BNTX - BioNTech FY22 Earnings Review - 5 Questions Answered After Today's Results

2023-03-27 19:47:03 ET

Summary

- BioNTech announced its Q422 and FY22 earnings today, and also provided FY23 guidance.

- Revenues were ~$18.7bn, thanks to its share of revenues from sales of the Comirnaty COVID vaccine it co-developed with Pfizer. Net profit was >$10bn.

- This exceptional performance won't be repeated in FY23 - the forecast is for revenues of ~$5.4bn and profits of ~$1bn. Cash position is >$14bn.

- BioNTech is more than a COVID vaccine developer - its infectious disease vaccine platform and multi-layered oncology platform are clicking into gear.

- It's going to take several years to understand exactly what BioNTech has under its bonnet - but based on the opportunities - as I discuss in this post - the outlook appears bullish.

Investment Overview

BioNTech ( BNTX ) - the messenger-RNA pioneer that partnered with pharma giant Pfizer ( PFE ) on the Comirnaty COVID vaccine - announced its Q422 and FY22 earnings earlier today, as well as updating on its product pipeline and providing financial guidance for FY23.

Let's start with the basics - total revenues for FY22 were $18.7bn, operating cash flow was $14.7bn, and net profit was $10.2bn (euro figures adjusted to dollars using xe.com). In 2021, using current exchange rates, revenues were $20.4bn, and net profit was $11.1bn. Earnings per share in FY22 were $40.77, vs. $42.78 in FY21.

BioNTech was established in 2008 to use new technologies to try to develop novel medicines, primarily against cancer, and the company IPOd in 2019, raising ~$150m at $15 per share, valuing the business at $3.3bn at the time.

Nobody could ever have predicted the pandemic, nor BioNTech's role in developing Comirnaty - which went on to become the leading COVID vaccine and generate >$75bn in revenues, split roughly 50/50 between BioNTech and Pfizer - and as such its likely investors who backed the company in 2019 would never have imagined that the stock price would be up >700% today, trading at $123 per share.

Of course, BioNTech shares traded much, much higher at the height of the pandemic - reaching >$350 per share in November 2021 when the Omicron strain broke out, which valued BioNTech at ~$85bn market cap - or 26x more than its initial post IPO valuation.

The company's current market cap valuation is $31bn, and BioNTech also announced its FY23 guidance today - for ~$5.4bn in revenues, and ~$2.7bn in R&D costs, ~$755m in SG&A expenses, and ~$593m in capital expenditures, and a tax rate of ~27%, implying net income of ~$1bn, and a forward price to earnings ratio - at current traded price of $123 per share - of ~31x.

That feels about right as an assessment of the value of BioNTech at the present time, given the blend of opportunities in play, which includes advanced stage programs in infectious disease and oncology as well as the emerging private COVID vaccine market.

What's clear is that - barring the emergence of a new and more deadly strain of COVID necessitating a fresh round of mass global vaccinations - BioNTech is not likely to generate revenues in the same ballpark as 2021 and 2022 for another decade at least, if it ever does. In fact, it may be that ~$5bn - $10bn in annual revenues may come to feel like a ceiling for BioNTech for the rest of this decade at least.

In order to explain why I have come to this conclusion I have come up with five questions - and answers - that help readers understand what the state of play is at BioNTech at the present time, and how it is likely to change across the rest of the decade.

Let's begin by looking at what BioNTech's management - led by husband and wife co-founders Dr. U?ur ?ahin and Dr. Özlem Türeci - continue to insist is one of their three strategic priorities for 2023, along with immuno-oncology and infectious diseases - the COVID-19 franchise.

Question 1 - How Will BioNTech's Covid Revenues Trend Over The Remainder Of This Decade?

BioNTech is doubtless correct that some sort of commercial - as opposed to government sponsored - market for COVID vaccinations will begin to emerge in 2023.

Partner Pfizer has discussed hiking the price of Comirnaty by >4x, to somewhere between $110 - $130, and in its FY22 earnings presentation , released earlier today, and during its earnings call , BioNTech management discussed the implications of such a market.

