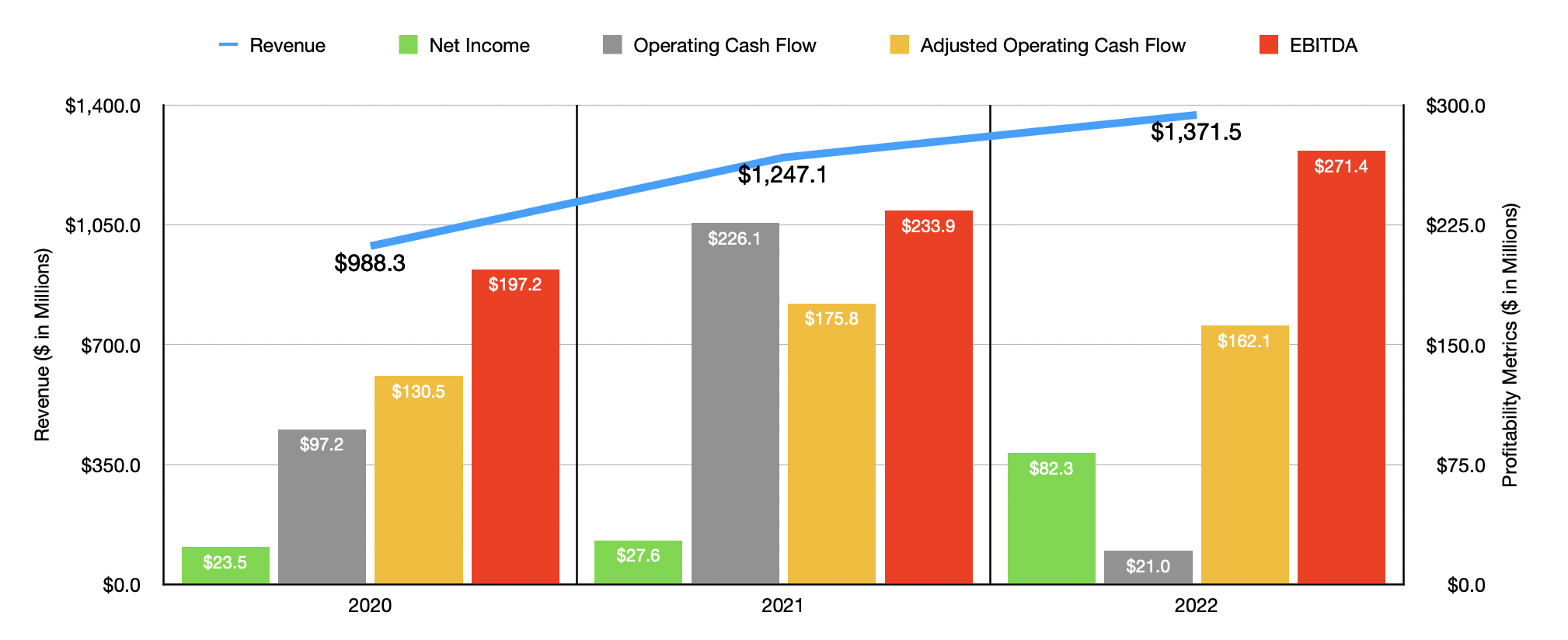

In the past three years, the company has done quite well for itself. Between 2020 and 2022, sales increased consistently, rising from $988.3 million to $1.37 billion. The increase from 2021 to 2022 of roughly 10% was driven largely by its Dymatize portfolio, with sales there jumping 35% thanks to higher average net selling prices. This is not to say everything was great on that front though. Volume declined during that time by 5%, driven in part by an unwillingness by customers to pay the higher prices and product discontinuations initiated by management. Although on a percentage basis, Dymatize did the heavy lifting, in dollar terms the largest growth came from the firm’s Premier Protein products, with sales jumping $75.2 million, or 7%, thanks to higher average net selling prices. Unfortunately, volume did decline in response to this in the amount of 8%.

The rise in revenue brought with it increased profits. Net income, for instance, expanded from $23.5 million to $82.3 million. Unfortunately, operating cash flow was a bit lumpy, rising from $97.2 million in 2020 to $226.1 million in 2021 before plunging to $21 million in 2022. But if we adjust for changes in working capital, the decline was more modest from $175.8 million in 2021 to $162.1 million last year. The only profitability metric other than net income that increased year over year was EBITDA. Between 2020 and 2022, the symmetric increased from $197.2 million to $271.4 million.

At this time, management seems very optimistic about the future. For 2023, the firm is anticipating revenue of between $1.56 billion and $1.64 billion. At the midpoint, that would translate to a year-over-year increase of 16.7%. This should help drive EBITDA up to between $300 million and $325 million. Unfortunately, we don't have guidance when it comes to other profitability metrics. But if we assume that those will increase at the same rate that EBITDA is forecasted to, then we should anticipate net income of $94.8 million and adjusted operating cash flow of $186.6 million. Management is so excited, in fact, that on December 5th of last year, they announced that they were initiating a $50 million share buyback program. Although this is small compared to the $3.6 billion market capitalization of the firm, it is interesting to see the company consider buying back stock at a time when it's growing so quickly. Normally, you would expect to see the company reinvest the cash in further growth.

