BMTX - BM Technologies: The Warrants

Summary

- BankMobile Technologies if a fintech acquiring a bank charter.

- They also maintain a defensible moat in the US higher ed student disbursement business market.

- The transition from a fintech to a full-scale bank coupled with their $2 billion in deposits is likely to generate significant profits.

- In this article I develop a conservative 2023 EBITDA estimate of $43.071m which implies BMTX is trading at a 5.47x EV/EBITDA.

- Then I explore how the warrants (BMTXW) may offer an even better investment opportunity in the company.

Subscribers to the Microcap Review received early access to this article on October 17th, 2022. Anyone looking for additional microcap value and event driven opportunities should take a look at the offering and author Safety in Value's work.

------------------------

Back in August I wrote up BM Technologies ( BMTX ) (BankMobile) as a fintech company acquiring a bank charter trading at just P/FCF of 2.97x. You can see that the stock price at publication was $6.45 and the pick overall has performed well in the near term.

Seeking Alpha: Chart of Author's Recommendation and Performance

But I want to talk more specifically about their publicly traded warrants ( BMTXW ) which expire January 4th, 2026. I believe that the warrants may be a better way to invest in the company if one believes in the long term prospects of the company.

BankMobile Technologies: A Recap

There’s a lot of relevant information about the company in my first article that I won’t be covering in this one. With that said I do want to provide an overview to contextualize the company. So here goes.

BankMobile Technologies previously was a subsidiary of Customers Bancorp ( CUBI ) before separating and coming public via the SPAC Megalith Financial Acquisition in January 2021. The company is run by CEO Luvleen Sidhu who originally developed the business model idea and pitched it to CUBI which was run by her father, Jay Sidhu.

The big idea was to create a full service fintech banking platform with a focus to generate low cost customer acquisition through its Higher Ed Disbursement and Banking-as-a-Service ((BaaS)) businesses. Let’s look at these in turn.

Higher Ed Disbursement Business

The Higher Ed Disbursement piece of the business partners with higher ed institutions to facilitate the process of financial aid disbursement. As of their latest investor presentation , BankMobile serves 1 in 3 of every higher ed student, has over 750 university partners, and disbursed $2 billion in financial aid in Q2’22 alone.

BankMobile controls 31% of the market with their second competitor simply being institutions doing this in house. That represents further market share the company could expand into. And they are working actively to build further offerings for their university partners.

BMTX Investor Presentation: Chart of US HIgher Ed Student Disbursement Market Share.

I believe that the company has established a meaningful moat in this niche market and with 98% retention and average contracts of 3-5 years this should sustain for a while. Additionally, there are numerous regulations the company is subject to unique to higher ed disbursement which provide a barrier to entry for the market.

From this moat that they’ve built the company processes $10 billion in payments each year for students. As part of this each student has the option to open a new BankMobile student checking account to receive their disbursement. Last year the company processed $13.4b disbursements and $1.8b of those chose to set up a checking account - a 13.43% conversion.

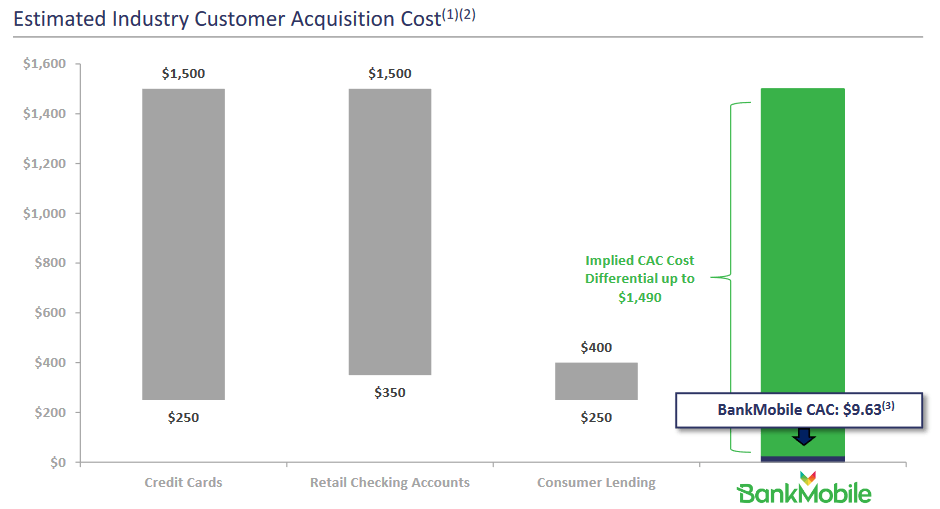

This is the key strategic feature of the moat they’ve built. That $13.4b disbursement amount represents an annual process that these university partners go through. Each year the company is exposed to up to $10 billion dollars of potential new deposits. The result is incredibly low customer acquisition costs ($9.63) compared to the industry as reported in August 2020 .

BMTX Investor Presentation: Chart of Customer Acquisition Costs

{kind=link}

From my view, the higher ed disbursement business is a huge operating benefit with a long term moat in place. They don’t break out profitability directly for the business but do note that it generates $60 million in revenue annually by itself.

Banking-as-a-Service Business

BankMobile also operates a BaaS business where they focus on a business to business to consumer model or B2B2C. Through this model, BankMobile services partners like T-Mobile with a white label digital banking platform which enables these partners to offer bank-like services (read: checking accounts, savings accounts, credit cards) directly while not managing the underlying deposits. The result is something that looks like T-Mobile Money and it exposes BMTX to T-Mobile’s estimated 110 million customers .

