NGLOY - BHP: Why Metals And Mining May Be The Best Hedge For Your Oil Stocks

2023-10-08 11:24:14 ET

Summary

- The energy transition is placing a massive call on the metals and mining sector.

- Supply is lagging in expected demand and BHP, as the owner of low-cost mining assets, is positioned well for the trend.

- Once the short-term China headwinds dissipate, commodity prices and BHP's earnings will revert to higher levels.

- BHP hedges both oil (if electrification accelerates) and inflation; the stock also pays a generous dividend.

Investment thesis

How does BHP Group Limited (BHP), one of the largest diversified mining companies globally, fit into an energy investment thesis?

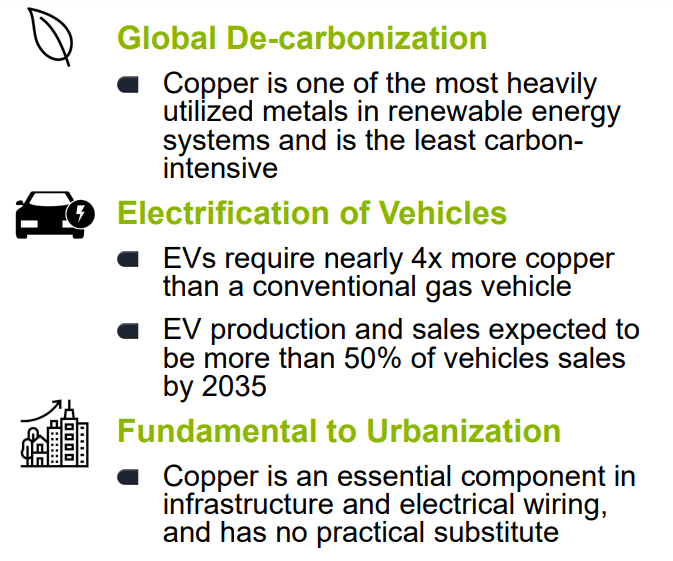

Despite the exceptional 2021-2022 run-up, energy continues to offer some of the best value opportunities - particularly among stocks with offshore exposure and oilfield services. The opportunity is there because fossil fuel demand won't ramp down as quickly as the International Energy Agency (the IEA) or others want you to believe. Hence, the underinvestment in supply over the last 10 years will lead to a market equilibrium characterized by higher prices and this situation will last for longer. The beneficiaries will be those who have claims on advantaged energy assets - whether these are low-cost oil reserves or scarce capital equipment such as offshore drilling rigs. As these assets are also real assets, they should see further upside from the inflationary regime that now characterizes much of the global economy.

That, in a nutshell, is my energy thesis which is probably shared by many others too. However, I constantly reevaluate this reasoning and ask myself what else needs to hold true for my energy investments not to work out. The answer I inevitably come back to is that we would need to see a massive acceleration in the electrification trend that would at least displace the transportation component of oil demand. Perhaps emerging economies like India ((INDA)) manage to bypass the wider adoption of ICE vehicles and directly go to EVs - or maybe the decarbonization in developed countries happens quicker due to technological breakthroughs.

I personally remain skeptical the energy transition will be completed by 2050 because the entire decarbonization project appears to be more based on ideology and political incentives than on sound economic planning that takes into account the physical realities. For example, cloudy countries in Northwest Europe keep installing solar panels; this makes little sense from ROI perspective but perhaps helps electioneering politicians score more points with an "environmentally conscious" voter base. In either case, for my energy thesis to be wrong and decarbonization to succeed on the 2050 timeframe, the world would require massive amounts of critical metals and minerals and even net-zero proponents as the IEA acknowledge this. This naturally points to the mining industry as a "hedge" if oil gets phased out faster - and within mining, BHP is one of major players with exposure to several critical resources.

BHP's mining portfolio has shifted over the years, but, after the sale of its petroleum business to Woodside ( WDS ), currently the group focuses on the following resources :

- Copper ( COPX ) and Nickel ( JJN ), used by solar farms, wind farms and EVs;

- Iron ore ( SCO:COM ) and metallurgical coal for steel ( SLX ) production, with steel being necessary to build new renewables infrastructure such as wind turbine towers;

- A new investment in potash for fertilizers, which though not electrification related, enables more sustainable farming;

- Smaller production of gold ( IAU ), an inflation hedge, and uranium ( SRUUF ), another important enabler for quicker decarbonization.

If the world wants to cut down on fossil fuels quicker, it has to consume a lot more of BHP's products, at least in the next few decades, to build out the new infrastructure that would support a low-carbon economy. Mining itself is very energy intensive, so to some extent producing the metals and minerals necessary for decarbonization will require even more fossil fuels, but let's assume that's only a short-term effect and in the long-run net fossil fuel use will still drop.

BHP is certainly not the only miner out there, but I think the company has several advantages that make it stand out:

- Well-established operations; junior miners clearly have greater risk-reward, but with high interest rates (translates into more expensive project financing, assuming you can even get it) and rising resource nationalism (more difficult to secure mining permits), I don't want to bet on any company that doesn't already have a fully functioning mine;

- Some of the largest and lowest cost assets globally; for example, BHP owns 57.5% of Escondida (in Chile), the largest copper mine in the world ;

- A shareholder friendly capital return policy that mandates dividend payouts of at least 50% of net profit; with the economy "hard landing" still not out of the picture, no one knows when exactly copper and iron ore prices will spike again - but why not get paid to wait in the meantime?

- Last but not least, BHP's valuation is quite reasonable compared to the mining sector.

BHP's year-to-date return is a negative -7.2%, but let's be clear - the only reason for this year's underperformance are fears over China's economy. Yet, the government in China is already focusing on stimulative measures and there are signs that investors' China sentiment may have bottomed. The markets are also forward looking, so commodity futures and BHP's stock will reprice way before the economic indicator data starts improving. As much as China remains the main risk, the inevitable turnaround in the China narrative may also be the catalyst that takes BHP higher.

What does the energy transition mean for the mining industry?

The short answer is that the world will need a lot more of everything. The Tesla ( TSLA ) in your garage only substitutes one type of non-renewable resource for a different one. Running away from oil and gas means crowding into the mining sector, and we know what happens when much higher demand meets finite supply. To the IEA's credit, their recent report , entitled "Mineral requirements for clean energy transitions", tried to quantify these exact megatrends.

