ARCC - BIZD: Top Of The Capital Structure Is The Best Seat In The House During A Recession

2023-04-28 06:49:50 ET

Summary

- We want to be ready if a recession comes, but we don't want to sacrifice income or pay a heavy "opportunity cost" if the long-awaited recession fails to happen.

- Best of both worlds: Senior, secured corporate loans sit at the top of the balance sheet, protected even during economic downturns, but paying us 10%-plus yields while we wait.

- Business Development Companies specialize in making these loans but are less leveraged and more liquid than banks (not subject to "runs").

- VanEck BDC Income ETF provides convenient, diversified exposure to the best of the BDC market.

- It also pays us 11.7% while we sleep well at night, whether or not a recession occurs.

Top Of The Capital Structure:

Best Seat in the House for a Recession

Let's face it. We've been preparing for a possible recession for the past year, and the economy has actually stayed flat or improved marginally.

But the risk still remains , especially with all the uncertainties we face: economically, financially, geopolitically. So it is no time to blow the "all clear" whistle.

What are investors to do if they:

(1) Need income and can't afford to go running into cash or totally "safe" (i.e. low-yielding, unproductive) assets every time some journalist or media guru says "the sky is falling" (again),

(2) But still need to protect themselves from the recession or economic downturn that remains a very real possibility?

We all know there are traditional ways to hedge against the risk of recessions or downturns. But so often they involve buying assets like longer-term, low-yield bonds that lock in losses if the recession does not occur; or involve moving to cash and then leaving ourselves "on the platform watching the train pull out of the station" if the market decides to recover and take off without us.

Fortunately, we can have it both ways , if we select an asset class that pays us well during good times when there is no recession or downturn, but can actually pay us even better during challenging economic times.

One such asset class is corporate credit , especially Business Development Companies ("BDCs"), which are companies that specialize in lending to middle market corporations. BDCs are similar to commercial banks, but with fewer of the risks. First of all they are not nearly so leveraged. Whereas the typical commercial or investment bank may be leveraged 10 to 1 or more, BDCs are limited by law to leverage of 2 to 1, and most are well below that limit. They also typically fund themselves by issuing bonds and notes, or through credit lines from banks, so they do not have depositors and are therefore not subject to potential "runs on the bank" the way commercial banks are (as we have seen recently).

What BDCs do have are loan portfolios consisting mostly of senior, secured corporate loans to middle-market companies. These are loans that sit at the very top of the issuer's capital structure, and are secured by collateral, in most cases virtually all the assets of the company, including intangibles like trademarks, etc. That means if the company defaults on its loan, the BDC lender is in the driver's seat in terms of controlling the workout of the loan and getting paid first from the disposal of the assets, or in most cases, the reorganization and/or sale of the borrower. The loans are also floating rate, which means their interest rates are adjusted regularly as interest rates move up and down, which reduces risk and makes a BDC's income more predictable.

"Secured" = High Recoveries, Lower Credit Losses

The impact of collateral security makes a huge difference for a corporate lender. The financial media, in its constant effort to attract viewers and readers, continually refers to projected levels of corporate "defaults" when discussing the possibility of recessions and economic downturns. While default rates are a useful data point, they hardly tell the whole story.

When a company defaults on its loans, bonds or other obligations, the senior, secured lender (usually a group of banks, like BofA, Citibank, JPMorgan, etc. or a BDC) generally steps in first and enforces its rights to its collateral. This means in most cases the company is reorganized or sold, or the assets (real estate, manufacturing facilities, etc.) are otherwise sold off to third party buyers. On average, based on statistics collected over many decades, the secured lenders recover about 65-70% of their principal. That means their losses, on average, are about 30-35%.

So when we see a headline "default rate" of, say, 5% (which is much higher than most economists have been predicting the default rate would be even if we have a recession in the next year or so), the projected losses to secured lenders would be 35% times 5%, since the 5% of the loans that defaulted would lose, on average, 35% of their principal. Therefore the overall portfolio loss would be 35% X 5% = 1.75%. Obviously that's a lot less than 5%, and if you were collecting 10% in interest on your portfolio, a loss of that size would take your income down for that year from 10% to perhaps 8%, which would not be much of a hit considering there would be a recession going on. (In other words, while the BDCs' income might be down from 10% to 8%, imagine the bloodshed in the equity markets.)

The story gets even better when you consider that credit markets, in the months leading up to a possible recession or downturn, as well as during it, invariably jack up the cost of credit across the board, often over-compensating investors for what a realistic estimate of credit losses might be (one colleague in the private credit market has called it the "worry discount ").