The first thing to note is that the Advisory Committee on Immunization Practices ("ACIP") and the Vaccines and Related Biological Products Advisory Committee ("VRBPAC") will rule on which strains COVID vaccine developers will be asked to target with a view to a fall booster season, so there may still be government buying in 2023, although the fall booster season never really took off in 2022 so expectations may not be overly high for 2023.

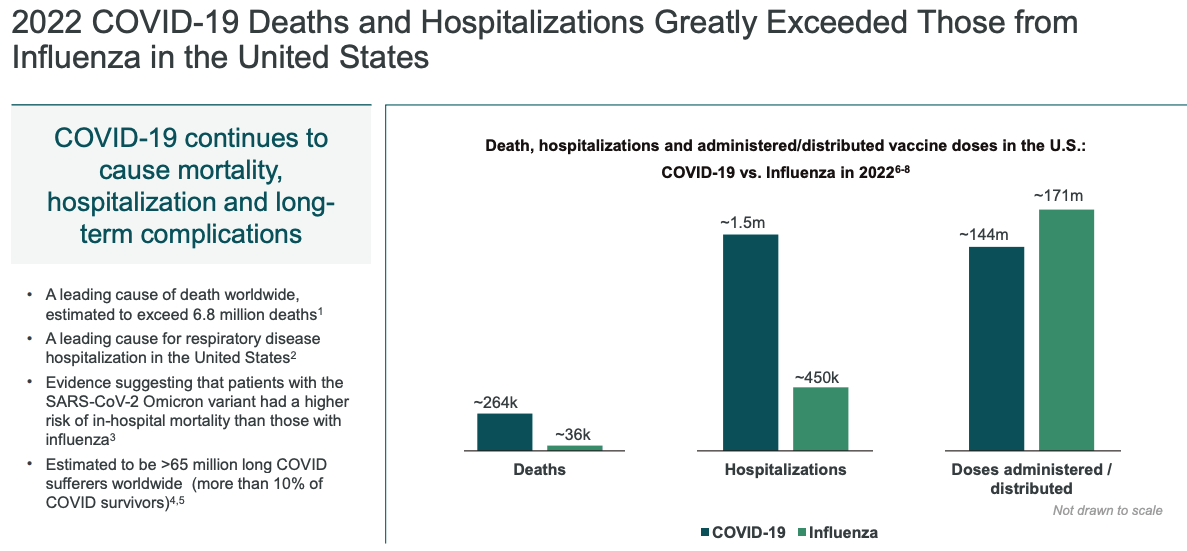

BioNTech's Chief Strategy Officer ("CSO") Ryan Richardson told analysts on the earnings call that "it will likely take a few years to fully transition from a pandemic to steady-state market," and went on to compare COVID rates of deaths and hospitalizations with influenza.

COVID vs Influenza deaths and hospitalisations 2022 (BioNTech Earnings presentation)

{kind=link}

As we can see, the CSO's point is that COVID is more deadly than influenza, and leads to >3x more hospitalizations , yet fewer doses are administered annually.

Going forward, it's therefore not beyond the realms of possibility that a COVID vaccine market may emerge that is similar in size - or perhaps larger than - the influenza market, currently valued at ~$7.5bn per annum and growing at a CAGR of ~7%.

A private COVID market could emerge that's worth as much as ~$15bn - $20bn per annum, perhaps, and if we consider Comirnaty's 60% market share in 2022, that could land BioNTech as much as $6bn per annum in peak revenues.

Management does not expect this market to reach maturity until after 2025, and insurers will likely need to be prepared to reimburse for vaccines for such a market to take off, therefore I would rate a $6bn per annum revenue opportunity as an optimistic scenario.

BioNTech does have a variant-adapted COVID vaccine in development, as well as T-cell enhancing variants, and a flu / COVID combo shot. In answer to my question, therefore, I would not expect BioNTech's COVID franchise to deliver >$5bn per annum in revenues certainly in 2024 and 2025, and $5bn could be the long term ceiling for the company in this emerging market.

