BAYZF - Breaking Up Bayer? Probably Not!

2023-11-10 10:56:34 ET

Summary

- Bayer is reporting rather terrible third quarter results, although currency effects had a huge negative impact on the top line.

- Additionally, Bayer is currently discussing several options how to proceed with the business – including the possibility to split up Bayer in three different businesses.

- Although the other two segments – Consumer Health and Pharmaceuticals – would profit from Crop Sciences being split off, such a move does not seem likely in my opinion.

- Overall, I remain confident that Bayer is a “Buy” and the stock remains undervalued – despite all the problems and lawsuits the Crop Science business is facing.

My last article about the German life science company Bayer Aktiengesellschaft ( BAYZF ) ( BAYRY ) was published less than three months ago. Nevertheless, it seems to be time for another update for three different reasons. First, the stock declined about 20% since my last article - although I called Bayer still a "Buy". Second, Bayer reported rather disappointing third quarter results, and finally, management pushed forward its discussion of the possibility of breaking up the company. Let's start with the quarterly results.

Quarterly Results

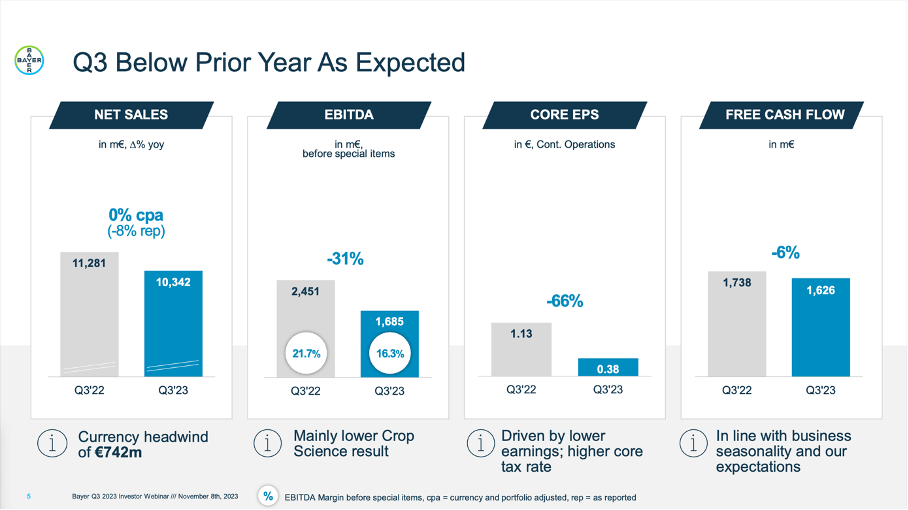

At first glance, we must describe the quarterly results as horrible. For starters, Bayer had to report declining sales as net sales decreased 8.3% year-over-year from €11,281 million in Q3/22 to €10,342 million in Q3/23. However, this steep decline was mostly due to FX effects and when adjusted for currency as well as portfolio, sales declined only 0.2% year-over-year (still not a great result, but more acceptable). The reported EBIT switched from €1,199 million in the same quarter last year to a negative amount of €3,594 million this quarter and earnings per share also switched from €0.56 in Q3/22 to a loss per share of €4.66 this quarter.

{kind=link}

When looking at the results in more detail we can identify two major problems. First, the cost of goods sold increased from €4,247 million in the same quarter last year to €4,812 million this quarter and with a simultaneously declining revenue, this led to a much lower gross margin (53.5% compared to 62.4% in the same quarter last year). Second, Bayer reported impairment loss reversals of €3,954 million, which had a huge negative effect on the bottom line.

To report a little more positive results, we can look at the core earnings per share Bayer is also reporting (an adjusted number). And while Bayer could still report a profit, €0.38 in earnings per share is reflecting a 66.4% decline compared to €1.13 in the same quarter last year. Only free cash flow was a ray of hope. The number also declined 6.4% from €1,738 million in the same quarter last year to €1,626 million this quarter but compared to the negative numbers Bayer had to report in the past, this is positive news.