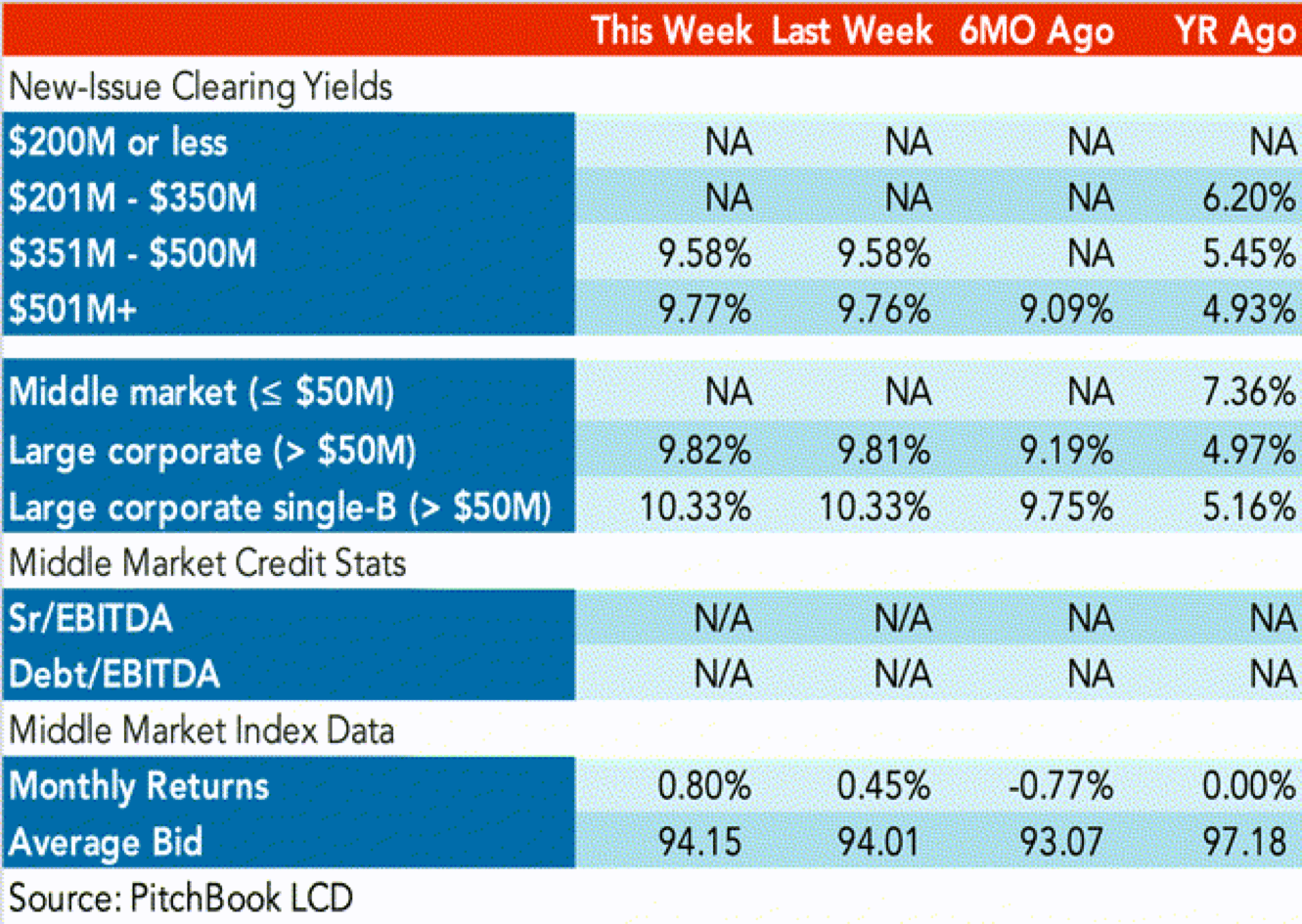

You can see the latest variation of the "worry discount" in this table showing recently issued corporate loan prices versus where they were a year ago. Notice in the 4th line down that new-issue clearing yields for large corporate loans averaged 9.77% recently, versus yields of about half as much (4.93%) a year ago. Smaller corporate loans, a few lines lower, that were paying only 5.16% one year earlier, were recently being priced at 10.33%. Some of this obviously offsets the increase in the underlying base interest rates from a year ago. But some of it is also over-compensation for the market's skittishness about credit risks. Credit risks that, while undoubtedly higher than previously due to the risk of a downturn or recession, are still modest compared to the gross margins currently available, and are capable of being modeled and managed by professional credit investors.

{kind=link}

Tapping the Professional, Private Credit Market

VanEck BDC Income ETF ( BIZD ) is my vehicle of choice for tapping the BDC market. BIZD holds a well-diversified portfolio of the "who's who" of business development companies. Here are BIZD's top 10 holdings, which comprise 75% of its total assets:

Ares Capital ( ARCC ) 20.12%

FS KKR Capital Corp. ( FSK ) 13.36%

Owl Rock Capital Corp. ( ORCC ) 11.92%

Blackstone Secured Lending Fund ( BXSL ) 4.81%

Main Street Capital ( MAIN ) 4.66%

Golub Capital BDC ( GBDC ) 4.65%

Prospect Capital Corp. ( PSEC ) 4.50%

Hercules Capital Inc. ( HTGC ) 4.07%

Goldman Sachs BDC ( GSBD ) 3.62%

Sixth Street Specialty Lending Inc. ( TSLX ) 3.57%

Total of Top 10 75.28%

Total# of Holdings 26

[Holdings as of 2023-04-22 per Seeking Alpha]

Besides the fact that the great majority of all the assets held by these firms are senior secured corporate loans with all the advantages previously discussed, we should also note that their sponsorship and management include some of the best known and most highly respected credit shops and asset managers on Wall Street, including Goldman Sachs, Blackstone, KKR, Ares, Owl Rock.

