AAIC - Big Dividend Yields Going Higher Dumb Debt And Snark

2023-09-28 17:45:07 ET

Summary

- Rising interest rates pose challenges for many REITs by impacting debt rollovers and investor alternatives.

- Higher rates will add around $2 billion to the national debt over the next decade. Even more if they create a recession.

- Apartment construction is declining, affecting rental unit supply and potentially leading to increased rental rates. Pretty obvious when you think about it.

- Preferred shares that are fixed-to-floating should see increasing prices as the floating date approaches, offering potential opportunities for investors.

Get ready for charts, images, and tables because they are better than words. Your continued feedback is greatly appreciated, so please leave a comment with suggestions.

Rates have been ripping higher, yet again. While small bumps don't hurt equity real estate investment trusts or REITs, the surging rates have been a huge headwind. I need to offer congratulations to everyone who predicted that Jerome Powell would jack up interest rates enough to add around $2 trillion to the national debt over the next decade. Since there is a perpetual deficit (anyone dumb enough to say a surplus is coming?), all interest expense is effectively financed by issuing new bonds. Like Einstein said: "Compound interest is no big deal. It's okay to let debt compound for decades. Nothing bad ever happens."

Disclosure: I might have that quote wrong. He said something about compound interest.

Well, congratulations anyway! You get the same reward as everyone else: more national debt.

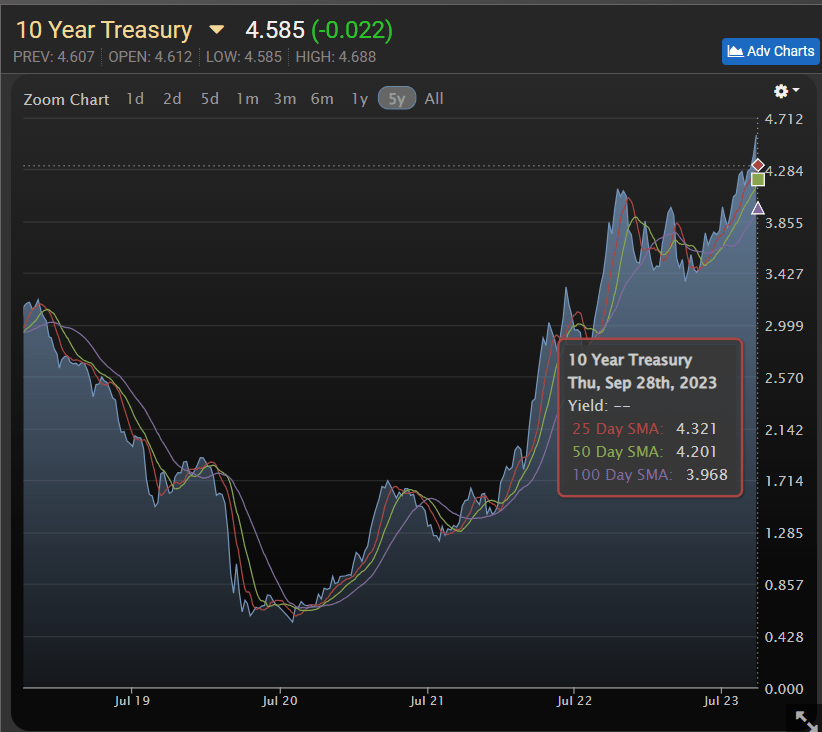

The market seems settled on raising rates:

{kind=link}

10-year Treasury rates (US10Y) are sitting more than 60 basis points above the trailing 100-day average. Great. Jacking up interest rates is supposed to kill off the companies that were not productive, right? That makes it a good thing?

Rates can be an issue for mortgage REITs ("mREITs") and equity REITs. For equity REITs, debt is eventually rolled over at higher rates and investors have more alternatives. When interest rates are high because of inflation, investors don't get an alternative. CPI smoothing through the housing index suppressed the actual rate of inflation. Consumer prices were actually rising at double-digit rates for a while. But you probably know that, because you've gone places and seen prices. A useful technique!

When actual prices were growing faster than 10% and Treasury rates were under 1.5%, investors didn't have a choice. Equity is a garbage hedge against inflation in the short term, but a great hedge in the long term. Real estate (such as that owned by equity REITs) can also serve as a good hedge over long periods.

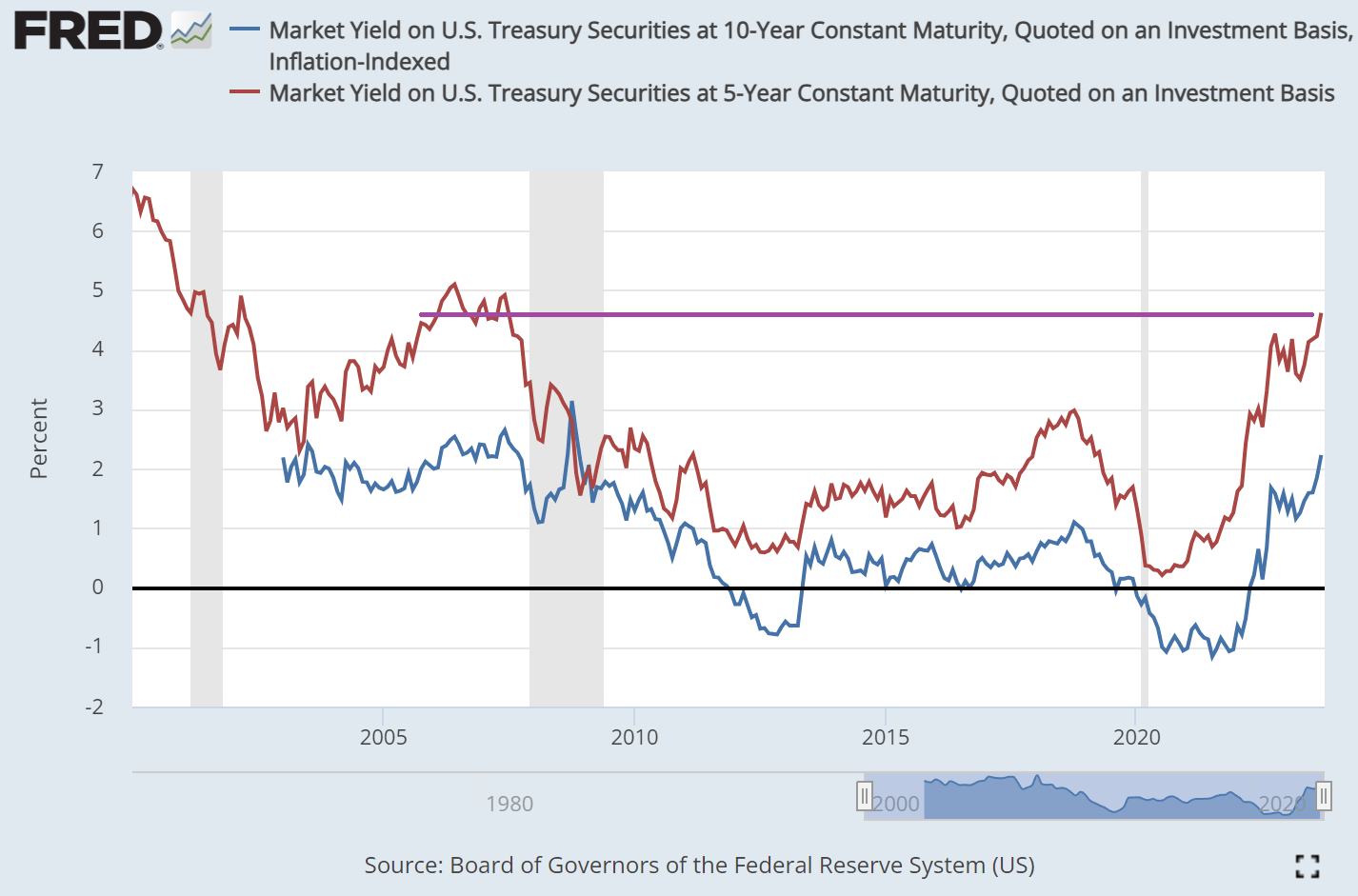

Those low rates pushed investors into equity markets. Today, Chairman Jerome Powell is ensuring they can get paid on Treasuries. We can use TIPS (Treasury Inflation-Protected Securities) to measure how much of the yield is coming from inflation expectations. If the TIPS yield is high, it means investors are being offered an unusually high real (inflation-adjusted) return in the bond market.

When was the last time the 5-year TIPS yield broke this level? See the chart:

{kind=link}

Cool, it was 2006 to 2007. We all remember nothing bad happened then, so that's great.

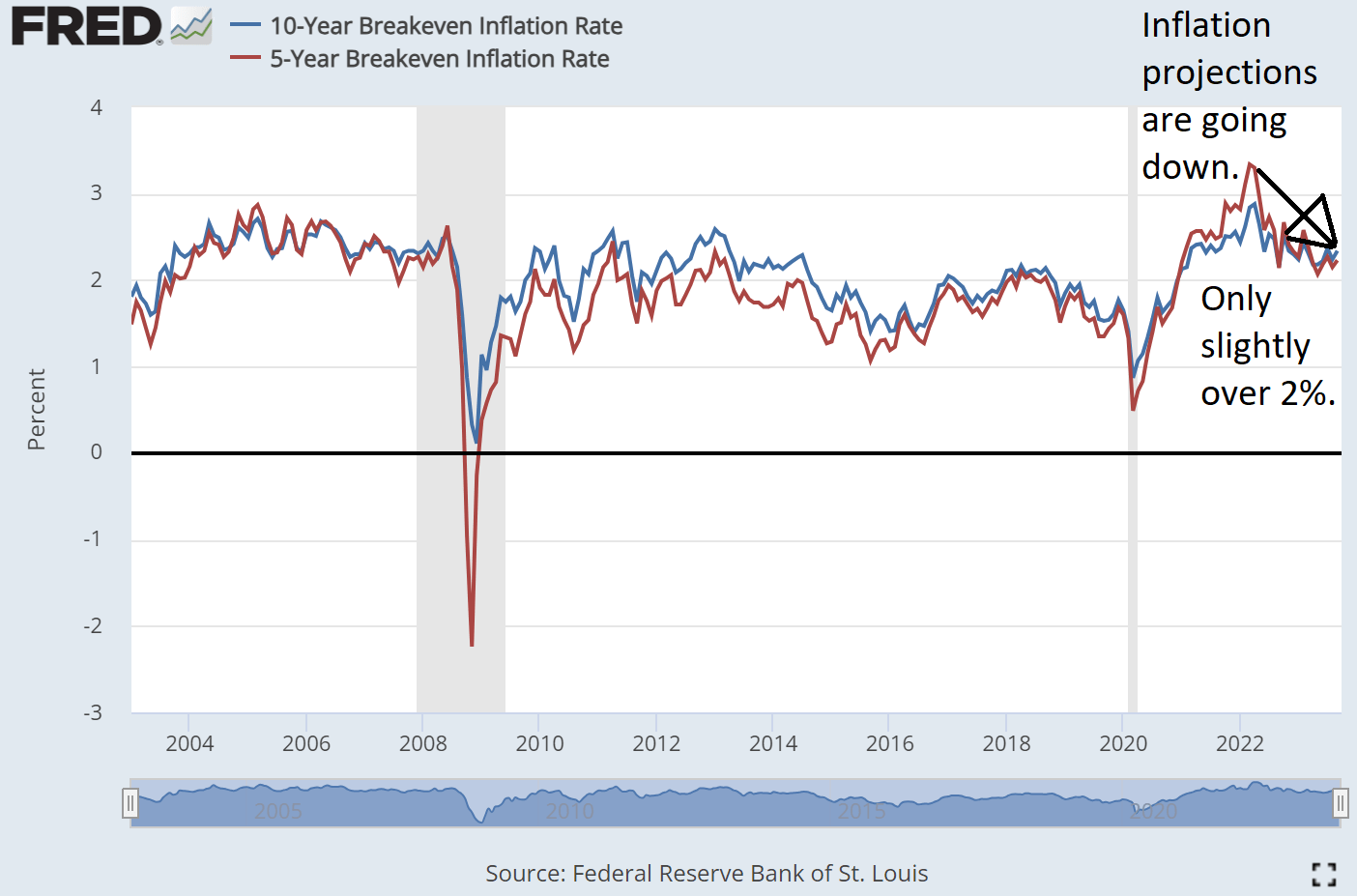

The Federal Reserve successfully convinced investors that they will keep elevated rates even if inflation subsides. Whether we get a recession or not, the Federal Reserve really wants to see interest expenses explode higher.

