TSVT - Bristol-Myers Squibb's Winning Formula: Dividends M&A And Innovation

2023-12-31 02:49:47 ET

Summary

- Bristol-Myers Squibb is a well-known blue-chip stock with a dividend yield exceeding 4.6%.

- Since 2019, Bristol-Myers Squibb has acquired pharmaceutical companies worth more than $115 billion, allowing it to expand its drug portfolio and product candidates in late-stage development.

- From 2022 to 2023, Bristol-Myers Squibb has won 13 regulatory approvals for Opdivo.

- Sales of Opdivo were about $2.28 billion in the three months ended September 30, up $130 million from the previous quarter, primarily due to its label and geographic expansion.

- I'm initiating coverage of Bristol-Myers Squibb with a "buy" rating.

Bristol-Myers Squibb ( BMY ) is an American pharmaceutical company and one of the leaders in the oncology and cardiovascular markets.

Thesis

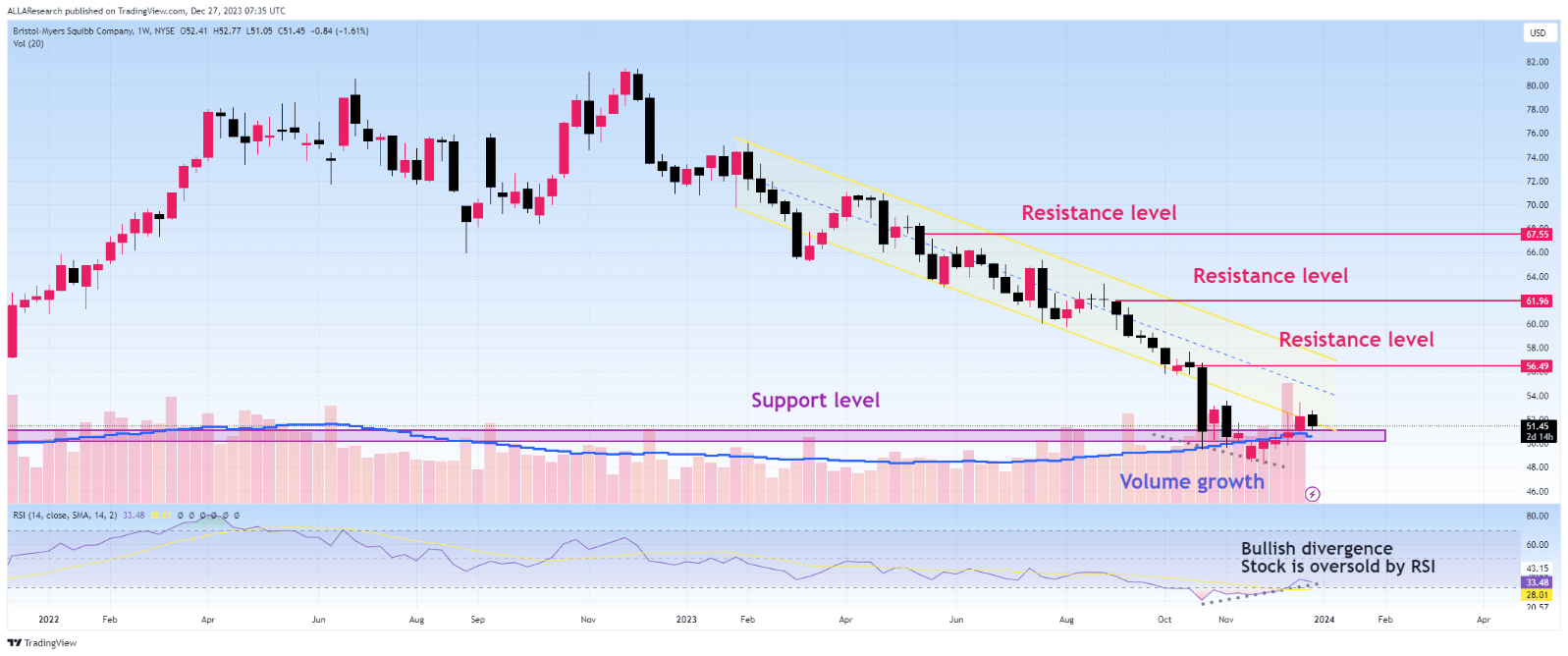

Since the end of 2022, the company's share price has fallen more than 36% before reaching the strong support level that caused a trend reversal in previous years. Before discussing the investment theses that make Bristol-Myers Squibb an attractive investment opportunity, I'd like to highlight the main reasons for the substantial decline in its price over the past year.

These factors include the ongoing downward trend in Revlimid's sales due to the increasing number of its generic versions on the market, unsatisfactory demand for Abecma as a result of tighter competition with Legend Biotech/Johnson & Johnson's Carvykti ( JNJ ) and Pfizer's Elrexfio ( PFE ), and investor fears caused by the expected loss of exclusivity of blockbuster blood thinner Eliquis in 2026.

{kind=link}

However, despite the financial risks, which will be presented in more detail later in the article, traders were unable to breach the support level indicated in the chart above. Additionally, a bullish divergence was formed on the weekly time frame, which, together with the increase in trading volume in recent months, indicates that the bears are losing strength and a rising influence of bullish forces in the market.

The company has a return on equity of over 25%, one of the largest dividend yields among Big Pharma at about 4.66%, high rates of Opdivo's label expansion, and strong sales of its recently FDA-approved medications. In addition, Bristol-Myers Squibb has a rich portfolio of product candidates thanks to its aggressive M&A policy, which will help minimize the financial risks associated with the expected loss of exclusivity of Eliquis (apixaban), Inrebic (fedratinib), Onureg (azacitidine) and Yervoy (ipilimumab) over the next five years.

Bristol-Myers Squibb also raised its diluted EPS guidance for the full year 2023 from $7.35-$7.65 to $7.50-$7.65, which corresponds to its non-GAAP P/E [FWD] of 6.8x, indicating that it is undervalued relative to its healthcare peers such as AstraZeneca ( AZN ), Eli Lilly ( LLY ), AbbVie ( ABBV ) and Merck ( MRK ).

Source: table was made by Author based on Seeking Alpha

I'm initiating coverage of Bristol-Myers Squibb with a "buy" rating.

Bristol-Myers Squibb has significantly strengthened its pipeline in recent years

Since 2019, Bristol-Myers Squibb has acquired pharmaceutical companies worth more than $115 billion, allowing it to expand its drug portfolio and product candidates in late-stage development. Ultimately, this will enable it to strengthen its position in the cancer medicines market and also expand its global presence in the fast-growing cardiovascular and neurological disorders markets.

I expect the company's aggressive M&A policy to impact its EPS in the short term negatively. On the other hand, Bristol-Myers Squibb's strengthened product pipeline ultimately reduces its need for large strategic acquisitions and also reduces the financial risks associated with losing exclusivity on some of its blockbusters over the next five years.

Source: graph was made by Author based on 10-Qs and 10-Ks

Next, I would like to closely examine the latest and key acquisitions that will continue to have the greatest impact on the company's financial position.

On October 5, 2020 , Bristol-Myers Squibb announced the acquisition of MyoKardia for $13.1 billion. The transaction strengthens the company's prospects in the fast-growing cardiovascular therapeutics market, where unmet medical needs still exist.

