PFE - Bristol-Myers Squibb: Big Dividend Yield Unloved Big-Pharma Deal

2024-01-12 10:12:55 ET

Summary

- I discuss a cheap Big Pharma stock and its performance in the market.

- I provide an overview of the stock's history, including its R&D cycle, dividend and yield on cost history, and valuation.

- With Eliquis generating $11.78 Billion in revenue and Opdivo $8.24 Billion, that's almost $20 Billion in revenue at stake that needs to be slowly replaced.

- Bristol Myers seems to be carefully charting the company's future pipeline and are very cognizant of the urgency to do so.

Yet another cheap Big Pharma stock

Having recently written about the cratered pharma stock and value opportunity in Pfizer ( PFE ), charting the big pharma sell-offs, reveals a nearly as strong downtrend in Bristol-Myers Squibb ( BMY ). The company is in a similar phase of R&D cycling and acquisitions to fill its next cycle of drugs for the next decade. Bristol Myers does not have the stigma around it from being a vaccine producer during COVID-19, but they also have their issues to reckon with.

The main issue for the company at current is the 2028 expiration of patents surrounding a couple of popular drugs. Regardless of that, Bristol Myers is attractively priced with a currently well-covered 4+% dividend to boot. Bristol Myers is a buy here and a good entry point if you are building a portfolio slice centered around a reversion to value. Healthcare and related picks have been the oft-mentioned 2024 rotational themes, amongst others.

The story up to here

This is a stock that had been GAAP negative yet non-GAPP positive for some time.

The interesting observation is that price was flat during the 2020-2021 period, whilst GAAP earnings were negative. Once they turned positive, prices spiked above $70 a share but have now reverted to a level well below the negative GAAP earnings period. Market anomalies like these are attractive from my point of view.

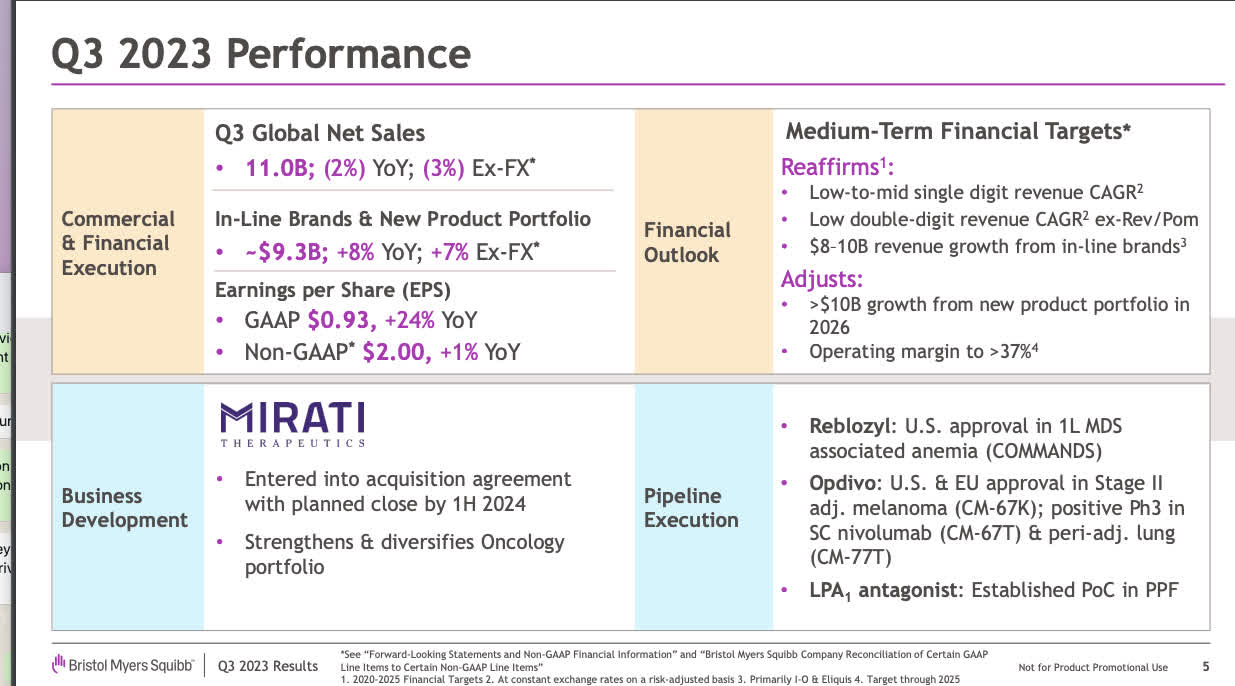

Q3 updates

{kind=link}

It exhibited solid Q3 performance in my view. Most important is the re-affirmation of low-to-mid single-digit revenue CAGR. Not huge, but not a negative revision when compared to the aforementioned Pfizer where several analysts are expecting negative revenue growth in 2024 with an average estimate of roughly +1.7%.