{kind=link}

Author - SEC EDGAR Data

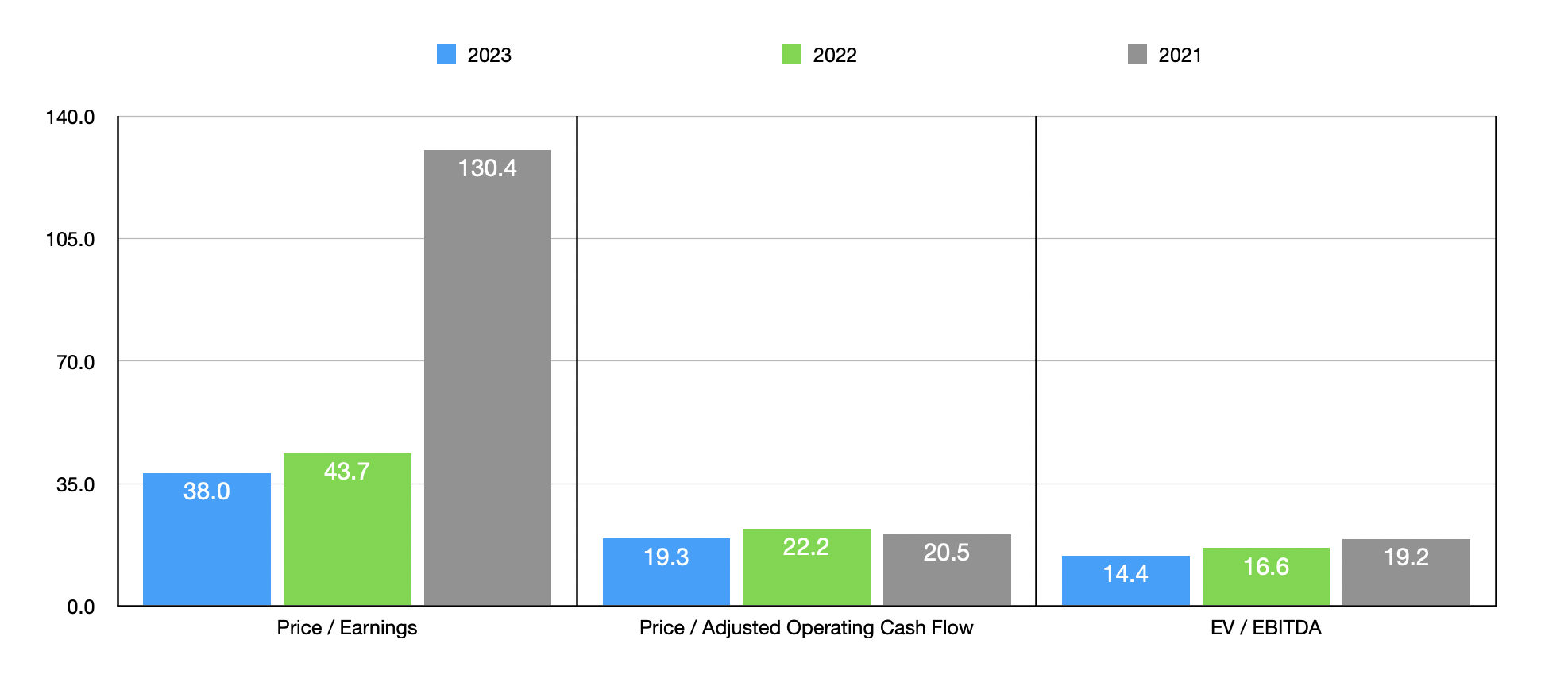

In the chart above, you can see pricing for the company based on data for 2021 and 2022, as well as projections for 2023. Given that 2022 data just recently came out, I've decided to value the company based on that. On a price-to-earnings basis, the firm is trading at a multiple of 43.7. The price to adjusted operating cash flow multiple is considerably lower but still quite high at 22.2. And the EV to EBITDA multiple for the company is lower still at 16.6. But to put all of this in perspective, I decided to compare the company to five similar firms. On a price-to-earnings basis, these companies range from a low of 4.5 to a high of 59.3. Four of the five businesses are cheaper than BellRing Brands. Using the price to operating cash flow approach, the range was from 2.8 to 12.3. And when it comes to the EV to EBITDA approach, the range was from 5.5 to 8.7. In each of these scenarios, our prospect was the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| BellRing Brands |

| 43.7 |

| 22.2 |

| 16.6 |

| Medifast ( MED ) |

| 9.1 |

| 10.1 |

| 5.9 |

| Herbalife Nutrition ( HLF ) |

| 4.5 |

| 4.2 |

| 5.5 |

| Nu Skin Enterprises ( NUS ) |

| 59.3 |

| 11.4 |

| 8.7 |

| WW International ( WW ) |

| 4.5 |

| 2.8 |

| 7.9 |

| Usana Health Sciences ( USNA ) |

| 14.1 |

| 12.3 |

| 5.9 |

Takeaway

With what data I have in front of me today, I would say that, from a purely fundamental perspective, I am a fan of this enterprise. I've never tried its products, nor would I be likely to. But I like the numbers that I see, particularly the rapid growth the company is experiencing. But even rapid growth has a price that an investor should not pay above. And in my opinion, this firm is on the edge of that. I can understand why somebody would purchase shares of the firm. But for value-oriented investors, including those who like GARP investing, I would say that a ‘hold’ rating is more appropriate at this time.

For further details see:

BellRing Brands: Great Growth But A Bit Pricey