BNTX - BioNTech: A Cheap Large-Cap Pharma With Growth Drivers

2023-03-28 11:06:44 ET

Summary

- BioNTech is quite undervalued after you back out its tremendous and growing cash hoard garnered from its COVID vaccine windfall.

- The company's mRNA technology and other therapies in development could support one of the cheapest long-term buy entries in the biotech/pharma sector.

- Intense selling pressure in the stock ended in 2022, as the world reopened from COVID shutdowns.

- The March 27th earnings release and reduced guidance for 2023 may have opened a terrific opportunity to purchase a position.

BioNTech SE ( BNTX ) just reported weaker-than-expected guidance for 2023 , despite another strong quarter in the middle of winter for sales of its Comirnaty COVID vaccine with partner Pfizer ( PFE ). Basically, management guided for as much as $2 billion less in sales for the whole year than Wall Street estimates.

You would think a sizable share price decline would ensue. At the open of trading BNTX did decline, as the German biotech concern experienced a price under $120. However, I do believe smart investors should be looking to buy shares at this level. Why? With some $15 billion in cash at the end of December (projected to rise to $17+ billion over 24 months) and almost no debt, on a struggling stock quote, the current equity market capitalization of $30 billion represents only $15 billion in enterprise value.

Eventually, management will have to do something with its extra cash, not needed to run ongoing operations. The massive cash hoard can (and should) be used for share buybacks. The company announced this morning, it will continue a buyback program, with 3.7% of outstanding shares retired at a price around $142 in 2022. Of course, with the big rise in short-term interest rates, $15 billion in cash should earn $500+ million in pre-tax interest income this year, with rates in Europe and America in the 3% to 5% range.

The capital could also be returned as a large one-time dividend to owners, or it could finance the acquisition of a number of existing drugs with billions in sales or a group of late-stage development assets, or it could be spent buying out another relatively large biotech/pharma name for cash. BioNTech doesn't need to borrow money to finance these deals, which would all be accretive to the long-term value of the underlying business (assuming management did not overpay for the assets).

COVID Shot Future

Another interesting note to contemplate is Pfizer now expects a RISE in vaccine demand after 2023. Pfizer and BioNTech co-developed, manufacture and ship the Comirnaty vaccine, which became the leading health care product to fight the COVID pandemic globally. In terms of success, total Comirnaty revenues reached $70+ billion during 2021-22, and will likely still be a major revenue source for both companies over the next 3-5 years.

