BVHBB - Bluegreen Vacations: Risks Ahead Can Slow Down Share Price Rise

2023-06-15 12:09:43 ET

Summary

- Vacation ownership interest provider Bluegreen Vacations Holding Corporation has seen a 35% price rise YTD. Its sales growth is healthy and margins are strong too.

- However, its price is at five-year highs and P/E is above the historical average. Also, economic uncertainty could reflect in higher loan loss provisions, further affecting the already softening EPS.

- It's possible that the risks don't actually materialise. But taking a cautious approach, I'd much rather wait and watch for now.

Despite the macroeconomic slowdown and its likely impact on the travel industry, vacation ownership interest [VOI] provider Bluegreen Vacations Holding Corporation ( BVH ) is in expansion mode. In a recent release, it said that it has acquired two new properties in Nashville, Tennessee, increasing the number of new properties in its portfolio to four in the last eight months alone. Its own recent above average growth also shows continued momentum in the market.

The reasons are not hard to find. The business model has the advantage of predictable, recurring revenues, which can be a nice cushion at time of economic uncertainty. Also, the margins are notably high. At 87.6% in 2022, BVH’s gross margins are high enough to give any bonafide luxury company a run for its money.

Does this mean that this segment will not be affected by a slowdown? It can be, of course. As I pointed out in my last article on another VOI company, Travel + Leisure Co. ( TNL ), the company expects some slowing down in sales in 2023. But the extent of the impact of a slowdown on the segment could be lesser than that for travel as such. Here, I take a closer look at the company’s recent numbers to ascertain if and why signs of a slowdown are becoming evident and what that means for its share price in the future.

