BIG - Big Lots: Dichotomy Between The Fundamental And Technical Landscapes

Summary

- The risk-reward on both the standalone chart and the relative strength chart looks appealing.

- We touch upon the vast array of fundamental challenges that the company faces.

- We have a Hold rating on BIG.

Introduction

At the outset of this article, let me state that we have a hold rating on the stock of the home discount general merchandiser - Big Lots, Inc. ( BIG ). The rating is driven by a stark contrast in the overall fundamental picture, and the risk-reward equation on the charts. We'll first start with the appealing facet of the BIG story, before moving to some of the troubling fundamental issues, which to be honest, are quite a lot.

Stock looks oversold, enticing risk-reward on the charts...

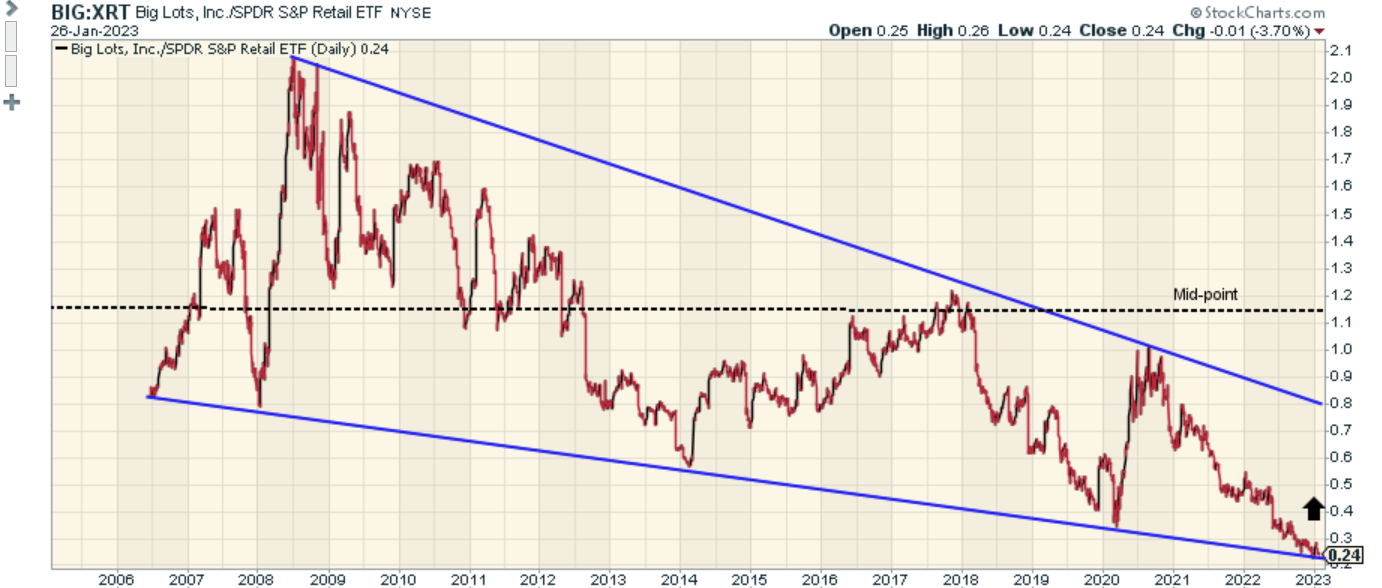

When we were fishing for suitable mean-reversion opportunities in the retail space, BIG was one of the primary names that jumped out. The image below provides a snapshot of BIG's strength, relative to the SPDR S&P Retail ETF ( XRT ) which focuses on 94 retail stocks that account for a share in the S&P Total Market Index.

What we can see is that this ratio is clearly oversold, trading at record lows and around 4.7x lower than the mid-point of the long-term range. Crucially, the ratio is now intriguingly perched at the lower boundary of its falling wedge pattern, which sets it up nicely for a potential reversal to the mean.