{kind=link}

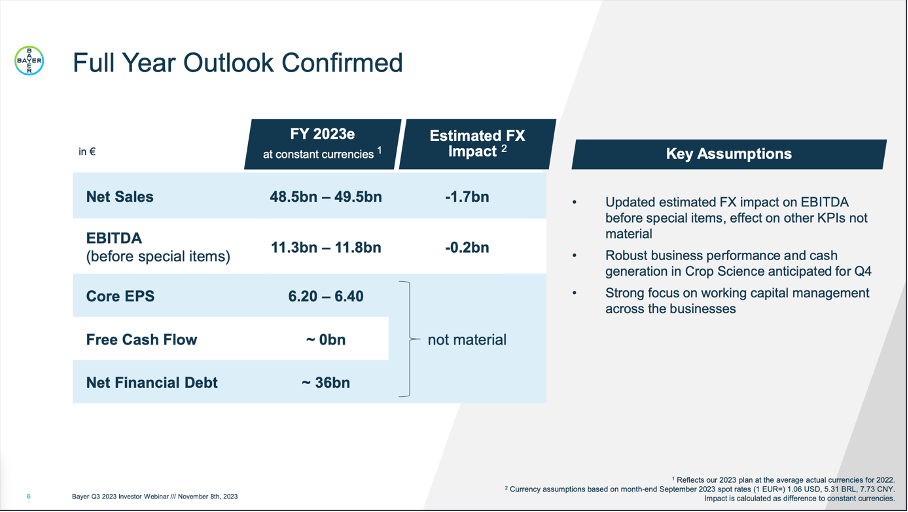

Additionally, Bayer confirmed the outlook the company had published in its half-year financial report. Management is still expecting net sales to be between €48.5 billion and €49.5 billion for the full year and core earnings per share to be in the range of €6.20 to €6.40. And free cash flow is expected to be zero for the full year.

The Future of Bayer

And this brings us to another important topic - the discussion about the future of Bayer. CEO Bill Anderson said during the last earnings call :

Nearly €50 billion in revenue, but zero cash flow is simply not acceptable, nor is the trajectory of our share price. So the status quo is simply not an option for Bayer. And I've spoken to many of you about this. We share the belief that there is no quick fix for the multiple challenges that Bayer is facing. We are committed to the fastest path to value creation. This is super important.

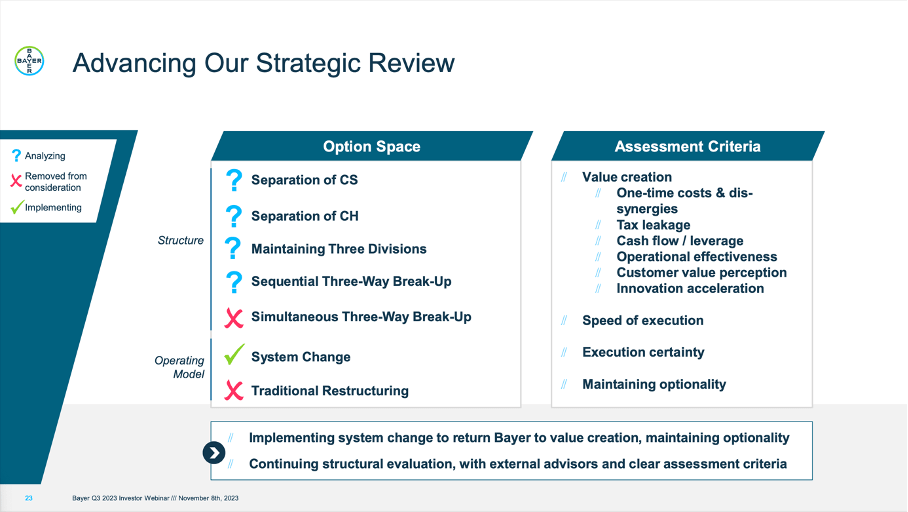

Right now, there seem to be several different options on the table - from maintaining three divisions (similar to the current business structure of Bayer) to breaking up the company entirely into three different businesses.