Sustained sale growth

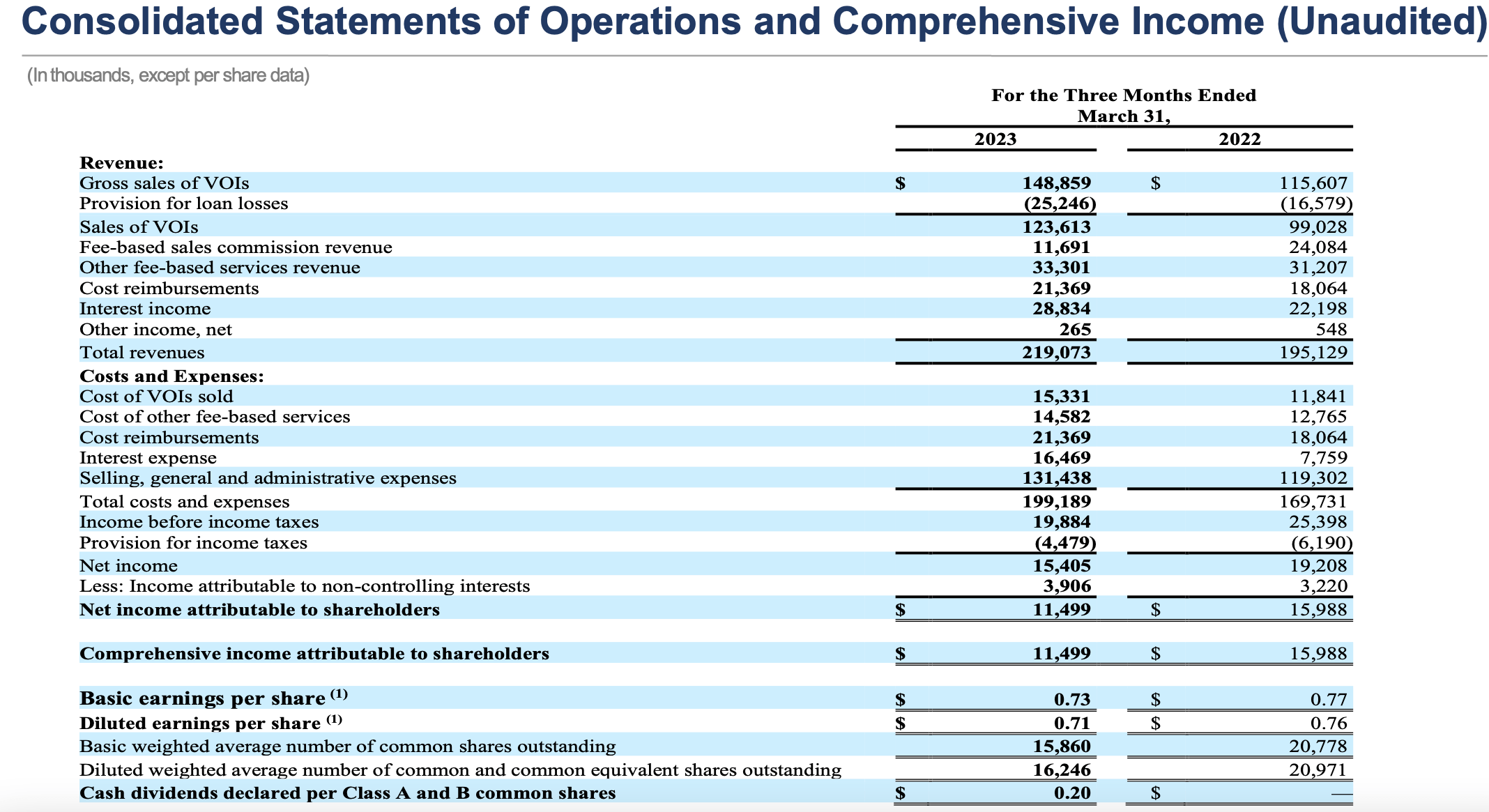

BVH’s sales figures for the first quarter of 2023 (Q1 2023) saw healthy revenue growth of 13% year-on-year (YoY). It is down from the 24% increase seen for the full year 2022, for sure, but it does need to be borne in mind that 2022 was driven at least partly by pent-up travel demand from the pandemic time period. Also, growth is still higher than the 9.4% pre-pandemic growth of 2019 and the compounded annual growth rate [CAGR] of 6.6% over the past decade.

Analysts are also bullish about the company’s prospects, with expectations of growth staying over 13% YoY for the full year 2023. Looking at this picture holistically indicates that growth will likely continue at a good pace, just not quite what we saw in 2022.

{kind=link}

Why the EPS has weakened

The company has also been able to largely maintain its gross margin in Q1 2023 at 86.6%, even with a rise in cost of revenues to 21.6% YoY. The company reported an increase in operating income too. However, its earnings per share [EPS] has still declined by 5.2% YoY.

A doubling in interest expenses from Q1 2022, on account of rising interest rates and higher debt for BVH, is one reason for the EPS decline. The sharp rise in this expense would have been a red flag were it not for healthy operating income, which has managed to keep the interest coverage ratio at a healthy 3.7x even though it has declined a fair bit from the 6.4x in Q1 2022.

The company also mentions a plethora of other expenses in detailing the reasons for the decline in EPS. Expenses on additional inventories, higher staffing costs in expectation of higher sales and costs of a new sales centre are some of them. Neither of these sound worrisome, on the contrary, they indicate an optimistic and expansionary mindset on the part of the company’s management.

Not all costs indicate expectations of future growth, though. The company has also faced a drag from closure of some resorts because of natural events, as well as higher provision for loan losses at 17% of VOI sales compared to 14% in Q1 2022. Bluegreen Vacations ascribes this to it having financed a higher proportion of the sales.

But this is a potentially risky time for loan increases. Even though bad debt is in check at the level of the economy, it is worth noting that the four biggest banks in the US saw a 73% YoY increase in bad loans in Q1 2023. I would watch this number in the coming quarters. Overall, though, the cost picture indicates that some could actually add to sales growth, while others point to risks ahead.