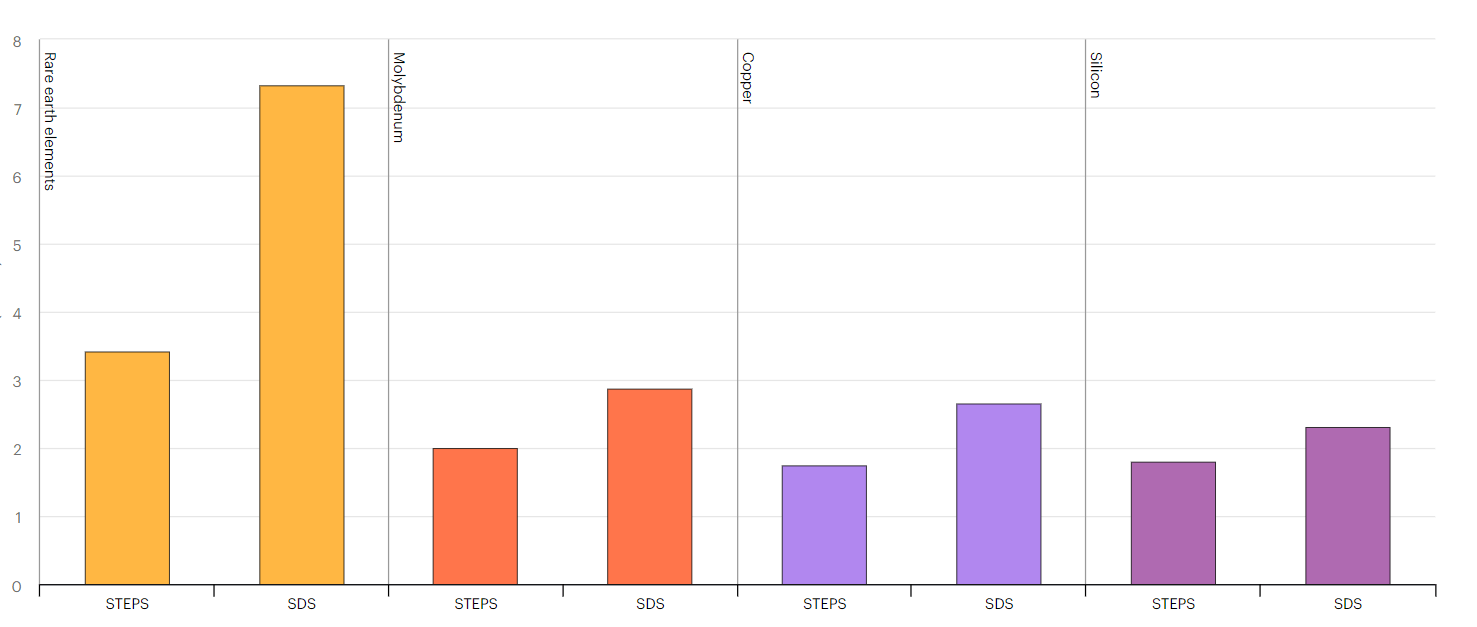

The IEA distinguishes between a "stated policies" scenario (STEPS), associated with a slower energy transition, and a "sustainable development" scenario (or SDS), which implies even faster decarbonization. The chart below shows the projected 2040 growth factor from 2020 demand levels, by resource type:

{kind=link}

Copper demand, of relevance to BHP, is expected to grow by a factor of 2x to 3x, depending on how quickly the energy transition moves! In 2020 the world consumed 23.5 million metric tons (or MT) of copper so this is no small deal.

The IEA explains:

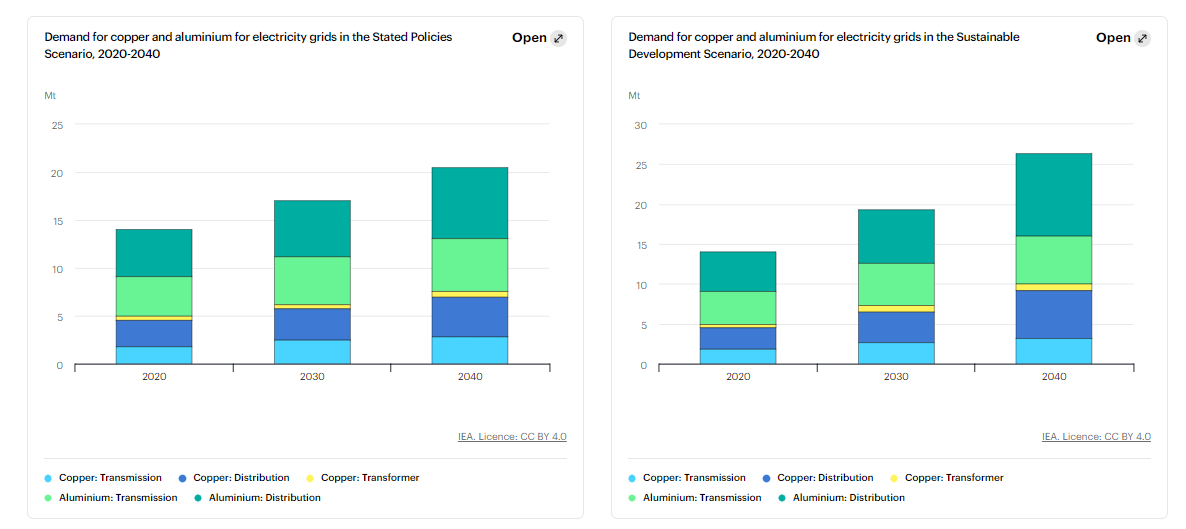

The huge expansion of electricity grids requires a large amount of minerals and metals. Copper and aluminum are the two main materials in wires and cables, with some also being used in transformers. Copper has long been the preferred choice for electricity grids due to its high electrical and thermal conductivity...

... Annual copper demand for electricity grids grows from 5 Mt in 2020 to 7.5 Mt by 2040 in the STEPS and to nearly 10 Mt in the SDS. Aluminum demand increases at a similar annual pace, from 9 Mt in 2020 to 12.8 Mt in the STEPS and 16 Mt in the SDS by 2040.

{kind=link}

On the production side, the IEA warns of the forthcoming challenges (my highlights):

In the near term, we expect demand to be met by a combination of rising primary and scrap supply. A small surplus or a balanced market is the most likely outcome for the current year, with operational disruptions being a key swing factor. In the medium and longer term, traditional demand (such as home building, electrical equipment and household appliances) is expected to remain solid while the decarbonization mega-trend is expected to bolster demand. In terms of meeting that demand, we anticipate that the cost curve is likely to steepen as challenges to the development of new resources (such as societal expectations, decarbonization and water challenges) progressively increase. We anticipate that the industry is likely to enter the final third of this decade with a low inventory buffer and therefore elevated prices may endure throughout this period .

Beyond the electric grid, solar power capacity will also be a demand driver per the IEA:

In the SDS, capacity additions in 2040 are triple those of 2020, resulting in a near tripling of copper demand from solar PV (photovoltaics). However, potential material intensity reductions could significantly dampen demand growth for both silver and silicon, with 2040 levels only 18% and 45% higher than in 2020.

Maybe not as bullish for silver and silicon but copper is again the common denominator.

Wind power, in turn, will drive both copper and steel (iron ore) demand. I recently analyzed the woes of wind giant Ørsted which is exposed to the rising cost of materials. And wind infrastructure requires a lot of material:

According to the U.S. Geological Survey, wind turbines typically consist of:

steel (66% to 79% of total mass)

fiberglass, resin or plastic (11% to 16%)

iron or case iron (5% to 17%)

copper (1%)

aluminum (0% to 2%)

Going back to the IEA's projections:

Over the next two decades, wind power is set for strong growth, with the offshore wind industry maturing and adding to developments in onshore wind on the back of technology improvements and low-cost financing.

Wind turbines require concrete, steel, iron, fibreglass, polymers, aluminum, copper, zinc and REEs (rare earth elements). Mineral intensities not only depend on the turbine size, but also on the turbine type. For example, turbines based on permanent-magnet synchronous generators - which dominate the offshore market due to their lighter and more efficient attributes as well as lower maintenance costs - require REEs.

Metallurgical coal itself isn't a direct input for electrification but indirectly steel production (blast furnace) still requires its use.

Finally, nickel, another of BHP's inputs is also a critical enabler for the energy transition:

The properties of nickel facilitate the deployment of the entire spectrum of clean energy technologies - geothermal, batteries for EVs and energy storage, hydrogen, hydro, wind and concentrating solar power. It is also necessary in nuclear energy technologies as well as carbon capture and storage.

Source: Nickel Institute

In sum, the energy transition guarantees the demand for BHP's outputs. Let's examine next the supply side.