In their Q2’22 earnings call the company announced a new BaaS partnership with a company servings tens of millions of US customers. Details about the new partner were deliberately scarce to protect the commercial launch for the partner expected in early 2023. I wrote another article speculating that this new partner may be Starbucks , and it still might be.

Regardless of who the partner is we can observe the benefits to BankMobile as these partnerships expose the company to large new customer bases. Depending on the brand strength and loyalty the results of this could be significant inflow of deposits as people sign up for say a Starbucks checking account.

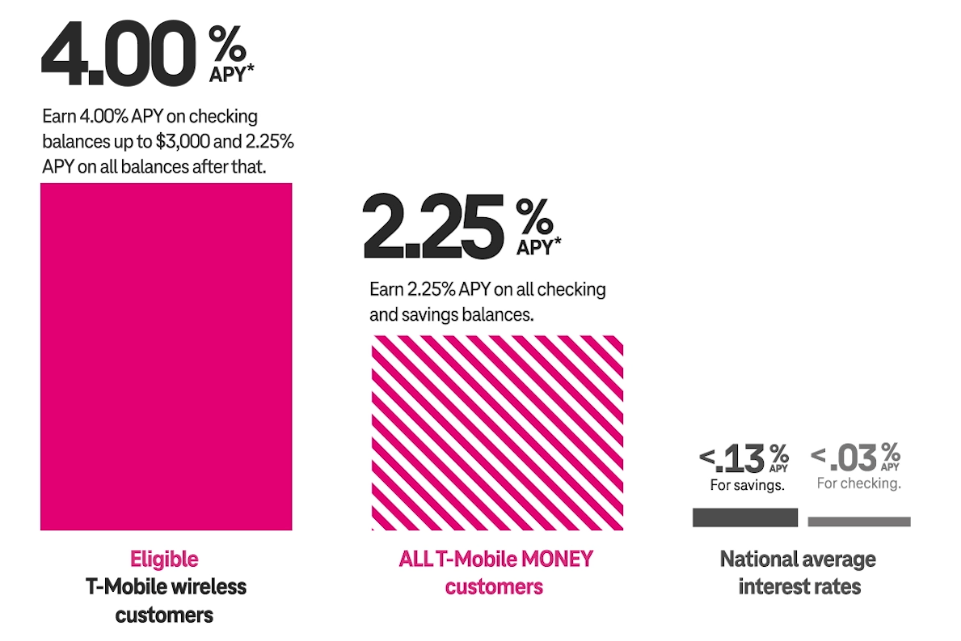

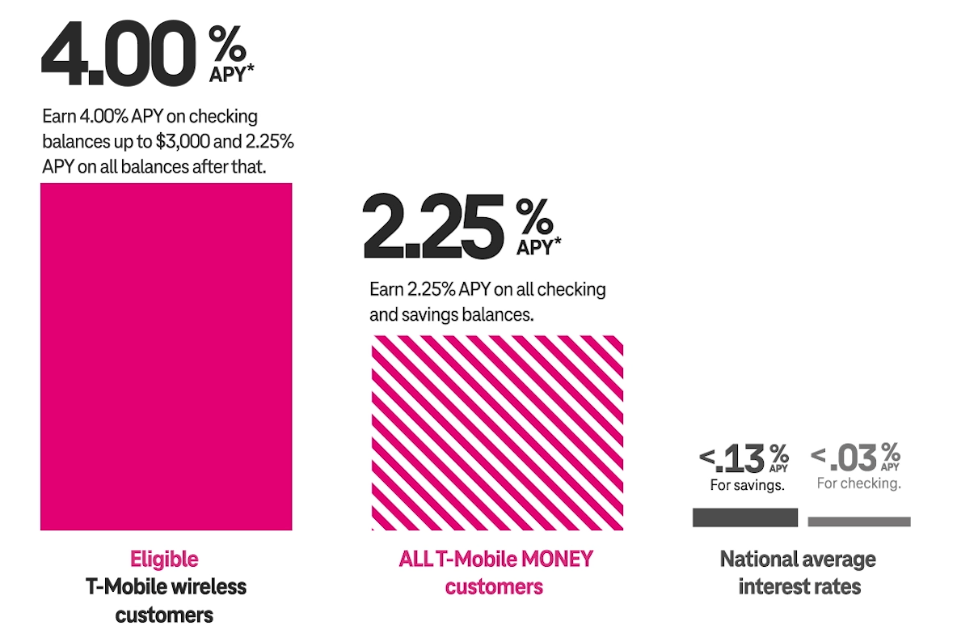

These programs can be merged with loyalty and rewards perks from the partner. You can see an example of this bundling tactic at T-Mobile where they offer a much higher interest rate (4.00%) to customers that already have a phone line with them versus those that don’t (2.25%).

T-Mobile: Account Interest Rates

{kind=link}

{kind=link}

Management indicates that they hope to onboard a new BaaS partner every 12-18 months. Early next year whenever a commercial launch happens we should get a better sense of the opportunity. The major benefit of these partnerships is the potential to grow the deposit base even further. Which, as we turn to next, you’ll see has grown significantly.