Source: Seeking Alpha

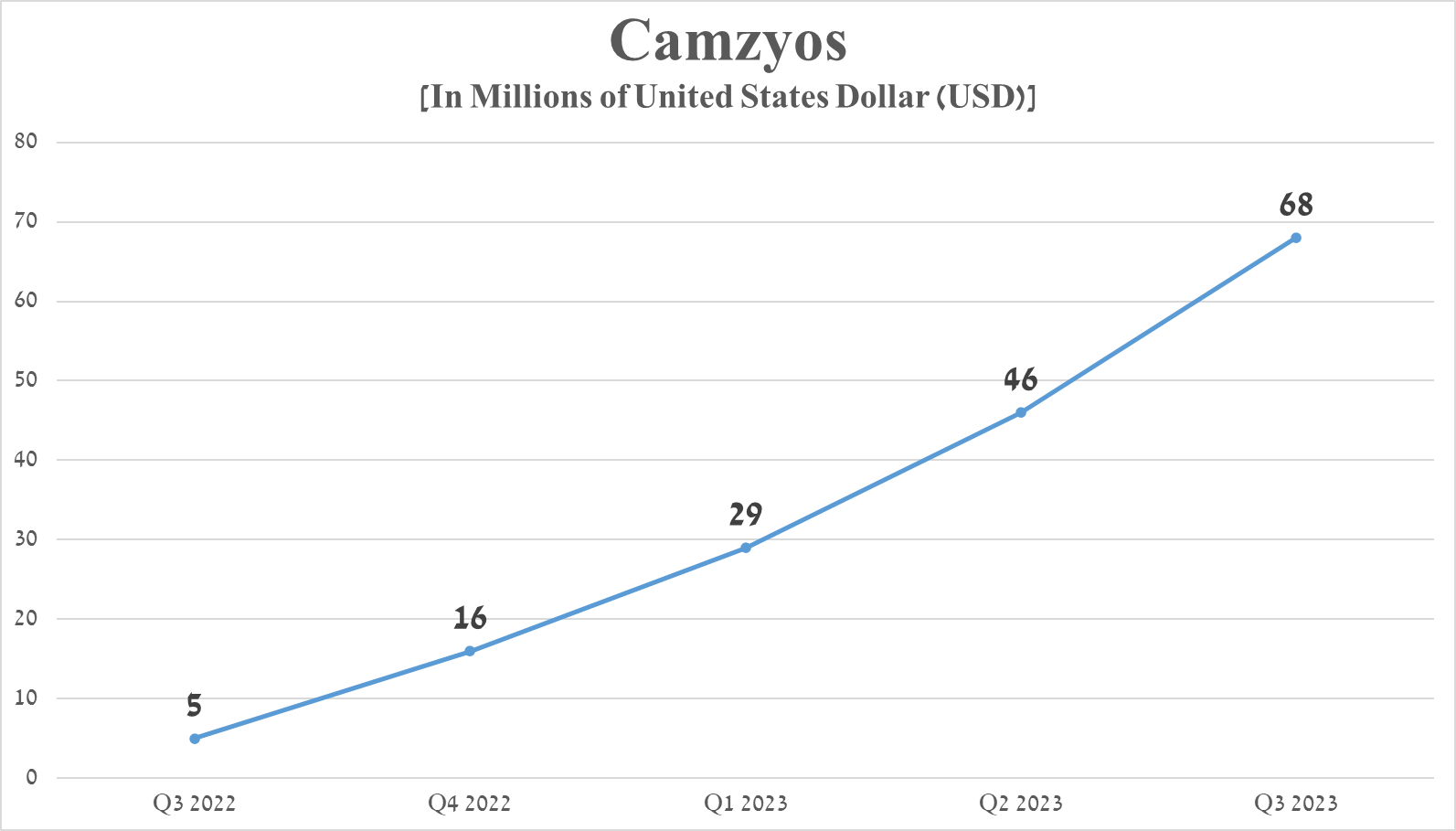

The flagship product that was developed by MyoKardia is Camzyos (mavacamten), approved by the FDA to treat certain patients with symptomatic obstructive hypertrophic cardiomyopathy ((HCM)) at the end of April 2022 .

Its sales were $68 million in the third quarter of 2023, an increase of 47.8% quarter-over-quarter, driven by its status as the first cardiac myosin inhibitor, the release of positive long-term follow-up data from the phase 3 EXPLORER-LTE trial , and its approval by the EMA in June 2023 .

{kind=link}

Camzyos is one of the company's key products on which its management has high expectations and which could potentially increase Bristol-Myers Squibb's revenue growth in the coming decade. The company expects its peak sales to be over $4 billion by 2030.

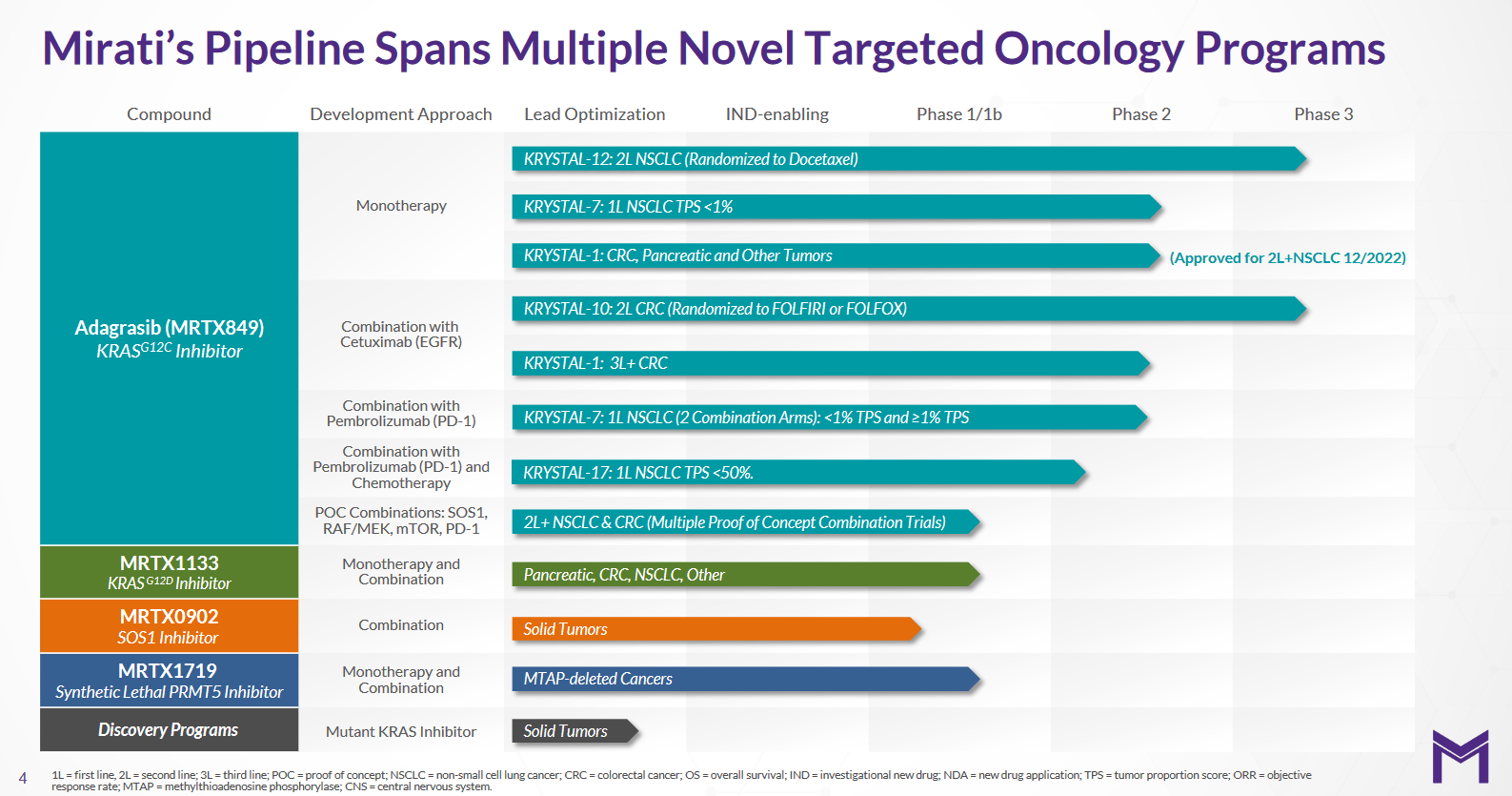

Bristol-Myers Squibb's second-biggest acquisition over the past year was Mirati Therapeutics ( MRTX ), whose FDA-approved product called Krazati (adagrasib) is a potentially best-in-class KRASG12C inhibitor. The deal allowed the company to diversify its oncology portfolio and acquire breakthrough treatments for cancer.

{kind=link}

Krazati received FDA approval for the treatment of certain patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) in mid-December 2022 . According to the American Cancer Society , approximately 238,340 new lung cancer cases are expected in the United States in 2023, representing a significant commercial opportunity for Bristol-Myers Squibb's product. However, the company does not rest on its progress and continues to evaluate its efficacy in the treatment of colorectal cancer, which accounts for about 10% of all cancer cases in the world.