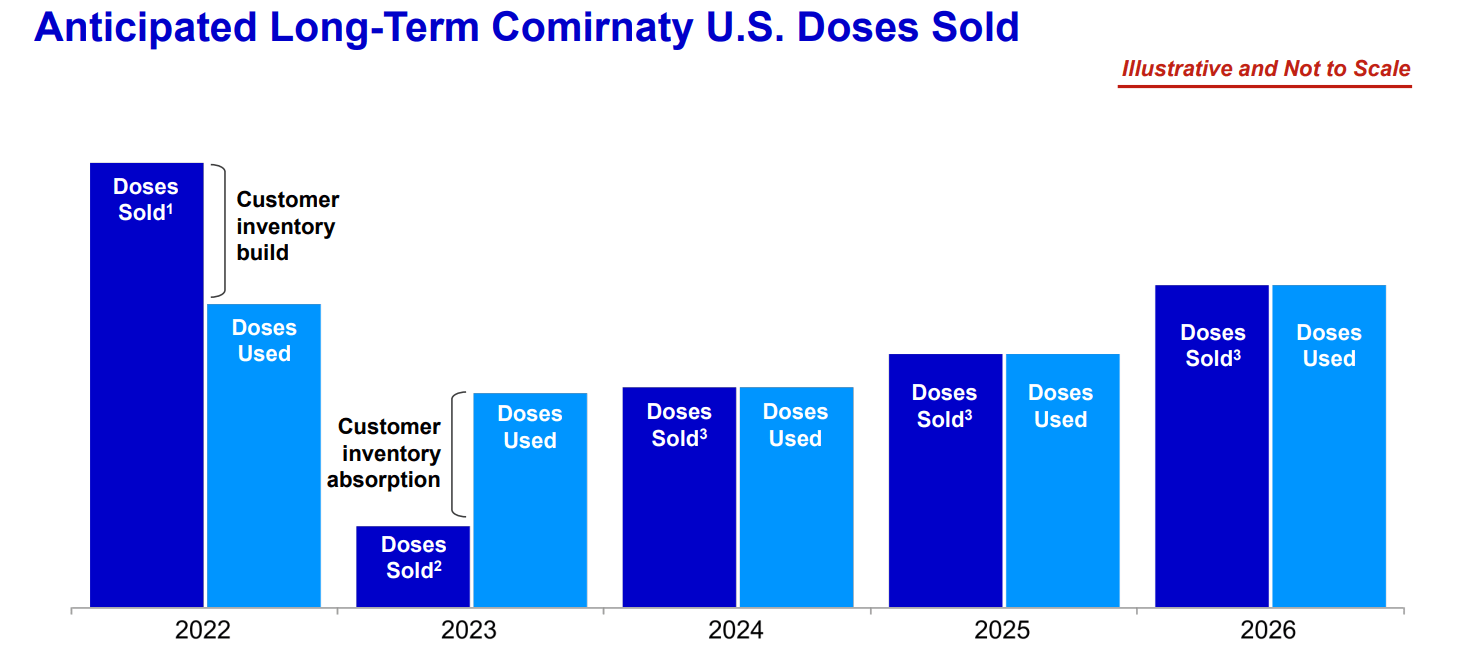

Part of the downgrade in 2023 results for BioNTech appears to come from an oversupply of shots to western governments sold during 2022, with this inventory projected to be worked off during the year. For 2024-26, new COVID shot formulas are expected to continue for the at-risk population, with pre-existing health conditions and/or weakened immune systems in age groups above 50.

In fact, a pediatric version of the vaccine may be approved this fall. Plus, a dual-medicine, single-injection shot to fight both COVID and Influenza at once (now in testing) could seek government approval as soon as 2024.

