TSVT - Bluebird Bio And 2seventy Bio -- Spinner And Spun: The Better Bet In Cell Therapy

2023-09-15 18:46:28 ET

Summary

- Bluebird bio and 2seventy bio are struggling as small biotechs in the challenging field of cell therapies.

- Bluebird has a longer history as a public company and has established itself as a gene therapy leader with FDA-approved therapies.

- Both companies are facing financial difficulties, but Bluebird has a more promising pipeline of FDA-approved gene therapies.

This is my first look at a pair of cell therapy hopefuls, bluebird bio ( BLUE ) and 2seventy bio ( TSVT ); the two have several FDA approved cell therapies with PDUFAs pending for both. In this article I report how these two small biotechs are struggling as they punch well above their weight in the challenging field of cell therapies.

Now that the deal has closed and both have an operational history as independent companies, this article assesses the situation. It identifies which of the two, bluebird — spinner or 2seventy — spun, is a better investment bet as I write on 09/14/23.

To be sure these are not the halcyon days for gene therapy. Those days are best exemplified by:

- Gilead's ( GILD ) 08/2017 $11.9 billion acquisition of Kite; I discussed its Kite deal in "Gilead: The Kite Cure ";

- Celgene's ( CELG ) 01/2018 $9 billion acquisition of Juno ( JUNO ) and

- Bristol Myers ( BMY ) ~$74 billion acquisition of Celgene

Interestingly Gilead's Kite subsidiary has been rather successful in achieving FDA approvals for its gene therapies over the years. The challenges have been in scaling the business as I discussed at some length in "Gilead's Cancer Follies". In some ways it's a foreshadowing of the experiences to date of bluebird and 2seventy.

Shareholders in bluebird have had quite a ride over its decade+ as a public company

Bluebird went public in 06/2013 with an initial public offering price of $17.00 as a gene therapy startup focused on severe genetic abnormalities. It has experienced two raucous peaks in its sales price over its ~decade long existence as a public company. It first peaked over $127 in 05/2015 on a buoyant market and hopes that it held the key to curing rare diseases.

It quickly fell back to close <$25 in 05/2016. Having thoroughly collapsed, it soon started to rise again. It peaked in 03/2018, trading briefly >$150 as cell therapy deal enthusiasm ramped. Its subsequent trading has been heavily dampened, skewing largely towards the negative as shown by its chart below:

Bluebird trades at a mere ~$3.33 as I write on 09/14/2023.

As reported by CEO Leschly during its Q2, 2023 earnings call (the " bluebird Call "), bluebird has a had a productive initial decade as a public company. It has established itself as a gene therapy leader:

... proving ... [its] clinical, regulatory and commercial capabilities. Clinically, we have the longest and most robust gene therapy program in the field with over 180 patients treated across eight clinical trials with up to nine years of follow-up and over a decade of gene therapy research. We have an established regulatory track record with two FDA gene therapies on market and the third BLA currently under priority review.

How is it that it has been so ostensibly successful in its business and yet so awful for its shareholders? Therein lies a tale.

In 01/2021 bluebird elected to separate its oncology business into independent company.

Bluebird management was apparently all atwitter as calendar year 2020 wound to a close. They hatched a plan to divide the company in two pieces:

- a severe genetic disease [SGD] business [SGD], under existing president of SGD Obenshain who will become CEO of bluebird bio, initially focusing on core therapies in treatment of ?-thalassemia, sickle cell disease ("SCD"), and cerebral adrenoleukodystrophy ("CALD") and

- oncology focused genetic disease business [subsequently named 2seventy bio] under the leadership of CEO Nick Leschly, who will move from his current bluebird bio CEO role focusing on idecabtagene vicleucel (ide-cel), in multiple myeloma and continued development of bluebird's oncology pipeline and investigational therapies.

After announcing the plan to spinoff its oncology business on 01/11/2021, bluebird bio announced that the spinoff was complete on 11/04/2021. During the intervening period bluebird's shareholders were roughed up as shown by its chart below:

Its spinoff, 2seventy began regular trading on the NASDAQ exchange on 11/04/2021. It had a crazy opening day. It started trading at ~$17.25. It shot up to a high of ~$64 settling back to close at $26.65, all on volume of ~43,900.