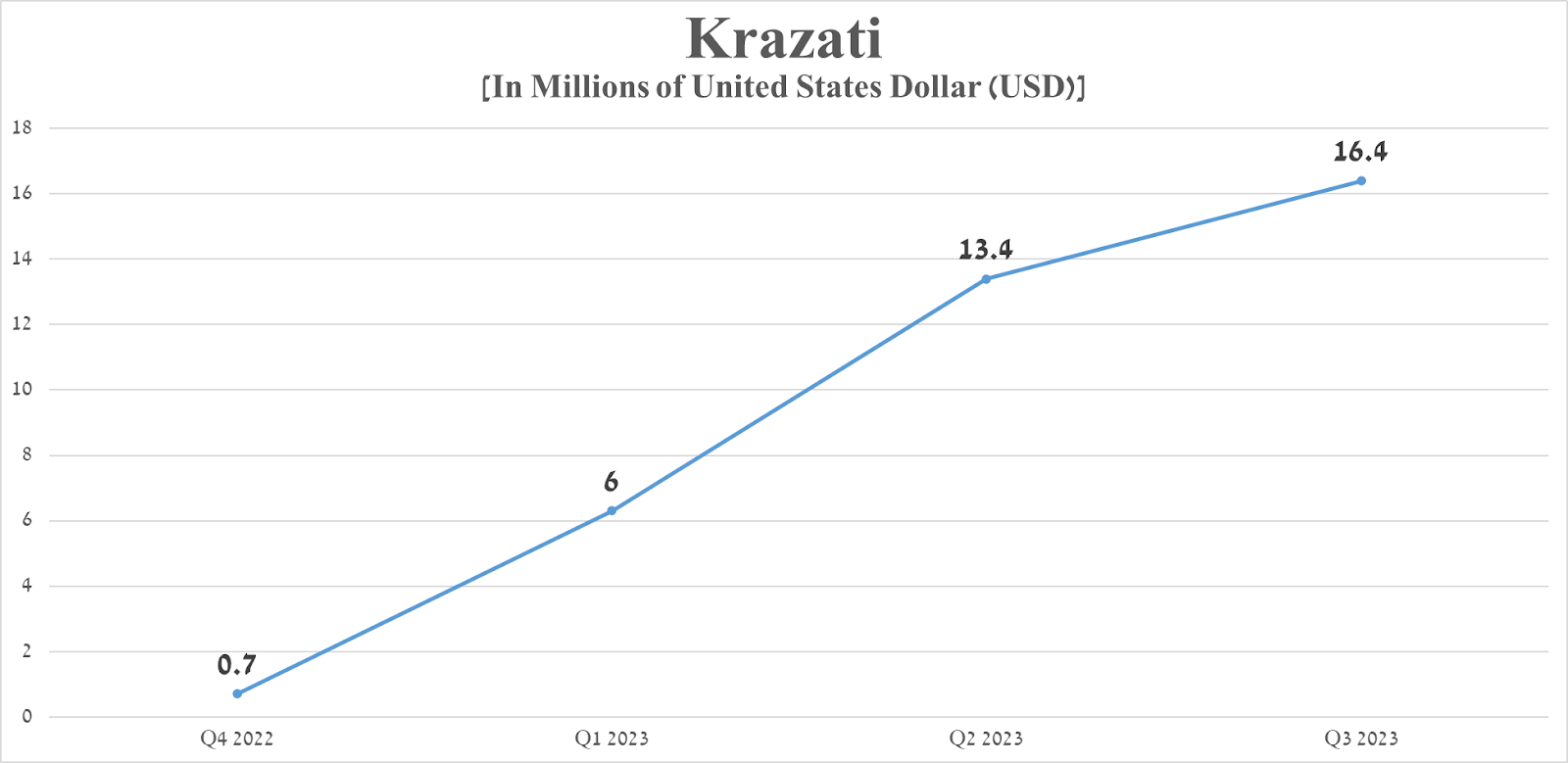

Krazati sales were $16.4 million for the three months ended September 30, 2023, up $3 million from the prior quarter due to its strong efficacy demonstrated in KRYSTAL-1 and the weaker clinical data of Amgen's Lumakras, which failed to meet a secondary endpoint that evaluated overall survival.

{kind=link}

Moreover, on December 26 , the FDA rejected Amgen's sNDA ( AMGN ) for full approval of Lumacras for the treatment of patients with KRAS G12C-mutated NSCLC, which ultimately is highly positive news for Bristol-Myers Squibb since, in my opinion, this could accelerate the growth rate of Krazati sales already in the short term.

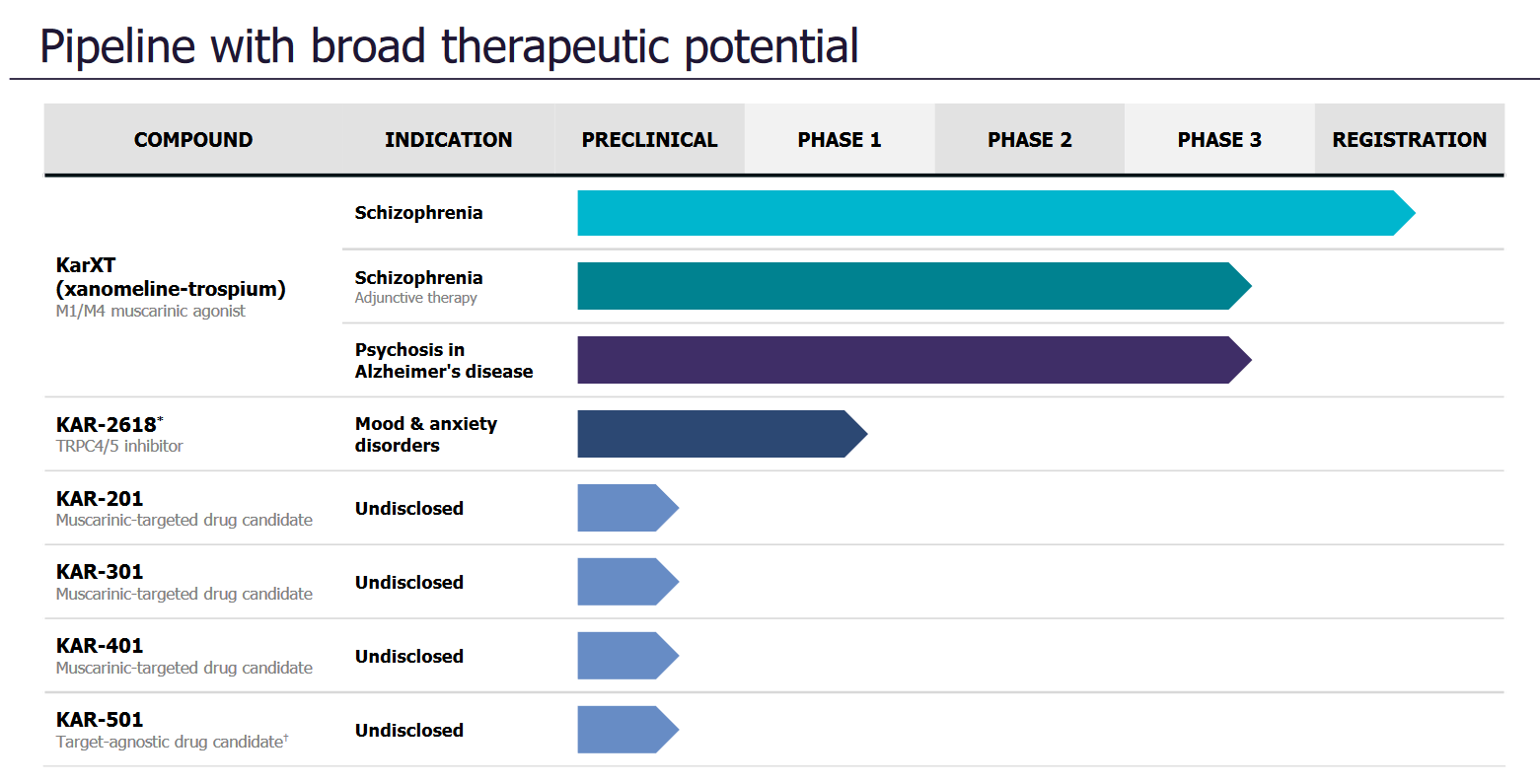

Also, I want to note the acquisition of Karuna Therapeutics ( KRTX ), which was announced on December 22, 2023 . This transaction strengthens the company's position in the neurodegenerative disease market with experimental treatments aimed at treating schizophrenia, Alzheimer's disease psychosis, anxiety, and mood disorders.

{kind=link}

Karuna Therapeutics' flagship product candidate is KarXT (xanomeline-trospium), which has a novel mechanism of action that targets activation of the M1 and M4 muscarinic receptors, which, unlike most FDA-approved medications, does not block dopamine D2 receptors.

On September 29, 2023 , Karuna Therapeutics announced that the FDA had accepted its NDA for KarXT for treating schizophrenia, with a decision date set for September 26, 2024. According to the World Health Organization, schizophrenia affects approximately 24 million people worldwide .

Given the convincing efficacy of KarXT demonstrated in three phase III trials and its favorable safety profile relative to most FDA-approved drugs, I expect that Karuna Therapeutics' product will not only be approved by regulatory authorities but also become commercially successful.