But not only do they have big names managing them, they also have some serious institutional heavy hitters among their ownership ranks. I always like to invest alongside of major institutions managed by people who invest millions of dollars every day for a living. The BDC business, for the various reasons we've mentioned - stability of earnings, lots of risk diversification, well-secured assets, etc. - is very popular with institutional investors, like major Wall Street firms, state pension funds, college endowment funds, etc. The average institutional ownership percentage of the top ten BIZD investments is 33%.

BIZD Performance

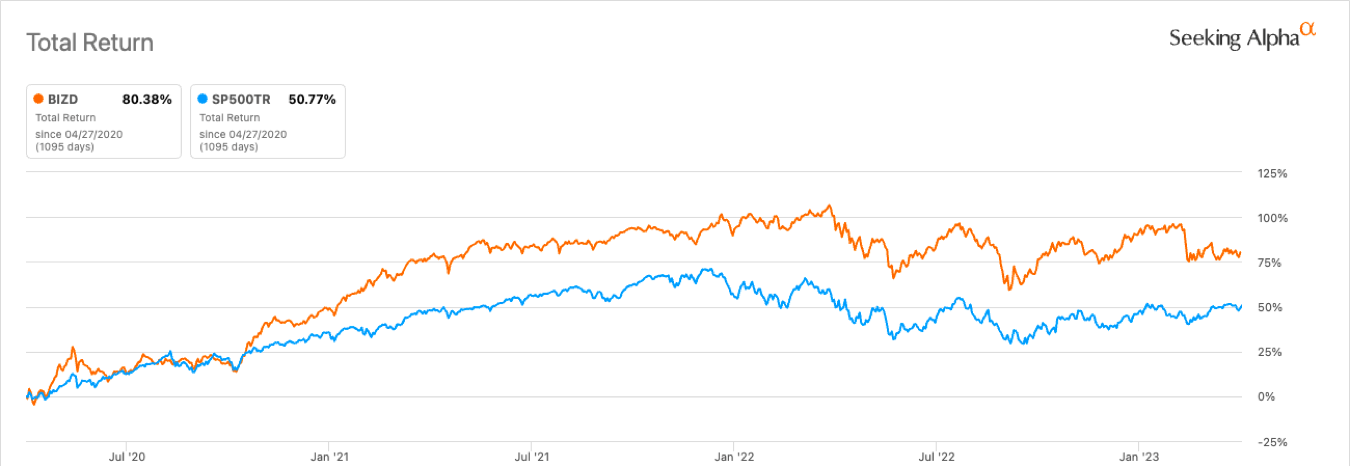

As noted on its website , BIZD has had a total return of just over 6% annually since its inception in 2013, reflecting mostly the low interest rate environment during much of the early part of the past decade. But its total return has been 8.5% per annum for the past 5 years, in spite of some challenges (like the Covid crash) during that period; and for the past three years it has averaged 29% per year, with a robust 4.8% return for the first quarter of 2023.

{kind=link}

This chart shows how BIZD has done over the past three years (since just after the Covid crash), actually beating an investment in the S&P 500 ( SPY ).

An even bigger difference is that throughout this volatile period BIZD investors also may have slept better at night collecting their high cash distribution (currently 11.8%), while SPY investors collected their 1.5% yield as they waited (and are still waiting) for the market to recover.

When or if a recession eventually comes, BIZD investors (or investors who may choose to invest directly in the BDCs named above, which is an equally valid strategy), should be in a good position to ride out the storm while continuing to "create their own growth" by reinvesting and compounding their generous dividends; knowing they are reasonably well-protected by collateral and by their position at the top of the capital structure.

Besides BIZD and its constituent holdings of BDCs, investors looking for other ways to tap into the protection and all-weather stability of senior secured corporate loans may also wish to consider closed-end funds that invest in this asset class. Some funds with excellent management and good records in this category, that are also paying attractive dividend yields and selling at discounts, include: Ares Dynamic Credit Allocation Fund ( ARDC ), 11.3% yield, 12.9% discount; Invesco Senior Income Trust ( VVR ), 12.6% yield, 8.2% discount; and Apollo Tactical Income Fund ( AIF ), 11.9% yield, 13.7% discount.

Editor's Note: This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

BIZD: Top Of The Capital Structure Is The Best Seat In The House During A Recession