{kind=link}

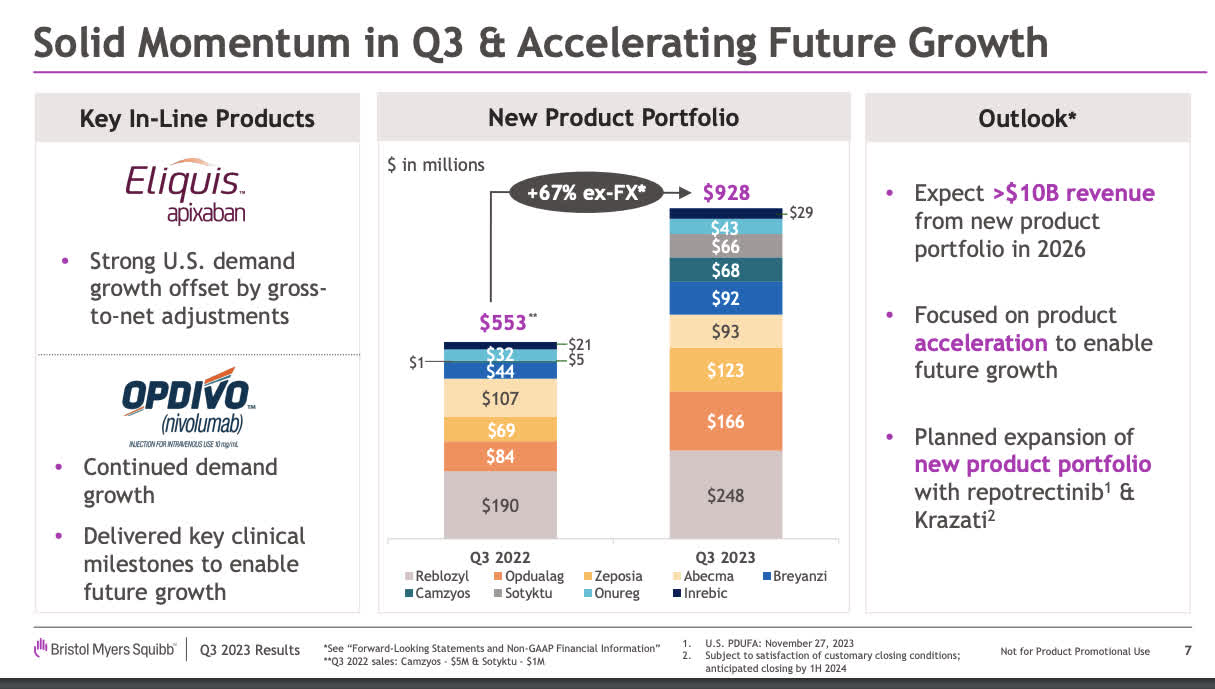

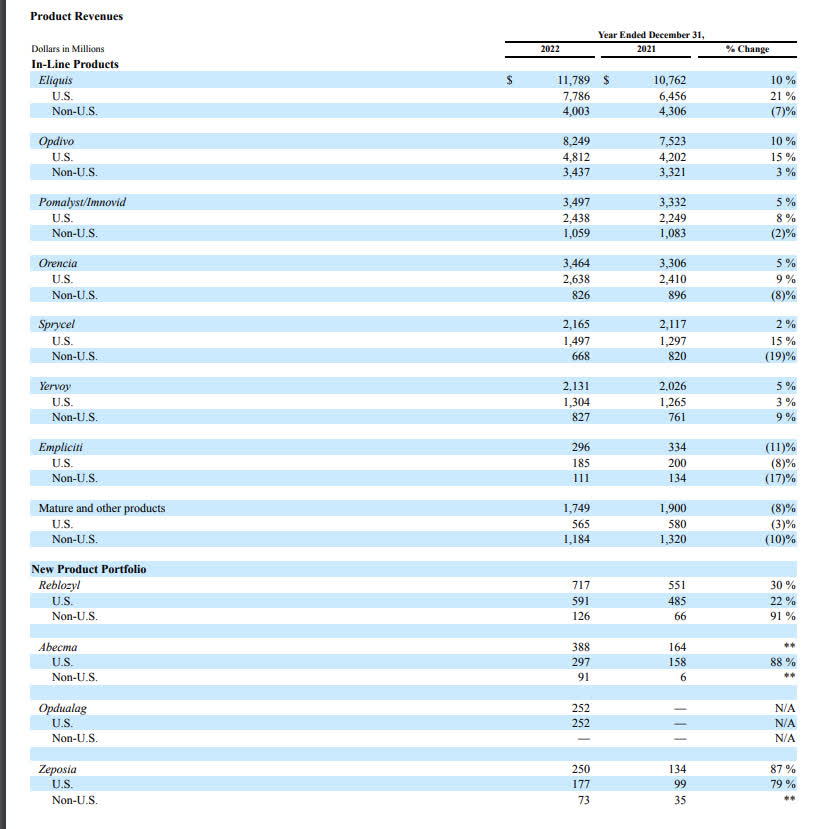

The key in-line products that Bristol Myers highlights in the presentation regarding the company's strongest demand products are the very products that are set to have patent expiration by 2028. We can expect large decreases in revenue amongst those two products, with a switch by many users to generics.

The new product portfolio of Reblozyl, Opdualag, Zeposia, Abecma, Breyanzi, Camzyos, Sotyktu, Onureg, and Inrebic are growing to the tune of +67% quarter over quarter. The new product portfolio generates nearly $1 Billion in revenue per quarter, with expectations to have $10 Billion in revenue for this portfolio by 2026.

With Eliquis generating $11.78 Billion in revenue and Opdivo $8.24 Billion, that's almost $20 Billion in revenue at stake that needs to be slowly replaced. If they lose only half the revenue to generics, the revenue would be possibly supplemented adequately by the new portfolio if growth estimates hold up. These two expiring drugs are amongst the sector's biggest in the next 5 years.

With the aim to hit 37% operating margins, a $10 Billion hit to revenue could mean a $3.7 Billion hit to operating income.

Percent off high

Depending on which drugs and therapeutics you are in as large-cap pharma, you are either adored or hated. Bristol Myers seems to be at least the second most hated of the big pharma stocks after Pfizer. Down -36.5% from the high, let's see if the price has now submerged below the decade earnings growth rate.