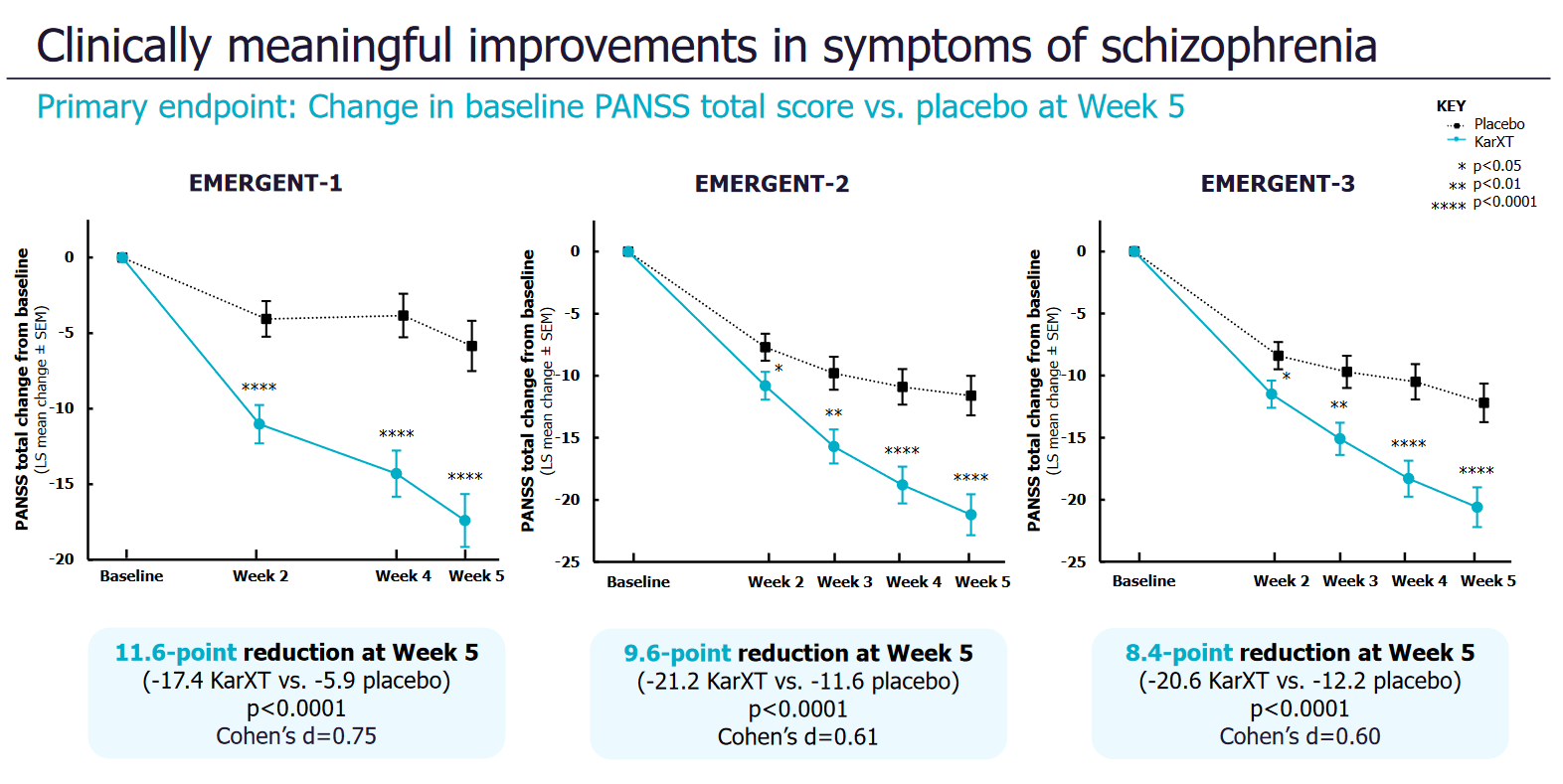

On March 20, 2023 , the company reported that KarXT demonstrated a statistically significant reduction in the PANSS total score compared to the placebo after five weeks of treatment. More importantly, the researchers observed an early and statistically significant decrease in symptoms in the group of patients taking Karuna Therapeutics' experimental drug as early as the 2nd week of treatment.

{kind=link}

Opdivo is Bristol-Myers Squibb's flagship product

Bristol-Myers Squibb's portfolio is rich and includes Eliquis, used to prevent strokes and treat other cardiovascular diseases; Sprycel, approved to combat chronic myeloid leukemia and acute lymphoblastic leukemia; Yervoy and Opdivo, used to treat several cancers, including such widespread ones as melanoma, lung cancer, and colorectal cancer.

In my estimation, the most important among them for the company's free cash flow is Opdivo (nivolumab) , a monoclonal antibody that blocks PD-1 and, as a result, can enhance anti-cancer immune responses within the patient's body.

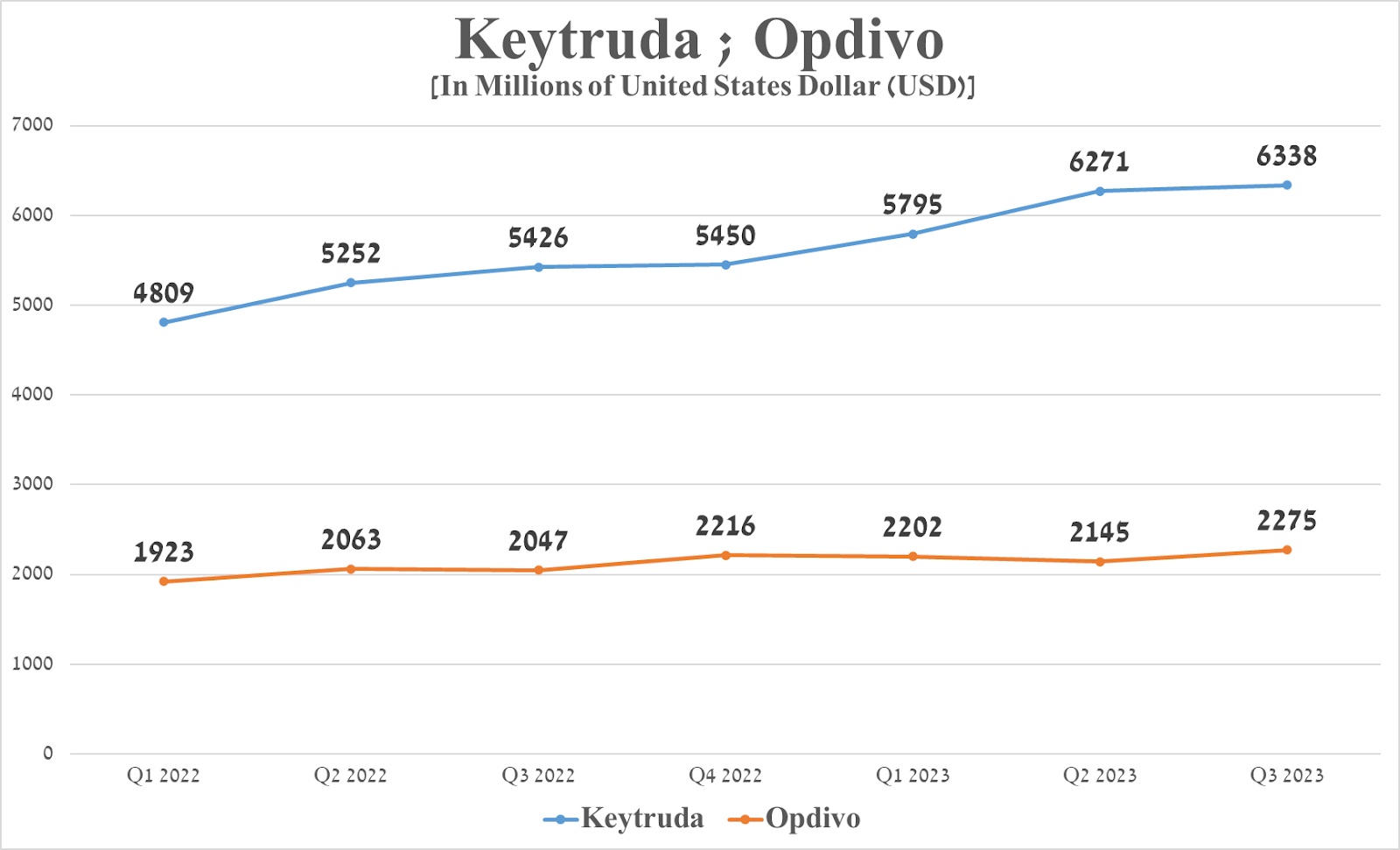

From 2022 to 2023, Bristol-Myers Squibb has won 13 regulatory approvals for Opdivo. So, on October 13, 2023 , the FDA approved the use of Opdivo for the treatment of patients aged 12 years and older with completely resected stage IIB or IIC melanoma.

Sales of the company's flagship medication were about $2.28 billion in the three months ended September 30, up $130 million from the previous quarter, primarily due to its label and geographic expansion. At the same time, the year-on-year increase in sales of Merck's Keytruda was significantly higher due to the greater number of indications for use and the growing preference for it as a first-line treatment.

{kind=link}

In the coming years, I expect continued label expansion for Opdivo as Bristol-Myers Squibb conducts numerous pivotal clinical trials to evaluate its efficacy in treating various types of cancer, including in combination with Yervoy.

Source: Bristol-Myers Squibb

Additionally, given the growing demand for Opdivo for the treatment of melanoma and its lower price relative to Keytruda, I believe that Bristol-Myers Squibb's product will continue to increase its share in the PD-1/PD-L1 inhibitors market, which Coherent Market Insights estimates will exceed $77 billion by 2028 .