{kind=link}

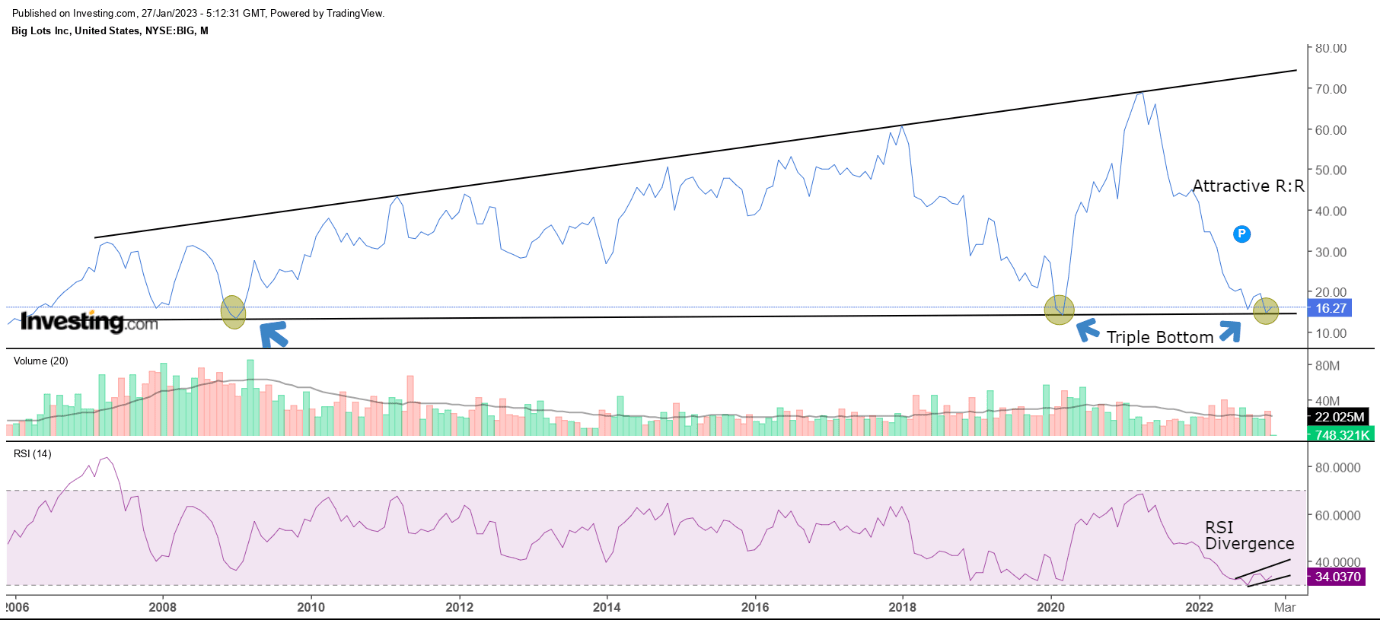

Then, if you switch over to the long-term standalone chart of Big Lots, there are a few things to note. Firstly, the upper and lower boundaries of the long-term price imprints are rather well-defined. Recently we saw the stock drop towards the lower boundary and bounce from that point, representing a triple bottom of sorts (it had hit those levels previously in 2008 and 2020).