BHP is a low-cost supplier in a tightening market

Portfolio overview

During its 30 June 2023 financial year, BHP produced the following quantities:

{kind=link}

To put these numbers into context:

- BHP produced about 7-8% of the world's cooper;

- 10% of the global iron ore output;

- About 1/5th of the metallurgical coal exports globally;

- About 2.5% of the global nickel production.

In addition, per BHP:

Among our by-products, we are a major producer of uranium and, following the acquisition of OZ Minerals in May 2023, we expect to become a major producer of gold.

For the June '23 year revenue and EBITDA were weighted towards iron ore:

BHP Form 20-F, Author's calculations

However, this can change quickly with the price of the underlying commodities. Compared to Rio Tinto ( RIO ) and Vale ( VALE ) which are even more heavily weighted towards iron ore, BHP is much better diversified.

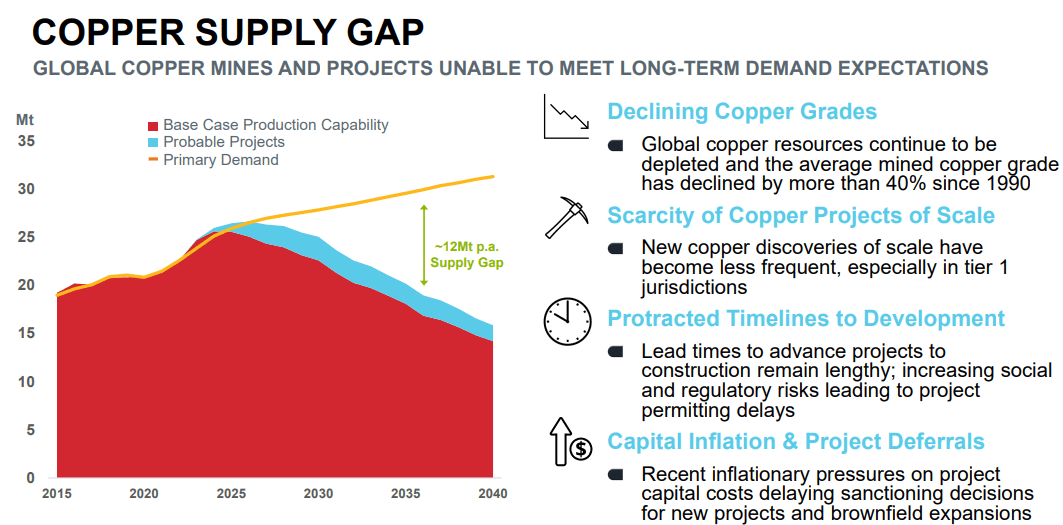

Copper supply lags demand

While copper was only 30% of BHP's revenue, BHP as noted is one of the largest producers globally and has a 57.5% stake in the largest copper mine globally. These assets may prove quite valuable in a few years as copper supply is lagging behind what is required for the energy transition. For example, copper producer Hudbay Minerals Inc. ( HBM ) sees demand outpacing supply as early as 2025:

{kind=link}

{kind=link}

The supply concerns are shared by S&P which sees low capital expenditures despite high profits in the industry:

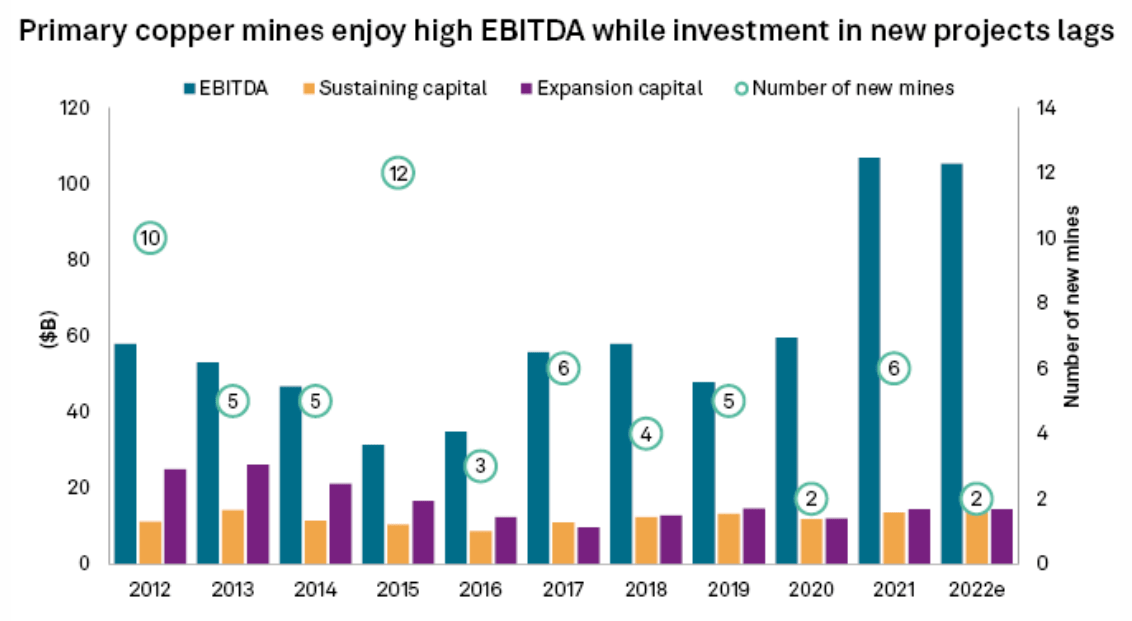

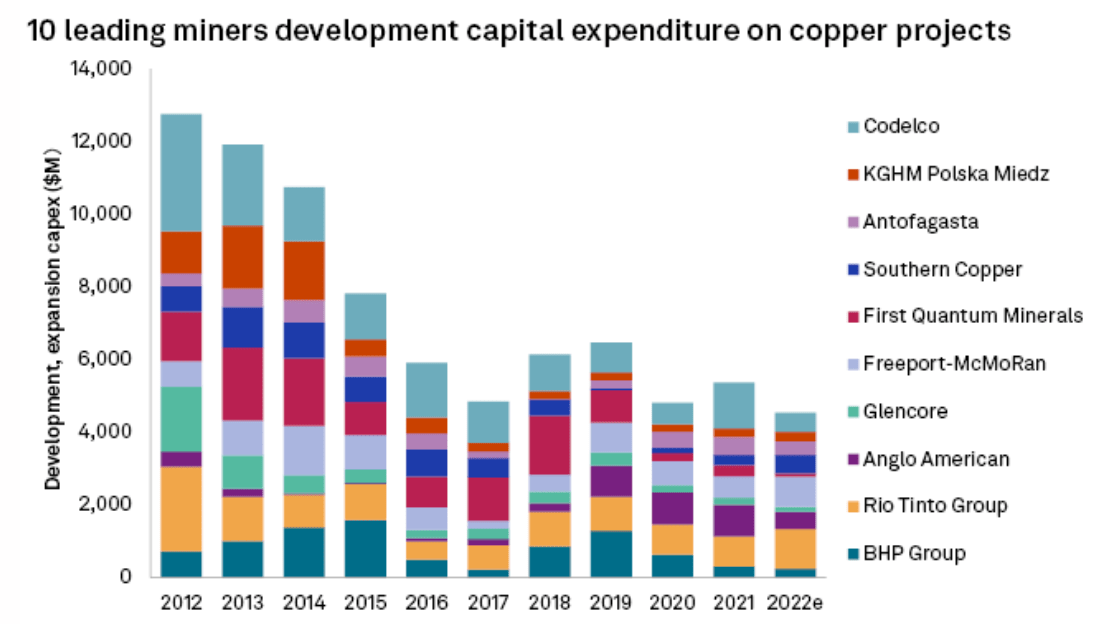

Global development and expansion capital for primary copper mines peaked in 2013 at $26.13 billion, almost halved in subsequent years and has not recovered since. Capital spend on copper projects is estimated to have been only $14.42 billion in 2022, based on Mine Economics' universe of coverage. There was an estimated 0.1% reduction year over year in development capital expenditure for copper projects in 2022, and a further decrease of 18.7% is projected for 2023.