The market already concluded that inflation would probably be back to about 2%:

{kind=link}

This can be a particularly hard environment for most investors. When interest rates increase by 50 basis points in a year, it's no big deal. When they rip higher like this, it slams into valuations.

When Higher Rates Increase Inflation

Higher interest rates delay demand. That reduces inflation in the short term, which is what everyone focuses on. However, bigger deficits create inflation. The recent inflation was not caused by monetary policy (which means interest rates). They were low for over a decade without causing inflation. Fiscal policy changed as we shifted from big deficits to "multi-trillion" dollar deficits. Some investors still believe that this is some kind of multi-decade-lagged impact of lower rates. I'll never reach those investors. Most of you can probably see that inflation picked up promptly after pushing trillions of dollars into the economy.

Don't get me wrong. Interest rates have a lagged impact. But it isn't a multi-decade lag. Inflation didn't run under 2% for about 12 years, only to rip higher suddenly from the same low rates.

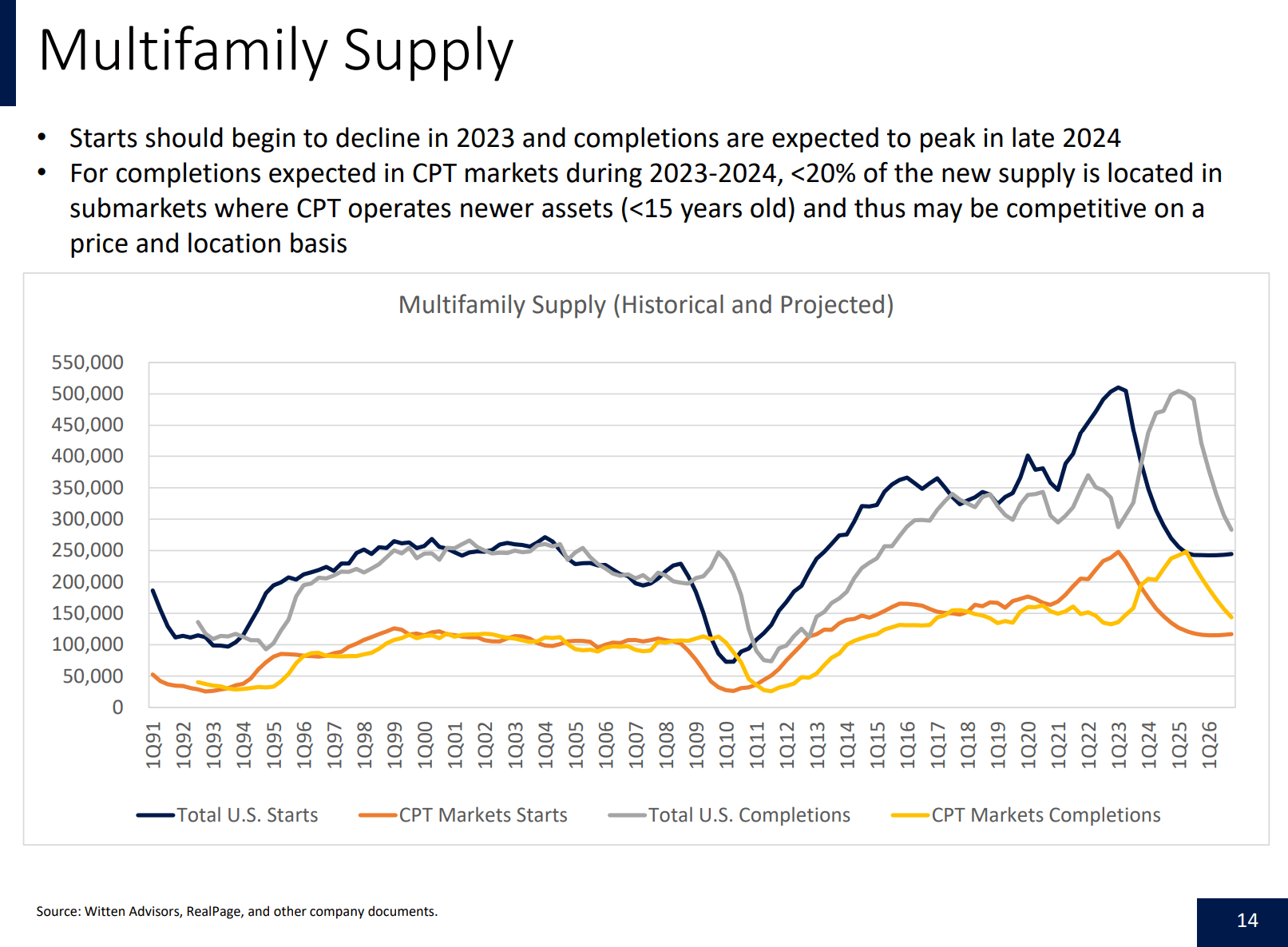

The issue now is that apartment construction is plunging.

{kind=link}

Why does this matter so much?

Let's be real. Most of Gen Z isn't going to be buying homes. Oops, did I hurt some feelings? Sometimes, reality hurts.

What I want you to see is the navy line and grey lines. That's a huge drop. Bad. Starts are projected to fall from over 500,000 to 250,000.

Do you know what impacts apartment rents?

It's supply and demand. That was a really obvious answer.

So, how can a country get more affordable rental units? There are two steps:

- Cheap financing, which involves low rates.

- Knock out restrictions on creating supply.

It's like rent control, except it works. Developers clearly responded to rates as it drove a surge in production and a subsequent plunge.

What do I say to the guy who assumes that building more apartments will just result in millions of new renters showing up to pay the exact same price? Nothing. That's dumb. Listen to conference calls and investor presentations. The big factor that puts pressure on rental rates is local supply levels.

Bold Predictions

The mortgage REIT book values are going to be down. It will be either "all" or "almost all" of the mortgage REITs listed here. On the other hand, business development company ("BDC") book values will be much closer to flat on average. There will probably be one or two outliers, but most will be pretty flat.

The worst losses are probably going to be in the high single-digit percentages or low double-digit percentages. Buyer beware when using the trailing BV figures (which are included below). Our strategy for trading in the mortgage REIT and BDC space relies on having frequent updates. We update estimates most weekends. Most Mondays, we go into the market with new information. For reference, there are still some reports on Wall Street where an analyst has one update for the quarter. What's better? 1 update or 12 updates? When rates are moving this fast, it matters.