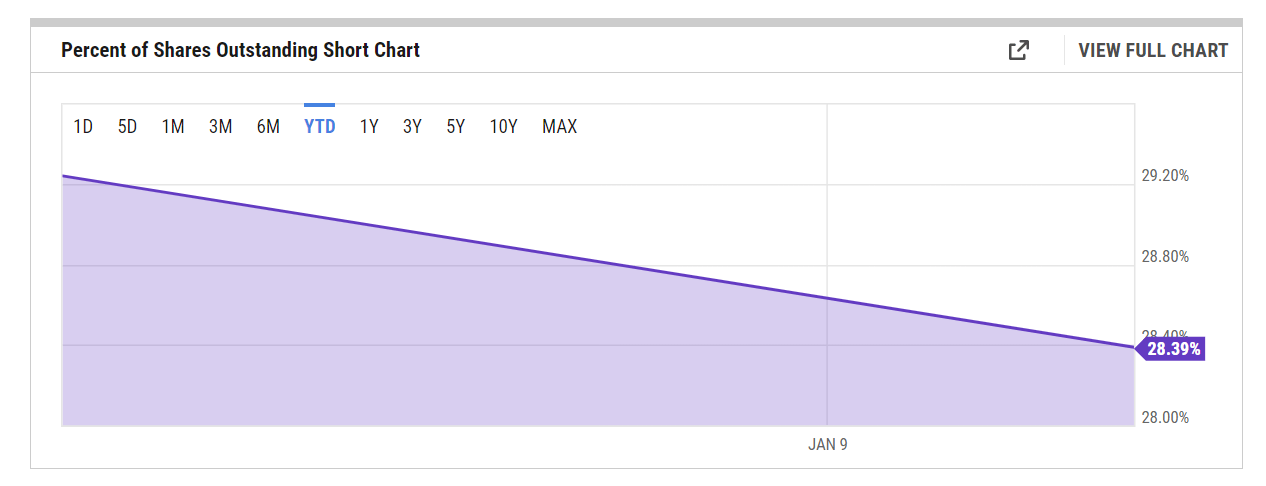

BIG "may" also benefit from a strong bout of short-covering as the level of shorts is quite elevated at 28.39%; interestingly enough, in January, there were already some faint signs of the short-sellers covering their position.

{kind=link}

There's no guarantee that the stock will trend upwards, but at least the prospect of bottom formation around these levels look rather encouraging. If you want to be a tad bullish also consider that the 14-period RSI has shown some signs of divergence by moving upwards.

{kind=link}

...but the fundamentals are a mess

Whilst there may be some promising signs with the technicals, it's difficult to turn bullish on the Big Lots stock when you consider the challenges it is currently going through.

In the recently reported quarter, group comp sales were down by 12%, and this is expected to be a lingering narrative for the foreseeable future, with the management guiding for yet another quarter of double-digit declines in Q4. Do consider that the sell-side community expects revenue declines to persist all through FY23, with expected FY declines of ~11% .

Given its inherently discounted profile, BIG's management seems to think they are well-positioned to attract customers who could trade down in a challenging economic environment. There may be some merit to that rationale, but when the company's largest selling item is a discretionary item like furniture (~25% of group sales), what sort of momentum could we expect when the housing market is in a slump?

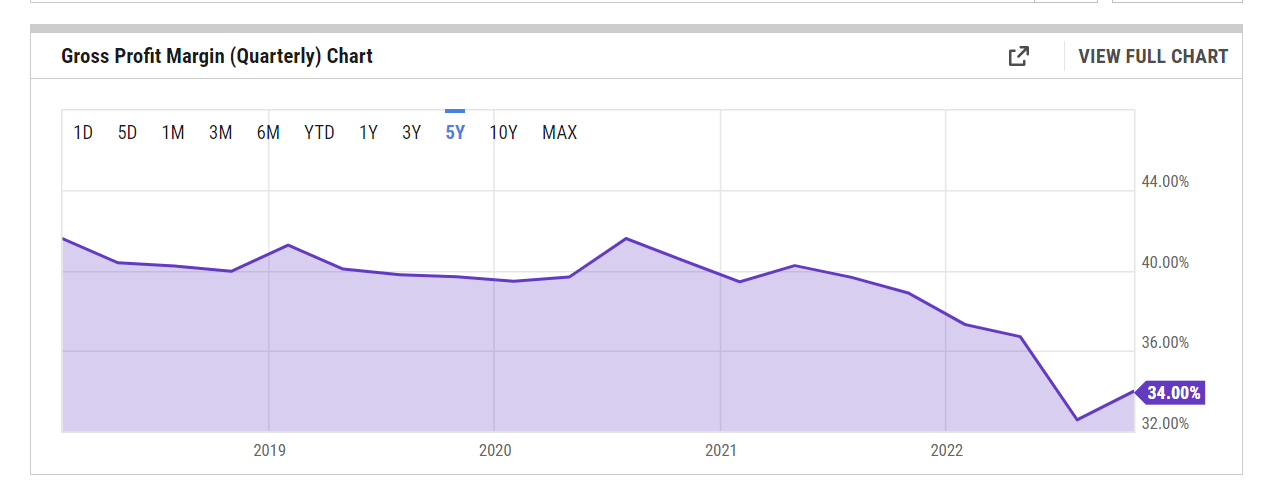

Moving on from the topline, note that gross margins have just about inched up from the 5-year lows, as the company engages in deep markdowns linked to store closures and inventory clearances.