{kind=link}

And it also seems to be a possibility for Bayer to split up into three different businesses - according to the three business segments. However, management has ruled out a simultaneous three-way break-up meaning the separation into three businesses would happen at least in two separate steps:

For example, we considered simultaneously splitting the company into three businesses. We're ruling that option out. It's just not feasible to do that all at once. A three-way split would require a two-step process. And we certainly will not pursue any structural moves that would come with a downgrade of our operational performance.

{kind=link}

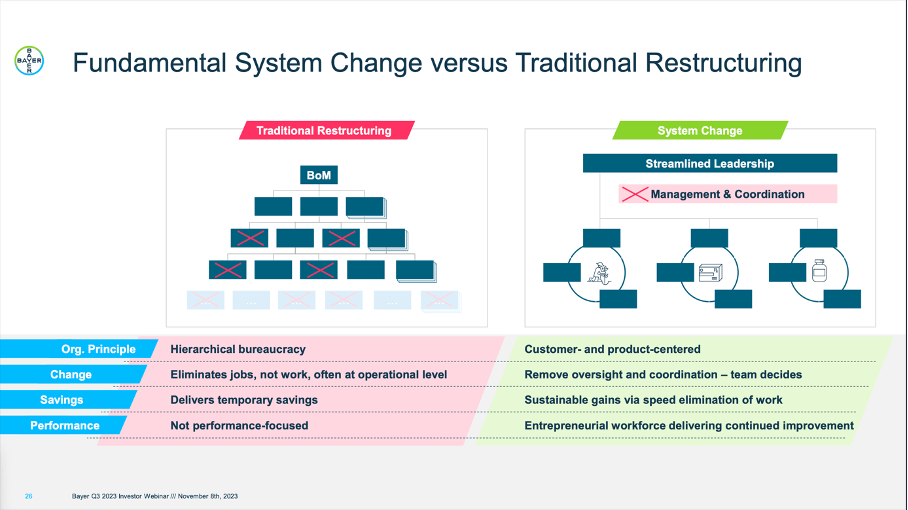

Aside from the different options breaking up the business, Bayer already implemented a "system change". During the last earnings call, Anderson was complaining about Bayer being rather inefficient and mentioned several examples. To be honest, Anderson painted the picture of a huge, sluggish, and very inefficient business:

But let me give you an example of what I say about administrative controls. So the company has 1,362 pages of Bayer-specific central rules and regulations. They even have a special name. And seriously, we have resources dedicated to promulgating these 1,300 pages of rules all around the world to every Bayer employee. Well, we're going to consolidate that dramatically. We're going to reduce it by 99%.

And maybe he is correct. It is difficult to assess from the outside how efficient Bayer is, but according to the numbers the business had to report in the last eight years, Bayer was a huge disappointment, and it is difficult to argue for a well-run business. It seems like Anderson is making really big efforts to make Bayer more efficient again. During the earnings call, he also stated:

So first, we're going to focus everything on the mission. Second, we're driving innovation; and third, we're going to strengthen performance. And I'm going to go through those one by one.