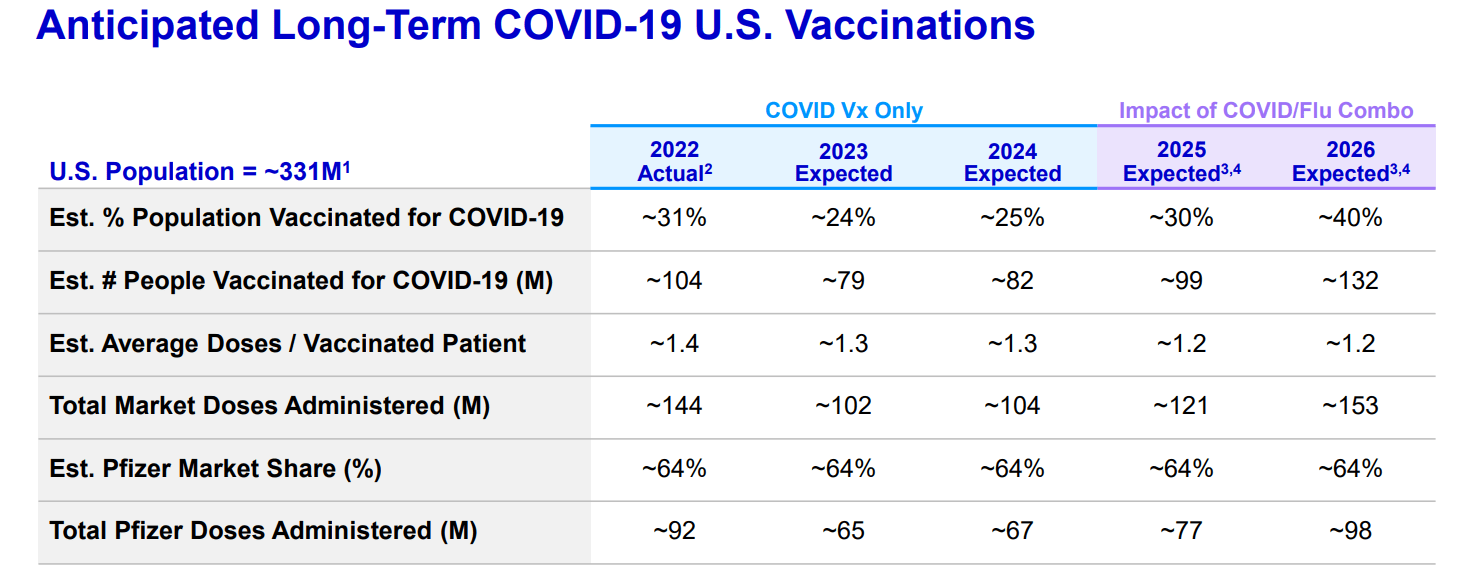

So, if you can get past the negative news drop of the day, COVID-related sales for BioNTech may actually "bottom" this year. Pfizer's estimates for sales into 2026 are pictured below.