{kind=link}

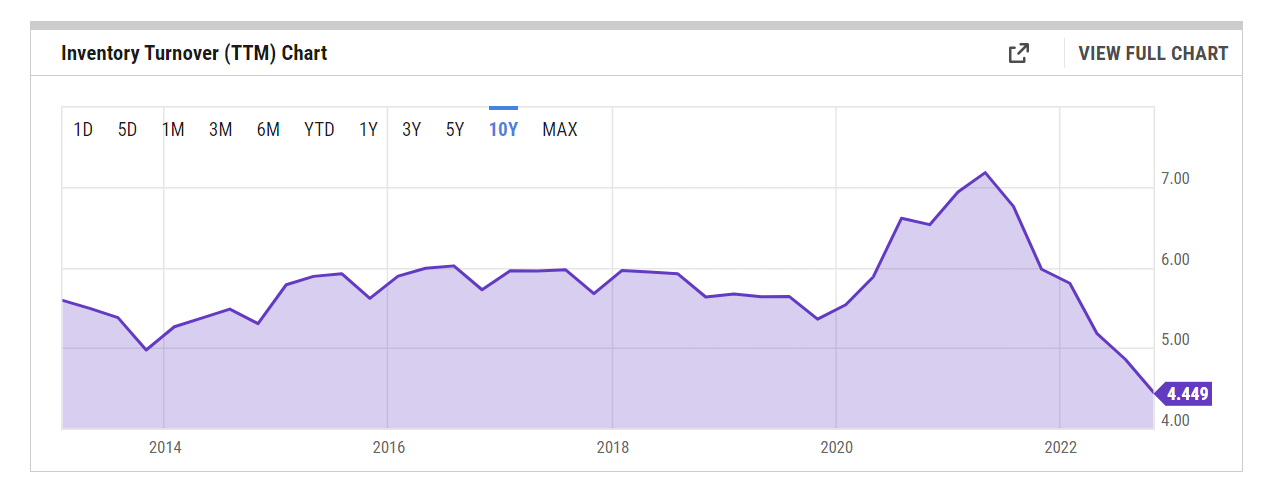

As far as the inventory is concerned, BIG still has its work cut out, as its level of inventory turns has now dropped to 10-year lows.

{kind=link}

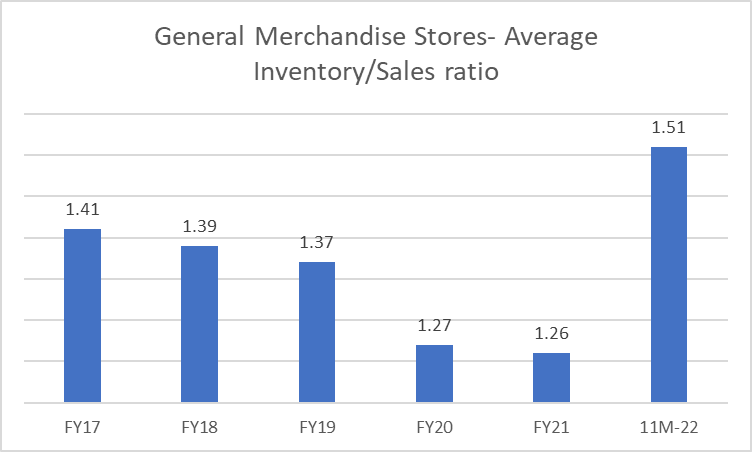

In Q4, BIG's management stated their desire to keep inventory flat or lower on a YoY basis, but I'm not sure that will move the dial. In fact, if one looks across the industry, excess inventory still seems to be a common issue. Data from Census shows that the latest average inventory turnover ratio of 1.51x for general merchandisers is well above the 5-year average of 1.34x.

