CA - Bristol-Myers Squibb's Recent $20bn M&A Spree Should Reward Patient Investors

2024-01-03 17:17:52 ET

Summary

- Bristol-Myers Squibb Company experienced a poor year in terms of share price performance in 2023, with a 27% decline in value.

- Bristol-Myers has focused on its late-stage pipeline and made several recent acquisitions geared towards offsetting losses from patent-expired drugs.

- The company's new product portfolio, bolstered by 3 multibillion dollar recent acquisitions, has the potential to drive future revenue growth and share price recovery.

- As the likes of Revlimid, Pomalyst Eliquis, and Opdivo's patents expire and revenues from these sources fall, new products will come to the fore.

- The acquisition of Karuna Therapeutics schizophrenia drug, Mirati's lung cancer portfolio, and RayzeBio's radiopharmaceuticals pipeline paints Bristol-Myers in a more positive light ahead of a critical year.

Investment Overview

Bristol-Myers Squibb Company ( BMY ), the Princeton, New Jersey-based Big Pharma concern, experienced a poor year in terms of share price performance in 2023.

BMY is currently the seventh largest of the "Big 8" U.S.-headquartered global Pharmas, with a market cap of ~$107bn at the time of writing. Eli Lilly ( LLY ) is the largest by market cap, worth ~$562bn, followed, in descending order by market cap valuation, by Johnson & Johnson ( JNJ ), Merck & Co ( MRK ), AbbVie ( ABBV ), Pfizer ( PFE ), Amgen ( AMGN ), and Gilead Sciences ( GILD ) - market cap of ~$103bn.

Although BMY was not the worst-performing of these companies in terms of stock price performance last year - Pfizer's 42% 12-month loss saved its blushes (read my SA note on Pfizer's abysmal year here ) - its 27% decline in value was the second worst. No other company lost >10% of its share price value last year, while Lilly stock posted a 12-month gain of >60%.

What this goes to show is that while these 8 companies - and international rivals such as Denmark headquartered Novo Nordisk ( NVO ), Swiss Based Novartis ( NVS ) and Roche (

RHHBY), French Pharma Sanofi ( SNY ), UK based GSK ( GSK ), and Anglo / Swedish firm AstraZeneca ( AZN ) - have similar business models - developing, manufacturing and selling therapeutic drugs - the market may treat their stock very differently depending on its perception of what their future performance may look like.

The market tends to be more interested in what financial performance will look like in 2-3, or even 5-10 years' time, which explains why a company like Pfizer, which earned >$100bn revenues in 2022 thanks to its COVID drug franchise but is guiding for just $58-$61bn in 2023, is valued 2.5x less than Lilly, which posted revenues of just $28bn in 2022, but is expected to earn peak revenues of perhaps >$50bn per annum from its "miracle" GLP-1 agonist drug franchise , led by Mounjaro in Diabetes and Zepbound in weight loss.

BMY's End Of Year M&A Spree Explained - An Attempt To Silence The Doubters?

BMY markets and sells a smaller portfolio of drugs than many of its Big Pharma rivals - the company reports quarterly revenue figures for just 18 commercialized drugs currently - although 10 of these are "blockbuster" drugs, i.e., they earn >$1bn per annum, and several are what might be termed "mega-blockbusters."