{kind=link}

{kind=link}

The causes, according to S&P, include permitting and financing difficulties among others:

Copper miners have become conservative about investing in new projects. It takes a long time to discover, explore, permit, finance and develop new mines. Companies have been focusing their capital expenditures on extending the mine life of operating high-grade, profitable projects that are already producing, rather than investing in exploration and development of new projects to meet increasing demand. It could take a long time to reverse this trend, as most copper companies have enjoyed record earnings from high copper prices.

The market copper price reached a historic high of $4.42/lb in 2021. The previous record of $3.59/lb in 2012 was much higher than the level required for new and expansion projects to be profitable, with a total cash margin averaging $1.79/lb. Post 2011, the copper price went through a prolonged downturn, which, along with high debt levels carried by producers, discouraged approval of new mines and drove a gradual reduction in development spending.

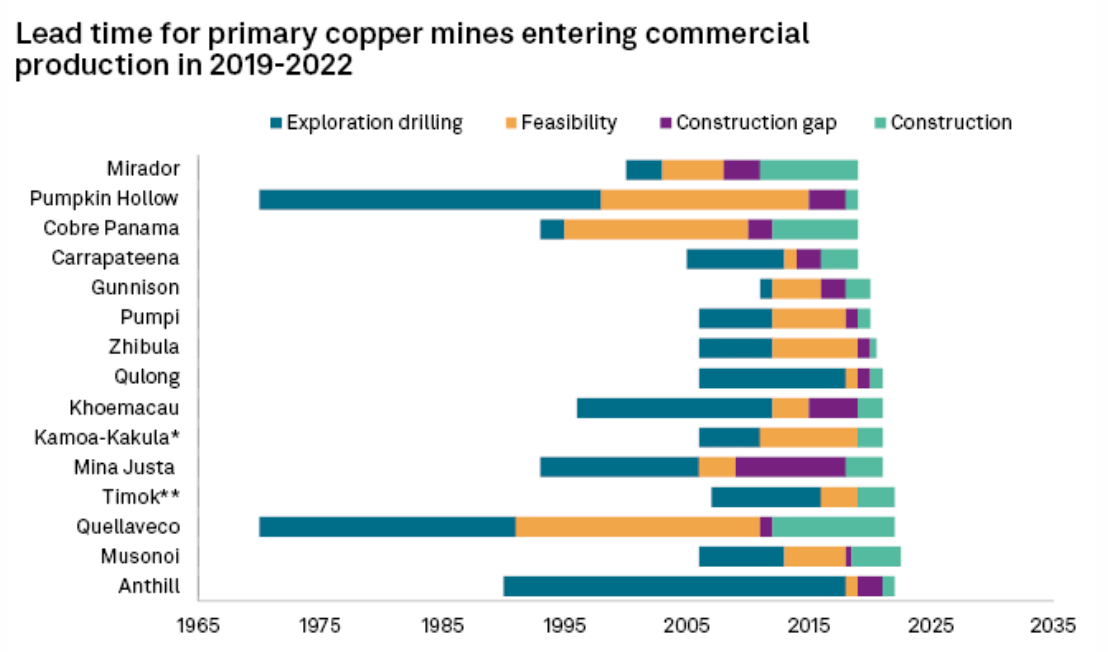

Energy transition advocates need to understand these realities. Moreover, just as with oil exploration, capital underinvestment can't be undone quickly; S&P's research emphasizes the long lead times (average of 23 years) that it has taken historically to move from discovery to production:

{kind=link}

The work on the Quellaveco mine, owned by Anglo American ( AAUKF ) started in the 1960s! By the way, this is another reason to focus on a mature company like BHP and avoid junior miners who may be years away from attaining production.

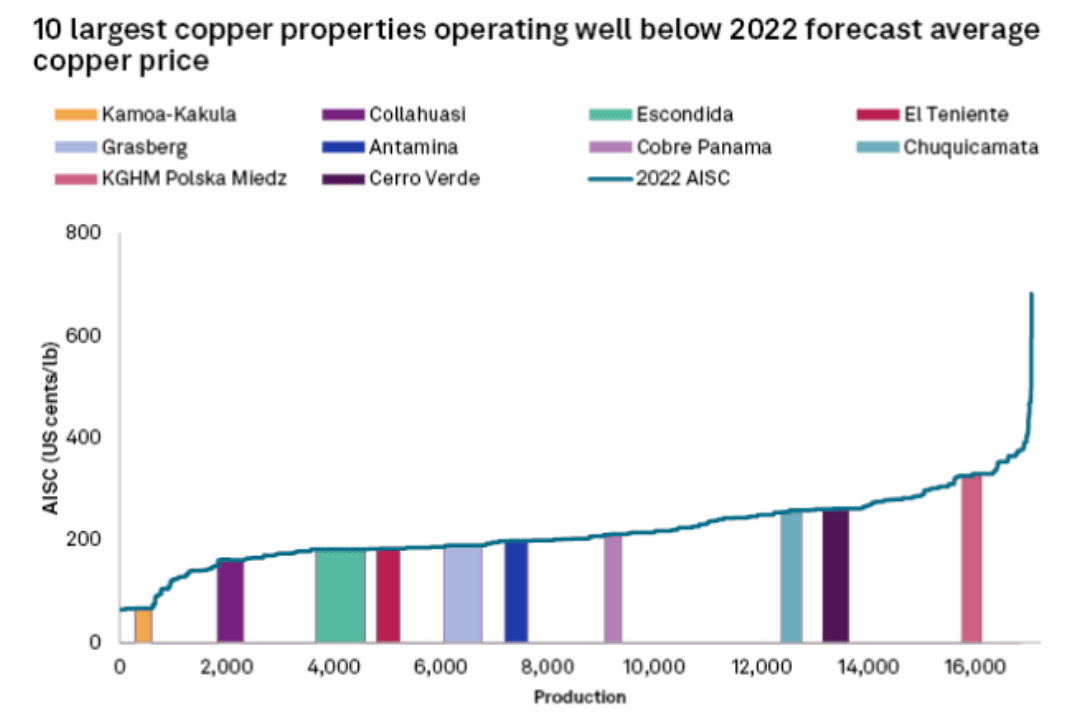

The costs of incremental supply have also been trending up; the all-in sustaining cost curve gets quite steep as you approach the 20 MT range:

{kind=link}

Note that to BHP's advantage, Escondida is one of the lowest cost assets out there.