{kind=link}

Basically, investors should expect massive price discounting and markdowns as incumbents grapple for market share. In light of that, it is difficult to envisage a massive improvement in gross margins. In fact, in the latest earnings call, BIG management stated that most of the freight-related cost reductions they would likely witness in early 2023, could be reflected in even lower price revisions, particularly in the furniture space.

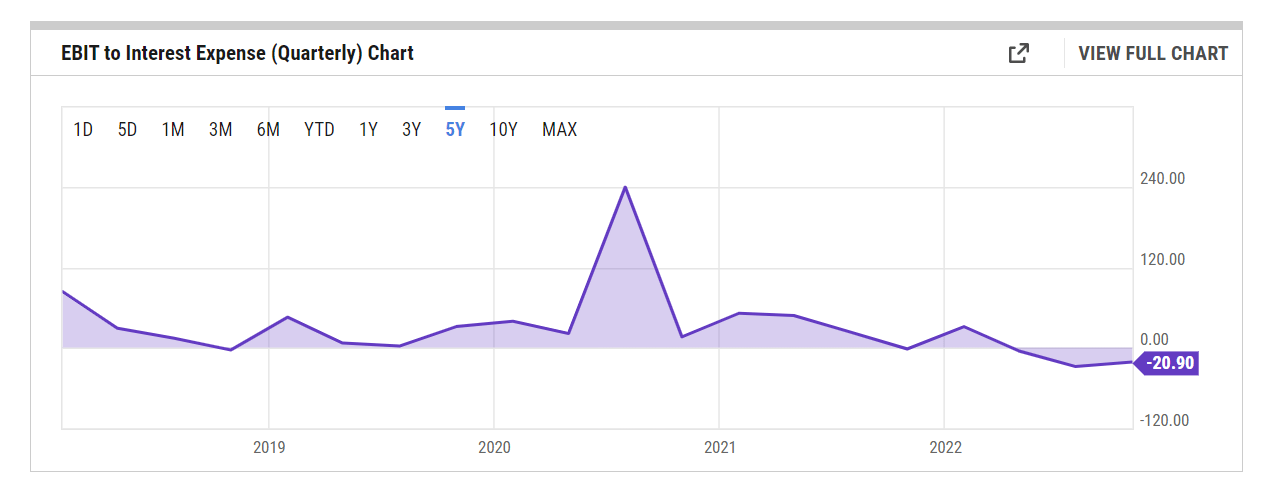

It's not as if BIG is generating ample operating profits to just pass on these cost benefits. As you can see from the image below, the EBIT is currently not in a position to cover the interest costs, which in Q3, grew by 2.7x YoY, even as the company sought to draw higher amounts of debt from its credit facility.

All in all, investors should consider that BIG will likely deliver losses through FY23 (-$6.3 ) and FY24 (-$0.69).