Bristol-Myers Squibb has a high dividend yield and return on equity

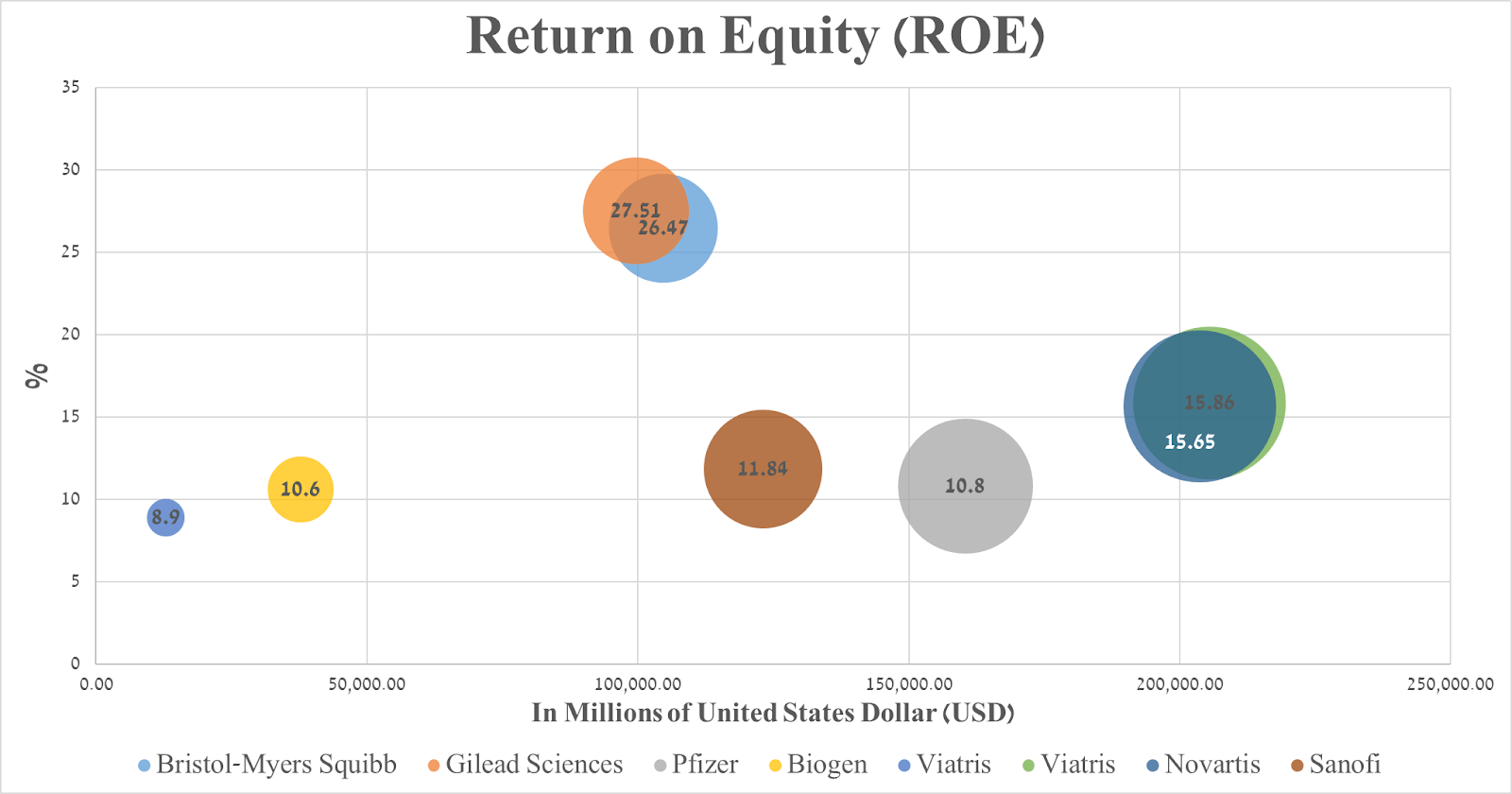

According to GuruFocus, Bristol-Myers Squibb has a return on equity ((ROE)) of around 26.47%, indicating that its financial management remains effective during a challenging time for the healthcare sector due to the Inflation Reduction Act.

{kind=link}

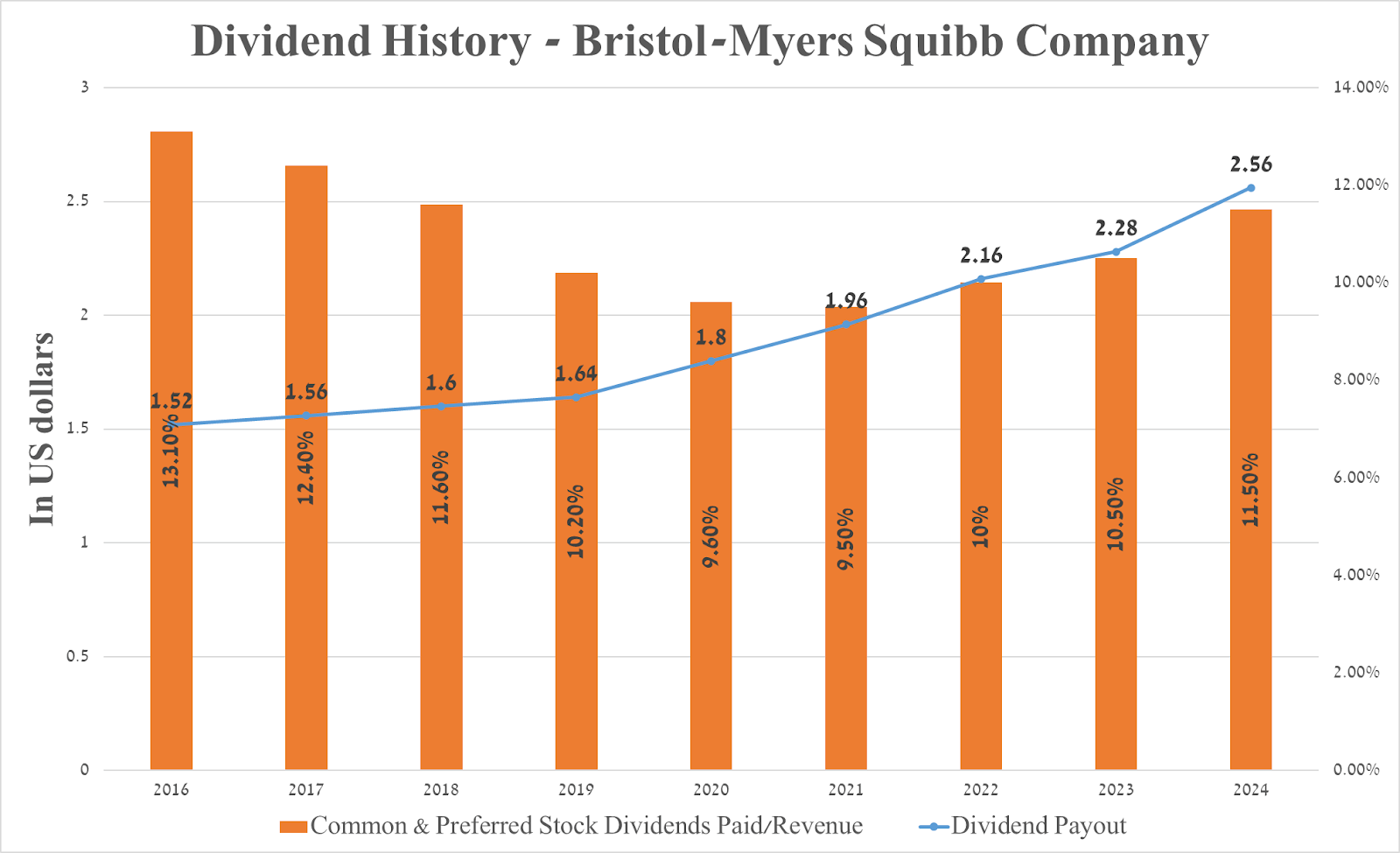

The company's management has consistently increased its dividend payout over the past 15 years, and I expect this trend to continue in the coming years thanks to its stable cash flow and growing sales of its recently launched FDA-approved drugs.

{kind=link}

Meanwhile, the company's 5-year dividend growth rate is 7.34%, which, together with the payout ratio [non-GAAP] of 29.92%, indicates a reasonable dividend policy pursued by its management.