Heat check

Here we can see over the past decade that EPS has grown 145% compared with a negative -12.81% price decline. The earnings have been very cyclical, as you can see from the jagged earnings growth chart, but have grown nonetheless. As Bristol Myers is looking for further avenues to secure sustainable growth, as mentioned in their Q3 earnings report, evening out this line is essential to remain a good, long-term hold.

With both EBITDA and GAAP EPS near all-time decade highs, the negative -12% growth rate in price seems unwarranted. If earnings can even simply hold the line for the next few years, there is a big gap between the two metrics.

R&D cycle

As you can observe in several pharmaceutical stocks that have volatile R&D cycles, spikes in R&D spending result in lulls for return on invested capital [ROIC].

Seeking Alpha

Looking at the forward numbers for the FWD P/E to Non-GAAP, 6.73 X is equivalent to an earnings yield of 14.85%. Charlie Munger had often said that long term, you will not do much better on a stock on an annual basis than the stock's return on invested capital. Currently, at 11.89%, the price has cratered to a point where the non-GAPP return on share price earnings yield is now above the company's return on capital.

The GAAP forward earnings yield is only 7.4% or a 13.37 P/E, but as we'll see later, Bristol Myers is a company that has far more depreciation and amortization than they do capital expenditures. In these cases, non-GAAP can often be a more accurate depiction of the current situation.