{kind=link}

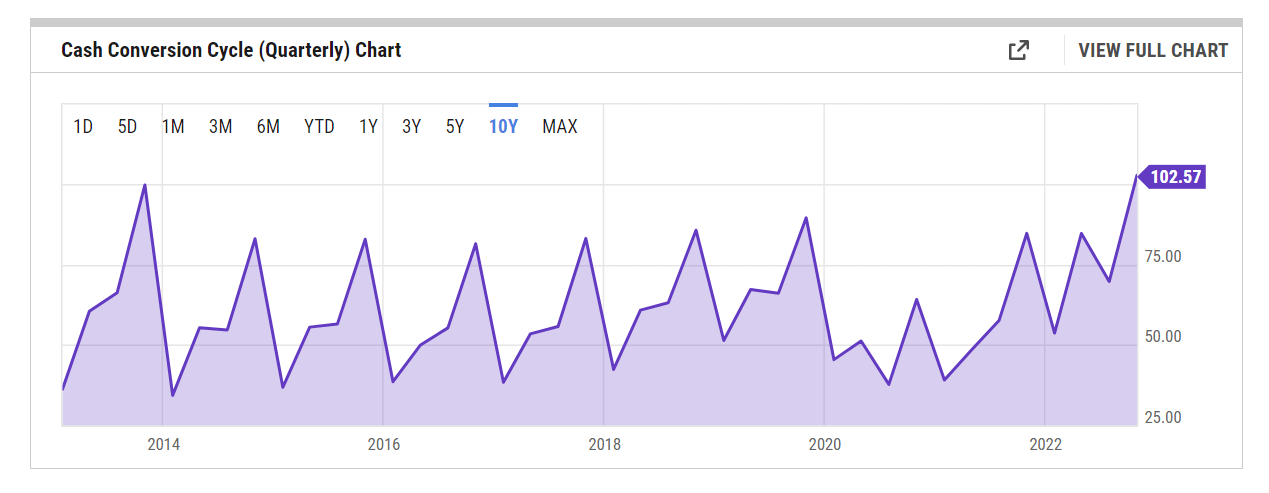

Besides inventory management, BIG is also not doing a great job of managing its receivables and payments functions either, and this means a lot of cash is unnecessarily tied down with working capital. As you can see from the image below, the cash conversion figure is currently at its highest point in 10 years.

{kind=link}

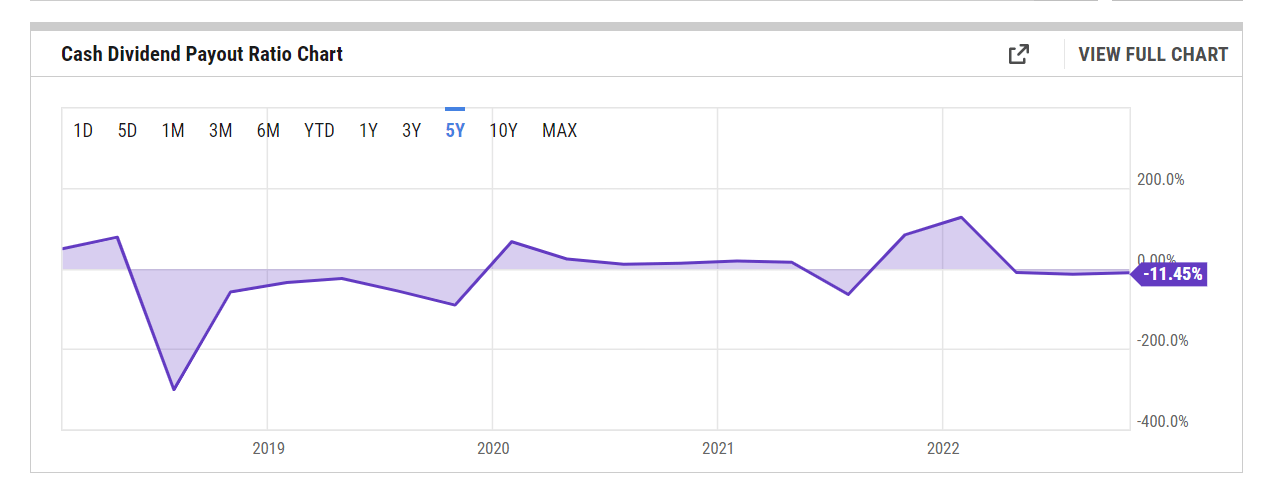

Then some investors pursue BIG solely for its dividend, and granted, a +7% figure is not something to be scoffed at, but I'm genuinely concerned with the inability of BIG to fund its dividends via cash flow alone. In fact, the cash dividend payout ratio, which gives you a sense of the dividends as a function of free cash is in negative territory. It is going to be challenging for them to meet their dividend bill (as of 9M-22 cash spend towards dividends was over $28bn) and investors should brace for the prospect of this being cut. Maybe management thinks that disposing off 25 odd-owned stores could bring some much-needed cash to fund the dividends, alongside the growing financial leverage, but is that sustainable?