2 - What's The State Of Play Within BioNTech's ex-COVID Infectious Diseases Pipeline

Of course, with its breakthrough messenger-RNA technology it's natural that BioNTech is developing vaccines against other infectious diseases. While rival Moderna ( MRNA ) has developed advanced stage mRNA vaccines addressing RSV, influenza, and cytomegaolvirus, BioNTech is looking at Shingles, Malaria, and influenza.

Only the influenza vaccine has made it beyond a Phase 1 study thus far - influenza is a crowded market however where pharma giants such as AstraZeneca ( AZN ), GSK ( GSK ), Novartis ( NVS ) and Sanofi ( SNY ) control market share, so BioNTech's candidate will have to deliver best-in-class efficacy and safety in order to succeed.

Regarding Shingles, co-founder and Chief Medical Officer Özlem Türeci told analysts today:

The Phase 1/2 multicenter randomized controlled dose selection study will evaluate the safety, tolerability and immunogenicity of mRNA vaccine candidates against shingles.

The study is aiming to enroll up to 900 healthy volunteers 50 through 69 years of age and is being concluded in the United States. Phase 1 will help select for optimal mRNA vaccine candidate, dose level, dosing schedule and formulation for advancement to Phase 2. Participants in the study will be followed to determine how long protection may last.

Regarding Malaria, management has promised "multiple additional trial starts in the next 12 months," and more generally, "multiple data updates from these newer infectious disease vaccine programs over the course of the year."

Given BioNTech's revenues will fall from >$18bn to ~$5bn in FY23, and potentially fall again in 2024, the company will become increasingly reliant on clinical trial updates to drive its share price upward, so these infectious disease study updates will be vitally important in 2023.

It's tough to know what the markets would look like if BioNTech can deliver improvements on current standards of care, but I would estimate $3 - $5bn for malaria / shingles combined, and also estimate that BioNTech would be unlikely to capture a >25% share.

Rolling these opportunities together - let's a say a potential 10% share of an influenza market, and 25% share of shingles and malaria, my takeaway would be there is a ~$2.5bn opportunity in play, but that approvals in any of these diseases are 2-3 years away at least.

3 - What's The State Of Play Within BioNTech's Oncology Division

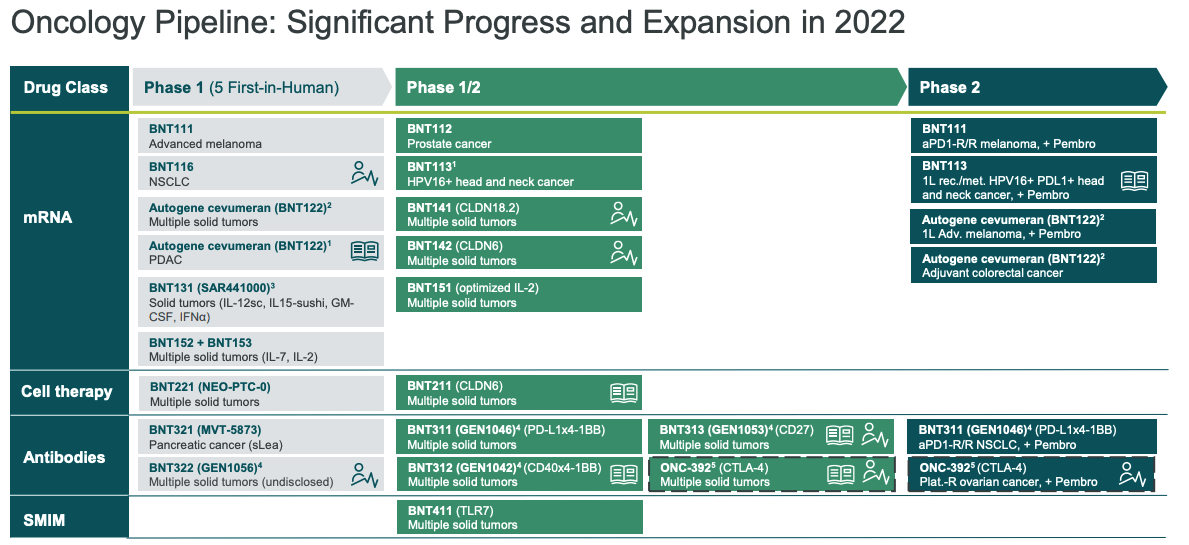

The sheer size and scale of unmet need in oncology makes the market opportunity huge, and BioNTech is casting its net wide, looking at four different classes of drug, as shown below.