{kind=link}

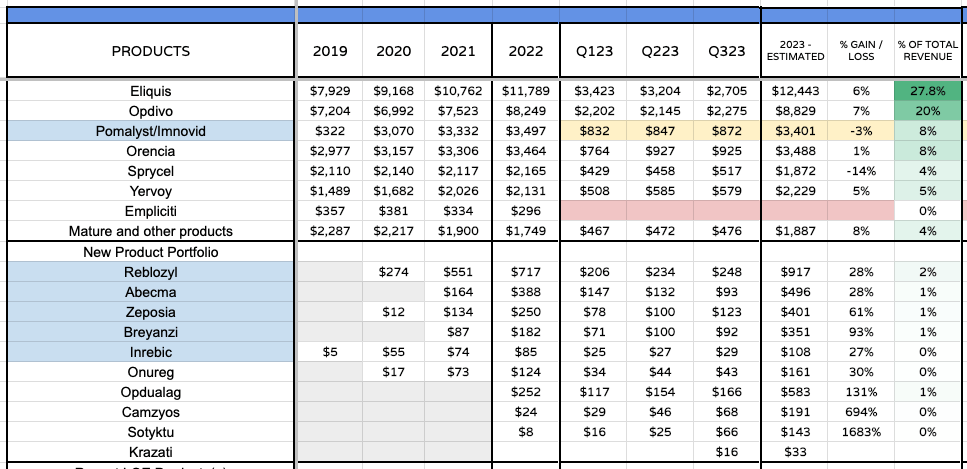

The anti-coagulant Eliquis, for example, earned $12.4bn revenues in 2022, and looks on track to exceed that figure in 2023. The immune checkpoint inhibitor Opdivo - indicated for a range of solid tumor cancers - earned $8.2bn in 2022, a figure which may tick higher in 2023, while BMY's 2019, $74bn acquisition of Celgene gave it access to the multiple myeloma drugs Revlimid - which earned >$12bn in 2020 and 2021, and $10bn last year, and Pomalyst, which earned $3.5bn of revenues last year.

The major problem on BMY's horizon - and the primary reason the market has been selling BMY stock - is that Revlimid, and now Pomalyst, have lost their patent protection, meaning they are subject to generic competition. Generics are copycat versions of branded drugs that are permitted to be sold after the branded drug's patents expire. They can be marketed at a much cheaper price point by generic drug companies who have no R&D costs to fund, and typically lead to the branded drugs' sales falling by 25% - 30% per annum.

Revlimid and Pomalyst are not BMY's only patent-expiring drugs, either - Eliquis is set to lose its market exclusivity in 2027, and Opdivo in 2028. These four drugs represented ~73% of BMY's entire revenues in 2022, so perhaps it is easy to see why the market is concerned.

Nevertheless, across the past few years BMY has been focused on its late stage pipeline, securing commercialization for 5 major new pipeline drugs acquired from the Celgene deal - anemia / beta thalassemia therapy Reblozyl, multiple myeloma cell therapy Abecma, auto-immune drug Zeposia, b-cell lymphoma cell therapy Breyanzi, and myelofibrosis drug Inrebic.

On top of that, BMY has secured approvals for in-house drugs Onureg, an acute myeloid lymphoma therapy, opdualog, indicated for melanoma, and sotyktu - a plaque psoriasis therapy which some analysts have speculated could earn $8bn - $10bn in peak sales, having shown superiority to Amgen's current standard-of-care Otezla in clinical studies.

Finally, BMY has added some bolt-on acquisitions - in 2020, the company paid ~$13bn to acquire Myokardia and its heart failure therapy Mavacamtem, which is now approved under the brand name Camzyos to treat obstructive hypertrophic cardiomyopathy. BMY management believes this therapy could realize >$4bn in peak annual sales.

BMY has previously promised to extract $10 - $13bn in risk adjusted sales of these newly approved products by 2025, and $25bn by 2030, with Camzyos, Opdualog, Sotyktu and Reblozyl all pegged for >$4bn revenues in 2030, Breyanzi and Zeposia >$3bn, and Abecma >$1bn. That figure is not far off the $33.5bn earned by Eliquis, Opdivo, Revlimid and Pomalyst in 2022, and of course, these 4 drugs still have major revenue contributions to make, even as they approach patent expiration.

Despite all of these new approval wins, however, it's clear the market still isn't buying the BMY story. Timothy Power, BMY's Vice President and Head of Investor Relations admitted as much during a November fireside chat at the Jefferies London Healthcare Conference, commenting:

if I just take a step back where we are right now, clearly the company is going through an important patent cycle at the moment and the market is obviously focused on that understandably.

I think though, if we sort of put that in context, thinking about the fact that this isn't the first time Bristol has gone through a patent cycle, and frankly, we've seen some other companies more recently go through something similar and come out very strong on the other side. I think it's important to remember that we're going into this actually with some real advantages in some ways.

Despite management's belief in the plans it has put in place for its new product portfolio, in the past few months it has clearly decided to pursue a more aggressive merger and acquisition ("M&A") strategy in order to bolster its late stage drug development portfolio still further, and eventually offset an even larger portion of its likely losses related to patent expired drugs.

In October, BMY completed a buyout of Mirati Therapeutics ( MRTX ), paying $58 per share, or ~$4.8bn for the oncology specialist, plus non-tradeable contingent value rights related to the approval of its drug candidate MRTX1719, a PRMT-5 inhibitor indicated for MTAP deleted cancers, which will enter a Phase 2 study in solid tumor indications such as nom-small cell lung cancer ("NSCLC"), bile duct cancer and melanoma next year.