{kind=link}

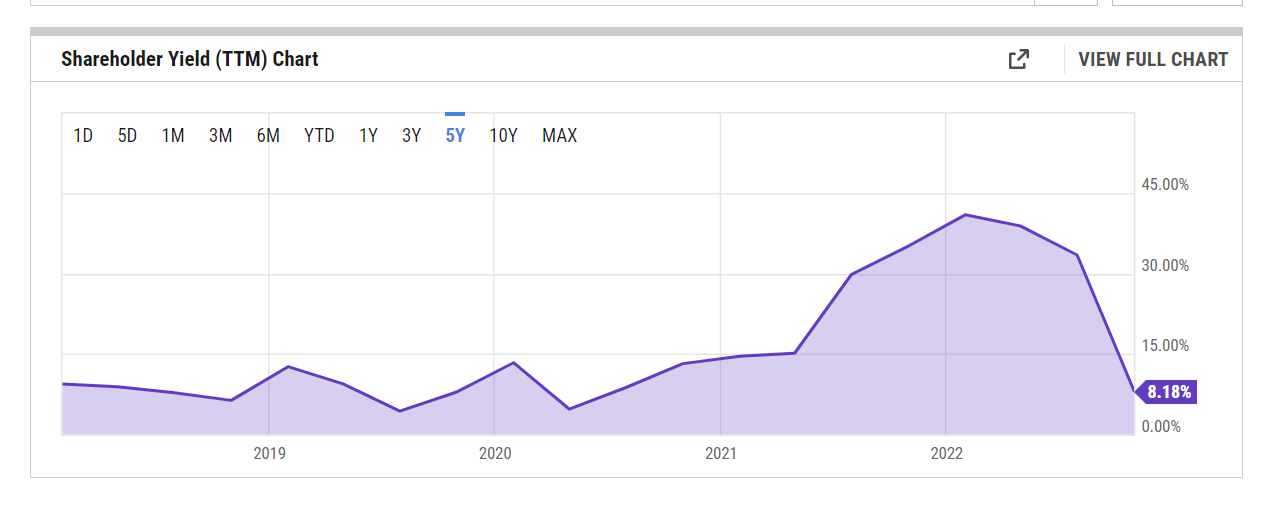

Typically, when a stock drops to lowly levels, management usually resorts to buybacks but note that with BIG they haven't done any buybacks this year, despite $159.4m of buyback authorization still pending (as part of the 2021 $250m Repurchase Authorization Plan). That doesn't reflect well on the funding position of the firm.

In effect, rather than looking at just the dividend yield, investors may consider looking at the declining trajectory of the "shareholder" yield which not only considers dividends but also buybacks and the level of debt pay downs. Over the last 5 years, BIG's shareholder yield has been around 16% , now it is half that.