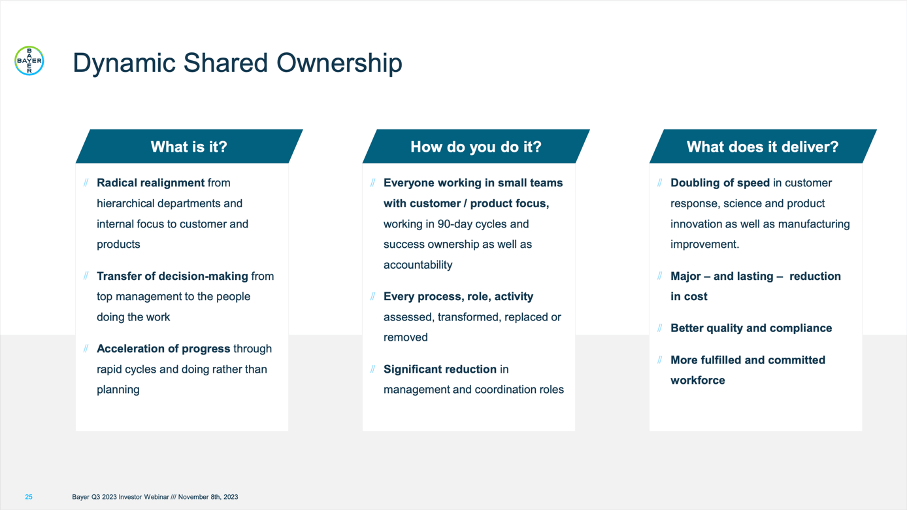

Among the changes Anderson is trying to make (or already has made) is a new incentive system that will be discussed at the 2024 Annual General Meeting. Additionally, he criticized that Bayer is spending too much time on planning, forecasting and target setting and the time high-qualified people are spending on these tasks will be cut by 80%. Additionally, Anderson is focusing on the strategy of "Dynamic Shared Ownership" to transform the decision-making progress within Bayer.

{kind=link}

In the future, everyone at Bayer will work in small self-managed teams and progress will be measured in rapid 90-day cycles.

And we should not assume high growth rates for Bayer in the years and decades to come. The company is a 160-year-old business that won't suddenly turn into a growth company delivering double-digit returns. Nevertheless, the company has the ability to return to solid mid-single digit growth. In the years between 1980 and 2015, Bayer could grow its revenue with a CAGR of 3.33% and earnings per share with a CAGR of 5.46% - and we should not forget businesses like LANXESS Aktiengesellschaft ( LNXSF ) (being worth €2 billion) and Covestro AG ( CVVTF ) (being worth €9 billion) that were spun-off during that timeframe.

Breaking Up The Business?

I personally don't assume Bayer will be split up and I rather think Anderson will try to restructure the business in some other ways. Nevertheless, let's analyze a breakup a little bit and the consequences of such a scenario.

Let's assume that management will split up Bayer into three different businesses - even if such a process will take time and cannot be done at once as CEO Anderson pointed out. In my opinion we have two solid businesses on the one side - the pharmaceutical business as well as the consumer health business - and on the other side the crop science business, which is the most interesting as it has potential but is posing major risks.

