BVHBB - Bluegreen Vacations: Not Taking This Vacation

2023-09-25 17:59:26 ET

Summary

- BVH has been on an expansion spree and has been focusing on growing its own receivables portfolio.

- Default rates have been steadily increasing skirting the 10% mark currently and could lead to further challenges.

- We initiate at Neutral as current multiples do not provide any margin of safety with potential of more downside risks going forward.

Investment Thesis

Bluegreen Vacations Holding ( BVH ) had a significant run so far with its share price climbing about 80%, significantly outperforming its peers driven by its continued expansion spree.

Its robust gross margin upwards of around 85% along with a recurring revenue profile bodes well for the company's overall business model. However, we believe its increasing shift to focus on growing its own receivable portfolio can be potentially risky particularly due to its exposure to a relatively middle to high income class consumer and the current macro environment can push up default rates which has already been rising. We believe the valuation is not attractive and believe there could be potential downside risks going forward. Initiate at Neutral.

Company Background

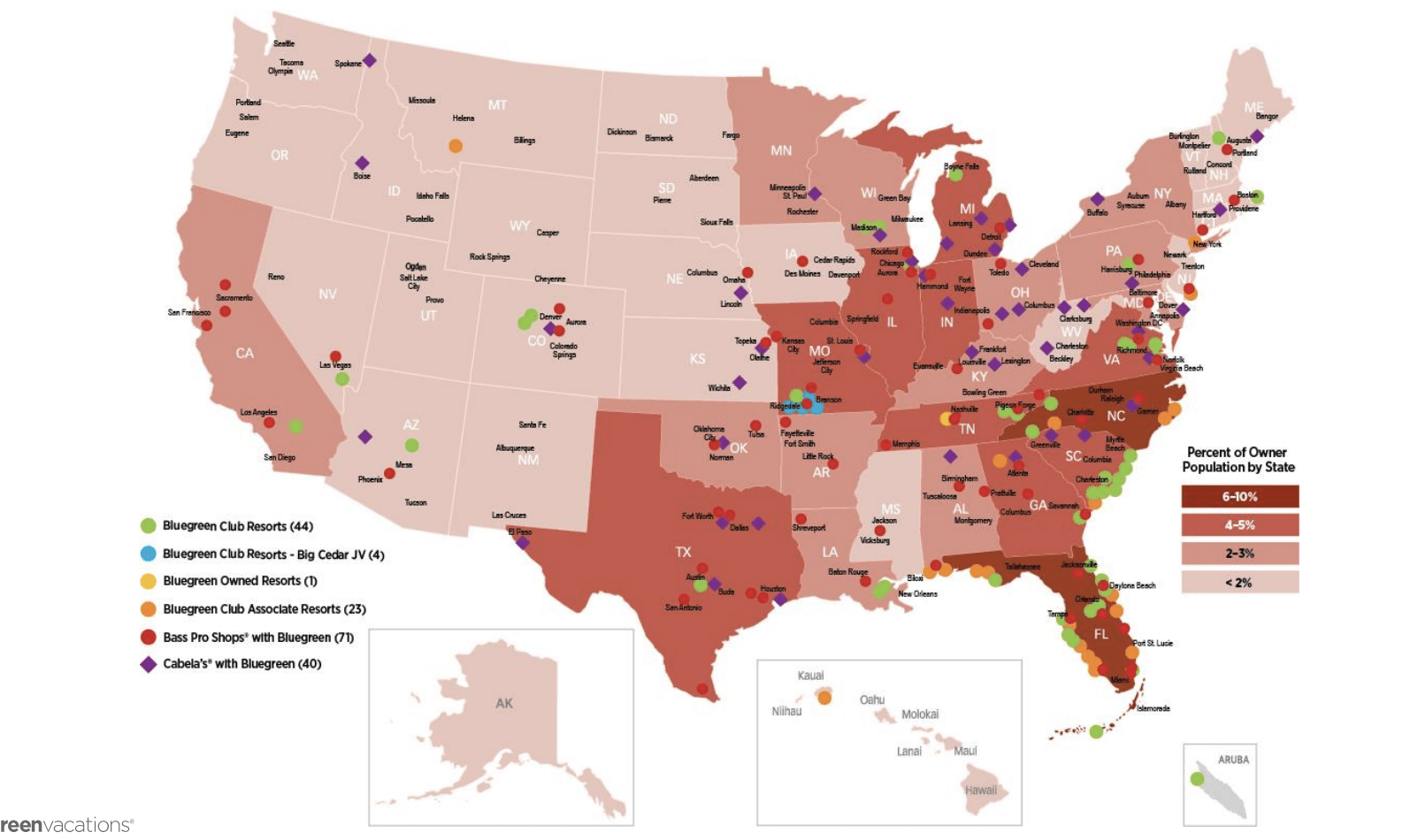

Bluegreen Vacations Holding ((BVH)) is engaged in marketing and selling of vacation ownership interests and managing resorts across several destinations. It has a network of 48 resorts (where owners have right to control most units) across different states in the US as well as 23 Associate resorts (where owners have limited right to use the units) as well as access to over 11,400 hotels through various partnership arrangements. It also has marketing agreements with Base Pro and Choice Hotels which enables them to attract prospective customers and sell vacation packages.

{kind=link}

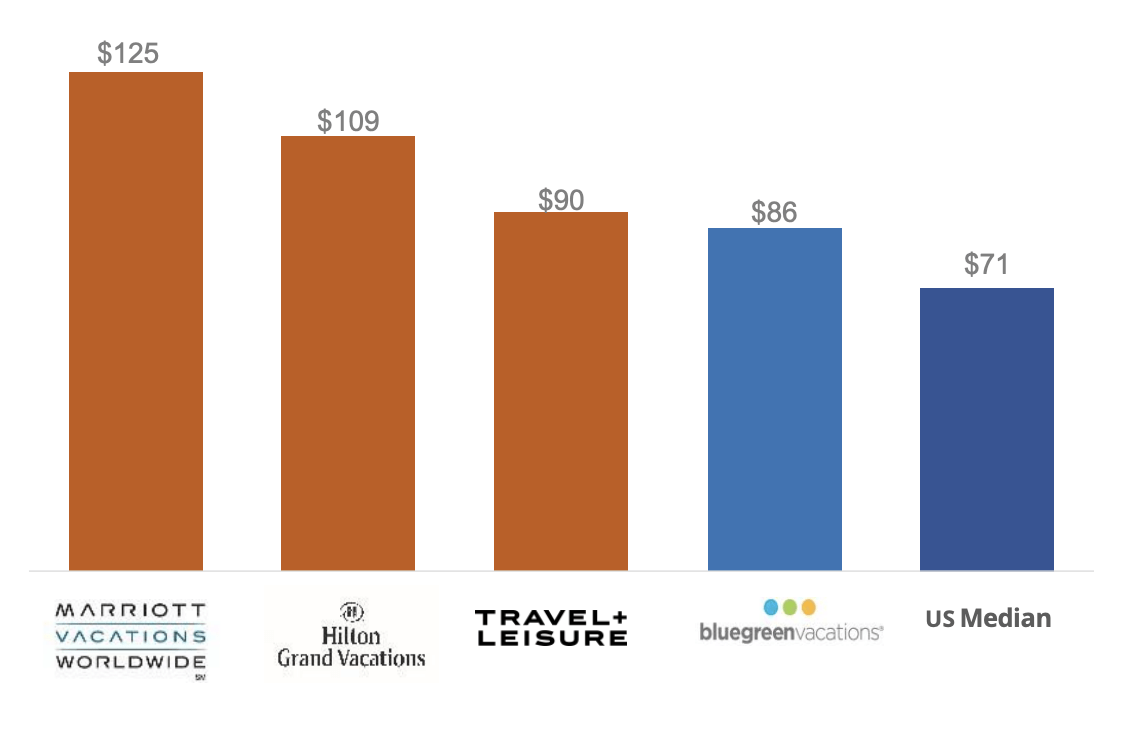

Its customer base remains at the bottom of the pile compared to its peers with average customer household income of $86k, higher than the US median.

Average customer household income

{kind=link}

Historical Track Record

BVH reported a steady growth prior to pandemic with revenues growing 6.3% CAGR during the 2015-19 period, before COVID-19 jolted travel and vacation industry during 2020 and 2021, but it swiftly recovered with 2022 revenues nearing its pre-COVID levels.