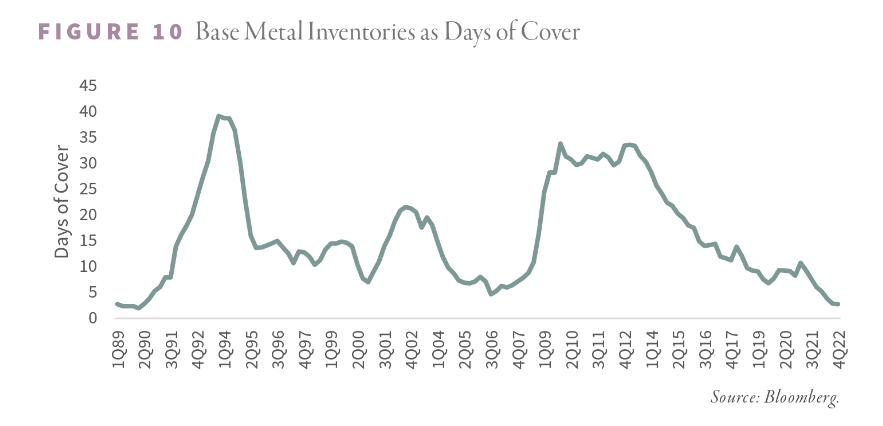

Finally, I wanted to mention a chart from the well-known G&R blog which suggests that inventories are also at multi-year lows:

{kind=link}

G&R bring in the ESG dimension as another limiting factor for the industry:

ESG pressures have placed substantial downward pressures on global mining industry capital expenditures in the last ten years. Environmental and related permitting issues have made both greenfield and brownfield mine development projects extremely difficult to bring into production. Given the vast ESG-related restrictions put on mining projects today, it is not uncommon that significant, economically robust discoveries made over 20 years ago are still not in production today.

Therein lies one of the ESG paradoxes too; even though de-carbonization is the number one ESG priority, the ESG hurdles sabotage the energy transition by cutting access to the metals and minerals that are needed to make it happen. However, just as in the fossil fuel world, this will hand the advantage to the owners of already developed assets.

Don't underestimate steel demand either

BHP produces iron ore and metallurgical coal, but the ultimate driver for both is steel. According to the World Steel Association :

Steel demand is forecast to grow by 1.7% in 2024 to reach 1,854.0 Mt. Manufacturing is expected to lead the recovery, but high interest rates will continue to weigh on steel demand. Next year, growth is expected to accelerate in most regions, but deceleration is expected in China.

Steel producer ArcelorMittal ( MT ) is quite bullish :

{kind=link}

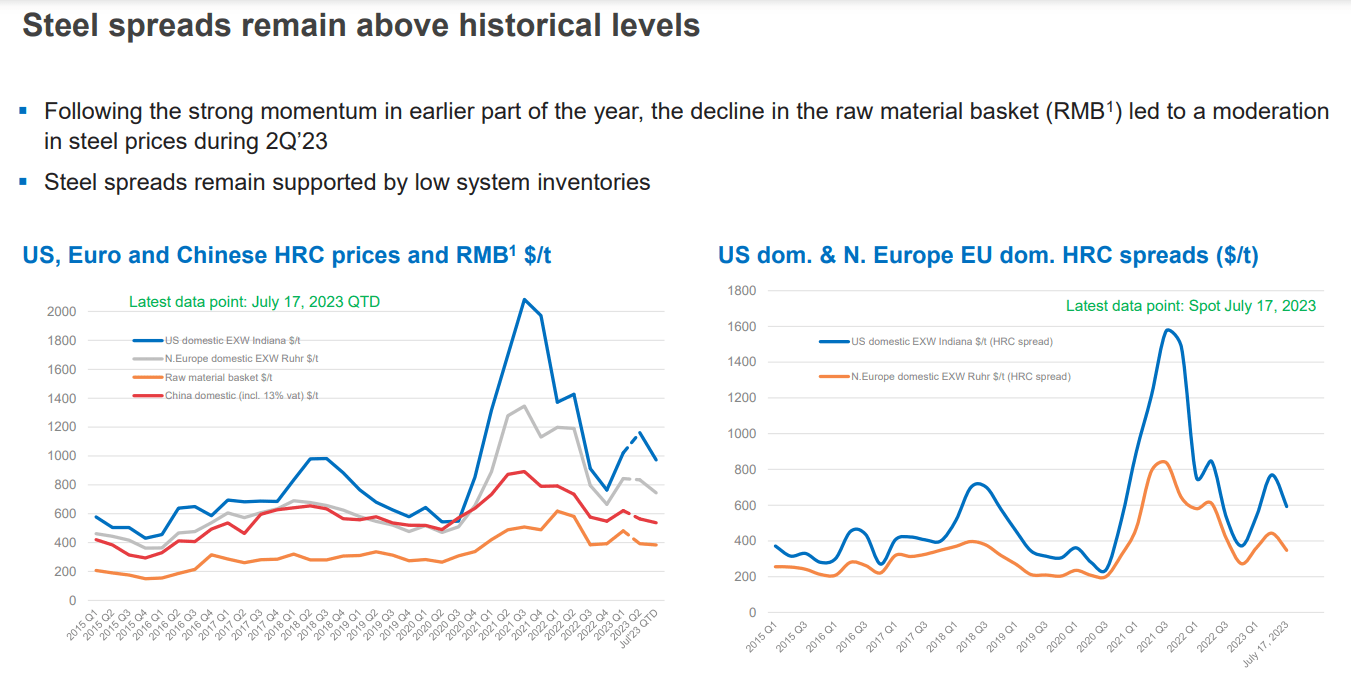

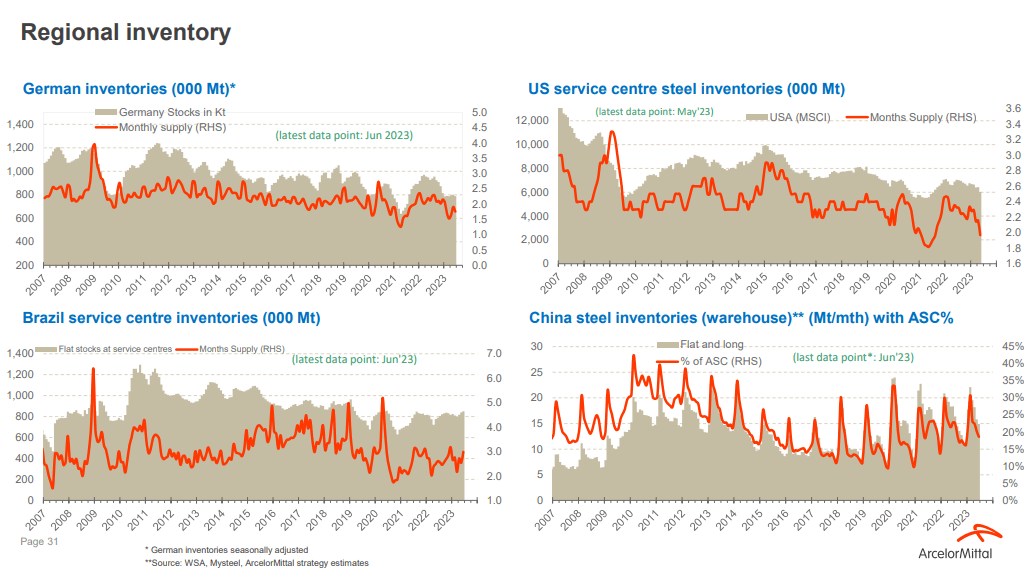

In particular, steel inventories are low:

{kind=link}

Just as with copper, much of the future steel demand will come from the energy transition :

{kind=link}

According to CleanTechnica (citing also an ArcelorMittal study):

Each new MW of solar power requires between 35 to 45 tons of steel, and each new MW of wind power requires 120 to 180 tons of steel.

This assessment is supported by Argus:

The steel industry will have a vital role to play in the coming acceleration of global offshore wind installations, with 4.5mn t of potential steel demand to be created from offshore auctions this year alone.