Pfizer - Q4 2022 Earnings Presentation Pfizer - Q4 2022 Earnings Presentation

{kind=link}

{kind=link}

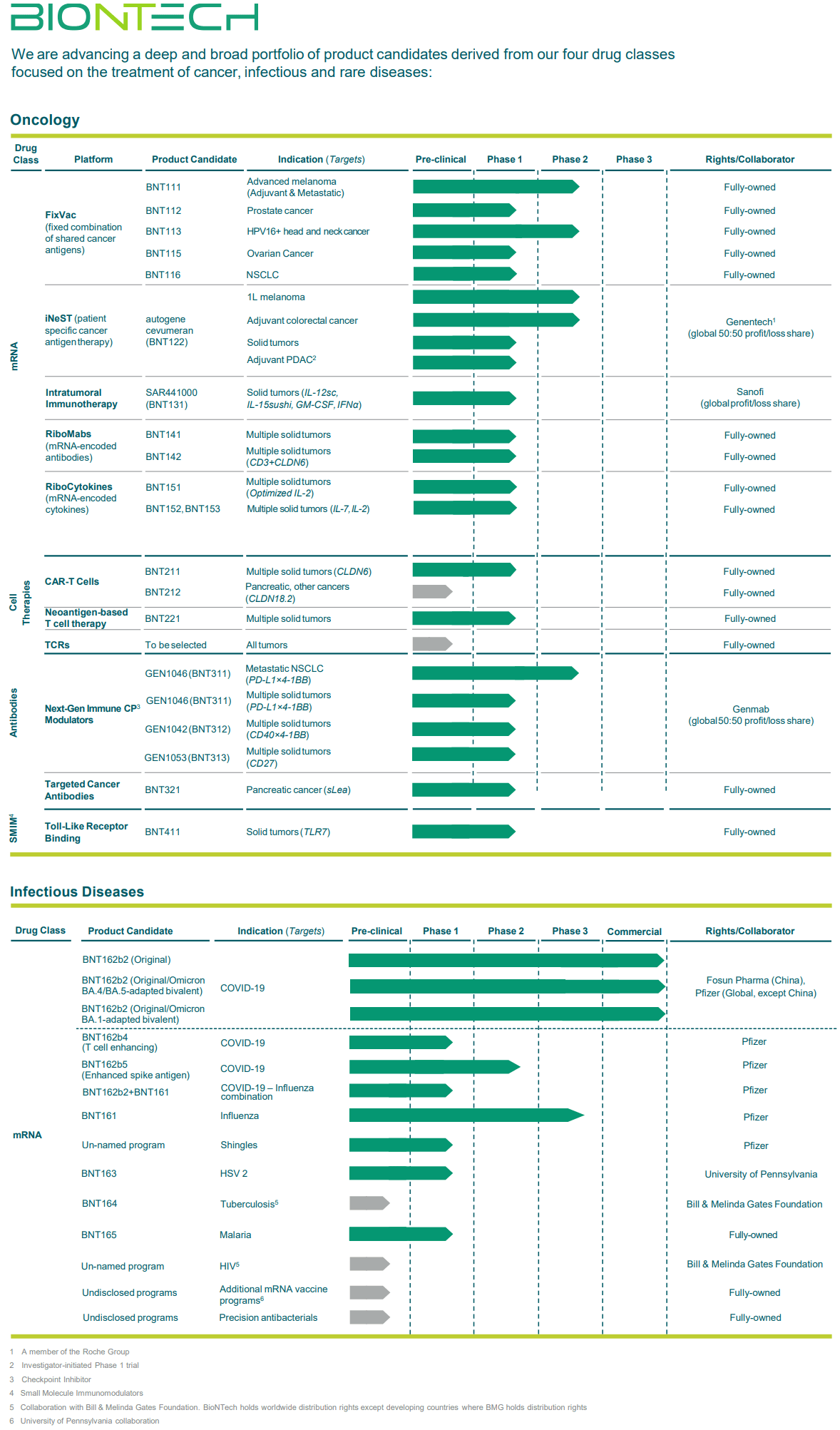

Large Pipeline of Drugs

In addition, a Shingles mRNA product could likewise be approved in 2024, according to Pfizer, jointly developed with BioNTech. For sure, this is a hint at all the patented drugs with billions in sales that could be approaching for the company using a whole new class of proven mRNA therapies.

Versions of BioNTech's revolutionary mRNA technology are being tested as a treatment for malaria, prostate/pancreatic cancers, and advanced melanoma to name just a few.

All of its medical inventions include 33 therapies in active testing. The company has one Phase 3 trial ongoing, plus six in Phase 2, and twenty-seven in Phase 1 or preclinical stages. Below is table of the strong pipeline well worth owning for pharmaceutical investors.

February 2023 - BioNTech Pipeline Slide

{kind=link}

BioNTech's Low Valuation

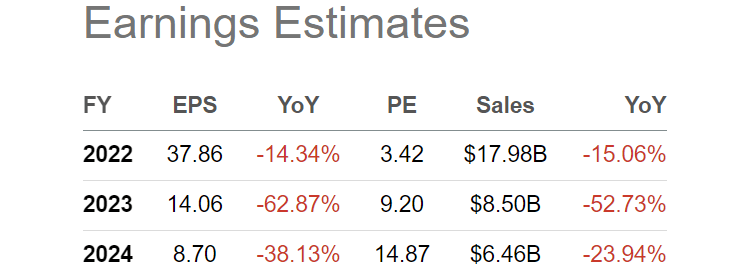

Here's the breakdown of the low valuation argument to own shares. Remember, the logic for BioNTech's big share price slide in 2022-23 is peaking revenues and earnings from the breakthrough COVID vaccination developed with Pfizer. Wall Street analyst estimates were already calling for a steep drop in company financial results this year and next, as the pandemic crisis fades.

BioNTech may prove a classic example of the difference in rearview mirror investing vs. taking an honest forward-looking view of reality. Until new drugs are approved, the operating business is relying on Comirnaty demand for almost all of its sales. If you take these bearish forecasts at face value, and limit your thinking to the immediate downgraded future of the business, what's to like is a fair question. Below are analyst estimates for 2023-24, before today's earnings release and lowered guidance.

Seeking Alpha Table - BioNTech, Analyst Estimates for 2022-24, Made on March 23rd, 2023

{kind=link}

Using the released guidance announcement, I would extrapolate 2023 numbers of more like $6 to $6.5 billion in sales, and EPS closer to $8 are appropriate. Using Pfizer's assumptions, new COVID shot creations alongside regular demand each fall/winter could mean the 2024 estimates for BioNTech pictured above may be close to reality. In the end, actual EPS/revenue results during 2024 and beyond will be affected by what the company does (if anything) with its cash stash this year.

Forward Valuation Data before Today's Guidance

It will likely take YCharts a few days to fully factor in changing Wall Street analyst forecasts using the new company guidance this morning. However, using the data on YCharts available now, we can review how inexpensive the company has become, after stripping out all the cash. (We can fairly assume the presented ratios will rise from those pictured.)

The truly bullish read of the valuation comes when you factor in BioNTech's pristine balance sheet with roughly $15 billion in cash and almost no debt held at the end of December 2022. Translation: fully 50% of the current stock quote is represented by this net cash position, earning interest for owners.

When we review enterprise valuations (subtracting the net cash from BNTX's equity capitalization), a whole different picture of cheap appears. On forward estimated results the next 12 months, shares are incredibly inexpensive vs. peers and competitors in the larger biotech company space. Multiples of EV to forward EBITDA and revenues are drawn below, with a history of trading back to January 2021. Investors are getting 4x EBITDA and 2.35x sales, once the cash is backed out of the equation (not necessary to run the business). Using my personal estimates after this morning's company guidance, 5x to 6x EBITDA and 3x sales ratios on EV are likely more accurate for 2023.