| Particulars ($ mn) |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Revenue |

| 741 |

| 820 |

| 869 |

| 946 |

| 947 |

| 520 |

| 757 |

| 919 |

| Adj. EBITDA |

| 132 |

| 138 |

| 150 |

| 142 |

| 122 |

| (13) |

| 122 |

| 140 |

| % margin |

| 18% |

| 17% |

| 17% |

| 15% |

| 13% |

| NM |

| 16% |

| 15% |

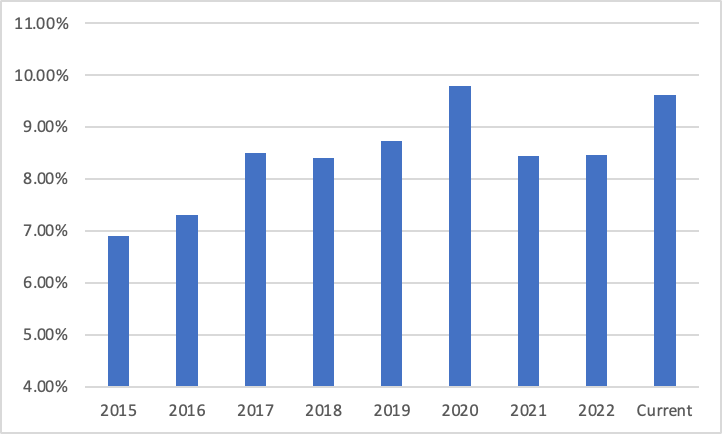

It reported a steady increase in its default rates during the 2016-2019 period as a result of class action lawsuit from the owners beginning 2016 against Bluegreen for allegedly misleadingly marketing and sales tactics without fully disclosing the details of their timeshare contract. Several owners of the timeshare property increasingly defaulted to get released from the contract during the period which created an adverse impact on Bluegreen's operations. Along with that, COVID led to a jump in the default rates which came down significantly as the pandemic restriction eased and the lawsuit being voluntarily dismissed in 2022 .

{kind=link}

Q2 Earnings Corner

BVH reported a steady Q2 with system-wide sale of VOIs up 1% YoY on the back of a 1% uptick in guest tours while sales volume per guest remained flat. Total revenue grew 11% YoY driven by an increase in interest income on the back of rising interest rates along with a 63% jump in cost reimbursements (which is essentially a pass-through) partially offset by a decline in sales commission revenue due to its focus on selling Bluegreen owned VOIs. The revenue growth slowed from the 13% growth it experienced during Q1 2023 and a 22% increase in Q2 2022 last year. Interest expenses spiked up over 70% as a result of an overall rising interest rate scenario. Provision for loan losses increased 80 bps as a result of higher proportion of VOI sales financed as the company continue to grow its own notes receivable portfolio. This is potentially quite risky given the current tough macroeconomic backdrop as the provisions for bad loans spiked up to $19 bn for US banks jumped 75% YoY and 17% QoQ, a three-year high when COVID-19 was ravaging the economy. In addition, default rates for the company has also been steadily climbing higher and has increased significantly recently. We believe given the continued uncertain macroeconomic environment could lead to further credit deterioration and its exposure to relatively middle income class of population compared to its peers is relatively more prone to economic shocks which might lead to default rates climbing above the 10% mark for the first time in its history.

Selling and marketing expenses as % of revenues improved to 53% currently from 57% in Q2 2022 (and 54% in Q1 2023) enabling them to deliver Adj. EBITDA of $41 mn, up 17% YoY. Management expects the selling and marketing expenses to be at 54% of the revenue at midpoint for the remainder of the year which implies a slight sequential deterioration. The deterioration in marketing costs was as a result of transitioning of kiosks at certain Cabela stores to virtual kiosks and further exiting certain kiosks entirely.

While the number of vacation packages sold grew 17% YoY for the quarter which is a positive considering the dip in marketing costs, active vacation packages went down by 10%. This essentially would imply that BVH would need to grow its vacation packages base and increase the new vacation packages which would imply an increase in marketing costs at the higher end of the management guidance and imply a 100 bps sequential deterioration in EBITDA margins. We forecast a 21% EBITDA margin for the second half of the year considering stable default rates. Diluted EPS grew 54% YoY primarily driven by a reduction in the share count (16.3 mn shares currently compared to 20 mn+ last year) along with strong operating profits.