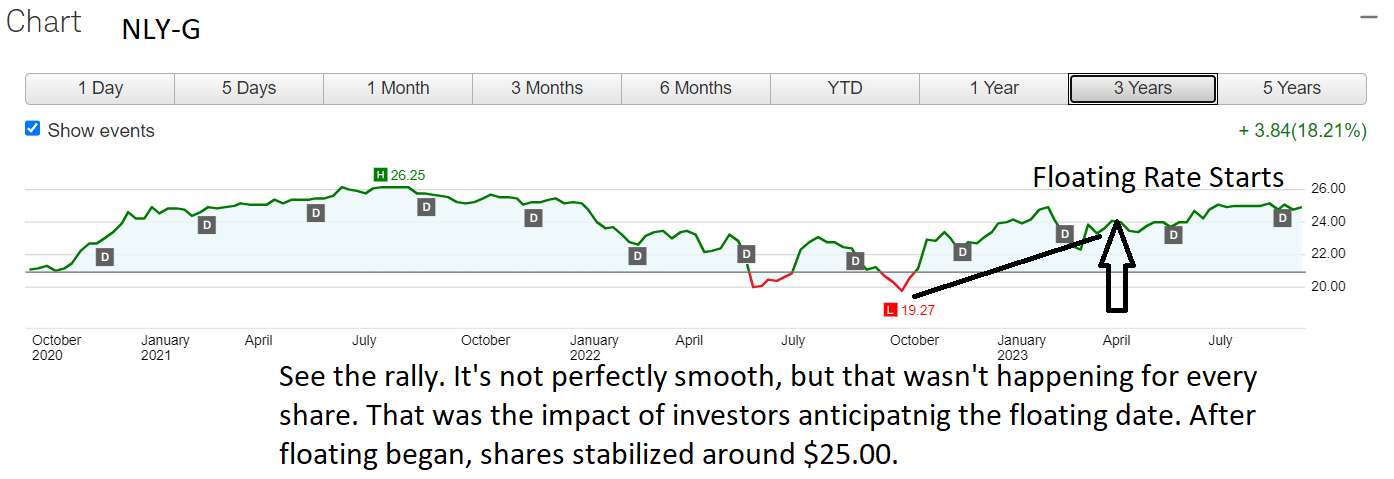

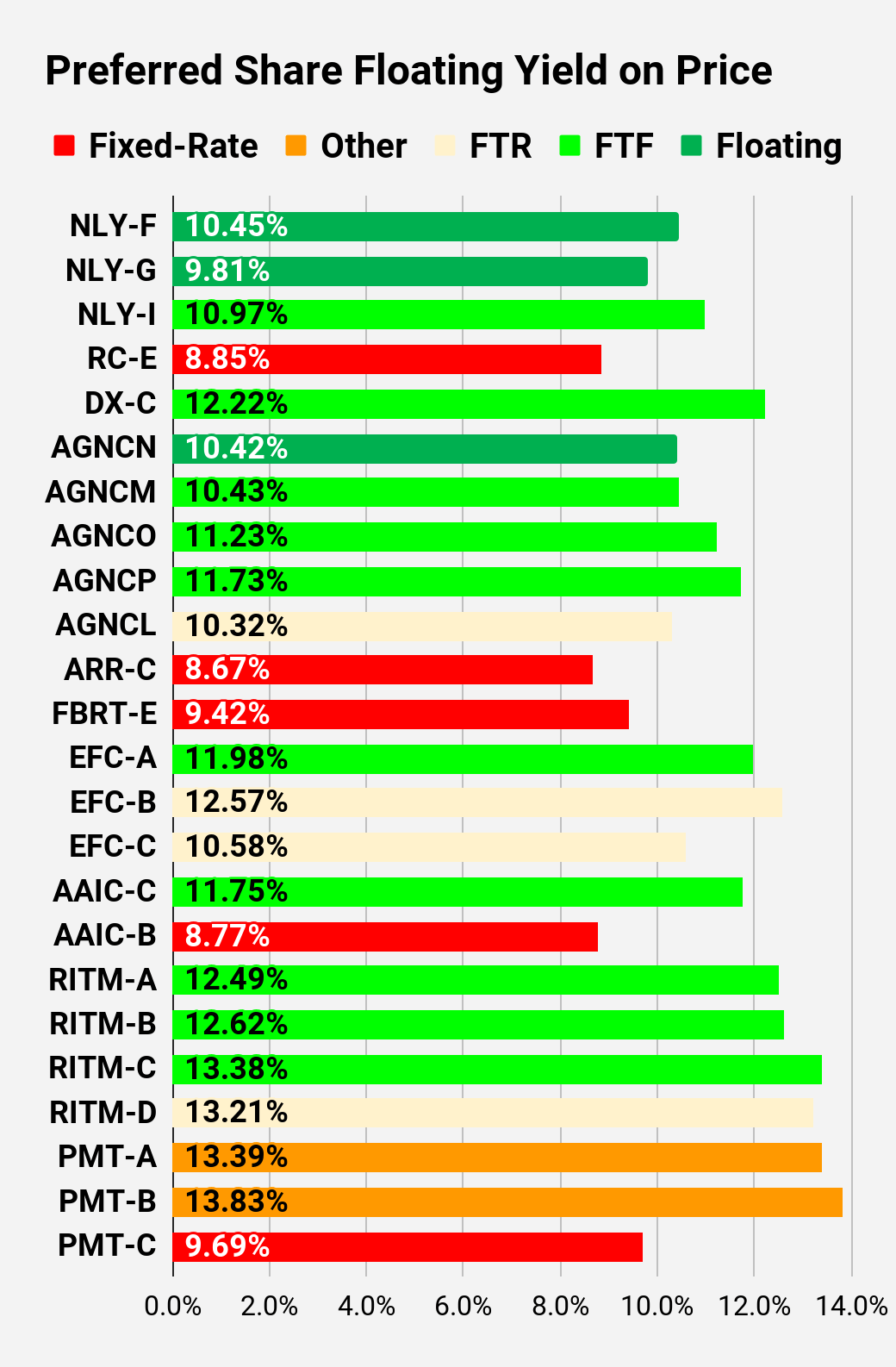

I've got another bold prediction, though. Absent a major recession or a plunge in interest rates (which would probably require a recession), preferred shares that are "fixed-to-floating" will have a tendency to climb toward call value as the floating date approaches. There are currently 3 mortgage REIT preferred shares that are floating: NLY-F, NLY-G, and AGNCN.

Their share prices are $25.34, $24.73, and $25.59, respectively. That puts their floating yields in the range of 9.9% to 10.5%. Some of the mortgage REIT preferred shares involve more risk. However, many of them have bigger floating spreads. Personally, I will gravitate more toward the lower-risk shares. However, I am venturing into a few of the higher-risk shares where upcoming floating dates imply dramatic upside. If shares rally toward $25.00, then the yield to call becomes a more useful metric even if calls don't actually occur. Of course, this only applies to shares that will have a floating rate.

Investors tend to like double-digit yields. Some of these shares hit the floating date and will see dividend rates jump 25% to 50%. As the floating date approaches, we've seen prices go higher:

{kind=link}

Of course, that's only one example. Yes, there are others. No, they don't fit in this article. I already wrote the sections below and the piece is getting too long. If you think I'm wrong, just look at the stability in the share prices for NLY-F and AGNCN over the last 2 years. They were the first ones to float.

Floating Rate Announced

If you missed the announcement, you should know that CIM announced CIM-B will float using SOFR plus the tenor spread adjustment. I plan to provide a bigger update on that publicly. The announcement came only a few business days after we encouraged Seeking Alpha readers to consider contacting CIM about the situation. Particularly appealing was CIM's confirmation in the filing that this would happen automatically under the law. CIM's prospectus for CIM-B has nearly identical language to PMT's prospectus for PMT-A and PMT-B.

Reading the waterfall intelligently results in a waterfall that doesn't function. The fixed-rate dividend wasn't a viable long-term fallback because the qualification was "no such dividend period" exists, rather than "no such rate exists." CIM was explicit about their shares falling under the LIBOR Act and automatically switching to SOFR (Secured Overnight Financing Rate) + the spread adjustment (about 26 basis points). It was an exceptional rebuke to a less ethical peer.

I want to repeat that with different wording for anyone who missed it. CIM did not say: "We're choosing to use SOFR." They said it would happen automatically under the law. The only options they had were to accept SOFR + the spread adjustment or break the law. No other option. Hey PMT, why are you looking so shifty over there?

I'll probably have a public article on it next week. For this week, I really wanted to:

- Get the bigger article with the updated charts out.

- Complain about trillions in additional debt for minimal benefits.

- Highlight that there are some great opportunities with shares that start floating in 18 months or less.

I'm excited to keep hunting in the preferred share space. Several of these shares already yield over 8% and will jump into double-digit yields when the floating rate kicks in (unless the Federal Reserve slashes rates).

Stock Table

We will close out the rest of the article with the tables and charts we provide for readers to help them track the sector for both common shares and preferred shares.

We're including a quick table for the common shares that will be shown in our tables:

| Type of REIT or BDC |

| Residential Agency |

| Residential Hybrid |

| Residential Originator and Servicer |

| Commercial |

| BDC |

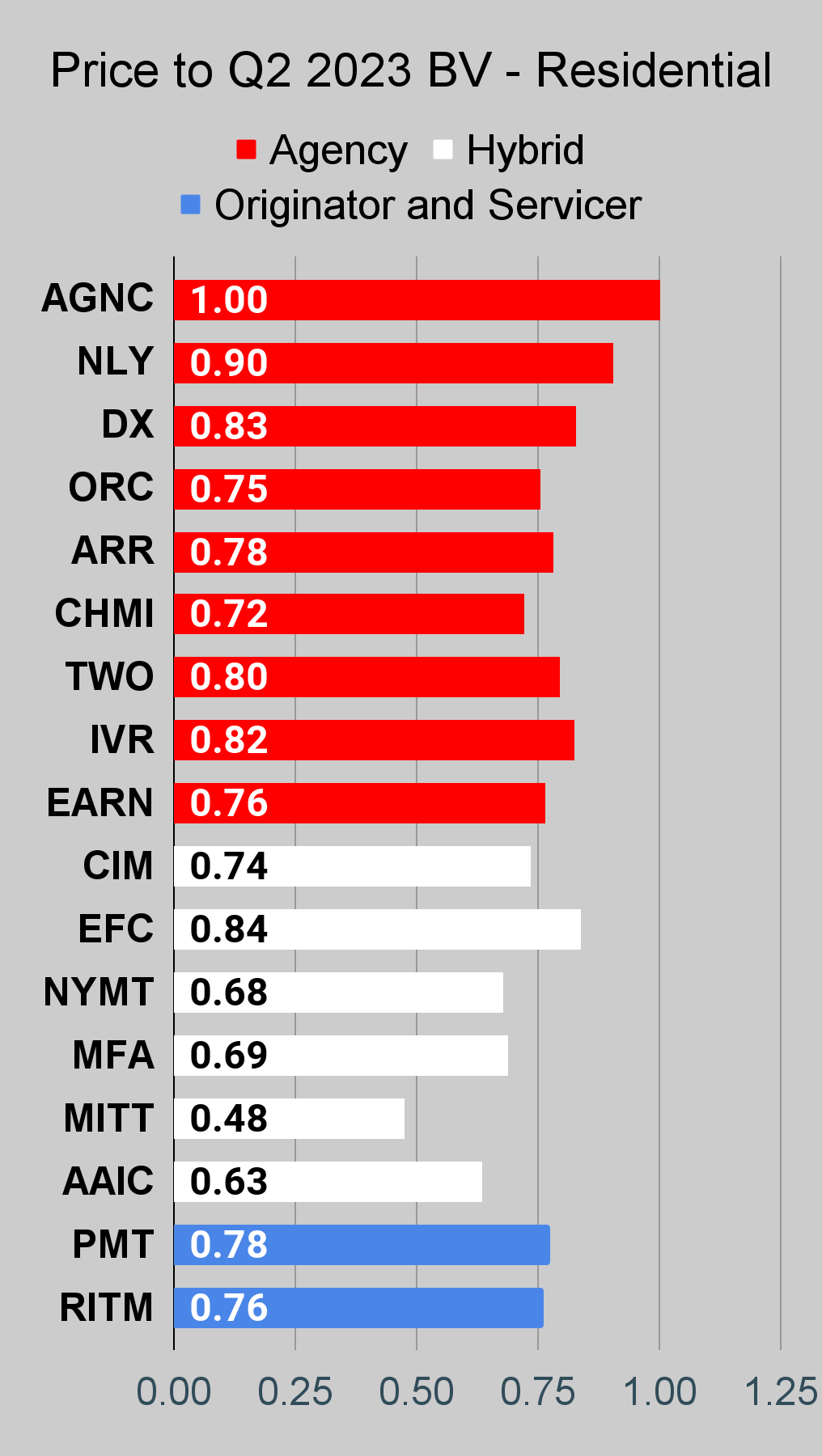

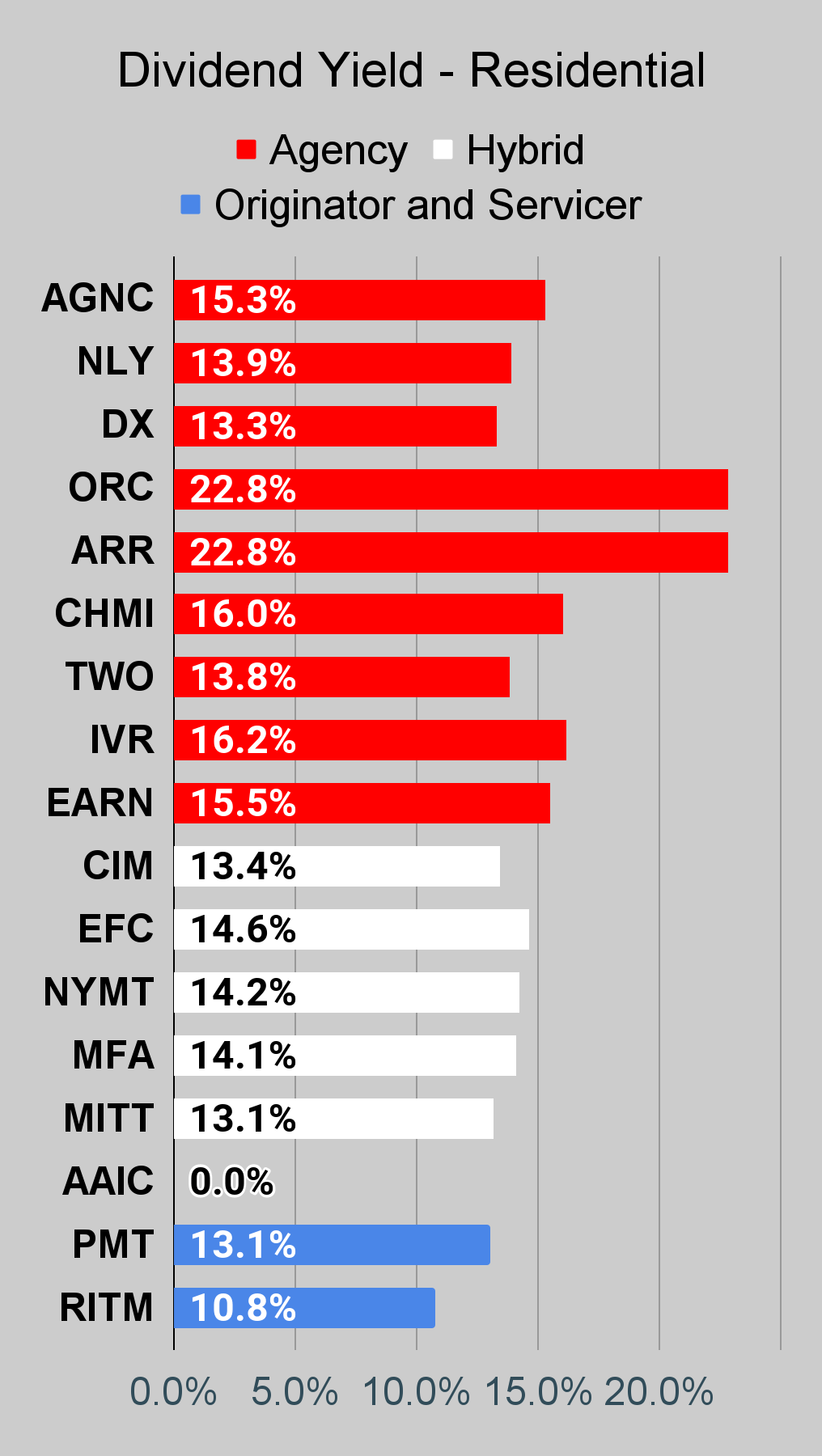

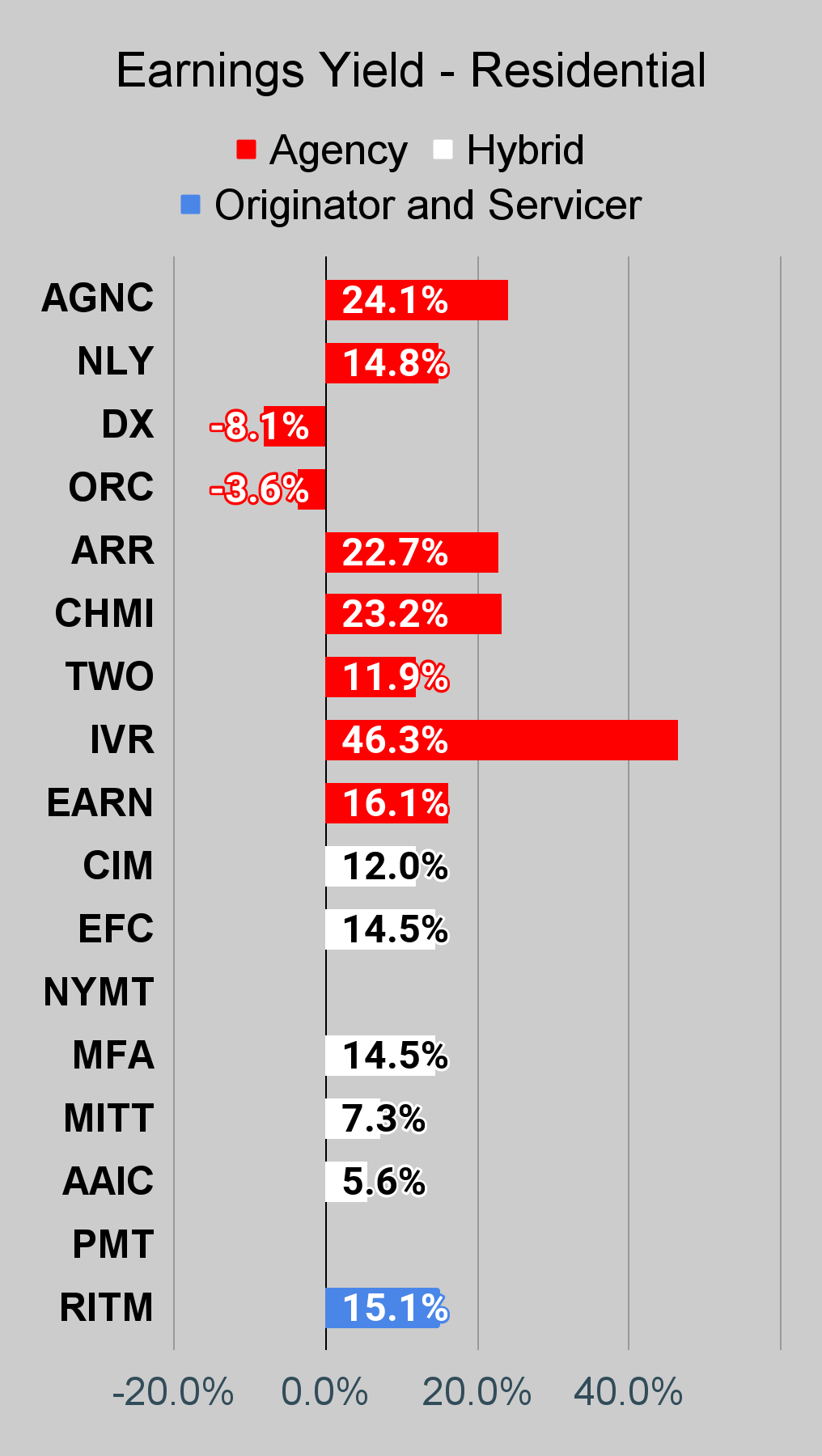

If you're looking for a stock and I haven't mentioned it yet, you'll still find it in the charts below. The charts contain comparisons based on price-to-book value, dividend yields, and earnings yield. You won't find these tables anywhere else.

For mortgage REITs, please look at the charts for AGNC, NLY, DX, ORC, ARR, CHMI, TWO, IVR, EARN, CIM, EFC, NYMT, MFA, MITT, AAIC, PMT, RITM, BXMT, GPMT, WMC, and RC.