The Deposits and Upcoming Bank Charter

As of Q2’22 the company had an average service deposit value of $2 billion which was up 29% YoY. What does the company do with all of these dollars sitting around?

Well historically BMTX had a partnership with CUBI where Customers paid a 2.75-3% service fee to hold the deposits themselves. This was a requirement really for BankMobile because they have no way to hold the deposits themselves as they are not officially a bank. By partnering with a bank (Customers) then they were able to monetize the huge deposit base.

But Customers announced that they would be ending the partnership this year meaning BankMobile needed a new plan to monetize this asset. One way to do this is to become a bank that can manage these deposits directly and aim to generate income through lending. And that’s exactly what they are on track to do.

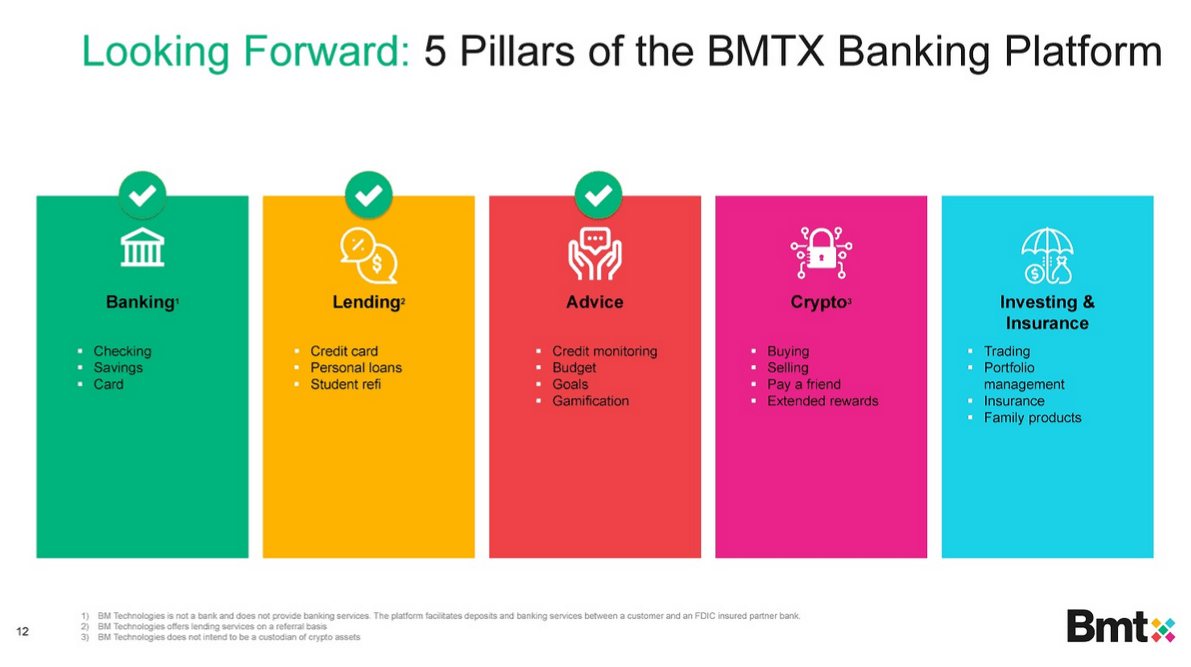

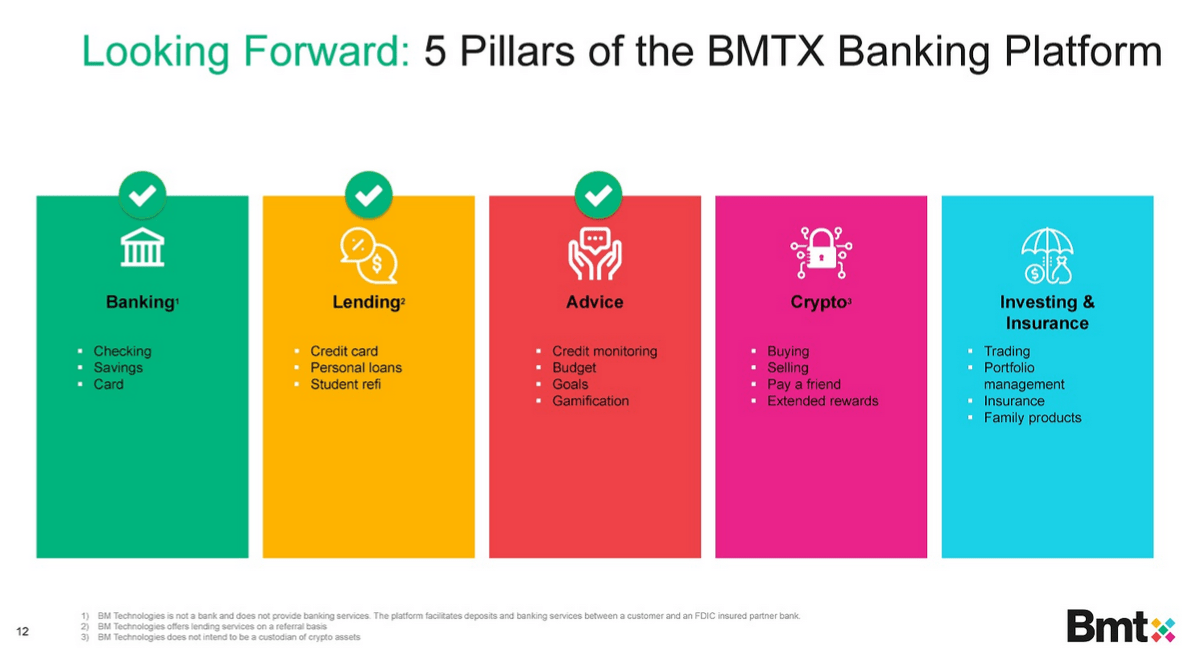

Sometime before the end of the year BMTX is expected to close an acquisition of First Sound Bank which would position the company with a national bank charter. Rather than generating income from a service fee on deposits the company is poised to transform into a full-service bank. From their guidance it’s even more apparent with expected options expanding into lending, financial advice, crypto, and investing & insurance.