The Inflation Reduction Act in the U.S. is also expected to be big demand driver for steel:

{kind=link}

Nickel

Nickel is of smaller significance to BHP, but it's worth noting it's also one of the key enablers for the energy transition. The IEA study already discussed here expects 60-70% of nickel demand by 2040 to be driven by "clean energy."

BHP's cost advantages

Copper

According to the company:

We hold the world's largest copper mineral resources.

Escondida unit costs in FY2024 are expected to be between US$1.40 and US$1.70 per pound. Spence unit costs in FY2024 are expected to be between US$2.00 and US$2.30 per pound.

Given even in the midst of the Covid pandemic copper held above $2/lb, BHP's primary assets look well positioned.

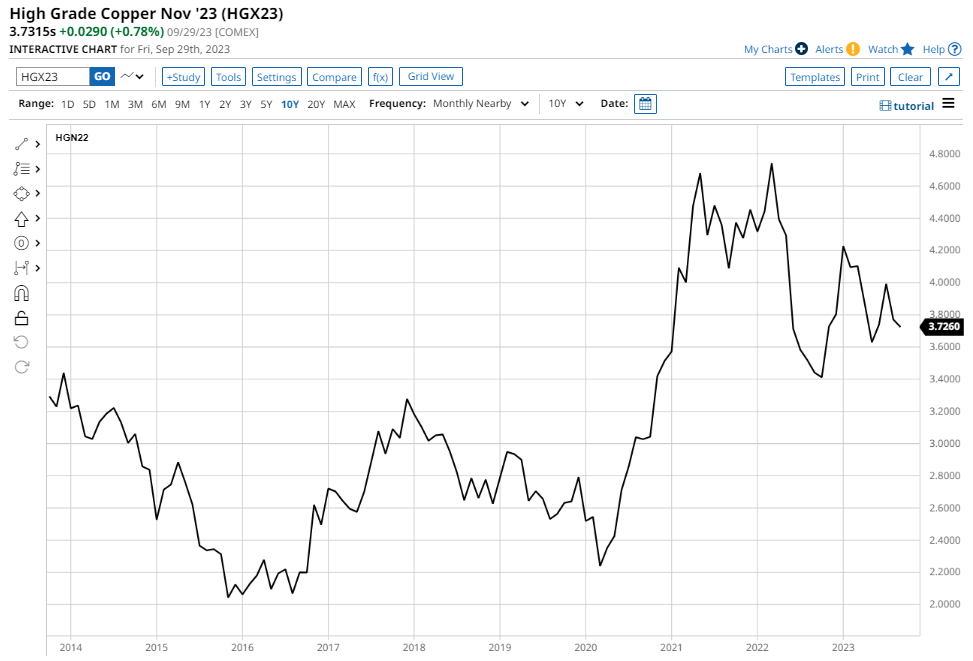

Copper is in contango, due to near-term demand weakness, but the prices remain quite high historically and are way above BHP's breakeven cost:

{kind=link}

Iron ore

According to BHP:

Western Australia Iron Ore (WAIO) is the lowest-cost major iron ore producer globally and has one of the lowest GHG emission production intensities of benchmarked seaborne iron ore operation.

The main concern over iron ore currently is China:

In the iron ore market, conditions were better in the second half of FY2023 than in the first half, but there are two key uncertainties for the coming six months. The first is how effectively China's stimulus policy is implemented, especially with regards to real estate. The second revolves around the breadth, timing and severity of any mandated steel production cuts. Our estimate of real-time cost support sits in the US$80-US$100/t range on a 62 per cent CFR (cost and freight) basis. In the medium term, China's demand for iron ore is expected to be lower than it is today as it moves beyond its crude steel production plateau and the scrap-to-steel ratio rises, though we expect demand for our products from elsewhere in developing Asia will offset this to a degree.

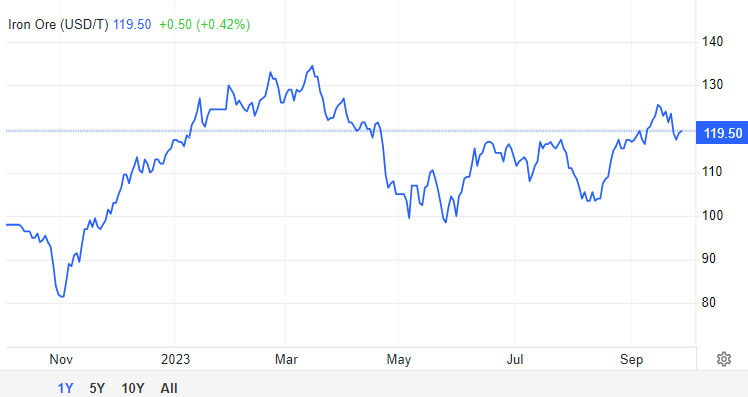

Even today with all the China negativity, iron prices remain above BHP's breakevens:

{kind=link}

Interestingly, JPMorgan ( JPM ) r aised its outlook for Rio Tinto based on improved iron ore outlook in 2024:

Iron ore prices look well supported as 2023 winds down, J.P. Morgan said Thursday, on the back of resilient Chinese steel production, port restocking, recent policy easing, and the bank's view that China steel cuts will be aggressively implemented.

JPM upgraded its medium- and long-run iron ore price forecasts, including a 13% boost in its 2024 projection to $110/metric ton, and tipped a likely consensus earnings upgrade cycle on the horizon for iron ore miners.

Narrative can drive the price, but the price itself is also a signal and it may suggest the worst for China is over:

Seeking Alpha

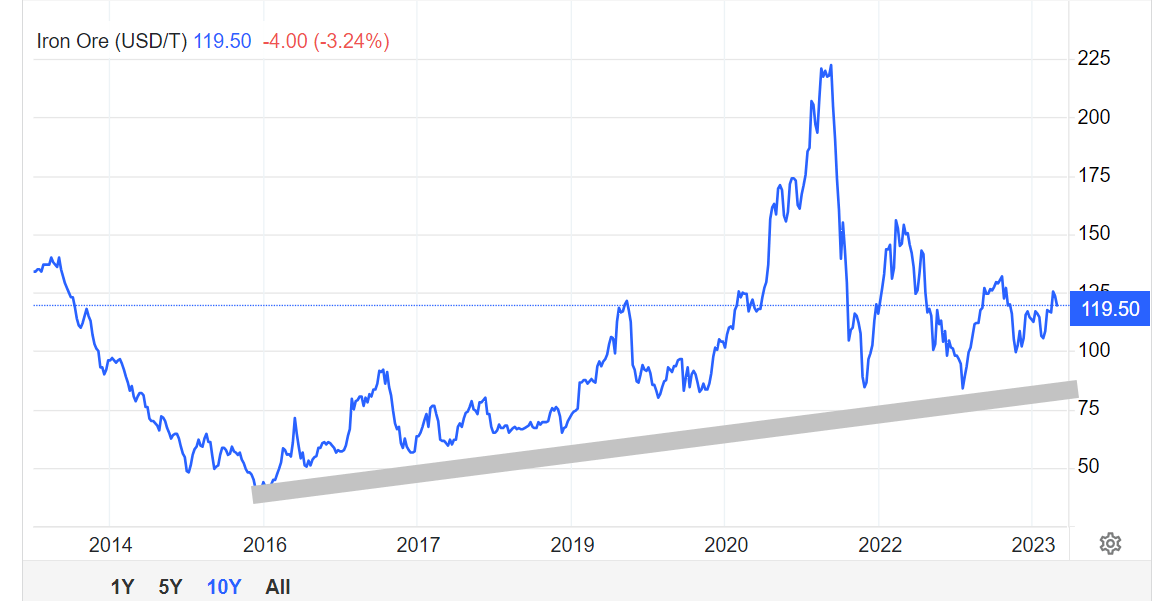

Iron ore prices have indeed come down a lot from 2021 but technically still look to be a in a multi-year bull market since 2016:

{kind=link}

Metallurgical coal

While short-term metallurgical coal is facing some headwinds, BHP is optimistic for the medium and long-term:

In the near term, we expect a modest improvement in seaborne demand from OECD importing regions as they see a gradual pickup in their steel industries, while India is expected to continue with its current momentum.