Valuation

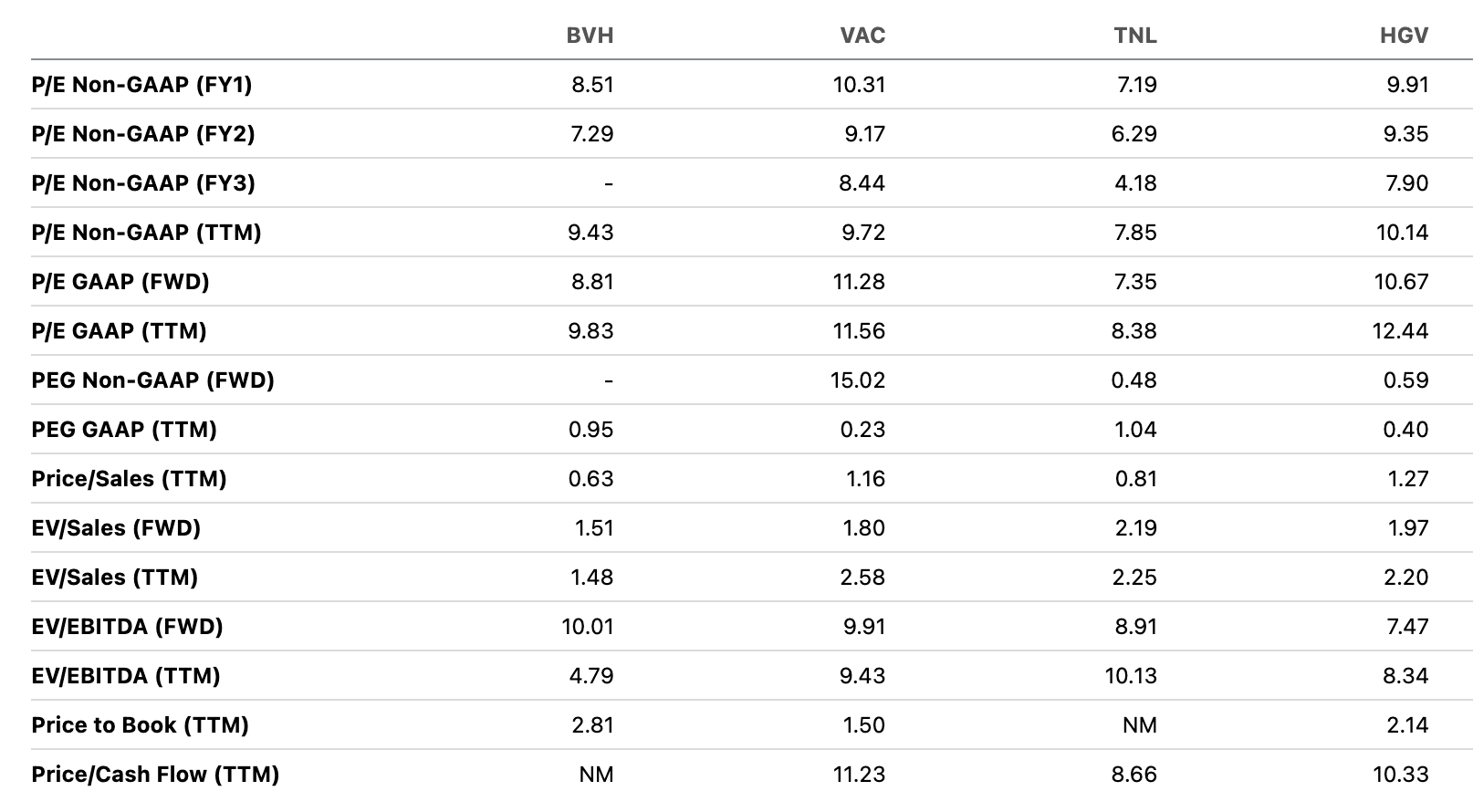

BVH trades at 8.5x Fwd P/E ratio which appears as a marginal discount to its peers. We believe VAC and HGV with their relative size as well as strong brand resonance deserves to trade at a premium.