BMTX Investor Presentation: The 5 Pillars

{kind=link}

{kind=link}

The merger will likely be immediately accretive as the bank is profitable as a standalone entity. What it enables for BMTX moving forward is the ability to start pulling those $2 billion of deposits over to the balance sheet as a source of funding. With a current market capitalization of $94.011m this change is likely to be material.

The process will not be immediate though. Banks are subject to capital requirements and must maintain a total capital ratio of 8% of their risk weighted assets (RWA) with 6% of this required to be Tier 1 capital. I did some analysis in my original piece to estimate what their balance sheet might look like post-acquisition which we can then use to estimate how much lending they can do.

Valuing BankMobiles Technologies

My guess was that they could bring between $65.12m - 256.29m while maintaining CET1 ratios of 10-13.1%. Shareholder equity as of Q2’22 totaled $52.779m. Even if we consider the low end of my estimate and a year of time to deploy those loans then that would give us a 2023 book value estimate of $117.899m. That’s 123% growth with no consideration of their core earnings.

From an earnings perspective we could do a rough calculation assuming annual interest payments of 5% on the principal ($65m) which gets us to $0.27 revenue per share.

We still need to consider what happens with the rest of the deposits. We can subtract the $65m from $2b and we’re left with $1.935 billion. Theoretically the company could invest all $1.935b into risk-free 20 year T-bonds at a 3.375% rate. If we do the math this would imply a revenue per share of $5.32 from these bonds alone.

These are the same deposits that Customers has been paying a 2.75-3.00% fee to use. Management indicated in their last call that they are considering partnering with a sponsor bank similarly which would likely imply a yield higher than the T-Bonds might offer. Chief Financial Officer Bob Ramsey indicated that they were expecting between the 3-4% range with likelihood being towards the higher end given rising interest rates.

Let’s do a conservative estimate then assuming another sponsor bank is willing to offer 4% on the deposits. That would imply annual revenue per share of $6.31 through this type of partnership.

Something to note is that the revenue per share numbers I’m giving so far are based on current shares outstanding of 12.273m. There are an additional 23.873m warrants exercisable at $11.50 which we should consider as well.

Here’s a table that pulls all this data together with a fully diluted revenue per share estimate.