Subsequently its volume picked up by factors of between ~5X and 50X to a more normalized daily trading volume. Its share price has never come close to its opening day high. Its closing price for the bulk of 2022 has been in the low to mid teens.

FDA interactions have been eventful for both spinner (bluebird) and spun (2seventy).

bluebird pre spin FDA approval

On 03/26/2021 the FDA approved ABECMA (idecabtagene vicleucel; ide-cel) in fifth line treatment of adult patients with relapsed or refractory multiple myeloma. Bluebird had a longstanding co-promotion and profit-share agreement with Bristol Myers Squibb ( BMY ) for ABECMA. In 05/2020 Bristol amended the deal to buy out its ex-U.S. milestone and royalty obligations to bluebird bio for $200 million

The spin-off effected a transfer of ABECMA and the Bristol collaboration to 2seventy. The excerpt below from 2seventy's Q2, 2023 earnings presentation slide 4 describes its current role:

{kind=link}

seekingalpha.com

bluebird post spin — BLA and FDA approvals

Bluebird quickly made up for the loss of its only FDA approved therapy in the spinoff by scoring two FDA approvals in quick succession:

- 08/2022 approval of Zynteglo (betibeglogene autotemcel, beti-cel) approved as a one-time potentially curative gene therapy for patients with beta-thalassaemia who require regular blood transfusions

- 09/2022 approval of Skysona (elivaldogene autotemcel), or eli-cel to slow the progression of CALD, a rare paediatric neurodegenerative disease in boys aged 4–17 years diagnosed with early-stage CALD.

Additionally the FDA accepted its BLA for nlovotibeglogene autotemcel (lovo-cel) in treatment of certain patients with SCD, setting a 12/20/2023 PDUFA date.

2seventy post spin — FDA sBLA

Unlike bluebird, 2seventy has no new approvals to boost its forward potential. It does have an important supplemental application pending with a 12/16/2023 PDUFA date. If the FDA grants its approval, ABECMA will move up from a fifth line therapy approved to treat patients who have failed four other regimens, to a third line therapy.

This would substantially boost ABECMA's market potential.

Despite successes with FDA, bluebird and 2seventy bio are both struggling financially.

bluebird finances

As one might well surmise from bluebird's price chart above, it has not shown much good news from a financial perspective. The following excerpt from its 2023 10-K results of operations (p. 79) shows how abysmally awful it has been for calendar years 2021 and 2022:

seekingalpha.com

During the bluebird Call it issued guidance setting out its expectations for the balance of 2023. It set out its liquidity at end of Q2, 2023 as $291 million in cash, cash equivalents, marketable securities and restricted cash. It anticipates this as providing it a runway including restricted cash into Q4, 2024.

It expects a cash burn in the range of $270 million to $300 million as it launches ZYNTEGLO and SKYSONA and prepares for the launch of lovo-cel. If it is unable to free up its restricted cash, its runway runs out in Q2, 2024. With a cash burn at its midpoint of $285 million perilously close to its liquidity, I have to question whether it truly has a runway beyond Q2, 2024.