{kind=link}

{kind=link}

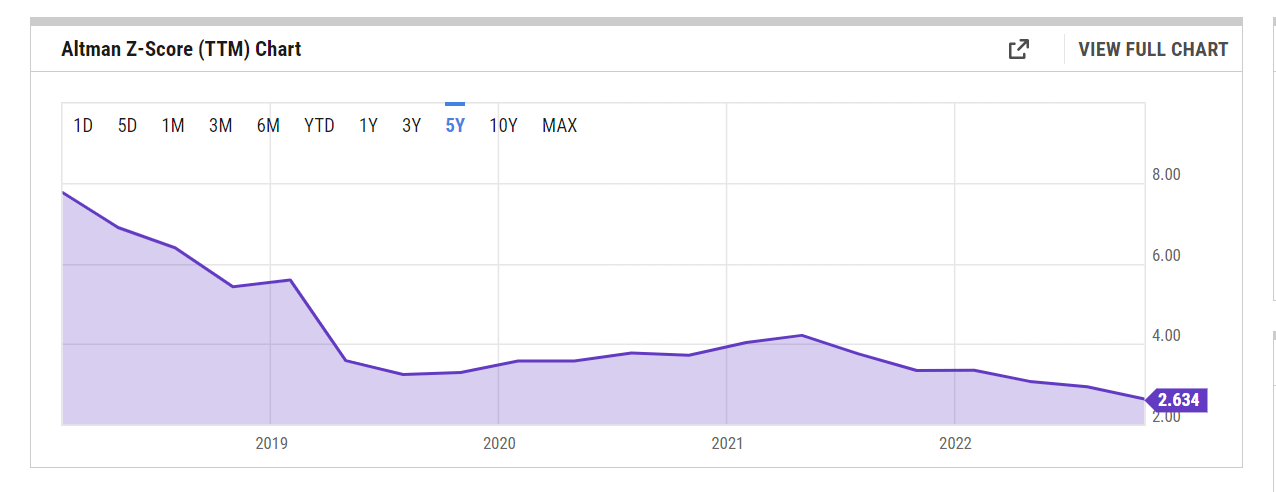

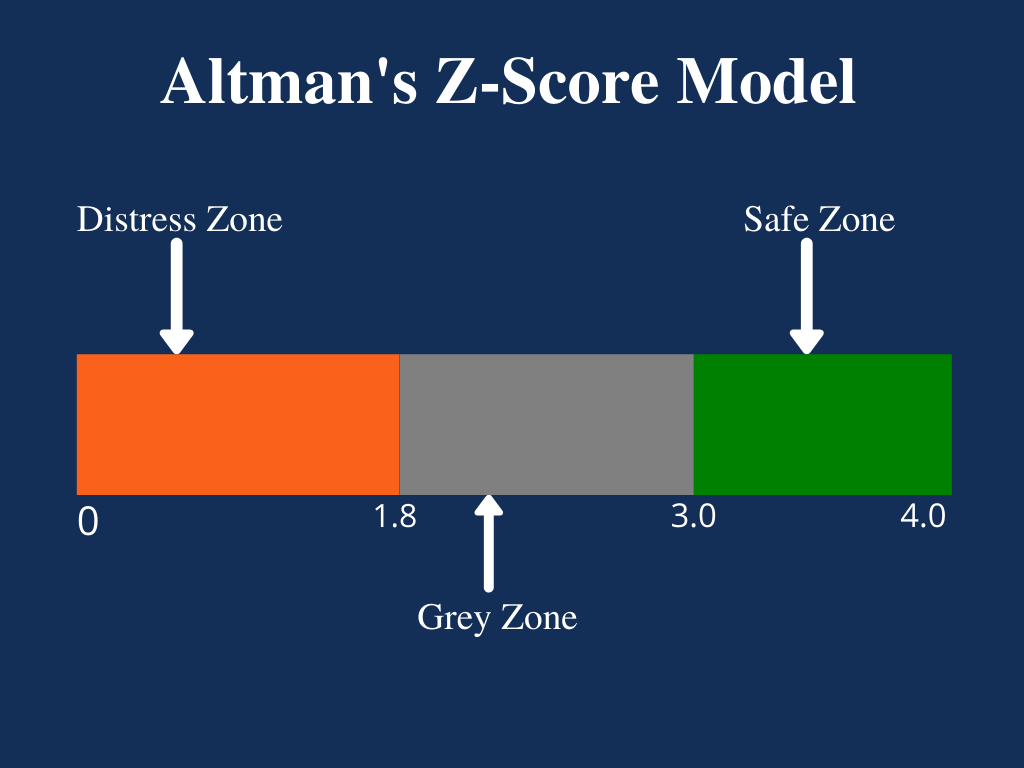

Clearly, BIG is on shaky ground, and whilst it is not yet in bankruptcy territory, things are quite troubling. The Altman Z-score throws up a composite figure based on 5 key ratios ranging from working capital, sales, EBIT, and retained earnings per asset besides the coverage of liabilities by equity. Traditionally BIG has enjoyed a Z-score of 4.2X, these days it is only around 2.6x, implying a moderate chance of bankruptcy.

{kind=link}

Closing Thoughts

Despite how appetizing the risk-reward equation looks on the charts, BIG's fundamental issues are too vast and troubling to warrant a long position at this point. Unless you're someone with an ultra-aggressive risk appetite, I would advise you to wait on the sidelines.

For further details see:

Big Lots: Dichotomy Between The Fundamental And Technical Landscapes