| Deposit Value |

| Yield Estimate |

| Revenue Estimate |

| Revenue Per Share |

| Fully Diluted Revenue Per Share |

| New Lending with CET1 @ 13.10% |

| $65.12 |

| 5.000% |

| $3.26 |

| $0.27 |

| $0.09 |

| Scenario 1: 20 year T-bonds @ 3.375% |

| $1,935 |

| 3.375% |

| $65 |

| $5.32 |

| $1.87 |

| Scenario 2: Sponsor Bank @ 4.000% |

| $1,935 |

| 4.000% |

| $77 |

| $6.31 |

| $2.21 |

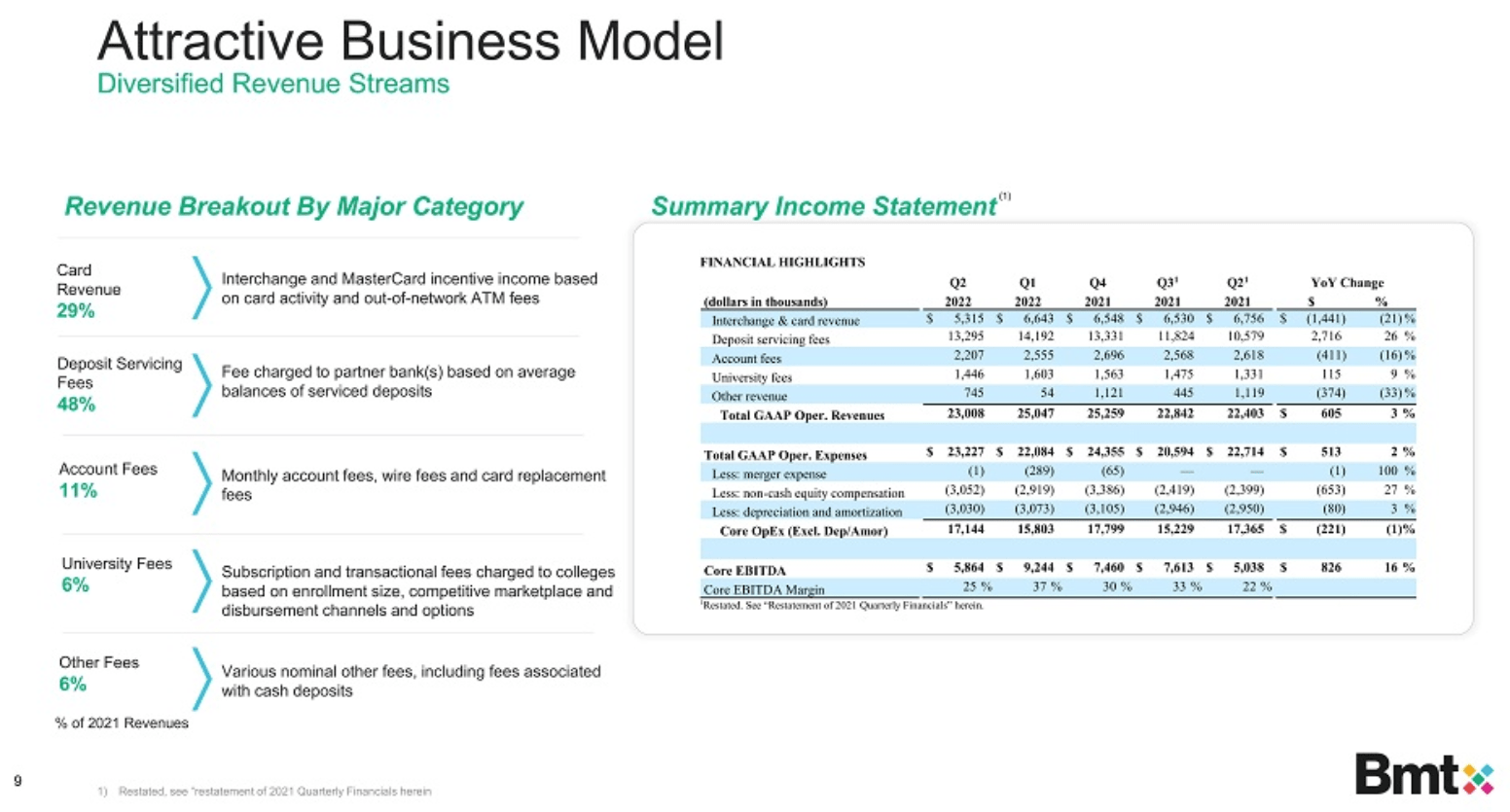

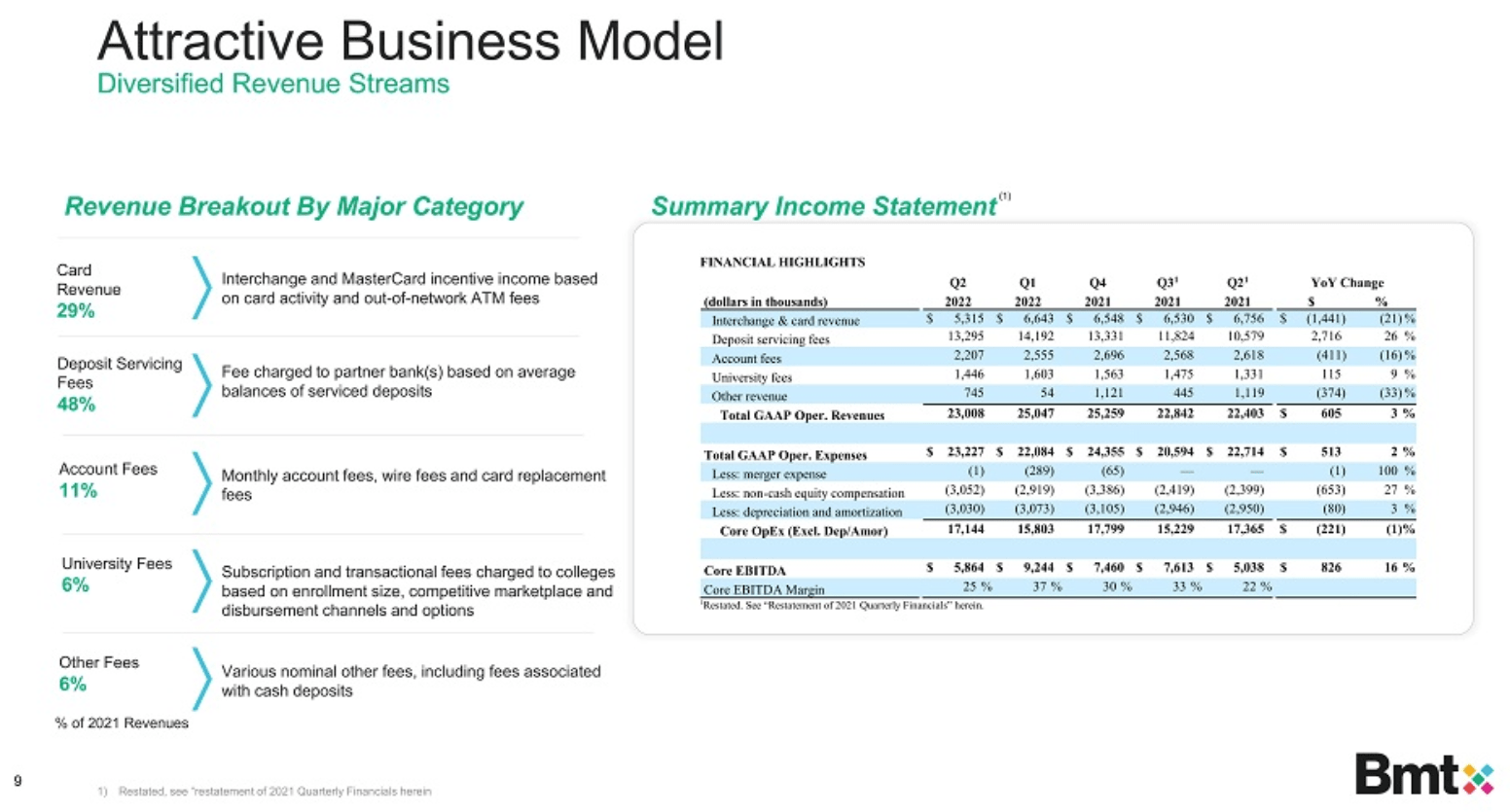

We can use this to estimate a fully diluted revenue range for their deposits of $1.96 - $2.21. Traditionally this revenue is reported as deposit servicing fees and is 48% of the revenue mix. Over the last five quarters they’ve averaged $12.644m revenue a quarter here which annualized is $50.576m or $1.45 per share.

BMTX Investor Presentation: Revenue Breakdown

{kind=link}

{kind=link}

That means that the low end estimate I developed based on very conservative estimates suggests a 35% increase in revenue in this segment. Using a five quarter average for each of the other revenue sources and operating expenses we get a model that looks like this.

| (dollars in millions) |

| 2023 Estimate |

| Interchange & card revenue |

| $25.434 |

| Deposit servicing fees/income |

| $68.260 |

| Accounts fees |

| $10.115 |

| University fees |

| $5.934 |

| Revenue |

| $109.743 |

| Core OpEx (excl. Dep/Amor) |

| $66.672 |

| Core EBITDA |

| $43.071 |

This compares to their five quarter EBITDA average of $7.044m which annualized is $28.176m. Full year EBITDA for 2021 came in at $28.6m. So we are looking at a conservative estimate of EBITDA which implies over 50% growth in the next year.

Here’s a table which gets us to a fully diluted enterprise value.

| Current BMTX Price |

| $7.55 |

| Shares Outstanding |

| 12.273 |

| Warrants |

| 22.703 |

| Market Capitalization |

| $92.661 |

| Fully diluted market cap |

| $264.069 |

| Total Debt |

| $0.000 |

| Cash |

| $32.484 |

| EV |

| $231.585 |

Putting this together with our estimate this means that BMTX is trading at an EV/EBITDA multiple of 5.38x on a fully diluted basis. All of this is based on conservative estimates for their deposits and assuming no growth for their other revenue verticals. There’s optionality built in here with the new BaaS partner that will launch next year as well.