The rights could add an additional $1bn to the value of the deal, valuing it at close to $6bn. Mirati's other product of significance is Krazati, already approved to treat KRAS mutated NSCLC, which could achieve "blockbuster" revenues, analysts have speculated , although the drug earned only $16m of revenues in 2023, to Q3.

More recently, on December 22nd, BMY announced the acquisition of central nervous system ("CNS") disease specialist Karuna Therapeutics ( KRTX ) in a $14bn deal, paying $330 per share. Karuna has no approved drugs, although its lead asset, KarXT (xanomeline-trospium), an antipsychotic with a novel mechanism of action (MoA), being an M1/M4 receptor agonist, has an FDA approval decision pending in September this year, in Schizophrenia.

BMY is confident the drug will be approved in schizophrenia and is also targeting additional approvals in indications such as Alzheimer's disease psychosis and bipolar disorder. If that were to happen, analysts have speculated peak sales could exceed >$6bn per annum.

Finally, BMY also announced in December that it would acquire newly IPO'd radiopharmaceuticals specialist RayzeBio ( RYZB ) in a deal worth $62.5 per share, or ~$4.1bn. Radiopharmaceuticals is an exciting new field of drug development in which radioisotopes bound to biological molecules are able to target specific organs, tissues or cells, and Rayze's lead candidate RYZ101, which targets somatostatin receptor 2 (SSTR2), has already entered into a Phase 3 study in patients with "GEP-NET" cancers, which can affect the pancreas or stomach. Small cell lung cancer is another target, and 2 other candidates target liver cancer, and renal cell cancer.

BMY's New Products Failing Short-term Expectations, But Could Thrive Long Term With Fresh M&A Impetus

In total, BMY spent nearly $23bn on M&A in a little under 3 months. None of the Pharma's deals appear to have been widely anticipated, although the rationale behind each is clear.

Mirati's portfolio supplies an already approved drug in Krazati, and lends a more innovative edge to an oncology division heavily reliant on multiple myeloma therapies. Karuna's KAR-XT has long been thought to be a potential standard of care in CNS disease, with a strong efficacy and safety profile, and peak sales expectations >$5bn, and the buyout of Rayze - similar to Mirati, future-proofs the oncology pipeline.

During the Jefferies fireside chat, Head of IR Power was forced to defend BMY against the accusation the pharma was falling behind in oncology as a result of not developing antibody drug conjugates - AbbVie ( ABBV ) snapped up Immunogen and its approved - in ovarian cancer - ADC Mirvetuximab Soravtansine, now marketed as Elahere, in a $10bn deal in November.

For good measure, BMY has also entered that space too, announcing an "exclusive license and collaboration agreement for SystImmune’s BL-B01D1, a potentially first-in-class EGFRxHER3 bispecific antibody-drug conjugate" last month - according to the terms of the deal:

Bristol Myers Squibb will pay SystImmune $800 million in an upfront payment and up to $500 million in contingent near-term payments. SystImmune is eligible to receive additional payments of up to $7.1 billion contingent upon the achievement of certain development, regulatory and sales performance milestones for a total potential consideration of up to $8.4 billion.

Perhaps BMY's spree could be interpreted as incoming CEO Chris Boerner putting his stamp on his new leadership position after the departure of Giovanni Caforio, who had been at the helm for 8 years. The new CEO may have trying to please shareholders after reporting on the slightly underwhelming 9-month sales of new products in 2023 - the company has forecast for ~$3.5bn of revenues in FY23, and postponed the date by which it believes new product revenues will exceed >$10bn per annum from 2025, to 2026.

The incoming CEO, on BMY's last earnings call , attributed underperformance to teething problems marketing products such as Abecma and Zeposia, but also suggested it was a matter of "when, not if" sales began to match management's ambitious targets.

If that does happen, then based on my forward revenue modelling, BMY should be able to grow revenues in 2024 and 2025, perhaps >$50bn in the latter year, achieving its promise of low-to-mid single digit revenue CAGR between 2020 - 2025, and low double-digit revenue CAGR ex-Pomalyst and Revlimid revenues.