{kind=link}

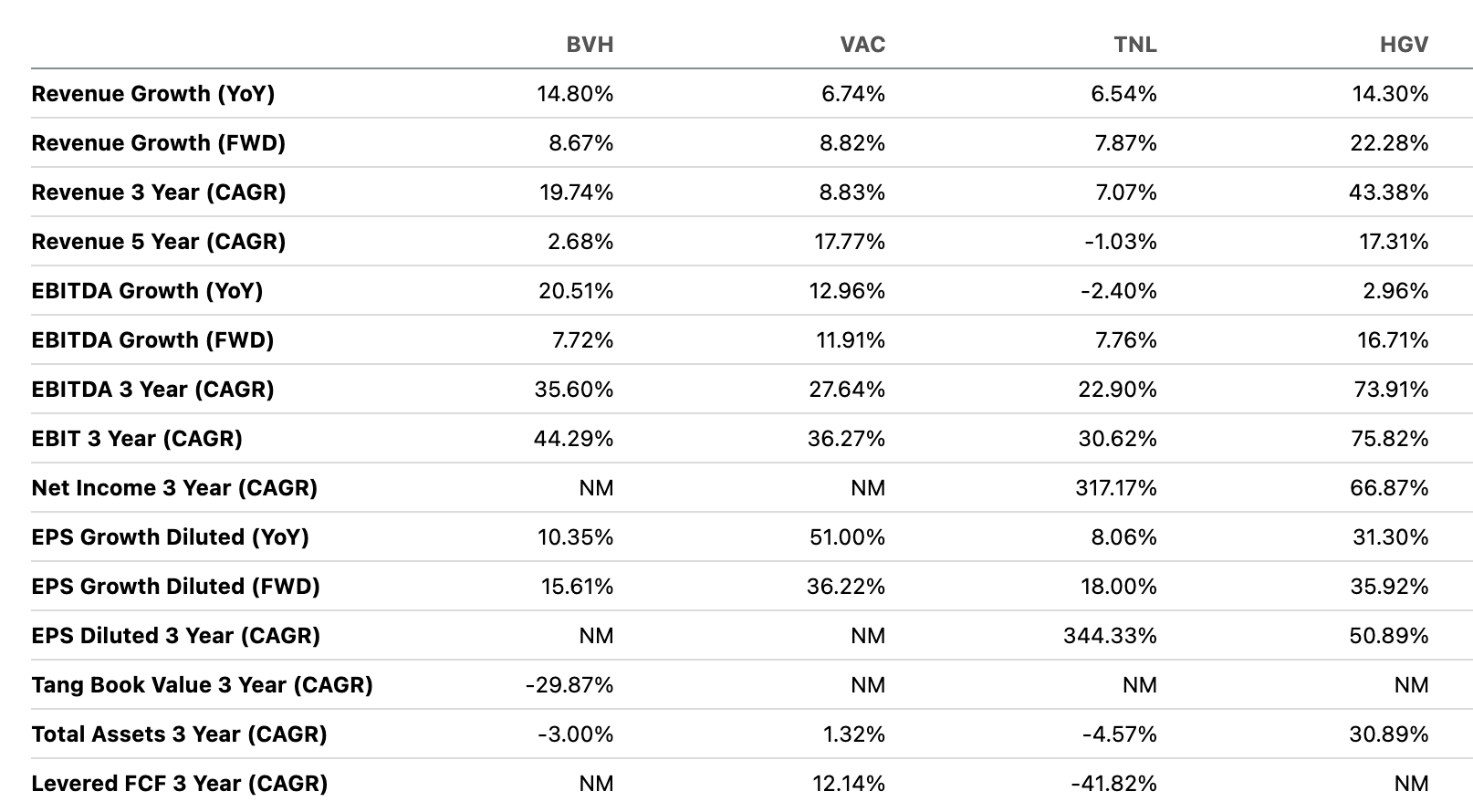

In addition, its 5-year revenue and EBITDA growth has lagged its larger peers and has been a bit underwhelming while it has managed to keep up with Travel + Leisure Co. ( TNL ). Its forward-looking growth forecasts also lag peers with EPS growth of 16% compared to the peer average of 30% growth .

{kind=link}

We believe while the company is continuing its expansion mode there are potential downside risks as a result of increasing default rates given the current tight credit period. We believe the company is likely to post a high double-digit growth during the remainder of the year driven by the follow through of its strong growth in vacation packages as well as seasonality due to the holiday season. However, margins are expected to shrink 100 bps even considering stable default rates which could be subject to further downward revisions in case of a jump in default rates.

We initiate at Neutral with a target price of $30 (at 7.2x Fwd P/E in line with TNL) and adopt a wait and watch approach, particularly on the default rates.

Risks to Rating

Risks to rating include

1) Any significant impact on the economic environment can lead to decrease in consumer spends, thereby reducing the vacation packages that the company is able to sell as well as a rise in default rates and which in turn can lead to credit losses and can badly hit its bottom line

2) It generates almost a fifth of its revenue from its partnerships with Bass Pro. Any significant impact on its partnership agreement or its inability to renew it in similar or favorable terms which is ending in 2024 can hamper its business operations

3) Its presence in the hospitality industry makes them more prone to providing extraordinary customer service at its resorts and its inability to maintain service standards can lead to higher customer churn.

Final Takeaways

BVH has done phenomenally well for the year driven by its robust gross margin as well as improving operating margin profile as a result of its decreasing marketing spends. However, given the current macro backdrop and its increasing push to grow its own financing based portfolio can be potentially risky and lead to higher loan losses, while the default rates has also been steadily increasing already. We believe the valuation multiple also reflects the future growth priced in which could be subject to potential downside risks going forward. We initiate at Neutral.

For further details see:

Bluegreen Vacations: Not Taking This Vacation