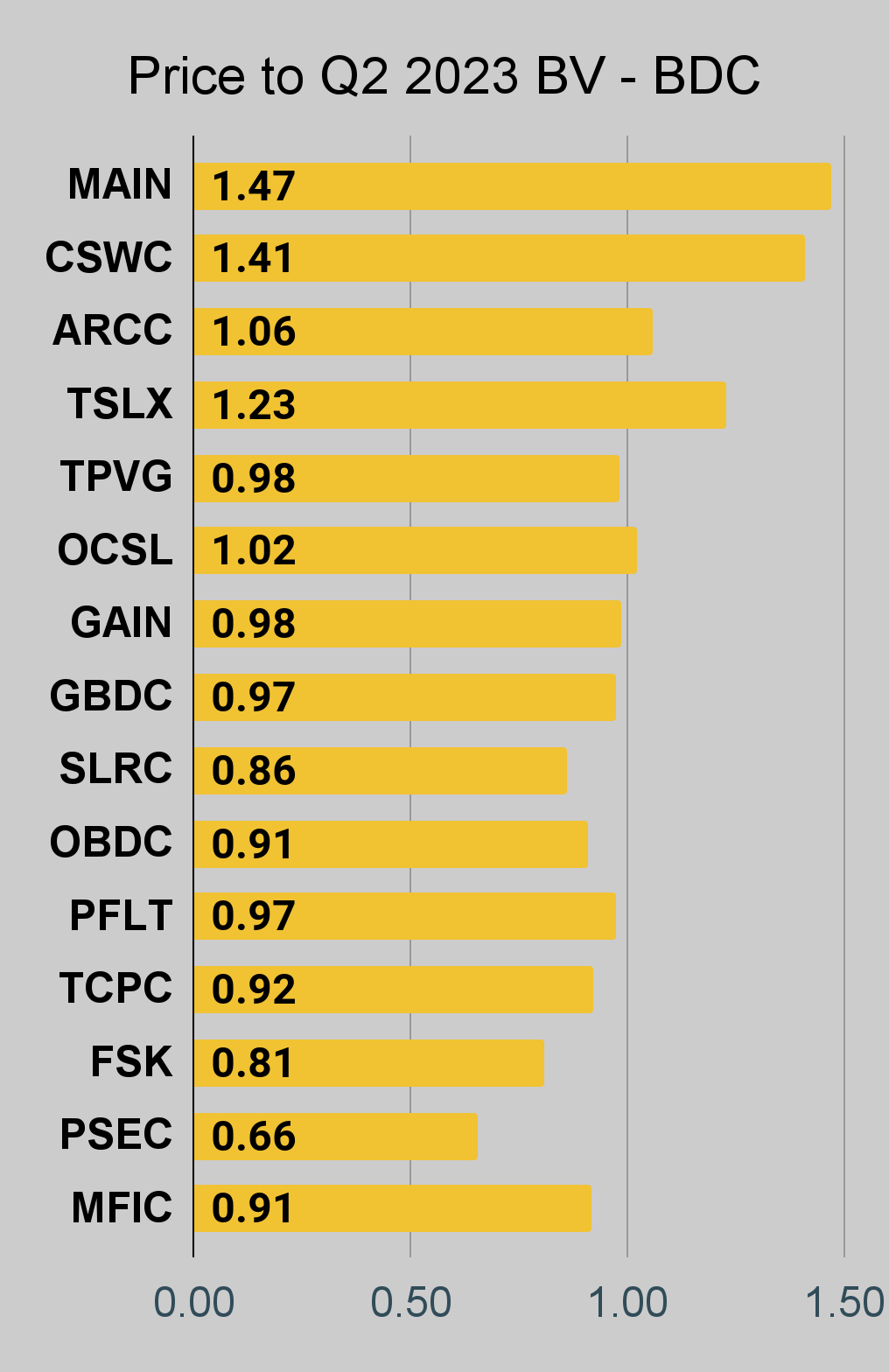

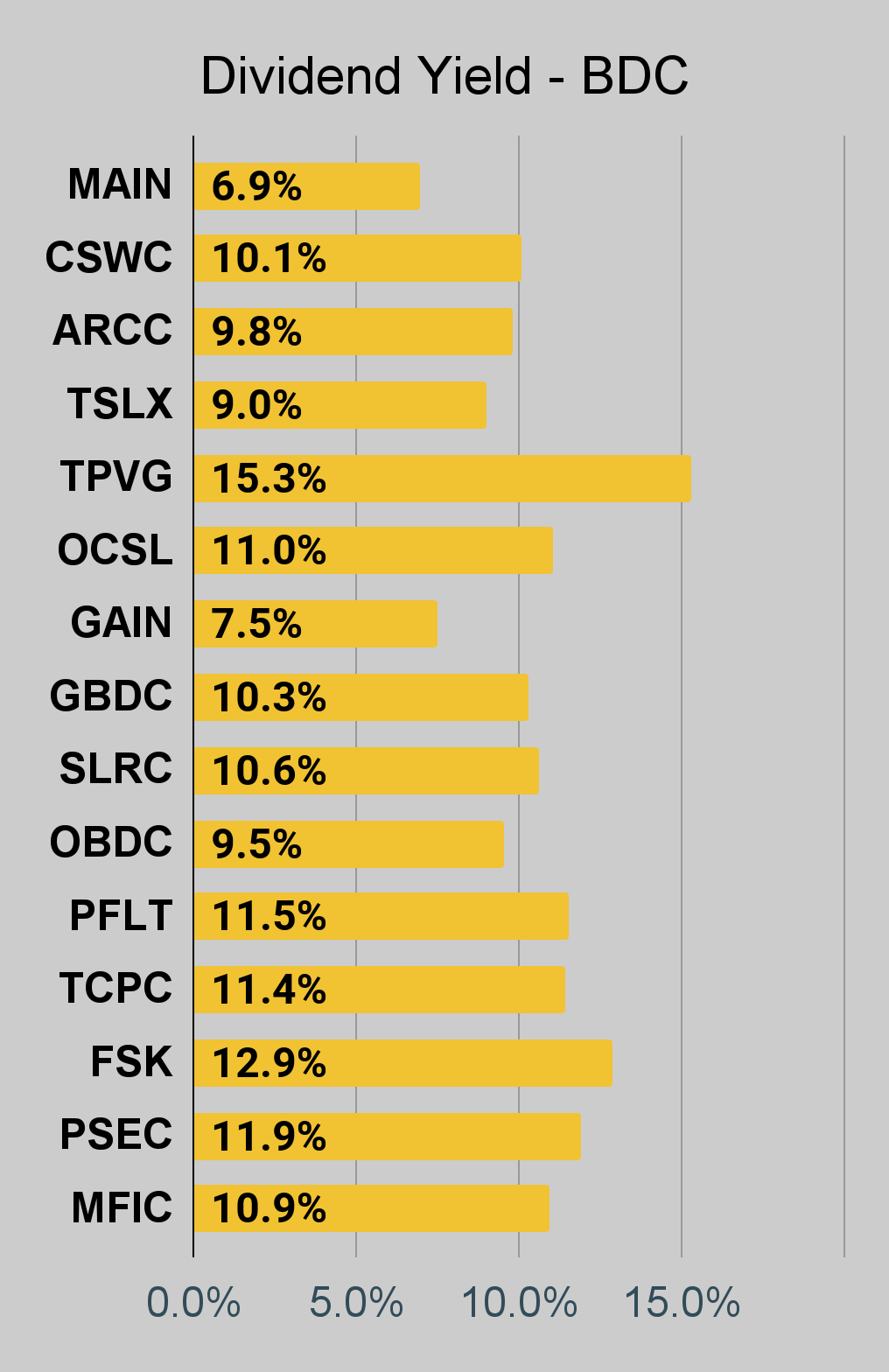

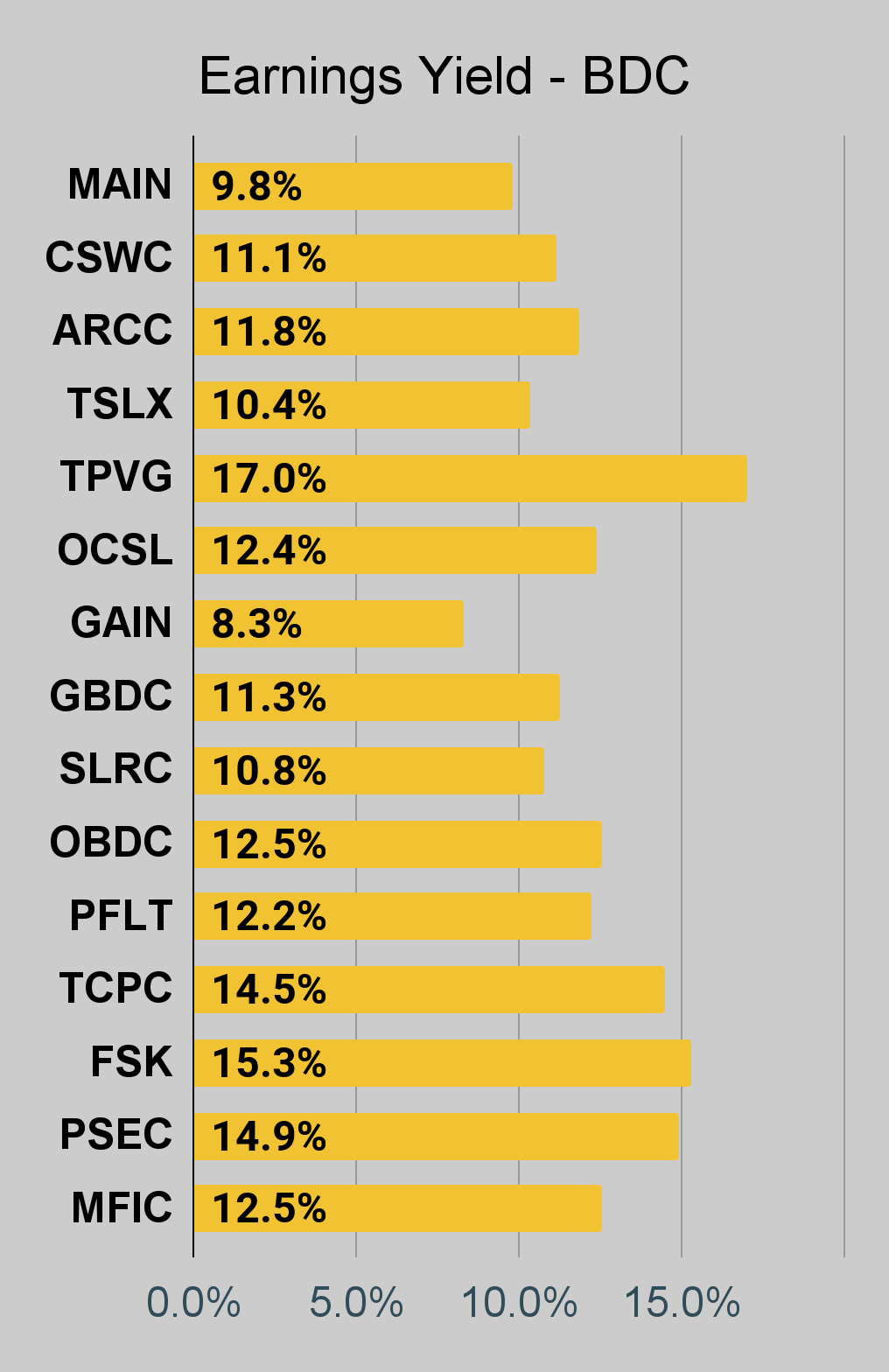

For BDCs, please look at the charts for MAIN, CSWC, ARCC, TSLX, TPVG, OCSL, GAIN, GBDC, SLRC, OBDC, PFLT, TCPC, FSK, PSEC, and MFIC.

This series is the easiest place to find charts providing up-to-date comparisons across the sector.

Residential Mortgage REIT Charts

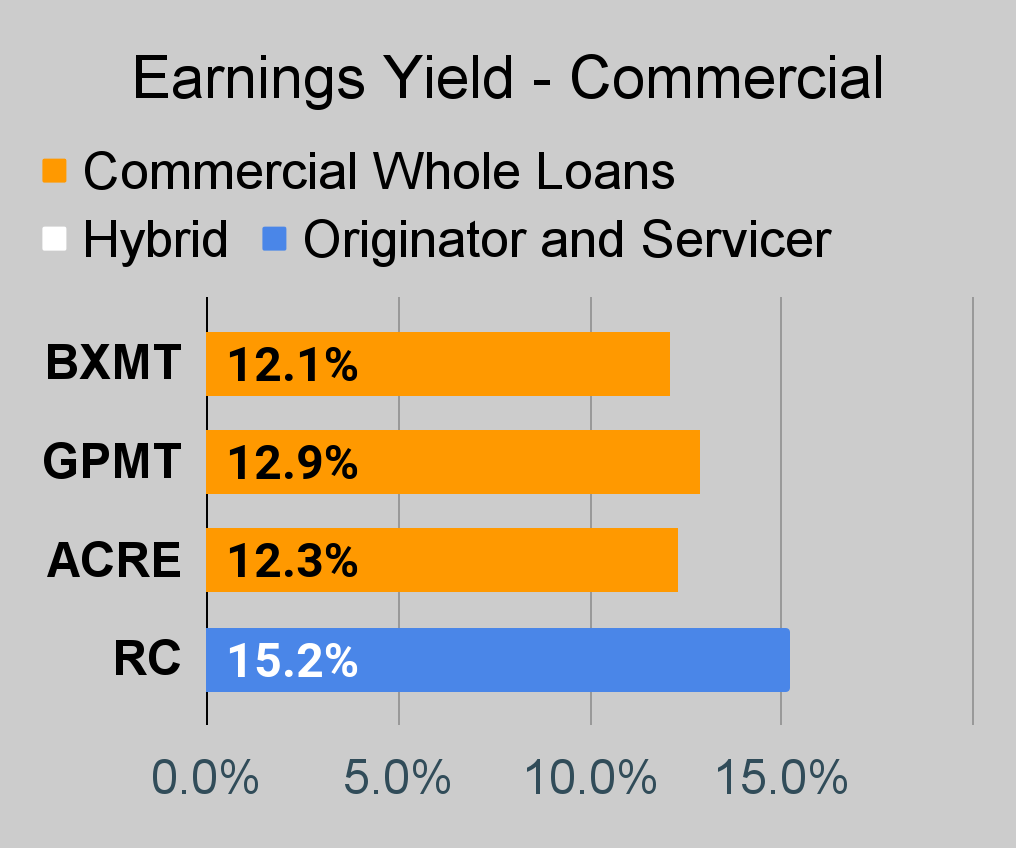

Note: The chart for our public articles uses the book value per share from the latest earnings release. Current estimated book value per share is used in reaching our targets and trading decisions. It is available in our service, but those estimates are not included in the charts below. PMT and NYMT are not showing an earnings yield metric as neither REIT provides a quarterly "Core EPS" metric. Presently, a few other REITs also have no consensus estimate.

Second Note: Due to the way historical amortized cost and hedging is factored into the earnings metrics, it is possible for two mortgage REITs with similar portfolios to post materially different metrics for earnings. I would be very cautious about putting much emphasis on the consensus analyst estimate (which is used to determine the earnings yield). In particular, throughout late 2022 the earnings metric became less comparable for many REITs.