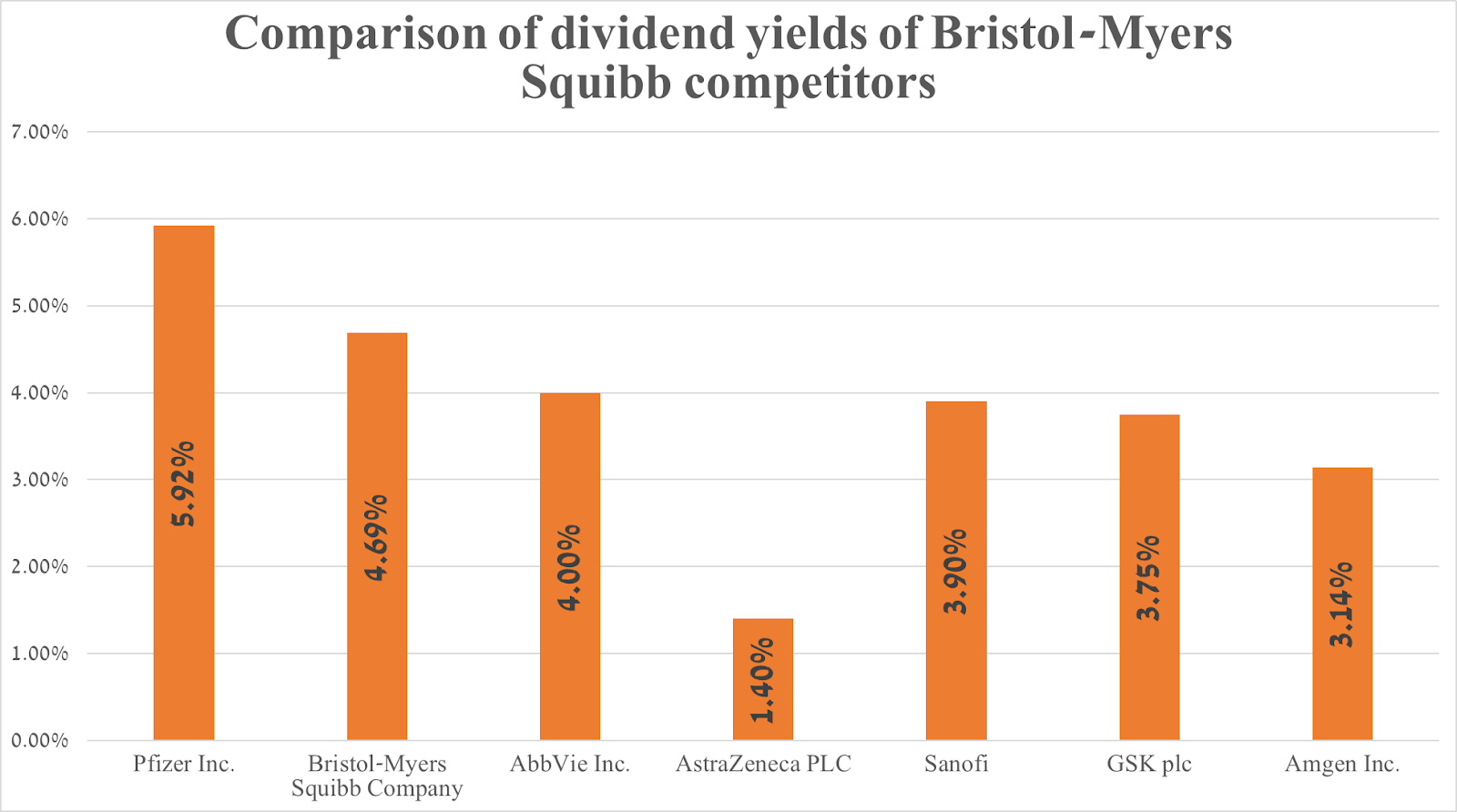

The company's dividend yield is 4.69%, outperforming its major healthcare peers Merck, GSK ( GSK ), Amgen and AstraZeneca.

{kind=link}

Bristol-Myers Squibb's financial results and outlook

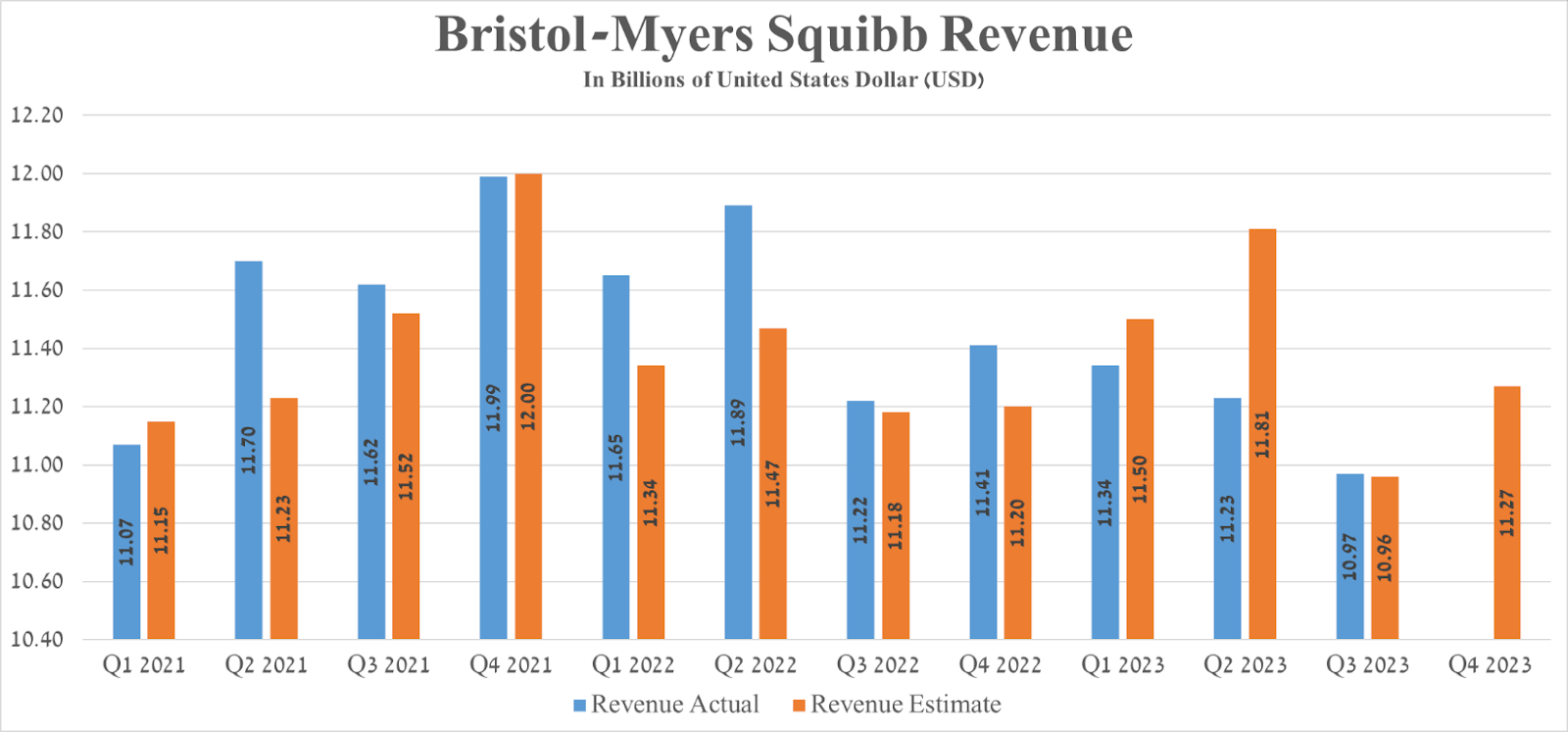

Bristol-Myers Squibb's revenue for the three months ended 2023 was about $10.97 billion, down 2% from the previous year but beating analysts' expectations by $10 million.