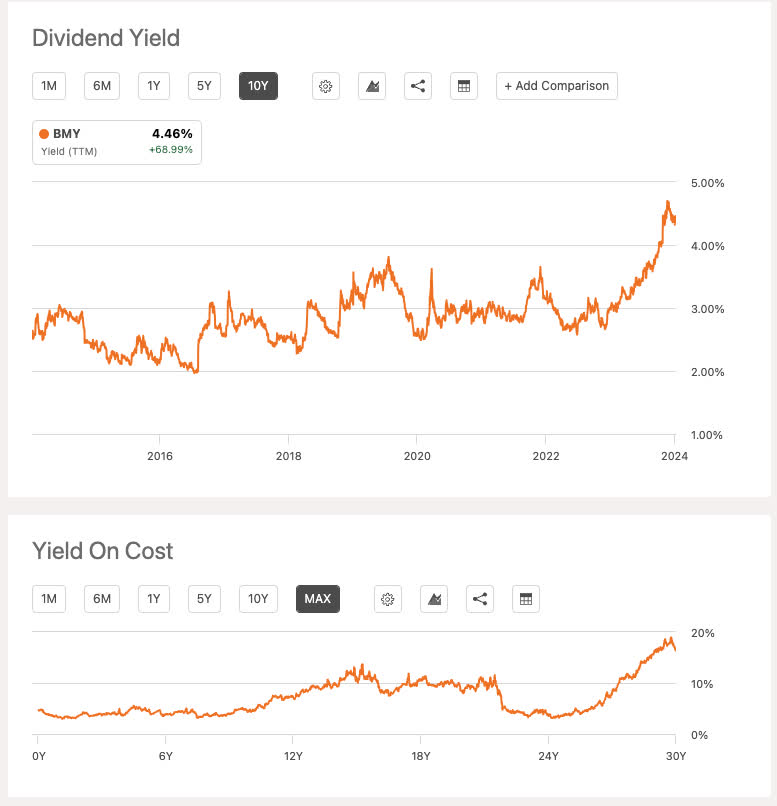

Dividend and yield on cost history

{kind=link}

Having paid and raised their dividend for 7 years, the company is not a dividend aristocrat, but looking at the yield on cost trends over long periods, the trend is normally up on most entry points. 30-year holders are being treated to a near 20% dividend yield on cost. Not bad even though the price action has been sideways.

Dividend coverage

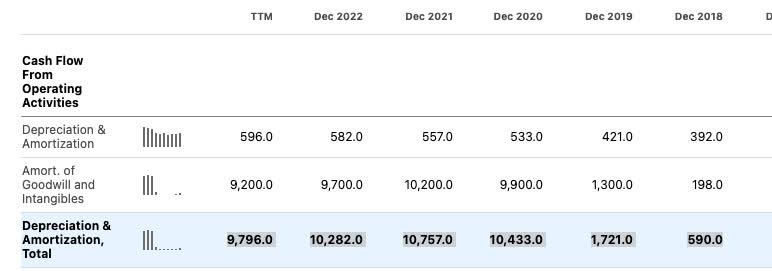

There is currently ample dividend coverage, and we can see that free cash flow growth has straddled the line of dividends per share for the most part. The ample current coverage will probably last for the next few years until the accelerated amortization of non-cash items is worked through. We'll see that normalized 5-year depreciation and amortization is quite a bit lower than what we are currently seeing later in this article.

Valuation

Using a Warren Buffett "Owner Earnings" model to get to a fair value, we'll take a look at the current value. This is a basic discounting of free cash flow. Here, I will use the 5-year average for depreciation and amortization rather than the TTM numbers. We can see that the company is going through a massive spike in these non-cash items that need to be normalized. This spike is most likely due to accelerated amortization of the two leading drugs expiring in the not-too-distant future.

{kind=link}

I am also adding a couple of points to the risk-free rate. Buffett was known to do this if risk-free rates were too low or cash flow and earnings were too unstable. Looking at the jagged earnings growth line, at least 2 extra percentage points, if not more, is warranted.

All numbers TTM in millions courtesy of Seeking Alpha

Current

- Net Income= $8,285

- Plus average 5 year Depreciation and Amortization = $8,285 + $7,263=$15,548

- Minus CAPEX= $15548-$1225=$14,323

- Minus other TTM cash expenses related to acquisitions=$14323-$704=$13,619

- Discounted at risk-free rate of 5.5%+2%[7.5%]=$181,586

- Divided by shares outstanding = $181,586/2034= $89/share

- Selling at 56% of fair value.

Karuna acquisition

Fresh off the December presses :

Bristol Myers Squibb and Karuna Therapeutics, Inc. today announced that they have entered into a definitive merger agreement under which Bristol Myers Squibb has agreed to acquire Karuna for $330.00 per share in cash, for a total equity value of $14.0 billion, or $12.7 billion net of estimated cash acquired. The transaction was unanimously approved by both the Bristol Myers Squibb and Karuna Boards of Directors.