{kind=link}

{kind=link}

{kind=link}

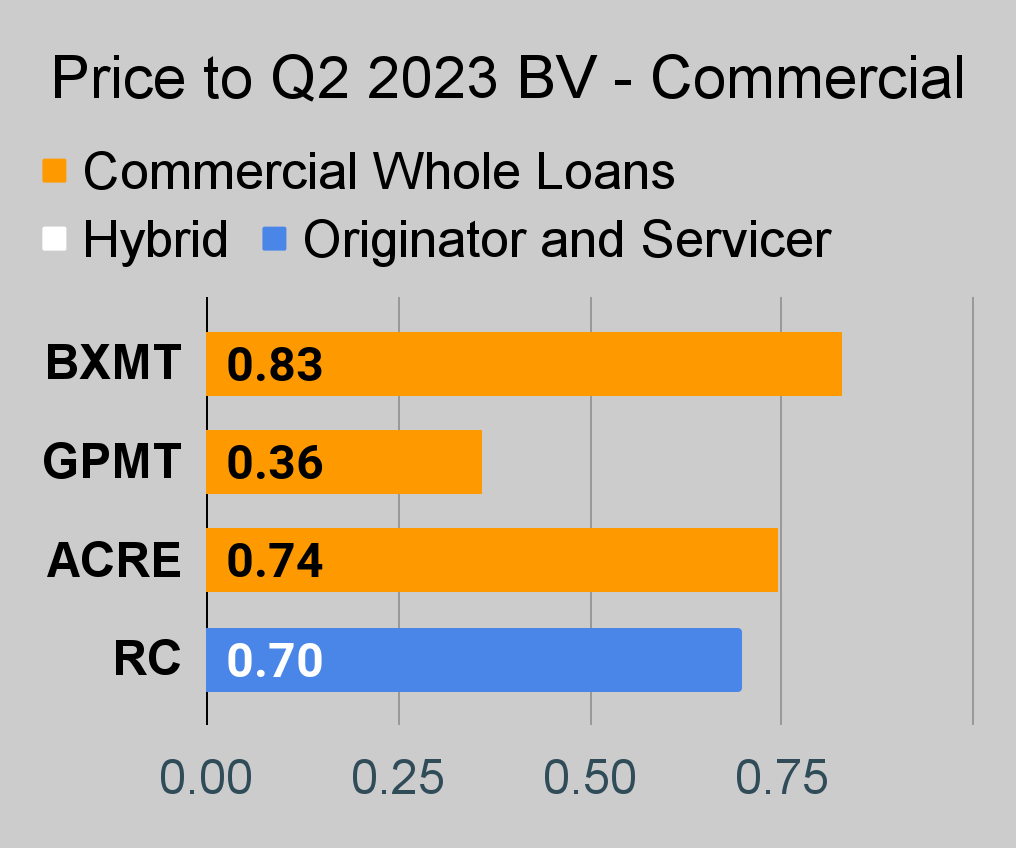

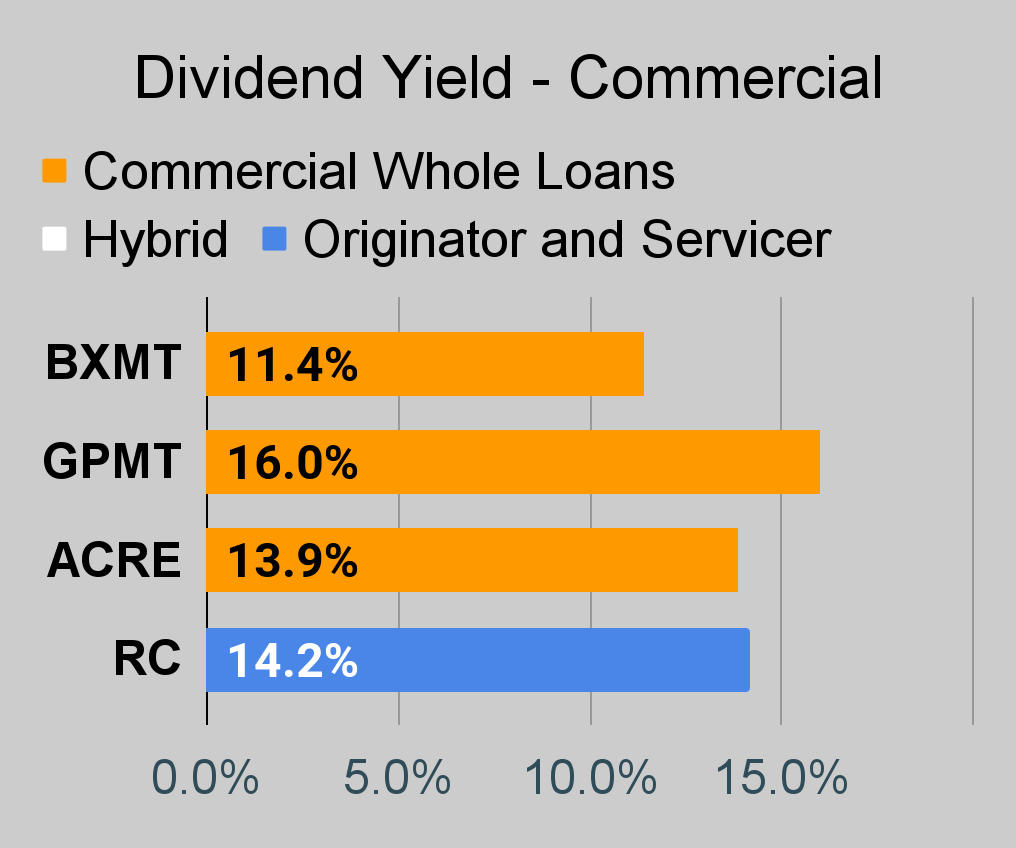

Commercial Mortgage REIT Charts

{kind=link}

{kind=link}

{kind=link}

BDC Charts

{kind=link}

{kind=link}

{kind=link}

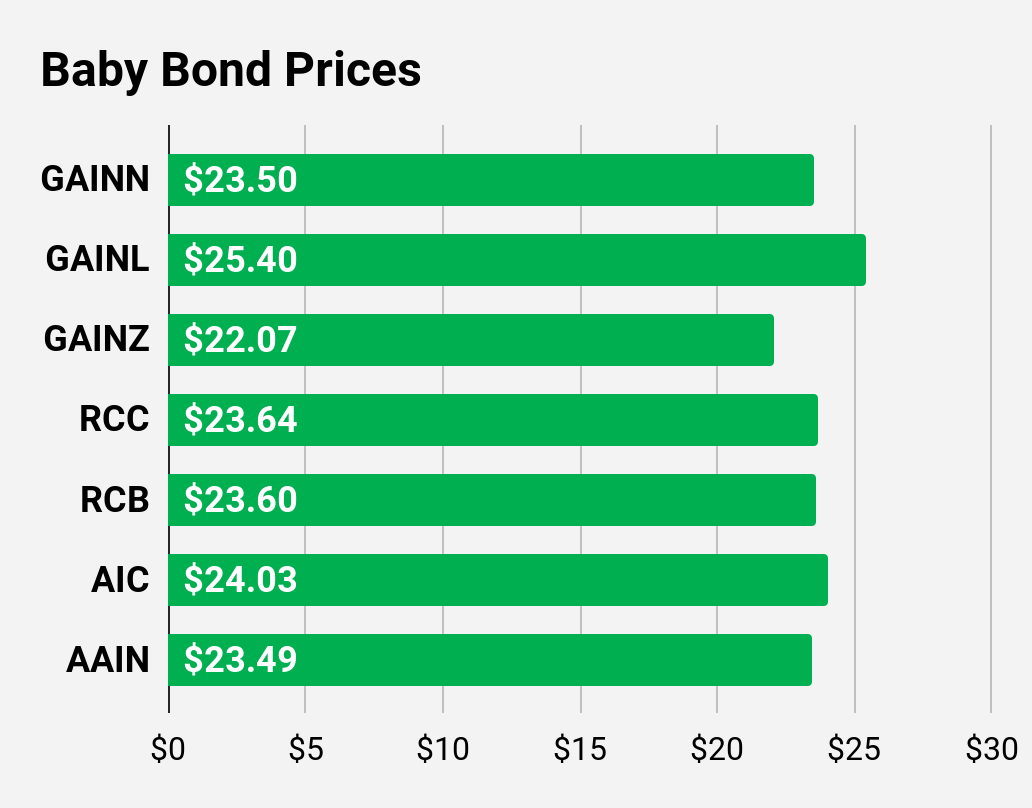

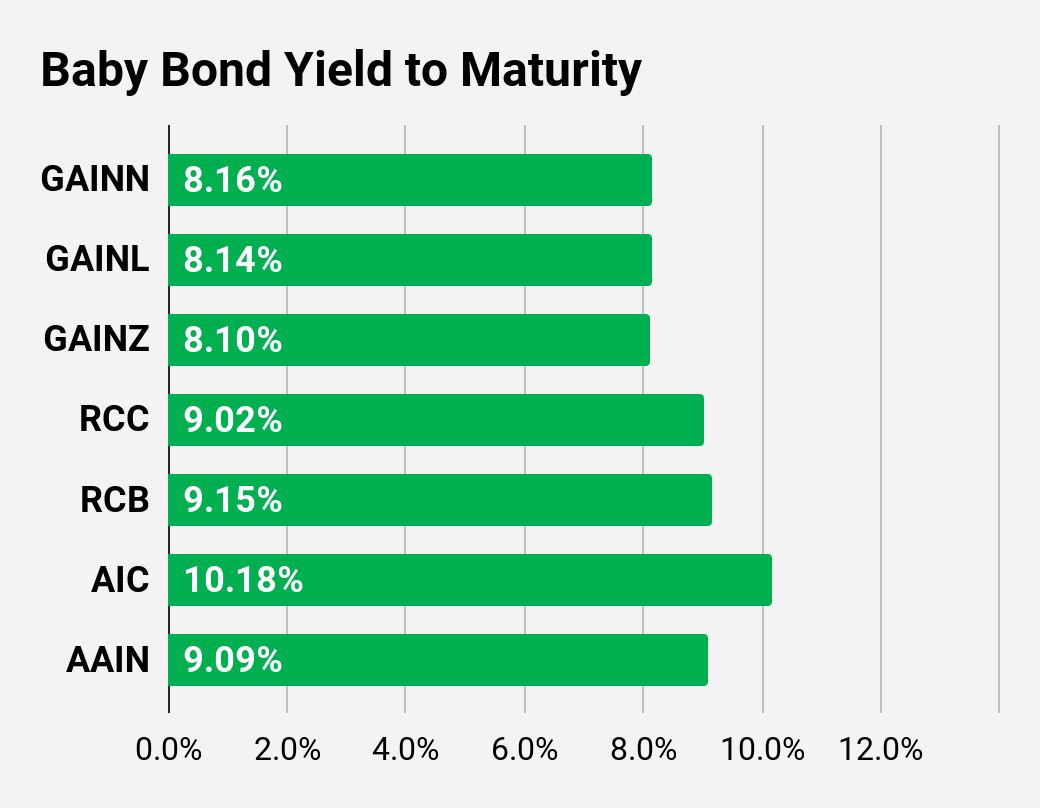

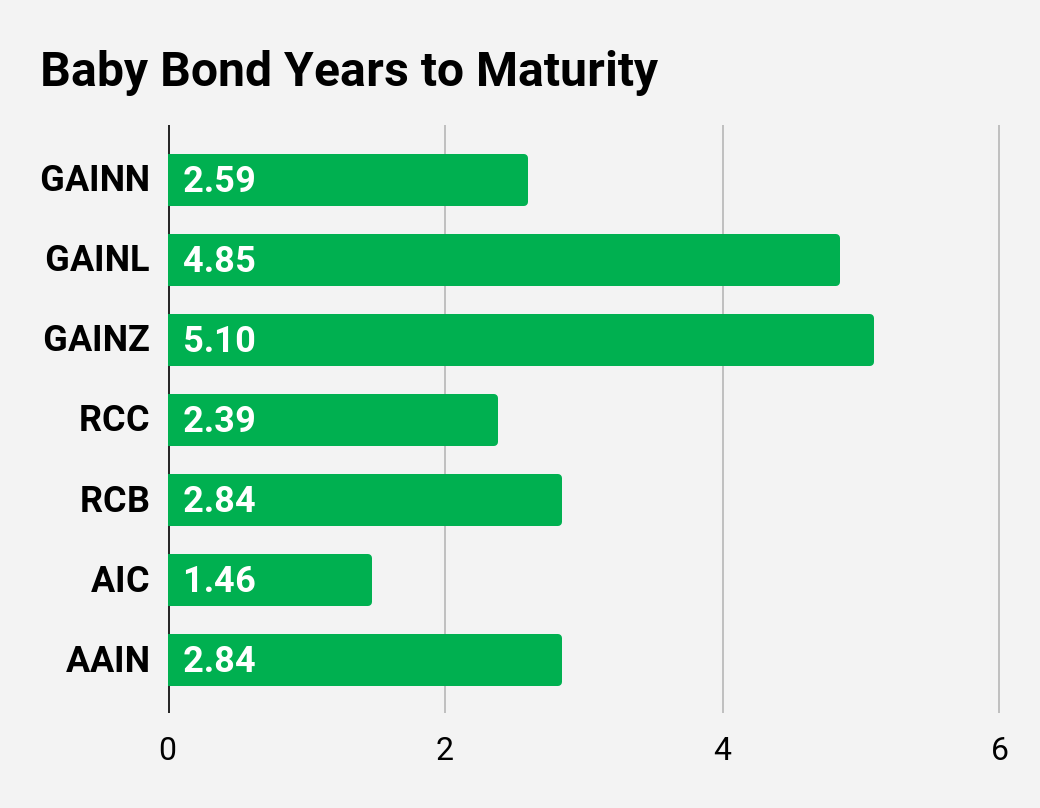

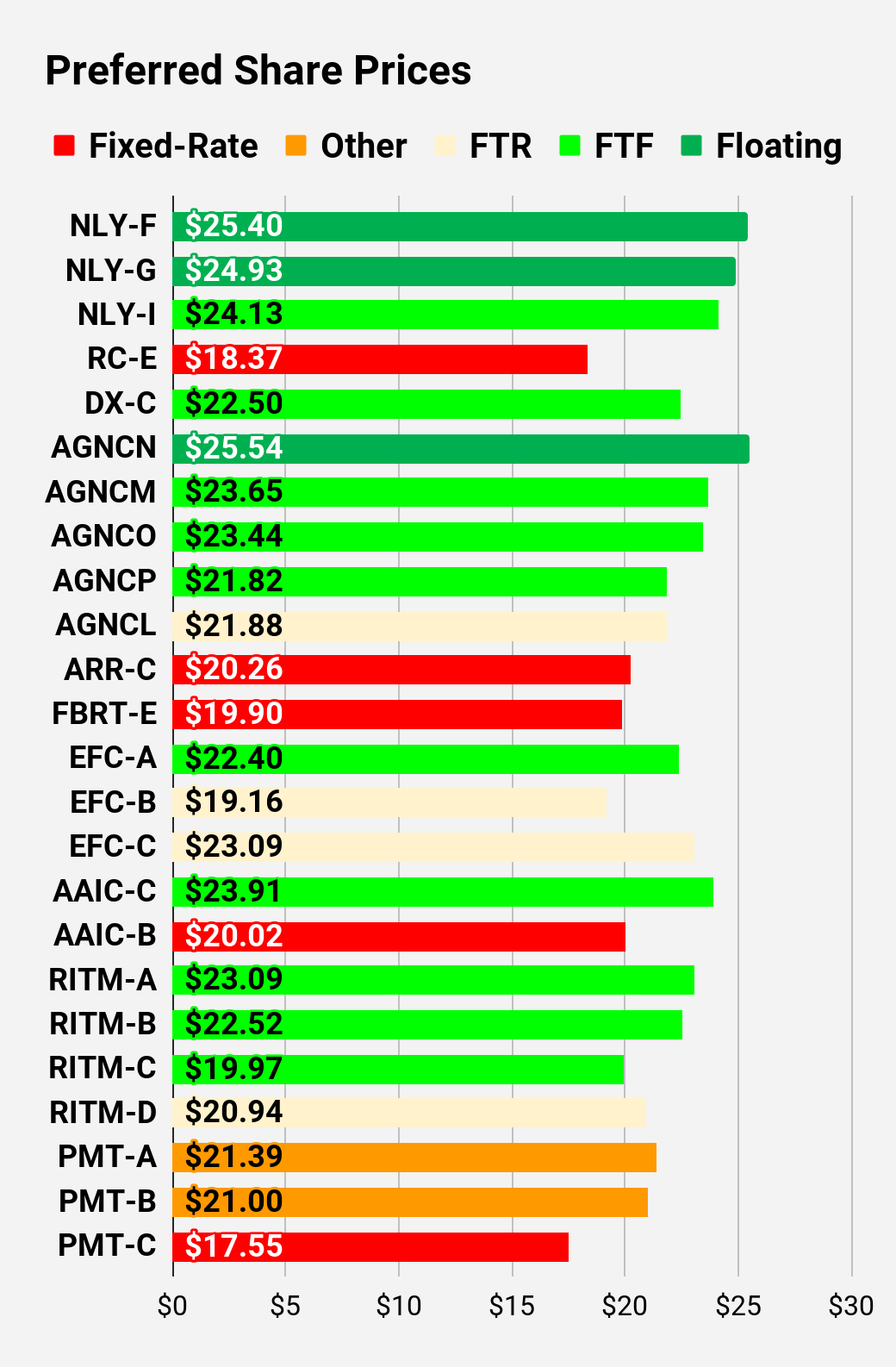

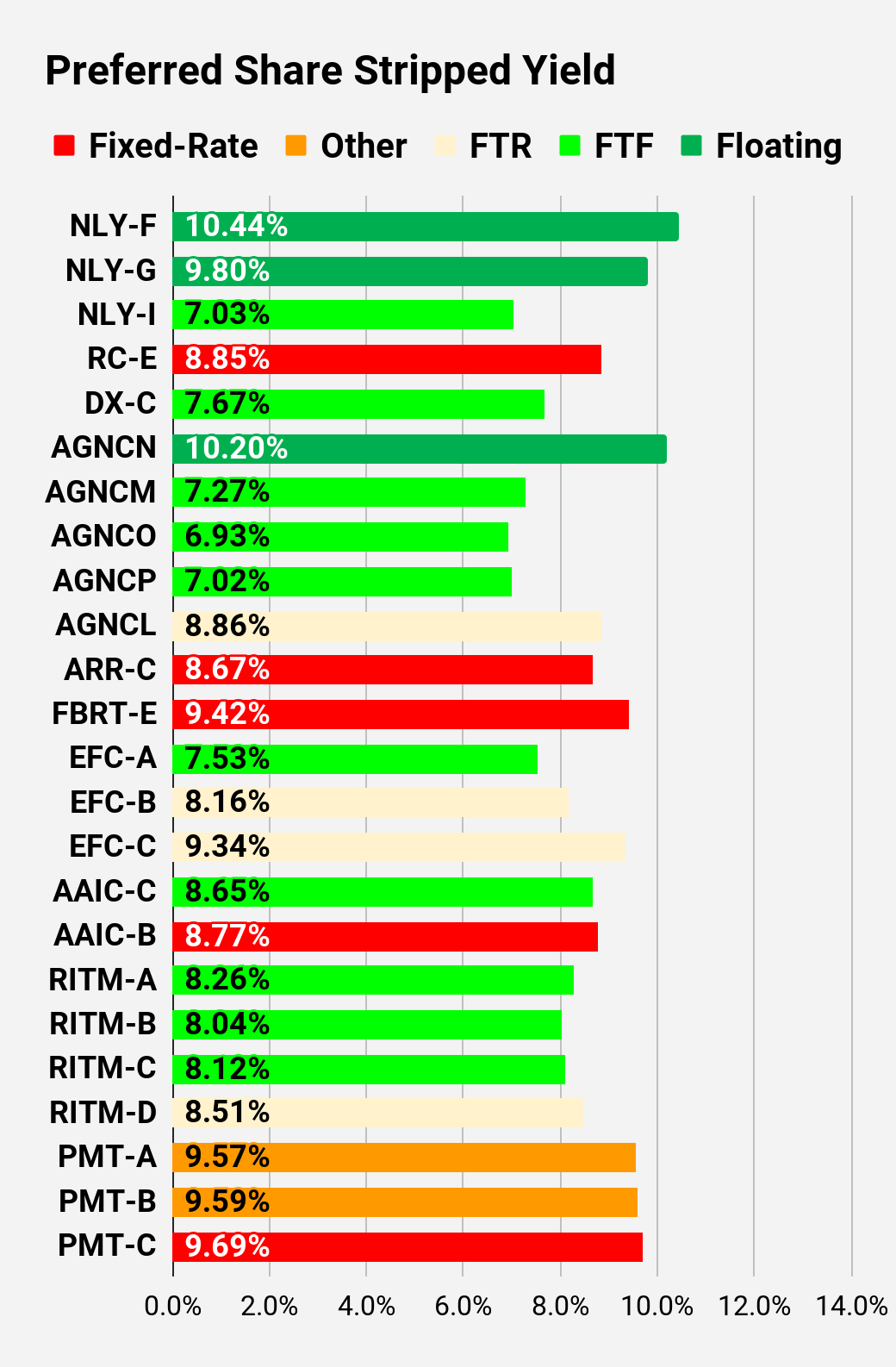

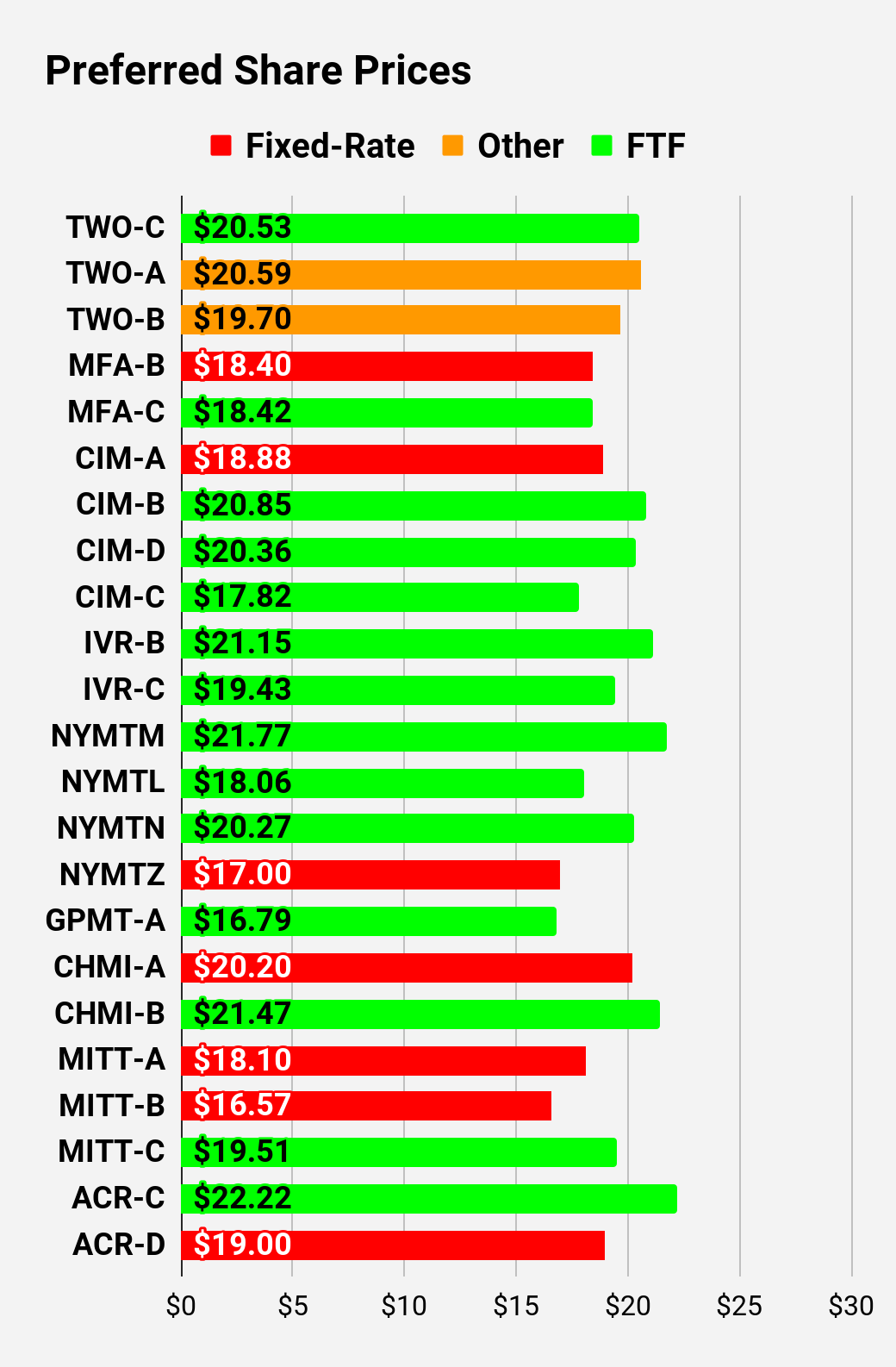

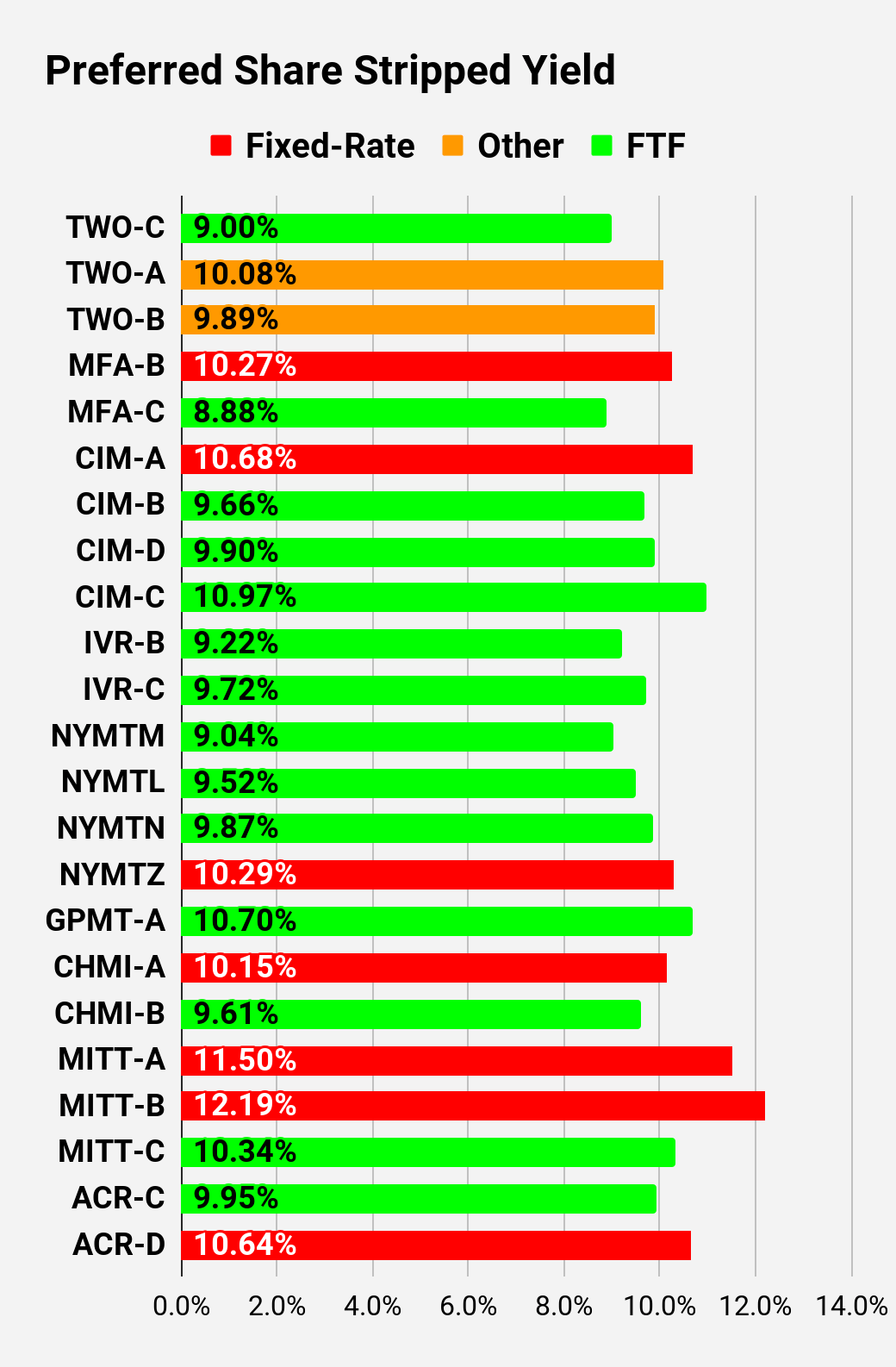