{kind=link}

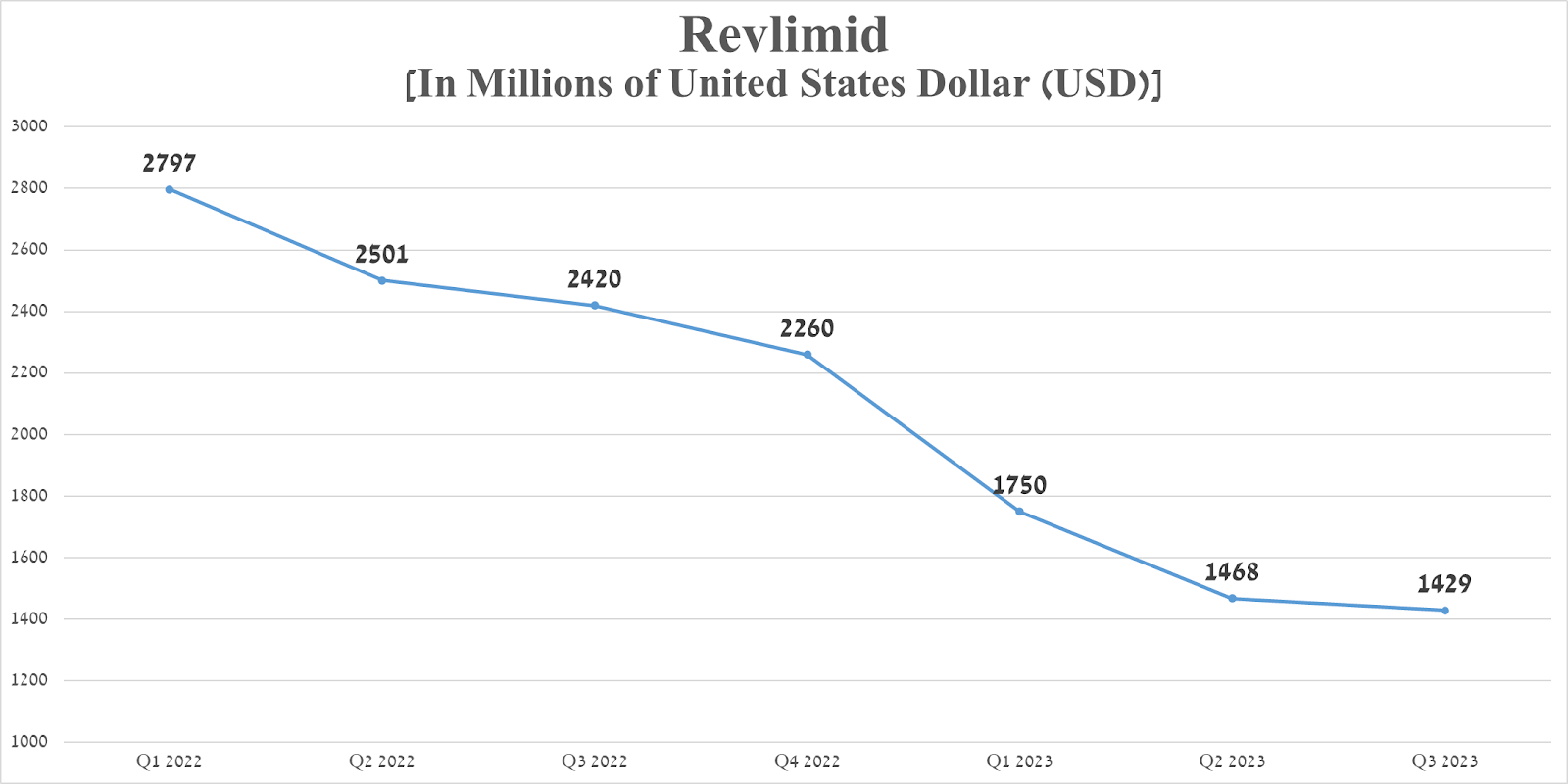

One of the main reasons for the decline in this financial metric is the decline in demand for Revlimid (lenalidomide) due to increasing competition with its generic versions produced by companies such as Viatris ( VTRS ), Sun Pharmaceutical, and Teva Pharmaceutical ( TEVA ).

{kind=link}

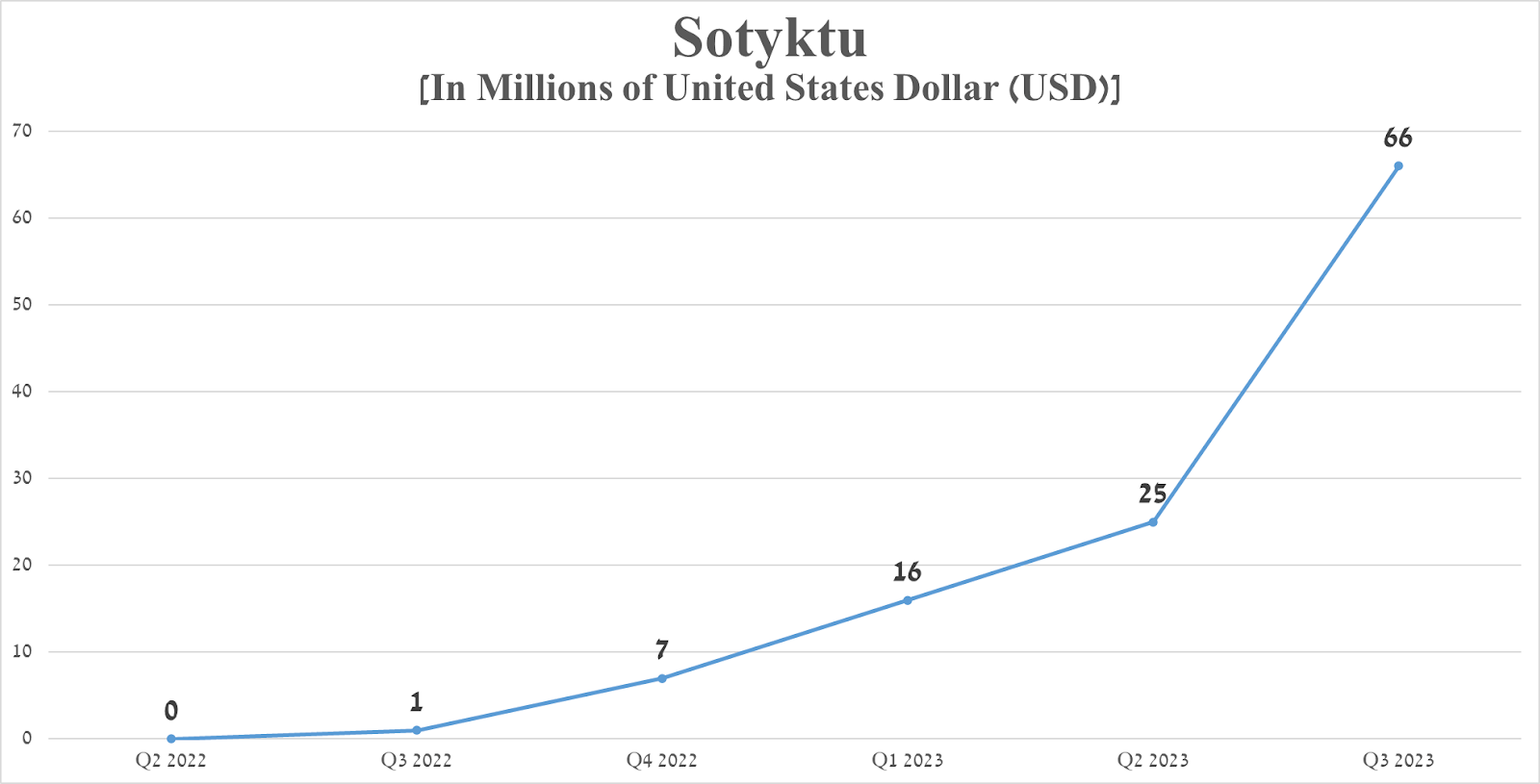

On the other hand, the company pleased investors with increased demand for Sotyktu (deucravacitinib), a TYK2 inhibitor approved by the FDA for the treatment of certain patients with plaque psoriasis. Its sales were $66 million in the third quarter of 2023, an increase of $65 million from the prior year. Bristol-Myers Squibb expects its peak sales to exceed $4 billion by 2030 .

{kind=link}

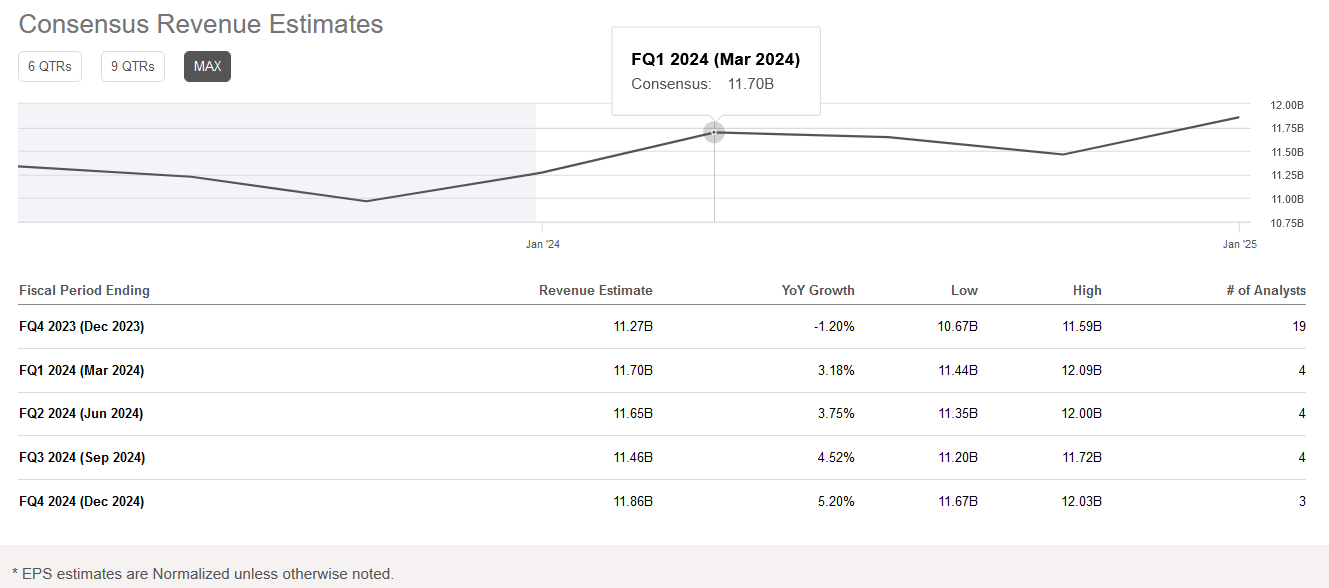

The Seeking Alpha platform offers data on Wall Street analysts' expectations for the coming years. So, Bristol-Myers Squibb's revenue for the fourth quarter of 2023 is expected to be in the range of $10.67-$11.59 billion, which is 1.2% less than the previous year.

{kind=link}

But even though the company's revenue is expected to fall year-over-year, its price/sales [FWD] is 2.3x, indicating Bristol-Myers Squibb is trading at a discount to most of its healthcare peers.