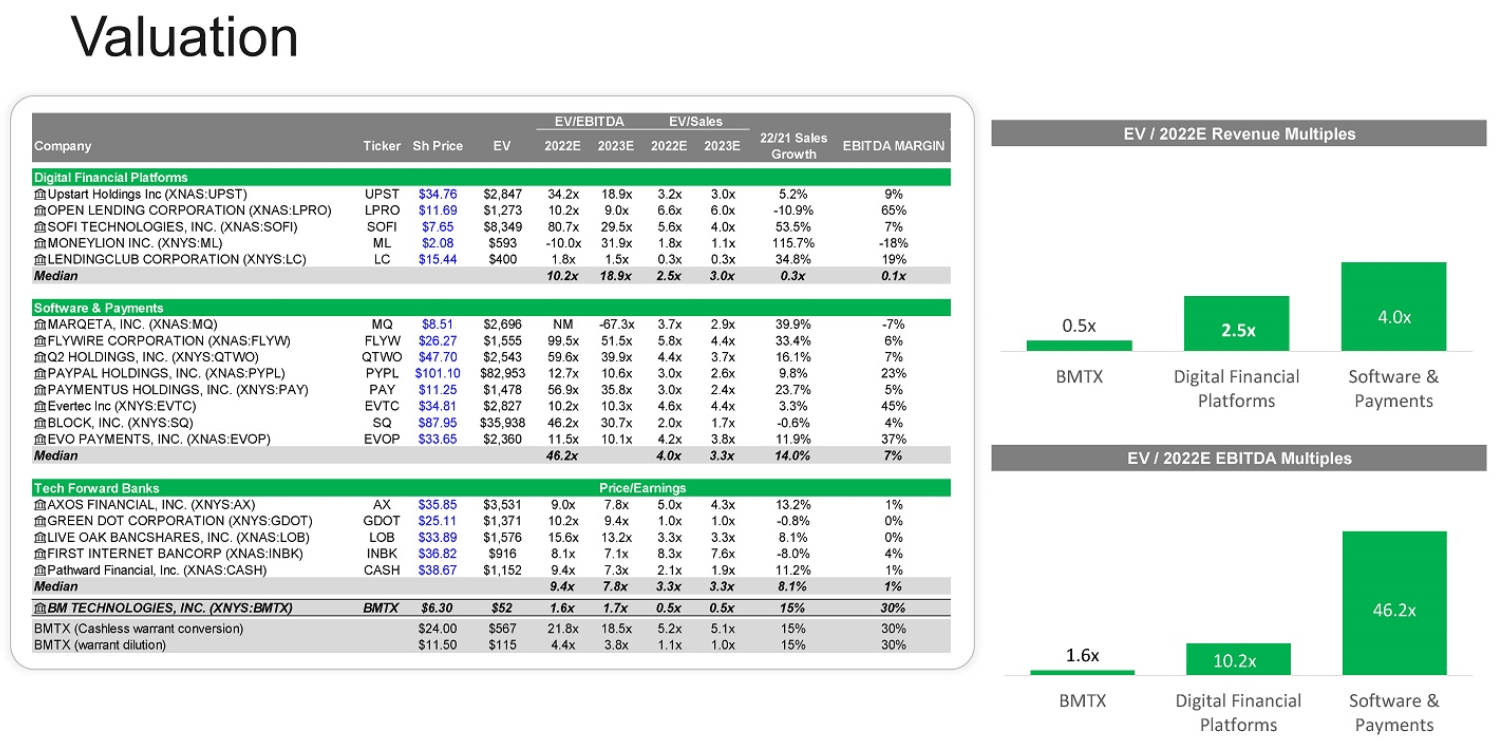

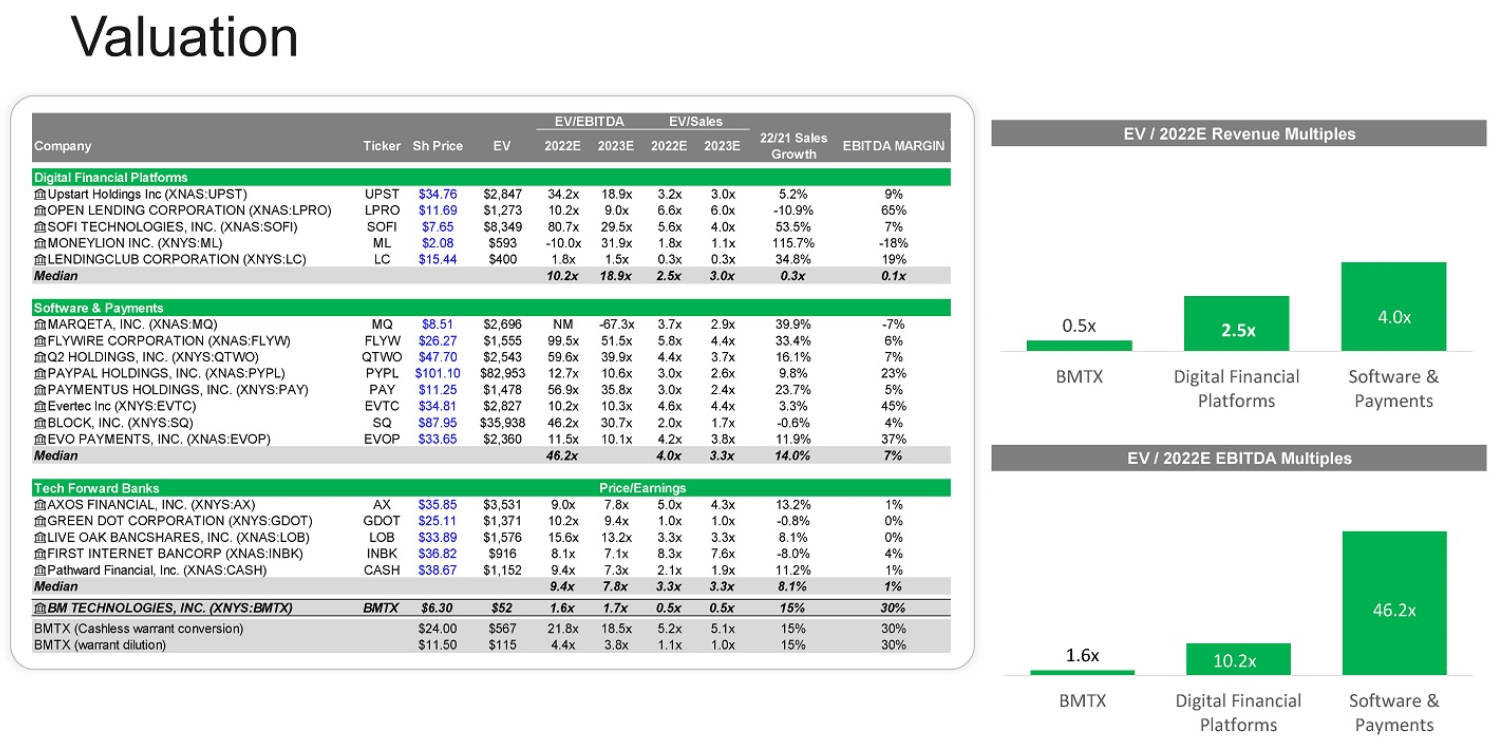

From a relative valuation basis we can review data compared to peers. We can see that an average of both medians for the Digital Financial Platforms and Tech Forward Banks categories the median EV/EBITDA is 9.8x or 82% higher than BMTX's current multiple. This excludes the much loftier valuation of the Software & Payments category.

BMTX Investor Presentation: Peer Valuations

{kind=link}

{kind=link}

The Warrants At Last

I believe from all of this a reasonable assumption is that BMTX should trade more in line with the 9.8x EV/EBITDA multiple. We can extrapolate from this that the stock price would be trading at $13.73 to get there. In my judgment this could happen over the next 1-2 years or sooner depending on results and would be an 82% return.