Karuna is a biopharmaceutical company driven to discover, develop and deliver transformative medicines for people living with psychiatric and neurological conditions. Karuna’s lead asset, KarXT (xanomeline-trospium), is an antipsychotic with a novel mechanism of action (MoA) and differentiated efficacy and safety. Karuna’s New Drug Application (NDA) for KarXT for the treatment of schizophrenia in adults was accepted for review by the U.S. Food and Drug Administration (FDA), with a Prescription Drug User Fee Act (PDUFA) date of September 26, 2024. KarXT is also in registrational trials both for adjunctive therapy to existing standard of care agents in schizophrenia and for the treatment of psychosis in patients with Alzheimer’s disease. Bristol Myers Squibb believes KarXT represents a significant revenue contribution opportunity. Bristol Myers Squibb also sees potential from Karuna’s early-stage and pre-clinical pipeline.

The transaction is expected to close in the first half of 2024, subject to customary closing conditions, including approval of Karuna stockholders and receipt of required regulatory approvals.

Again, this is another growth angle, not chasing the hot weight loss drugs that I am avoiding. GLP-1 drug growth chasing has become euphoric. There are still strict doctor guidelines before getting the weight loss drugs prescribed, rather than just grabbing it at a local Walmart over the counter.

Schizophrenia and Alzheimer's are very important areas of health to address with the prolonged life span of human beings. This is a good growth avenue to go after in my opinion.

2028 Patent loss risks

From the most recent 10K:

{kind=link}

{kind=link}

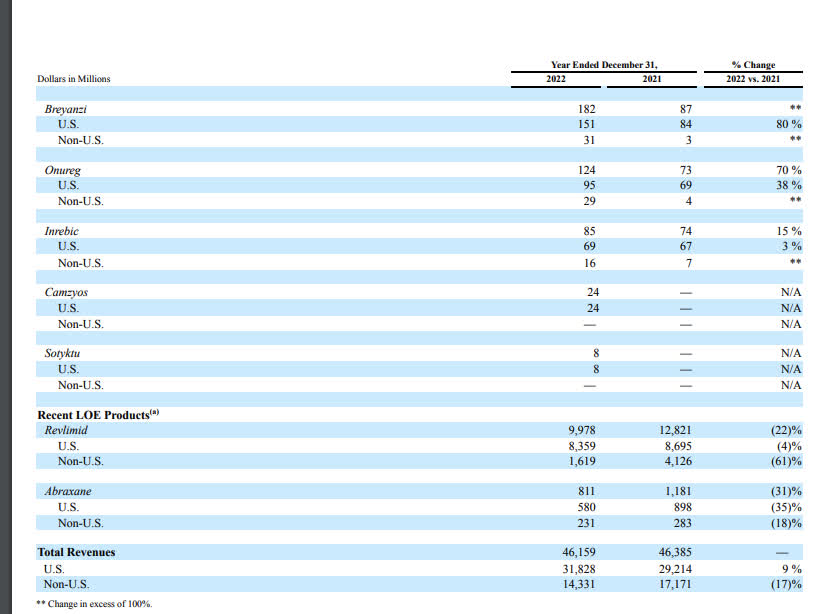

- Eliquis revenue:$11.789 Billion

- Opdivo revenue: $8.249 Billion

- Total revenue for period: $46.159 Billion

- Total percentage for both products of revenue: 43%

No doubt about it, this percentage of revenue is massive. New acquisitions and the new existing portfolio should make up for shortfalls come the expirations, but margins will not be as stable for new products as ones that have been in the pipeline for this long. This is the biggest risk and problem the market sees with the stock.

Again, much of the great cash flow numbers that we are picking up have to do with some accelerated amortizations related to expiring drugs, once those make their way through the system, it may get more difficult to justify some of these discounted earnings numbers, and price targets.

Balance sheet

Total current assets are more than $10 Billion below debt. This is not the most pristine balance sheet, but EBIT is still in excess of net interest payments on a TTM basis of 12.18 X.

Share buybacks have normalized after the spike and dilution in 2019. This is indicative of a return to stabilization.

Summary

The stock is undervalued and has ample dividend coverage with a 4+% yield. They seem to be carefully charting the company's future pipeline and are very cognizant of the urgency to do so. On the flip side, the non-cash add-backs are probably too generous taking into consideration the current situation. While $89/share is probably too high of a price target with headwinds and future product replacement uncertainty, Bristol Myers is certainly worth more than $50/share. Buy.

For further details see:

Bristol-Myers Squibb: Big Dividend Yield, Unloved Big-Pharma Deal