Market valuation

The odds so far seem to be in BVH’s favour though, with analyst expectations of positive EPS in 2023. The non-GAAP figure is expected to end the year at USD 4.2. This yields a forward non-GAAP price-to-earnings [P/E] ratio of 8.2x. The company’s forward GAAP P/E is at 8.4x.

The consumer discretionary sector, as such, has a higher forward valuation , but compared to its closest peers, Bluegreen Vacations looks less undervalued. TNL, for instance, has both lower TTM and forward P/Es compared to BVH. Though, others like Marriott Vacations Worldwide ( VAC ) and Hilton Grand Vacations ( HGV ) have higher valuations.

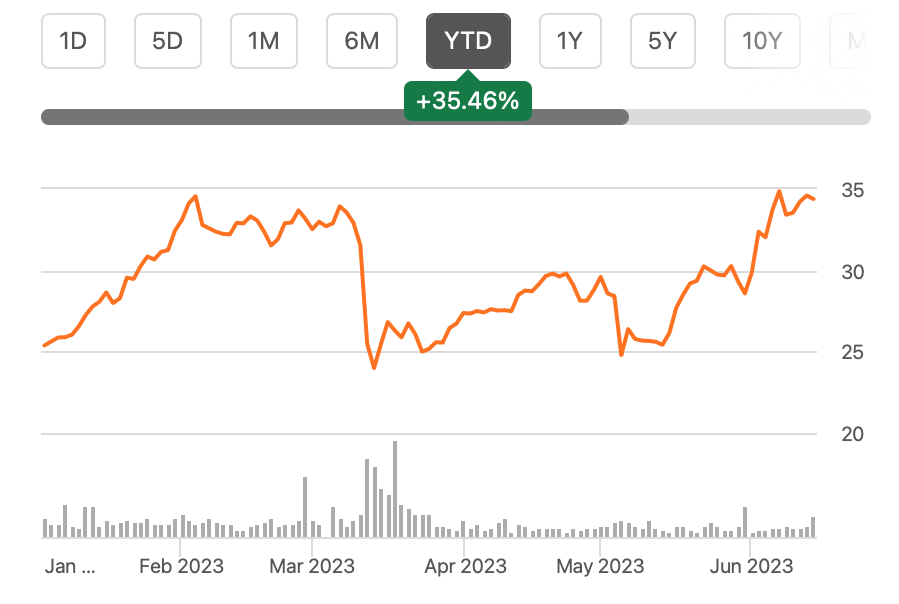

Just to keep things simple, here I look at the average TTM GAAP P/E for the vacations sector to assess the share price potential for BVH. At 12.2x, it indicates a 13% upside to the BVH stock, which has a current P/E ratio of 10.8x. Investors have clearly realised this, as indicated by the 35% increase in share price year to date. However, because of this price increase, BVH is trading at some of the highest levels in the past five years. Also, the current P/E is at higher levels than the long-term median of 7.9x. Moreover, peers like VAC and HGV are far more established and bigger than BVH, which can explain the relative premium to their prices.

{kind=link}

What next?

This is not to say there aren’t clear positives to BVH. There are. The VOI segment can be cushioned from a challenging time for consumer demand. Its growth is still strong and expected to remain so. Robust margins are in its favour too, as are expectations of healthy EPS. The company is expanding, which can further fuel growth and justifies some of the cost increases it has seen recently. Its attractive P/E ratios compared to the sector also go in its favour.

At the same time, it is hard to overlook the fact that its price is already at near the highest levels seen in the last five years. Also, while its P/E maybe lower than that for some peers, it is still higher than the stock’s own historical average. Macroeconomic challenges can also tell on its fundamentals, both in terms of demand for VOI sales and the possibility of bad loans. For these reasons, I am cautious about it, especially since the slowdown story is yet to play out fully. At this time, it's possible that the risks don't actually materialise. But taking a cautious approach, I'd much rather wait and watch for now. I am going with a Hold on Bluegreen Vacations.

For further details see:

Bluegreen Vacations: Risks Ahead Can Slow Down Share Price Rise