Over the longer term, we believe that higher quality metallurgical coals will continue to be required in blast furnace steel making for decades, driven by the growth of the steel industry in hard coking coal importing countries such as India. In particular, such higher quality hard coking coals are expected to be valued for their role in reducing the greenhouse gas emissions intensity of blast furnaces. And with the major seaborne supply region of Queensland having become less conducive to long-life capital investment as a result of changes to the royalty regime, the scarcity value of higher quality hard coking coals may well increase over time.

It is the familiar theme - the demand will stay high but regulatory issues are hindering investment. The major uncertainty in the short-term is, of course, China. Ironically, in the long run the energy transition may again drive a preference for the specific grade of coal mined by BHP.

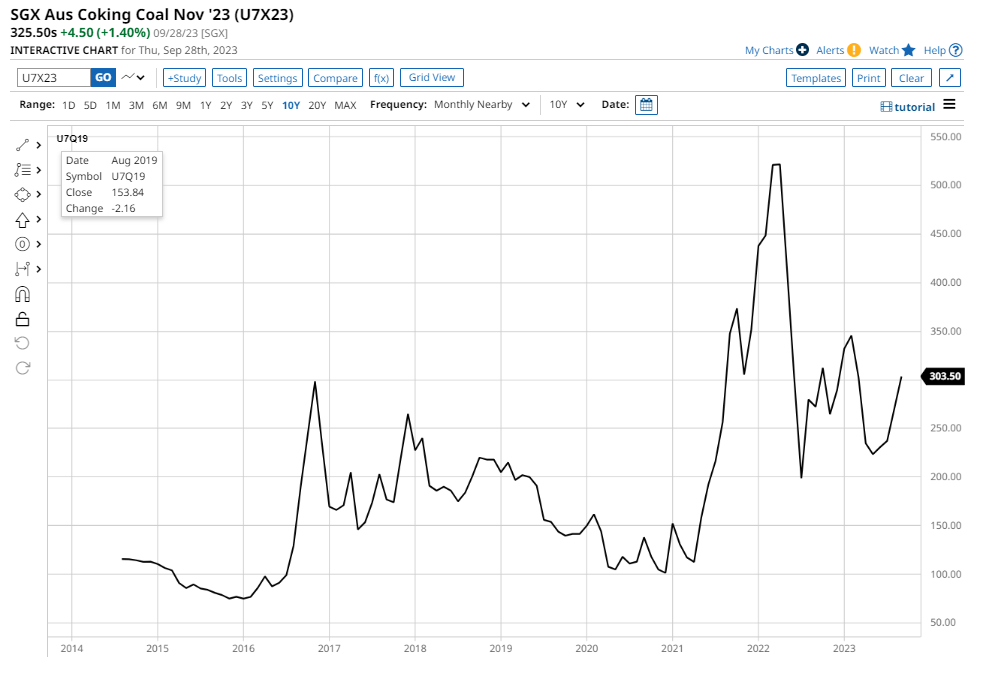

Australian coking coal is down from the 2022 peak but is doing pretty well compared to the pre-pandemic years:

{kind=link}

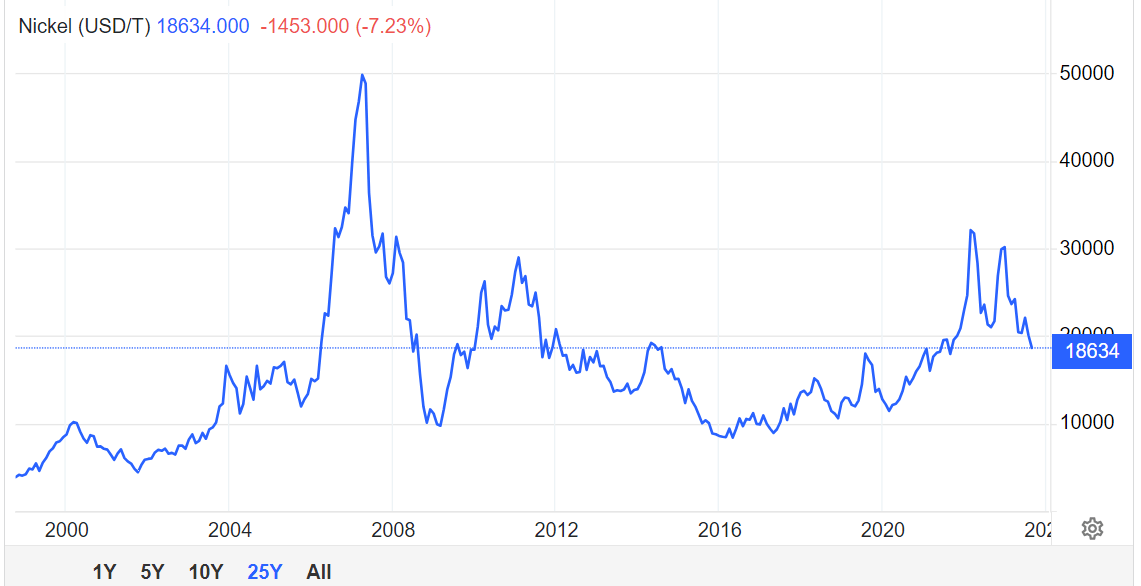

Nickel

While Nickel is less important to BHP as a revenue driver, BHP's nickel production is quite important for the energy transition. According to the company:

We hold the second-largest nickel sulfide resources globally and our nickel operations in Western Australia have one of the lowest GHG emission production intensities of benchmarked nickel mines and processing plants.

The challenges appear limited to the near-term:

The nickel industry moved into further surplus over the course of FY2023 as Indonesian supply continued to grow apace at a time of slowing economic growth. Battery demand is anticipated to record healthy growth across CY2023, but a de-stocking episode across the EV value chain early in the year made its presence felt across all the battery raw materials.