{kind=link}

Once again, in the mRNA space BioNTech is competing with Moderna, which has teamed up with Merck ( MRK ) and its cancer wonder drug Keytruda to design personalized cancer "vaccines" for patients - attempting to stimulate a greater immune response - and have had some initial success in melanoma .

BioNTech is not far behind in PCVs - it too is working with pembrolizumab - Keytruda - in melanoma, and head and neck cancer. BioNTech in general has a more diverse oncology pipeline than Moderna, although there has been much in the way of clinical data released to date.

The high point is probably the objective response rate ("ORR") of 57% and Disease Control Rate ("DCR") of 85% generated by CAR-T cell therapy BNT211 in testicular cancer which was presented last year at ESMO.

Nevertheless, CSO Richardson sounded bullish on oncology during the earnings call, telling analysts:

we plan to initiate multiple registrational trials in the next 12 to 18 months. In parallel, we plan to accelerate the build-out of our oncology commercial capabilities in 2023 and 2024 with the goal of commercial readiness in the United States, EU and other selected regions, to support first oncology launches from 2026 onwards.

We anticipate further M&A and/or product candidate in-licensing will further complement our organic pipeline with synergistic programs. Finally, we expect several pipeline updates from our oncology pipeline in 2023, including from our individualized cancer vaccine program in first-line melanoma, BNT122, our CLDN6 CAR-T program, BNT211, and from several of our next-generation checkpoint programs, including BNT311 and BNT312.

Frankly, given BioNTech is investing $2.7bn in R&D this year, it says, it needs to justify that outlay this year with some positive data readouts. These could become major price catalysts for the company's shares as a successful cancer drug can generate $5 - $10bn per annum in revenues in just a few years.

With that said, most of BioNTech's candidates tend to be adjunctive to other drugs, such as Keytruda, like its antibodies which are being evaluated in Non-small cell lung cancer ("NSCLC") and Ovarian cancer alongside Pembro.

With its funding and ability to invest in M&A - which management says it is prepared to do - BioNTech has a great chance to assume a leading position in oncology - I would tentatively compare it in terms of potential, if not revenues, to Seagen ( SGEN ), which has just been acquired by Pfizer ( PFE ) for ~$43bn.

4 - How Can BioNTech Usefully Deploy Its >$14bn Of Cash

Speaking of M&A, BioNTech's profits have been verging on the obscene for the past couple of years and the company now has a war chest of >$14bn to spend however it sees fit.

An R&D budget of nearly $3bn per annum can potentially be supported long term by revenues from a private COVID vaccine market of ~$5bn per annum - although there's a risk as mentioned that no such market will emerge - which suggests BioNTech has money to burn.

$0.5bn has apparently been earmarked for a share repurchase program during 2023 - good news for shareholders since BioNTech does not pay a dividend - leaving as much as ~$10bn for M&A I would estimate. Frankly, I do not see BioNTech - a company which prides itself on its proprietary tech - spending much more than $1bn on a deal, so deals for bolt-on technologies as opposed to commercialized assets are likely to be pursued.

Unless you're an industry insider it is likely going to be tough to assess the value of such acquisitions - they may feel unnecessary to some shareholders - but they will simply have to trust that the team responsible for developing Comirnaty knows what it is doing when it comes to its first love - oncology.

5 - What Will BioNTech's Valuation Look Like in 1, 5 and 10 Years' Time

I will end with the key question for prospective or existing buyers of BioNTech stock - where is the share price headed?

Actually, after a period of almost inconceivable volatility, which has seen BioNTech valued at >$85bn based on a single commercial product, I think BioNTech stock may trade fairly steadily for the next 3-5 years at least.