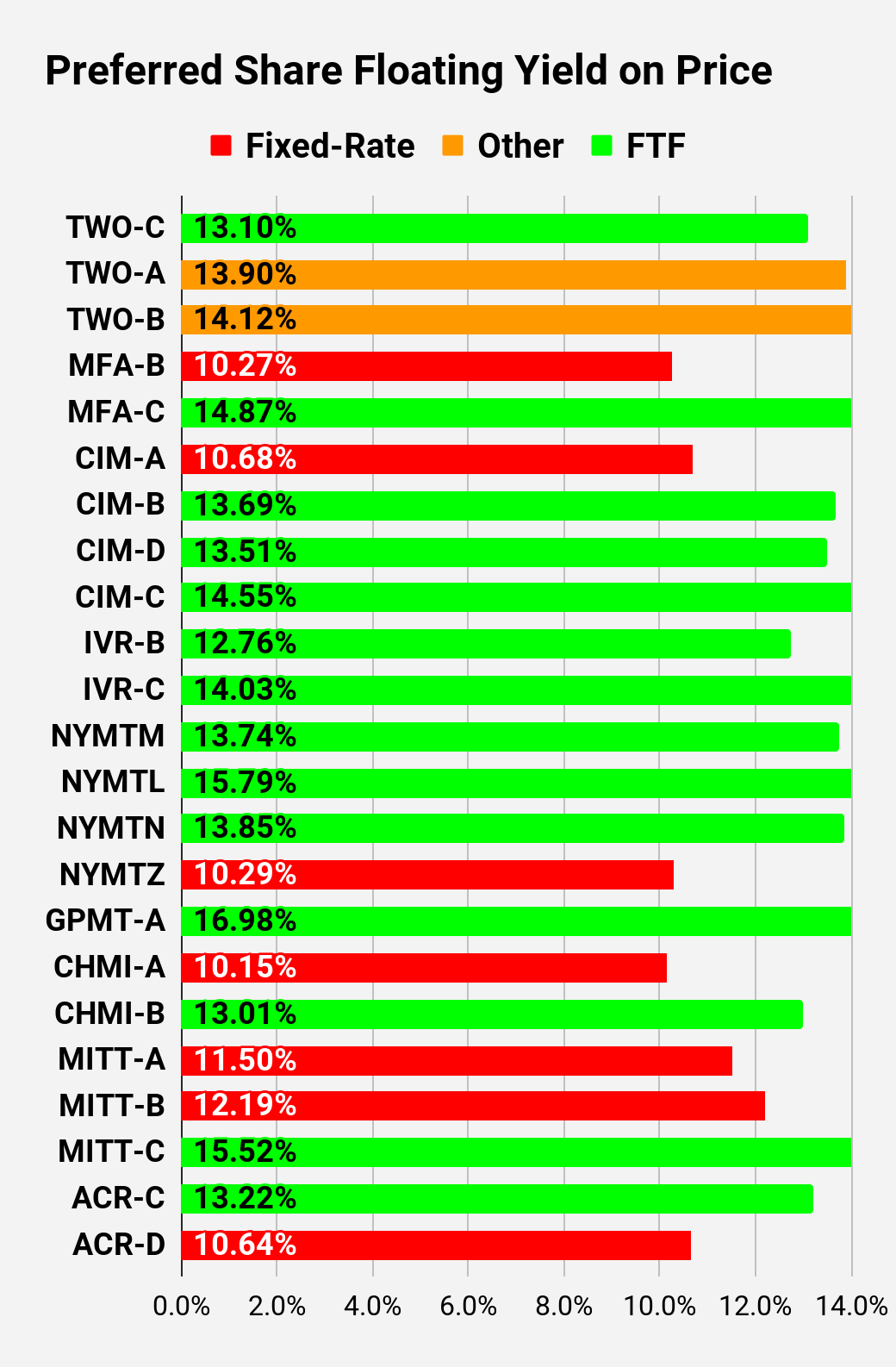

Preferred Share and Baby Bond Charts

I changed the coloring a bit. We needed to adjust to include that the first fixed-to-floating shares have transitioned over to floating rates. When a share is already floating, the stripped yield may be different from the "Floating Yield on Price" due to changes in interest rates. For instance, NLY-F already has a floating rate. However, the rate is only reset once per 3 months. The stripped yield is calculated using the upcoming projected dividend payment and the "Floating Yield on Price" is based on where the dividend would be if the rate reset today. In my opinion, for these shares the "Floating Yield on Price" is clearly the more important metric.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Note: Shares that are classified as "Other" are not necessarily the same. Within The REIT Forum, we provide further distinction. For the purpose of these charts, I lumped all of them together as "Other."

For further details see:

Big Dividend Yields Going Higher, Dumb Debt, And Snark