Nickel prices are down from the recent highs but still well above the 2016-2020 lows:

{kind=link}

Valuation

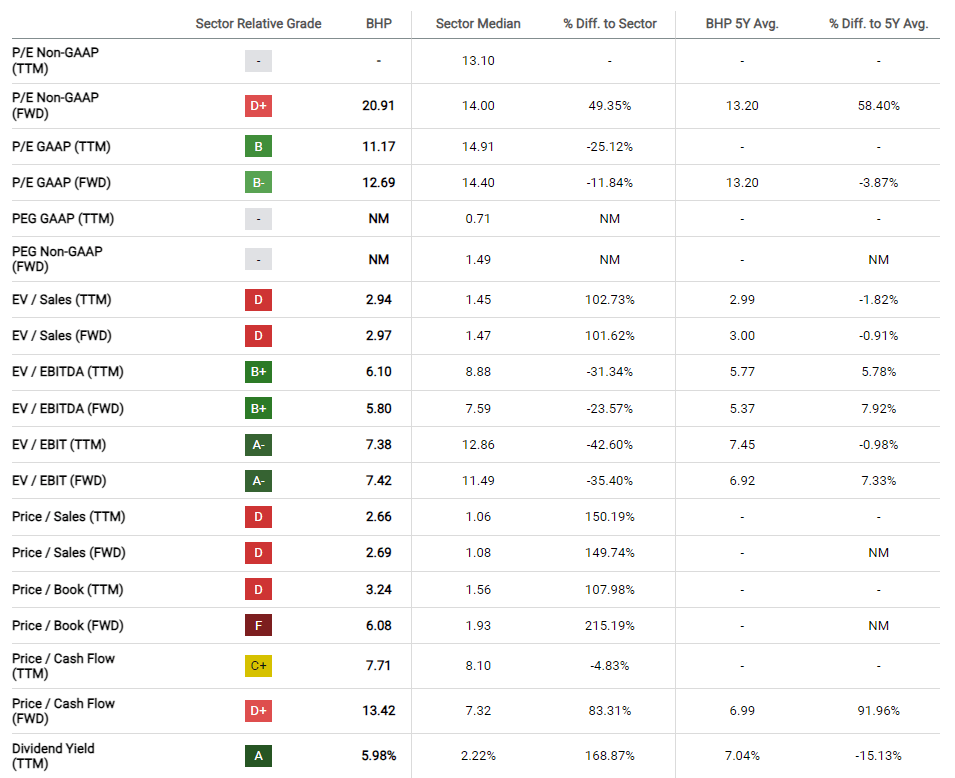

BHP is relatively undervalued compared to the broader sector, at least focusing on enterprise value multiples:

{kind=link}

The 5.8x EBITDA multiple is consistent with how the market has valued the company over the recent years:

To be clear, I don't necessarily expect the multiple to re-rate higher but rather see the gains coming from higher EBITDA in the future as energy transition demand drives up the prices for BHP's outputs.

Conveniently, BHP provides in its filings a sensitivity table that shows how EBITDA would change with changes in the prices of the underlying commodities:

{kind=link}

Starting off the forward EBITDA estimate of about $27 billion, I show the implications for the stock if copper prices and iron increase back to their recent highs (copper above $5/lb and iron ore about $150/t):

{kind=link}

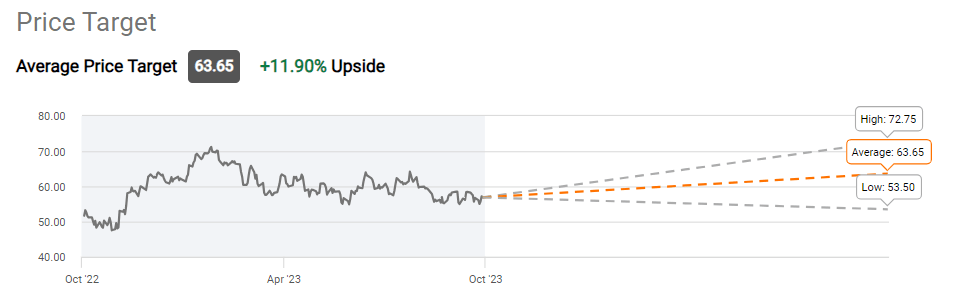

The upside can be quite significant and I think BHP has good prospects of trading around $80 (mid-point between the copper and iron ore scenarios) by the end of next year. This is about 40% upside and is more than what Wall Street projects:

{kind=link}

I am of course expecting that the underlying commodities will trade higher in a year compared to the futures curve.

Downside risks

China fears

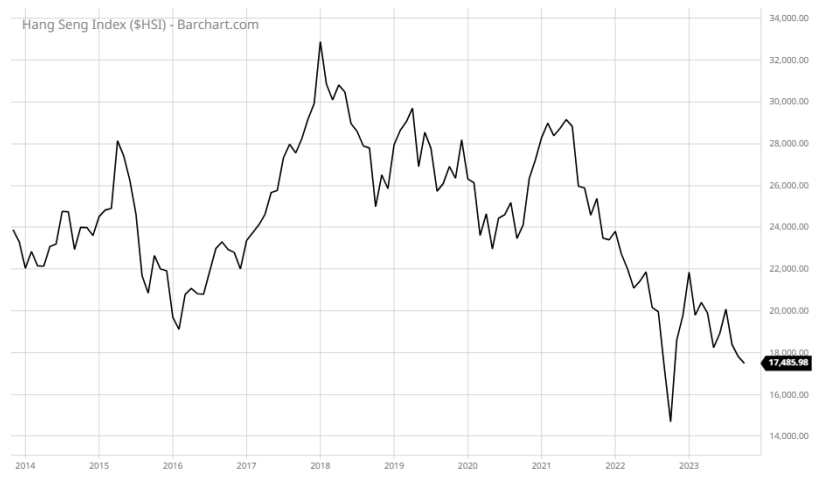

The main near-term risk ahead of copper and iron ore is China:

{kind=link}

The situation in China is obviously not good and the financial media coverage is as bad as it could be. However, at some point (I think sooner rather than later), the government in China will step up the stimulus measures and the economy will rebound. They simply don't have another choice, especially with the complicating geopolitics.

On the flipside, commodities seem to be waiting for the slightest signal from Beijing to rally. As reported by Seeking Alpha a couple of weeks ago :

Freeport McMoRan (NYSE: FCX ) +3% pre-market Thursday with copper prices rising after the Peoples Bank of China cut reserve requirements in an attempt to boost China's struggling economic recovery.

The PBOC lowered the reserve requirement ratio for most banks by 25 bps, the central bank's second such cut this year.

In my view, it is only a matter of time before we see further accommodative measures and copper and iron ore will react quickly.

Backtracking on the energy transition

Long-term the bigger risk is that governments in the West realize that the energy transition project is too expensive and backtrack on their de-carbonization pledges. However, as I am recommending BHP as a "hedge" within an energy-oriented portfolio, I am not really concerned about this possibility.

Getting paid to wait

Lastly, I want to highlight BHP's governance and dividend policy. Mark Twain infamously defined a mine as "a hole in the ground with a liar on top" and it is indeed of utmost importance that management's incentives are aligned to the shareholders. BHP has extensive corporate institutions to ensure transparency and the company is quite exemplary in terms of its public reporting, including voluntary reports that aren't mandated by regulators. As one of the largest companies in Australia that also maintains listings in the UK, US (through ADRs) and South Africa, BHP is watched by many pairs of eyes. This is likely true of other large mining groups too, so the distinction I really want to make is from junior miners who are more likely to have higher governance risks.

BHP also has a robust dividend policy that mandates a minimum of 50% of net profit has to be paid as dividends:

{kind=link}

Seeking Alpha reports the forward dividend yield as 5.62% which compares well to the peer sector:

Seeking Alpha

For BHP's 30 June 2022 year the yield was higher due to the special dividend which distributed the proceeds from the sale of the oil business. However, the regular yield of 5-6% is not bad either. It is consistent with what you can earn on T-Bills so even if BHP's stock doesn't take off, you are at least covering your opportunity cost.

Bottom line

While my portfolio emphasizes energy stocks (oil and gas), there is always the possibility that de-carbonization limits oil demand earlier than what energy bulls expect. However, for that to happen, there must be a massive call on the metals and mining sector to supply the resources needed for the energy transition. BHP, as one of the largest diversified miners with low-cost resources, offers a good "hedge" for the energy thesis. Moreover, even if you don't buy into the energy thesis, BHP could be a good inflation hedge and also pays a dividend that covers the time value of money.

For further details see:

BHP: Why Metals And Mining May Be The Best Hedge For Your Oil Stocks