That seems attractive in the current environment. And the bank company is inflation and recession resistant with their revenue potential increasing each time interest rates rise.

But let’s look at the warrants exercisable at $11.50. At the time of writing the BMTXW price was around $0.94 and if we use our BMTX price target of $13.73 we can derive these numbers.

| Stock Price |

| $7.55 |

| EV/EBITDA reversion |

| 82.00% |

| Implied stock price |

| $13.73 |

| Warrant Conversion |

| $11.50 |

| Implied Warrant Value |

| $2.23 |

| Warrant Price |

| $0.90 |

| Warrant Return |

| 147.78% |

Not only do the warrants offer a higher return potential if my estimates are correct, the warrants stand to benefit the company exactly when they need to bring more capital on hand. Cash conversion of warrants will bring more cash to the company even as it dilutes the common shareholders. From a warrant holder’s perspective that means that if and when you exercise the warrants you are actually helping improve the company’s capital ratios which enables more of their deposits to be brought directly on the balance sheet.

For reference, if all the warrants are exercised at $11.50 that will bring $261.08m in cash to their balance sheet. That is cash that immediately improves their CET1 ratios and can be redeployed. So the warrants represent a burst of liquidity if the stock price starts to trade meaningfully over $11.50.

There are redemption rights for the warrants if the stock trades over $24.00 for twenty out of thirty days. If it came to that then the company will likely have experienced a significant sentiment shift. That caps the upside potential for the warrants at a tidy 1230%.

There are obviously greater risks associated with the warrants. The stock price may simply never reach a value where the warrants are exercisable. I think this is mitigated by the factors leading to potential growth if the bank acquisition closes.

Putting All The Pieces Together

I’ve tried to paint a bit of a picture here of the company and prospects moving forward which I think support my conservative estimate of 2023 EBITDA at $43.071m. Based on this and current trading data I suggest that the stock price return for BMTX could be 82% over the next 1-2 years.

The publicly traded warrants for BankMobile seem to offer an even better risk-reward potential. If we use the same estimates to get an 82% return from BMTX then that would imply a return on the warrants of 148%. Warrant conversion will help the company as it makes this transition to a bank by bringing liquidity to the balance sheet which can be used likely immediately.

The mechanics of this suggest that owning the warrants offers an even better opportunity to invest in what may be a multi-year compounder.

There are risks here and I’ve gone in more depth in my other articles. A few things I’ll note though is that they are coming off of delayed filings and recently changed auditors. Stock based compensation has been high over the last year related to some auditing concerns but everything seems to be accounted for at this point. It’s still a number that I’m keeping an eye on.

The merger itself with First Sound Bank has not completed and is material to my thesis. If it does not go through then much of what I outlined above wouldn’t be applicable any longer because the company would not be acquiring a bank charter. So this is a risk to keep in mind as well, though I do not think it’s likely. It does not, however, prevent the company from partnering with sponsor banks further to monetize the deposits.

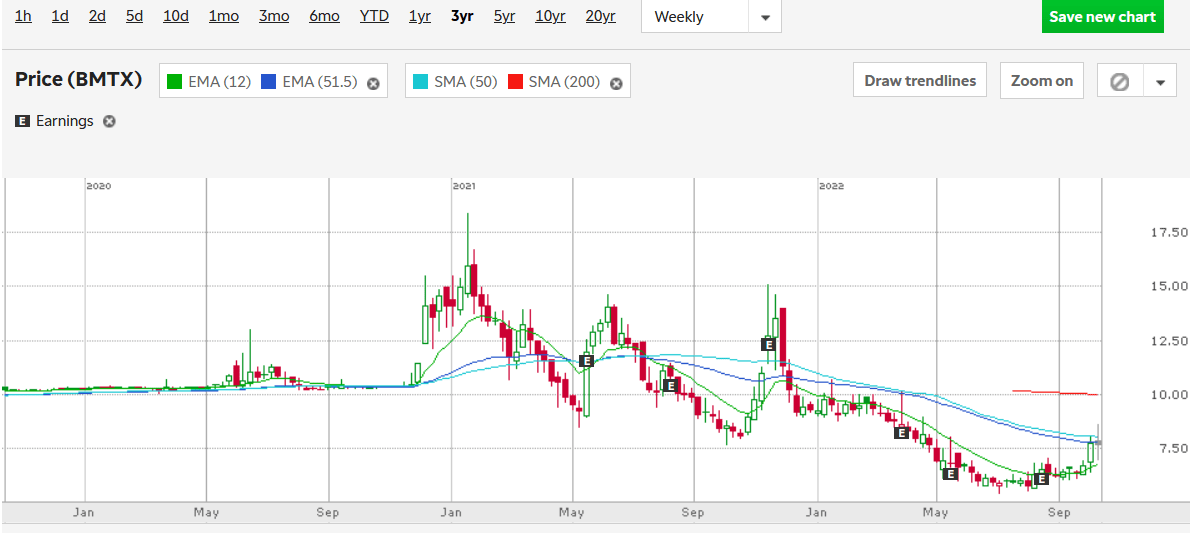

And just as a final visual, look at the BMTX three year price chart. Even before all of this change in the company’s prospects the stock price has traded meaningfully above the warrant conversion price ($11.50) three times. It seems that next year it may happen again.

TD Ameritrade: BMTX 3-year Price Chart.

{kind=link}

For further details see:

BM Technologies: The Warrants