There are several reasons for this. Firstly, nobody knows what a commercial COVID market might look like, but you can bet your bottom dollar there will be a great deal of speculation, and while there's a potential $20bn market in play, there will be a reluctance to sell out of BioNTech stock given its fabulous COVID track record.

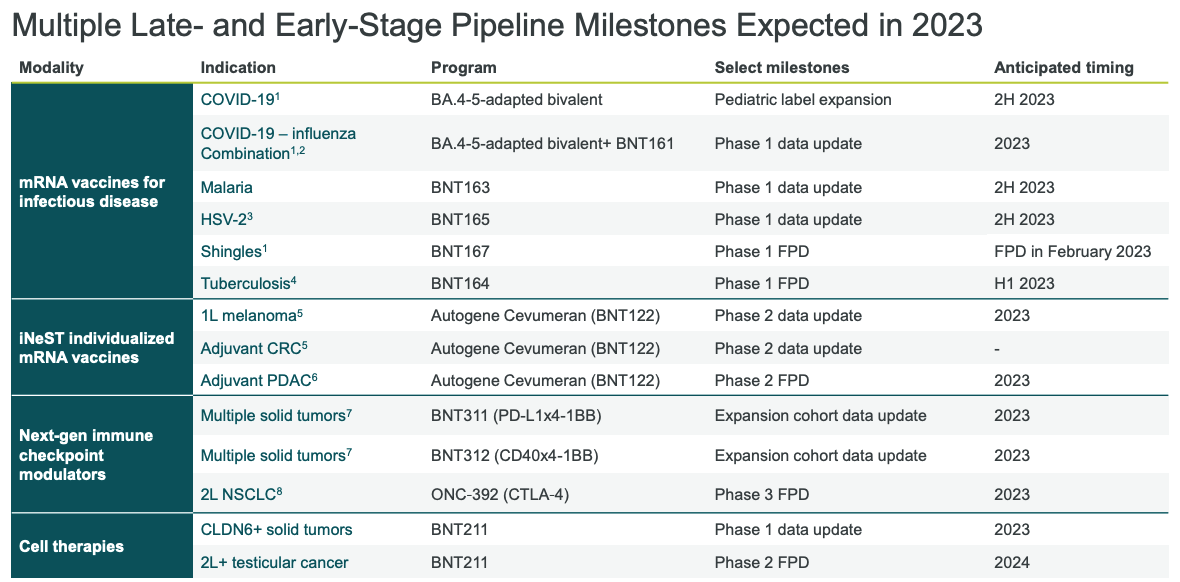

Secondly, BioNTech is much more than a COVID vaccine developer. Although I would not say that either its infectious disease or oncology franchise is thriving, as commercialization still looks a long way away, the breadth of data readouts the company has planned for 2023 is impressive:

{kind=link}

I would expect to see a similar volume of readouts in 2024, 2025, and so on, with the increased probability of commercialization towards the end of the decade also keeping investors and the market interested.

Finally, BioNTech stock has the cash to pivot its R&D projects if needs be, and add whatever bolt-on technologies it may need using its huge pile of cash.

For all these reasons, I suspect that stability will be the name of the game for BioNTech over the coming weeks, months, and years. That does not mean there will not be catalysts and price spikes - these may arrive with regulatory milestones, but the days of an $85bn market cap are long gone.

Nevertheless, I will conclude by saying that I like BioNTech stock at ~$124 per share, and a market cap of $31bn. I'm not expecting wild fluctuations in the share price, and the lack of dividend adds an element of risk not shared by larger pharmas , which have dividends that typically yield >2.5%.

The breadth of opportunities, management's track record, the market opportunities and the abundance of cash however suggests to me BioNTech's share price will trade up rather than down for the foreseeable future, with inevitably a few bumps in the road.

Gazing into my crystal ball, and acknowledging plenty of uncertainty, I can see BioNTech's valuation creeping higher than e.g. Seagen's acquisition price of $43bn before the end of the decade.

For further details see:

BioNTech FY22 Earnings Review - 5 Questions Answered After Today's Results