YCharts - BioNTech, EV to Forward Estimated EBITDA & Revenues, Since January 2021

Here's how BioNTech stacks up against a list of "profitable" large-sized biotechs and a select group of leading Big Pharma names. You will notice BNTX shares are far and away the least expensive of the group. The EV discounts to industry averages are around 65% lower on EBTIDA (40% post announcement estimate) and 55% less on sales (40% post announcement estimate)!

YCharts - Major Biotechs Earning Profits, EV to Forward Estimated EBITDA, 1 Year YCharts - Major Biotechs Earning Profits, EV to Forward Estimated Sales, 1 Year

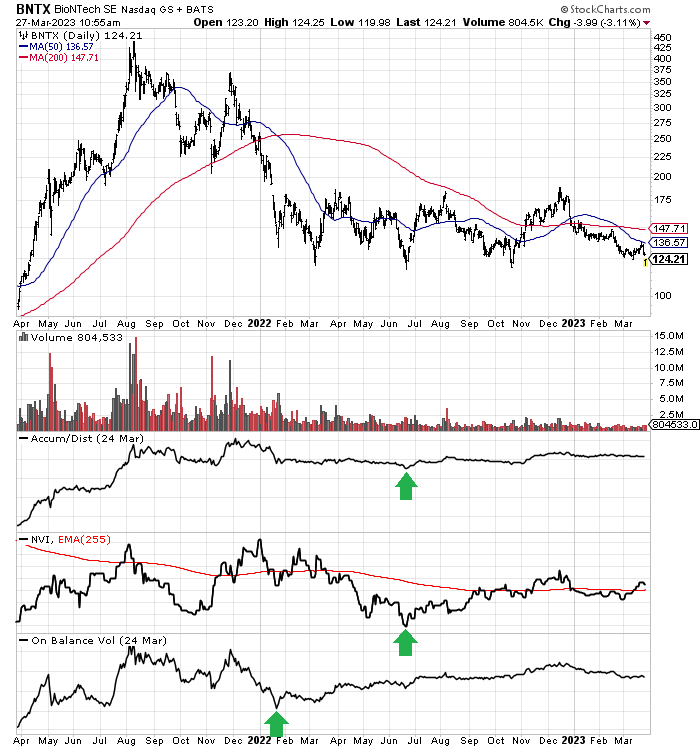

T echnical Trading Pattern

BioNTech's stock trading momentum has also been stronger than you might think over the last 12 months, when you dig deeper. Sure, price has been in steady decline since August 2021, but the -70% price dump has witnessed less-intense selling pressure after June 2022. I have drawn green arrows below highlighting the indicator reversals in the Accumulation/Distribution Line , Negative Volume Index , and On Balance Volume readings. These 3 signal-callers are on a short list of my favorite momentum constructs. Essentially, each of them is moving in the right direction now, not confirming the -30% price weakness from December 2022 to the present.

StockCharts.com - BioNTech, 2 Years of Daily Price & Volume Changes, Author Reference Points

{kind=link}

Final Thoughts

My trading forecast is BioNTech is nearing an important price reversal. Investor and analyst sentiment is now completely washed out. My bullish logic goes as follows - if regular seasonal COVID shot demand surprises to the upside from this point, while new medicine inventions are approved for a wide array of illnesses, on top of the cash hoard being spent wisely in an accretive fashion, the future for shareholders is actually quite bright. There could be 5 or 6 catalysts for share growth starting today (sentiment bottom), moving through the next 12-18 months.

Pharmaceuticals and biotechs often fight recessions and bear markets better than many other sectors of the market. In terms of investment risk for BioNTech, I tend to think there is now very little downside, with rotten COVID vaccine demand now the baseline, fully-discounted case.

My research conclusion is BioNTech is currently valued at a low 10x multiple on 2024 after-tax earnings, after subtracting a projected $17+ billion in cash on hand in 18-24 months (assuming it is not used for share buybacks or acquisitions) and using today's $30 billion equity capitalization at $120 a share.