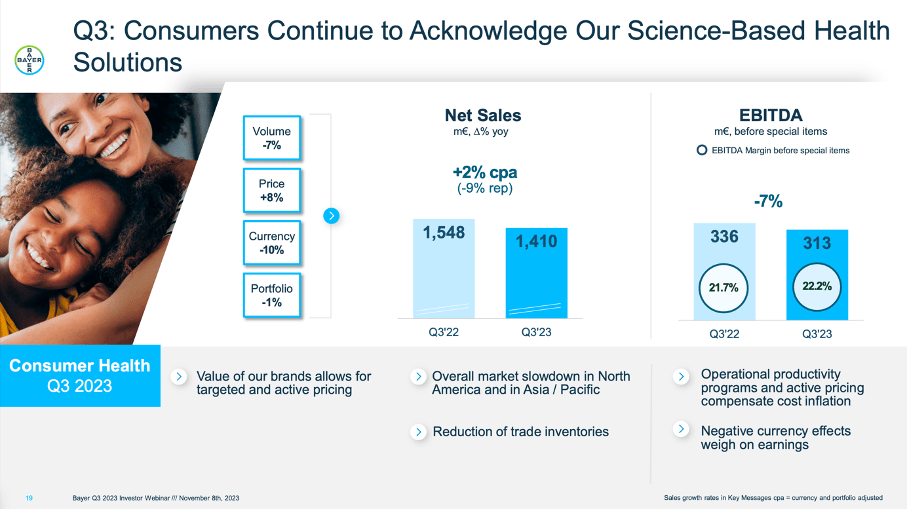

In Q3/23, Consumer Health had to report a revenue decline of 8.9% YoY to €1,410 million in revenue. However, adjusted for FX effects and portfolio, the segment could grow 1.7% YoY. And in this case, volume declined 6.5% while prices increased 8.2%. EBITDA still declined 8.1% year-over-year to €305 million but at least the segment is generating solid profits for Bayer.

{kind=link}

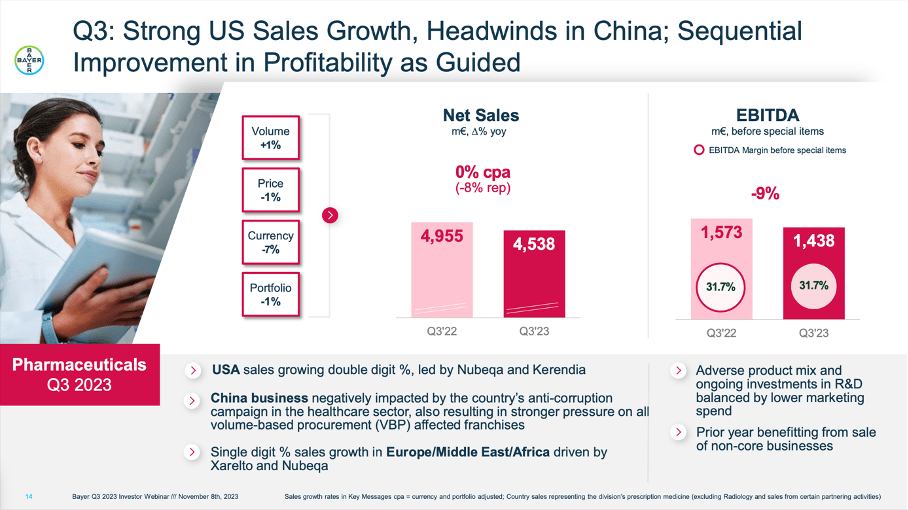

And when looking at Pharmaceuticals the picture is similar in Q3/23. Reported sales declined 8.4% YoY to €4,538 million, but when adjusting for FX and portfolio, revenue declined only 0.3% YoY. In this case, volume increased slightly (0.7%) while prices declined slightly (-1.0%). And EBITDA also decreased 5.4% year-over-year, but the business contributed €1,420 million to overall profits.

{kind=link}

The most interesting business segment is "Crop Sciences". And when trying to break up Bayer in three different businesses, "Crop Sciences" would be similar to a bad bank - a new company with problematic and non-performing assets that are a burden for the main business. In the case of Bayer, we are talking about the different lawsuits that are mostly affecting the crop science business. Aside from some other lawsuits - like shareholders suing Bayer for the damages suffered due to the drop in the company's share price following the Monsanto acquisition - we are mostly talking about the claims against the former Monsanto business. Right now, there are about 165,000 claims in total of which 113,000 have been settled or at not eligible for various reasons.

By the way, other companies have tried similar steps - excluding the problematic part of a business that is affected by major lawsuits and leading that part of the business into bankruptcy to avoid huge settlement costs for the main business. 3M Company ( MMM ) as well as Johnson & Johnson ( JNJ ) would be two major U.S. corporations that tried a similar move (see here for a bit more information).

But "Crop Sciences" is not only facing major problems, it is also the segment that is offering growth potential for Bayer in the years to come. As I have written in many articles in the past, we can identify several megatrends that are a tailwind for Bayer. In my last article, I wrote:

Additionally, the growing population by itself is also a huge megatrend. Bayer is expecting 50% more food and feed required to meet the growing demand and innovations in crop sciences will be needed. The situation will be worse due to expected pressures on the ecosystem. Bayer is expecting 17% harvest losses from climate change and to keep up with demand for food, crop sciences products will be needed even more.