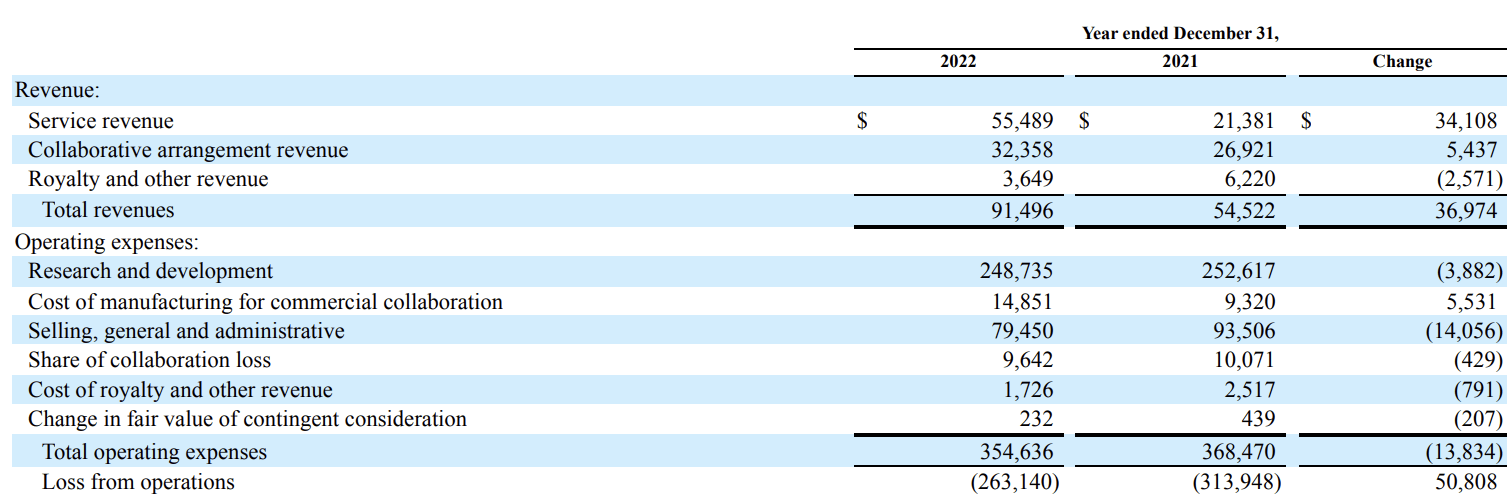

tseventy finances

While bluebird is in the process of launching two and possibly a third newly approved therapy, 2seventy is further down the line with its ABECMA. Plus it has a big pharma partner helping it out, albeit at a heavy cost of half of its profits.

Its loss from operations for years 2021 and 2022 as shown by its 2023 10-K is not all that different in terms of order of magnitude from bluebird's:

{kind=link}

seekinalpha.com

The revenue line for 2seventy is more substantial than is bluebird's. It consists of the following:

- share of commercial profits from ABECMA sales;

- collaboration revenue with partners such as Regeneron, and

- service revenue from collaboration and license agreement with Novo Nordisk, reimbursement by Bristol related to performance of services for ABECMA that benefited ex-US geographies under collaboration agreement.

A healthy chunk of 2seventy's 2022 services revenue of ~$36 million was non recurring.

In terms of guidance, 2seventy presents a tough picture. During its Q2, 2023 earnings call (the "tseventy Call"), CFO Baird spoke of its commitment to maintain a cash runway into 2026. This appears to rely upon grant of approval for its sBLA to move ABECMA up to a third line treatment.

In response to an analyst question on the 2026 runway during the tseventy Call, CEO Leschly acknowledged that his answer might not be entirely satisfactory. Indeed the company's 09/12/2023 press release advising of a major restructuring, reflects a major shift in focus.

The restructure will include:

- resignation of CEO Leschly who will move to role as chairman of its board of directors upon appointment of a successor CEO;

- cutting 40% of its workforce;

- rigorous efforts to right-size facilities and related external spend by 2025 to better reflect current needs;

- annual savings of ~$65 million.

Both bluebird and 2seventy pose substantial risk of loss of investor capital.

A quick look at their stock charts should disabuse anyone who has any doubts about the risks inherent in these two unproven microcap biotechs:

[object HTMLElement]

Both of these companies are bleeding cash at prodigious rates. Neither has a proven path to reverse course.

Conclusion — why I prefer bluebird to 2seventy.

Both bluebird and 2seventy are speculative bets. Each is waiting on the FDA to decide on outstanding PDUFA's. Both are losing copious amounts of cash on a regular basis. To its credit, 2seventy is addressing its financial distress with a major restructuring. No such program appears in the offing for bluebird.

My preference for bluebird lies in its superior prospects. It appears to be building a solid phalanx of FDA approved gene therapies. On the other hand 2seventy looks to be a one trick pony for the foreseeable future. Indeed given its sharing arrangement with Bristol one might more accurately characterize it as a half trick pony.

For further details see:

Bluebird Bio And 2seventy Bio -- Spinner And Spun: The Better Bet In Cell Therapy