Although BMY will then face challenges after 2025, including the patent expiration of eliquis circa 2026, and opdivo circa 2028, the momentum of the new product division - which remember, has now been bolstered by a commercial stage asset with supposed blockbuster revenue potential, and a late stage pipeline asset supposedly with peak revenue expectations of >$5bn, plus another late stage radiopharmaceutical asset - can ensure the company keeps growing, even as the revenue contributions from Opdivo and Eliquis fall drastically.

Management does have plans in place to find a replacement drug for Eliquis, in Milvexian, a Phase 3 stage anti-thrombotic Factor XI inhibitor, which IR Head Power commented in November is hoped will have "efficacy that's the same if not better than existing Anticoagulant like 10As, but a better bleeding profile."

BMY also has a strategy in place for opdivo, attempting to develop and secure approval for a subcutaneously administered form of opdivo, which could presence a substantial chunk - likely one third or higher - of the drug's revenue streams post patent expiry, as the subq version would remain patent protected, and represents a more convenient option for patients versus intravenous infusion.

And finally, BMY has multiple other late stage assets close to approval - Augtyro in NSCLC, Iberdomide in multiple myeloma, candakimab in eosinophilic esophagitis, for example - further de-risking the company against underperformance of any member of its new product portfolio.

Looking Ahead: Debt & Patent Issues Are Red Flags To BMY Bulls - But It May Not Be Time To Take Flight Yet

To conclude this post, I believe there are two different contexts in which BMY's November / December M&A Spree can be interpreted. The first is as a knee-jerk reaction by an incoming CEO to underperforming sales of new products, and an attempt to curry favor with shareholders, which lacks long-term viability.

The second - and the conclusion I would make - is that these could be the right deals at the right time for a company which already has excellent cash flow generation - ~$14bn, $16bn, and $10bn across the past 3 years - and now, a genuine shot at solving its patent expiry issues while continuing to grow its top line.

Debt remains a concern at BMY - as of Q3 2023, the company reported its current portion of long-term debt to be $4.87bn, and its actual long-term debt to be $32bn, so an additional ~$23bn of outgoings in the last quarter of 2023 has surely cranked up the pressure on the company to maintain its investment grade rating.

On the other hand, with interest rates widely predicted to fall - 3 cuts are apparently planned for this year - and as mentioned, exceptional cash flow - and operating margins forecast by management to grow to >37% by 2025 - maintaining its debt at manageable levels may not be an issue that weighs too heavily on the company.

Certainly, based on my research, if BMY's new product portfolio, bolstered by these latest acquisitions, can meet management's expectations - or even fall just short of them - the Pharma ought not to have to struggle to keep growing the business, and top line revenue growth - provided it is sustainable in the market's eyes, i.e., Lilly's diabetes / weight loss drugs - is generally correlated closely with share price growth.

I don't think $100 per share is necessarily an overly ambitious share price target for BMY stock, bases on its future revenue generating capabilities as I interpret them.

As mentioned, profitability is not an issue at the company - net profit margins in 2020 and 2021 were ~15% - and the outstanding cash flow generation can absorb the substantial debt payments without their becoming too burdensome. It should also be remembered that BMY's dividend payout ratio is currently >4.5%, which is above the industry average and acts as a small hedge against a falling share price.

All that needs to happen for BMY stock to recover a sizeable portion of the value it lost through 2023 is for new product sales to pick up - which I believe they can under more favorable economic conditions. With an extra year of experience managing relations with physicians and patients - and for the new acquisitions to bed in successfully - the two most crucial developments, in my view, would be the approval of KARXT in September, and a possible spike in revenues for Krazati owing to the failure of Amgen's rival KRAS-targeting therapy to secure a full commercial FDA approval.

I think both of these events can happen, and that ought to translate into a decent year for BMY's share price, which may have sunk too low in 2023 on overblown missed revenue figures, worries around patent expiries, and full year revenue guidance forecasts for a low-single digit year-on-year decline.

Full-year 2023 GAAP EPS forecast of $3.68 - $3.83 still implies a price to earnings ratio of ~14x, which is above average for the Big Pharma sector. Although there will be no explosive single-asset revenue growth to celebrate, I am expecting outperformance from Bristol-Myers Squibb Company in 2024 based on incremental improvements across the new product portfolio, which will impress the market equally. All of this makes me think this could be a good time to buy Bristol-Myers Squibb Company stock.

For further details see:

Bristol-Myers Squibb's Recent >$20bn M&A Spree Should Reward Patient Investors