And we should not ignore the growing market that will be the result of these megatrends.

{kind=link}

And despite all troubles and lawsuits surrounding Bayer and especially its crop science business, we should also not ignore the leading position the company has.

{kind=link}

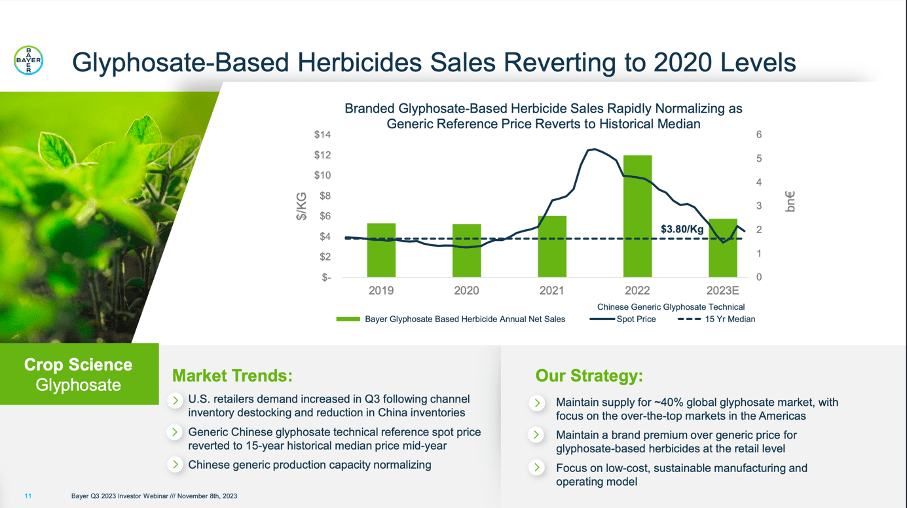

When looking at third quarter results we see - similar to the other two segments - sales declining. Revenue declined 7.0% YoY to €4,365 million however in FX and portfolio adjusted numbers, Crop Sciences could report 0.6% year-over-year growth. And while volume increased 25.0% year-over-year (which is impressive), prices declined 24.4% year-over-year. Among the different "Strategic Business Entities" within the Crop Science segment, it was especially herbicides being a problem for Bayer: Sales declined 21.0% year-over-year (17.3% when adjusting for FX and portfolio).

{kind=link}

And while a 24.4% price decline seems like a huge problem, we have to put these numbers into context and look at the bigger picture. Right now, prices for glyphosate-based herbicides are in line with the 15-year median and 2021 and 2022 were rather an outlier and in 2023 prices are returning to "normal" levels again.

Bottom Line

If Bayer shareholders could only keep the Pharmaceutical and Consumer Health business and the company is able to spin off the Crop Science business, it might be positive news and might have a positive effect on the share price. We can assume that these two business segments by themselves will be worth more than the current stock price of Bayer. Nevertheless, we must ask ourselves how likely such a spin-off is because Bayer either needs a buyer for the segment or does an IPO. And in both cases, investors are needed and it seems unlikely at this point to find investors that are willing to buy the business with tens of thousands of unresolved lawsuits for an acceptable price.

Nevertheless, I remain optimistic that Bayer is able to resolve its legal issues and the stock is clearly undervalued as long as we are ruling out the risk of bankruptcy. In my opinion, Bayer remains a "Buy" as the entire business is worth more than €40 per share. In my last article I calculated an intrinsic value of €92 for Bayer and although this might seem too optimistic for many, I still think the assumptions made in my last article are realistic and Bayer should be worth more than it is trading for today.

For further details see:

Breaking Up Bayer? Probably Not!