IBM - BlackBerry: Breaking Up Is Hard To Do

2023-10-12 01:03:22 ET

Summary

- BlackBerry will spin off its Internet of Things segment.

- Investors are waiting to hear key financial details of the transaction.

- The move could create value with shares trading like a distressed asset.

Perhaps the most disappointing name that I've covered in my more than a decade of writing on this site has been BlackBerry (BB). The Canadian technology firm has seen its shares lose a tremendous amount of value despite overall markets soaring. The main culprit has been a failed transition from a once-leading hardware firm to one based on software and services, which has gutted the company's revenue base. Last week, BlackBerry announced a plan to separate its two major business segments , a move that could potentially be a turning point in the company's history.

I've long been neutral or bearish on BlackBerry, with the main reason being management's inability to execute a long term plan. Next month will mark ten years since John Chen took over the company, and one could argue that the company is in its worst spot ever. Last month, BlackBerry issued another large revenue warning , setting up this fiscal year to see the lowest revenue figure reported under Chen's leadership. He failed to transform the company's device business in his early years, and a number of questionable acquisitions since have wasted billions in precious capital.

Last week, the company announced that it will IPO its Internet of Things ("IoT") segment. The target date is the first half of the next fiscal year, which means by the end of August, but those following this company know that holding to timelines has not been a great strength at this name. Each business will be allowed to pursue its own distinct strategy and capital allocation policy, although it probably will be a few quarters before we see the exact terms of the entire transaction.

Investors in the technology space have become more used to these types of moves in recent years. Service and technology giant IBM ( IBM ) spun off its managed infrastructure services business, becoming Kyndryl Holdings ( KD ), while we saw chip giant Intel ( INTC ) go with an IPO of its driver assistance segment Mobileye ( MBLY ). So far, Kyndryl shareholders have seen their shares lose quite a bit of value, while Mobileye has nearly doubled from its IPO price.

The IoT segment is the crown jewel of BlackBerry currently, as it is the one segment showing decent long term promise. The company has touted a number of design wins for its driver assistance and vehicle software packages in recent years, which should become more widely used in the future. BlackBerry's new Ivy platform will also look to take advantage of the massive amounts of data used in today's more technologically advanced vehicles.

{kind=link}

Management recently reduced the yearly revenue forecast for the segment to a range of $225 million to $240 million. However, that's still decent growth from the $130 million reported three fiscal years earlier. The top line should continue to grow moving forward, with BlackBerry reporting a QNX backlog of $640 million at the end of the most recent fiscal year. I will be most curious to see how the complete financial picture breaks down once this part of the business is taken away from the whole.

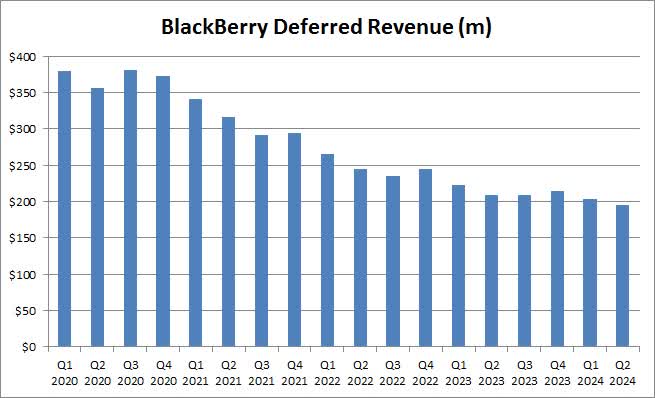

At the moment, I have a lot less faith in the company's cybersecurity segment. This division has seen its revenues plunge in recent years, going from nearly half a billion dollars a few years back to likely under $400 million during the current period. Worse yet, recurring revenue here has dropped from $364 million to $279 in the past two years, with the net retention rate barely holding above 80%. This segment is also the lower gross margin one when compared to IoT, and it is highly reliant on government contracts that don't always close when hoped. The disappointment here is the main reason why investors have soured on the name so much. As the chart below shows, deferred revenue which can be an indicator of future revenue progress, has continued to decline almost every single quarter.

{kind=link}

The details of the transaction will also be important when it comes to BlackBerry's capital structure moving forward. The company finished its latest quarter with about $150 million in net cash, which is after including the company's debt to be paid back next month. Earlier this year a large group of patents was sold off , so there could be more cash coming in from that deal over time. However, there is limited financial flexibility here, and BlackBerry's ongoing losses are leading to some cash burn right now.

The reason that this proposed transaction could have a positive outcome for shareholders, in the long run, is because BlackBerry currently trades like a heavily distressed asset. Using just half of Mobileye's price-to-sales ratio for expected 2024 revenue, a 6X multiple for the IoT segment at $250 million in annual revenues gives you a $1.5 billion value. That leaves about $600 million for the rest of BlackBerry, which gives you about 1.5 times ongoing full-year revenue, which is a small fraction of the roughly 11 times sales that a key competitor like CrowdStrike (CRWD) goes for. Of course, BlackBerry doesn't have the overall growth profile, profits, or cash flow of those two other names, but that's significant discounts just to get to the company's current value.

I do think there is some potential in the long run for the IoT segment, as that is the one division of the two I'd be more interested in buying. However, I can't quite recommend buying BlackBerry as a whole today for three reasons. First, we really need to see the key details of the transaction, because dividing up the overall financials is a critical part for investors. The second reason is that BlackBerry really needs a capital raise to improve its balance sheet, so I need to see how much new money would be coming in here. Finally, overall results have been quite weak in the past few quarters, so I can't recommend buying the stock unless management shows things are starting to improve as we head into calendar 2024.

In the end, BlackBerry announced last week that it will be spinning off its IoT segment, a move designed to create more value for shareholders. This division is the company's crown jewel, showing decent growth currently and seemingly having a bright future. Shares have not reacted well to the news, as investors want to hear key details of the transaction, and weak cybersecurity revenues continue to weigh down overall results. This might be a good move for the company in the long run, but this management team has found a way to disappoint investors time and time again, so I can't recommend the stock just yet.

For further details see:

BlackBerry: Breaking Up Is Hard To Do