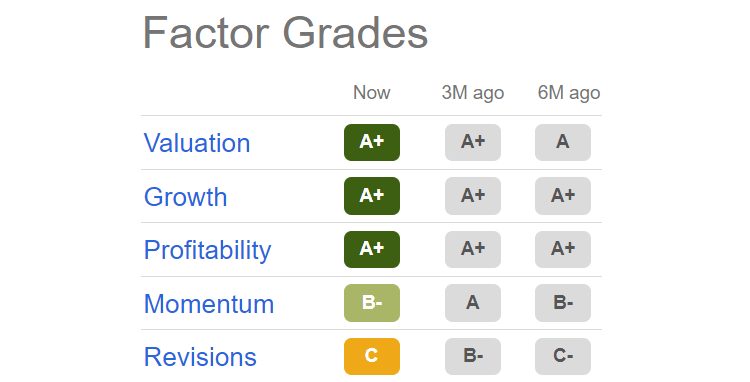

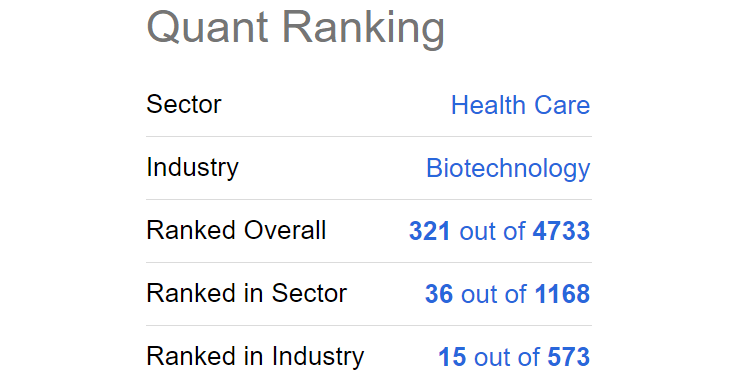

Seeking Alpha's computer ratings actually like BioNTech as an investment idea, compared to a universe of alternative equity choices beyond 4,700 names. Factor Grades are much higher than the average pharmaceutical, while the Quant Ranking is Top 3% for the prescription drug industry and Top 7% vs. the overall U.S. equity market.

Seeking Alpha Table - BioNTech Factor Grades, March 23rd, 2023 Seeking Alpha Table - BioNTech Quant Ranking, March 23rd, 2023

{kind=link}

{kind=link}

The biggest risk to an investment in BioNTech would be a complete and total end to the COVID pandemic, including our healthcare responses to it. Yet, medical experts tend to believe the novel coronavirus will take many years, if ever, to become irrelevant for higher-risk health condition individuals. The good news for BNTX shareholders is regular demand for annual vaccine inventions may be the new normal, similar to flu shots.

Additional long-term risks "might" include limited to zero success developing new mRNA (alongside other therapy) products for cancers and contagious diseases. Plus, the possibility of a U.S. stock market crash could affect the share price for at least a spell, if a rotten economic scenario unfolds from the spike in inflation and interest rates witnessed since early 2021. However, BNTX's monster cash holdings should buffer against serious selling pressure, and prevent an immediate price decline over the next 12 months of greater than -20%, in my estimation. A 20% share price drop under $100 would translate into EV ratios roughly 65% of the current setup, all other variables remaining the same.

The upside opportunity over the next 3-6 months is a Pfizer takeover offer (or bid by another major pharma concern) at a +30% to +40% premium. Pfizer could easily decide it wants the mRNA technology and expanding BNTX drug pipeline for itself. The net cost of a BioNTech takeover by a Big Pharma concern is far lower than you would think, with 50% of the current stock price backed by cash holdings.

Longer term, if COVID refuses to go away quietly, BNTX may be dramatically undervalued today, as the cash hoard piles up. A +50% gain back to $180 a share is not out of the question over the next 12 months, if heaven forbid another variant worse than the omicron version now dominant in the world is unleashed.

Weighing all the BioNTech pros and cons, I lean toward the Buy camp at $130 or lower for a share quote into April. Strong Buy territory is likely around $110, again assuming the company spends its cash in an accretive way for shareholders.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

BioNTech: A Cheap Large-Cap Pharma With Growth Drivers