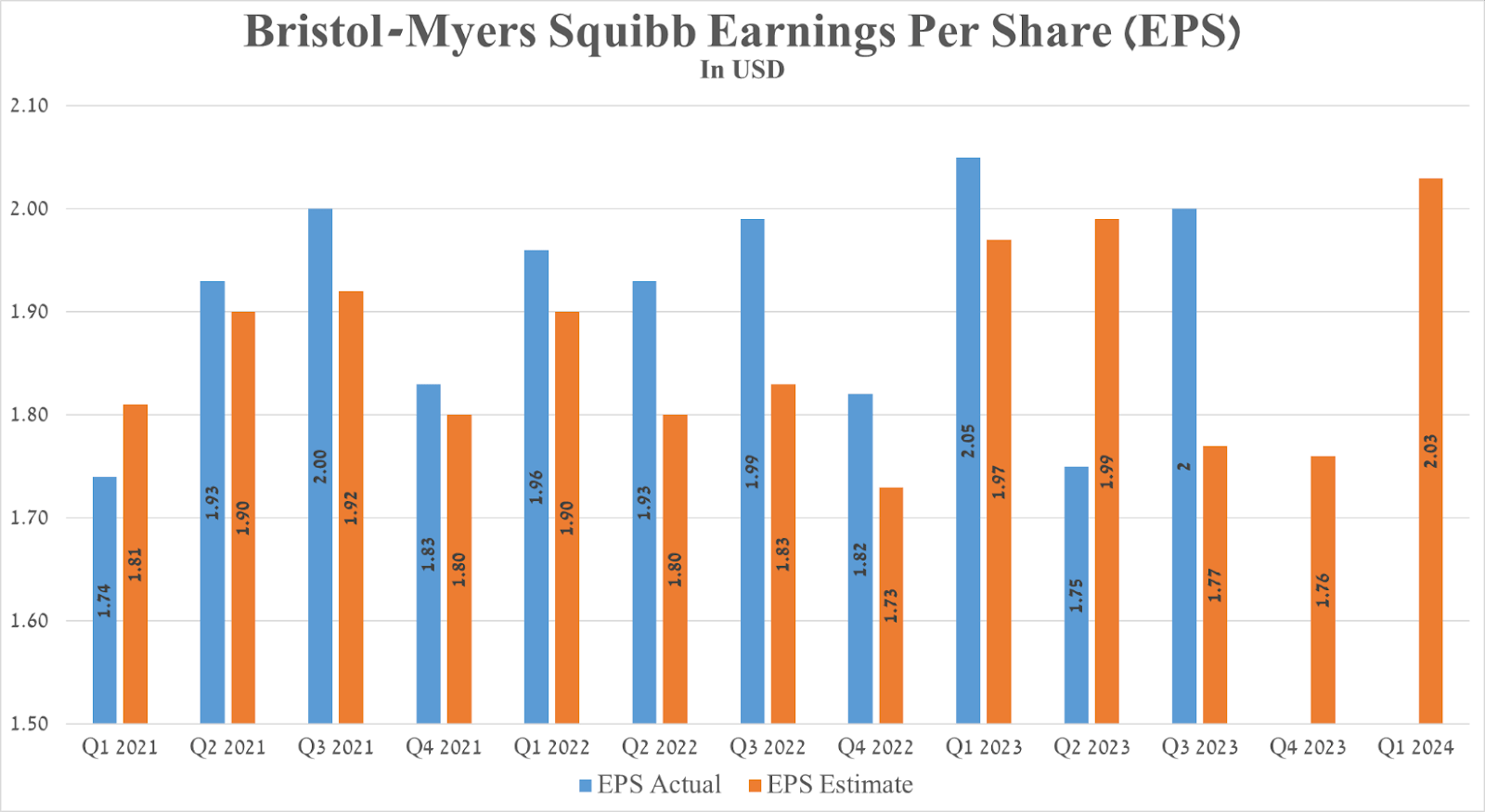

Bristol-Myers Squibb's Q3 Non-GAAP EPS was $2, beating analysts' consensus estimates by $0.23. However, its EPS is anticipated to be in the range of $1.43 to $1.91 in the fourth quarter of 2023, down slightly from the third quarter of 2022.

{kind=link}

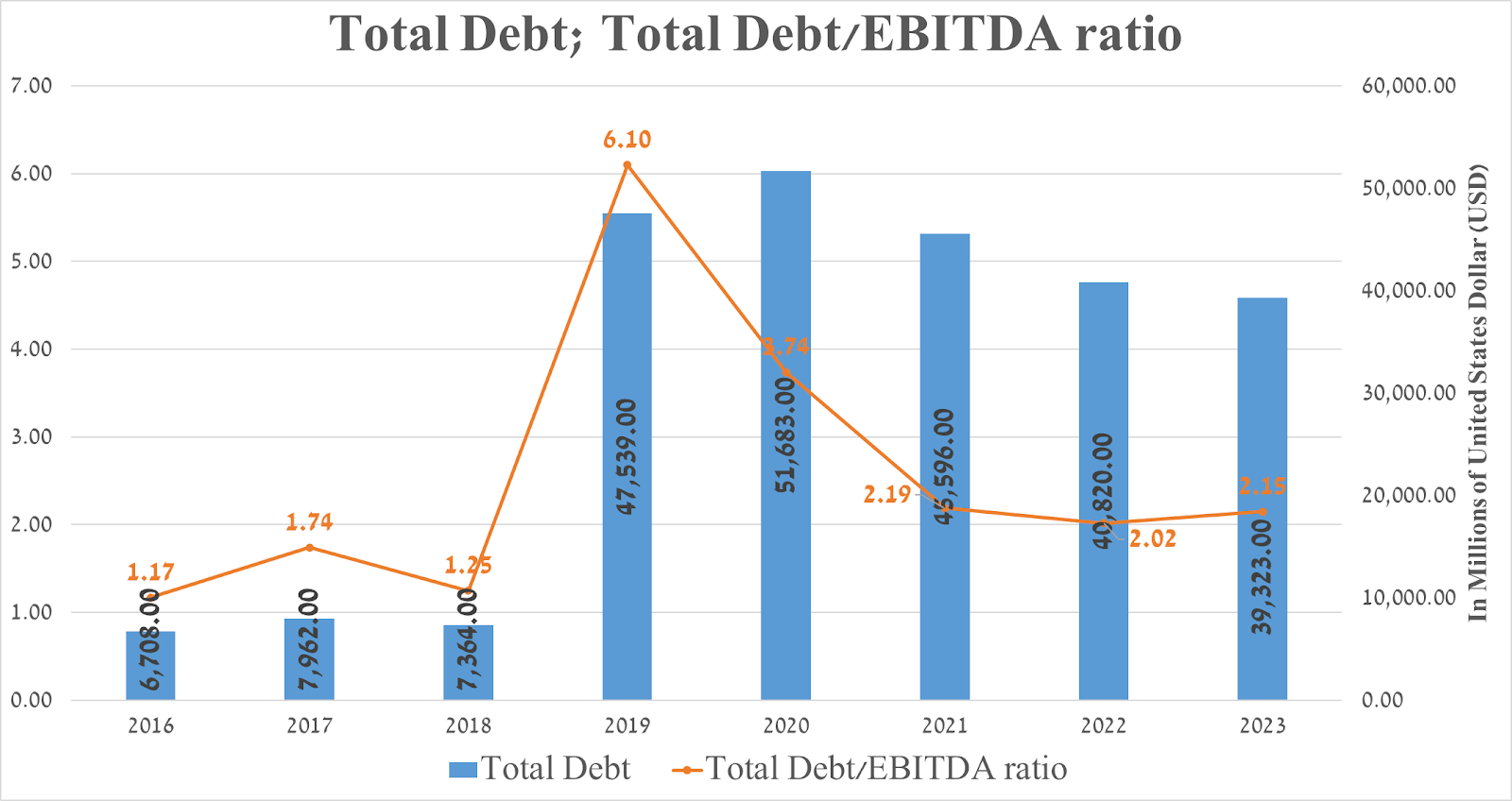

Additionally, it is important to discuss Bristol-Myers Squibb's debt. The company's total debt was about $39.3 billion at the end of Q3 2023, and it has continued to fall since 2020 despite its aggressive M&A policy. Also, I want to note that its total debt/EBITDA ratio remains around 2x, indicating Bristol-Myers Squibb's financial stability and the absence of significant risks associated with servicing its debt.

{kind=link}

Key risks to consider

In addition to the negative impact of the Inflation Reduction Act, I highlight two main risks that financial market participants need to consider.

Exclusivity of six Bristol-Myers Squibb medicines expires in the next five years

The first risk I highlight, which is key to the company's financial position, is the expiration of exclusivity on some of its products in the next five years. Once a medication's patents expire, pharmaceutical companies will have the right to commercialize generic versions or biosimilars, ultimately leading to a significant drop in sales of Bristol-Myers Squibb's branded drug.

Source: table made by Author based on 10-K

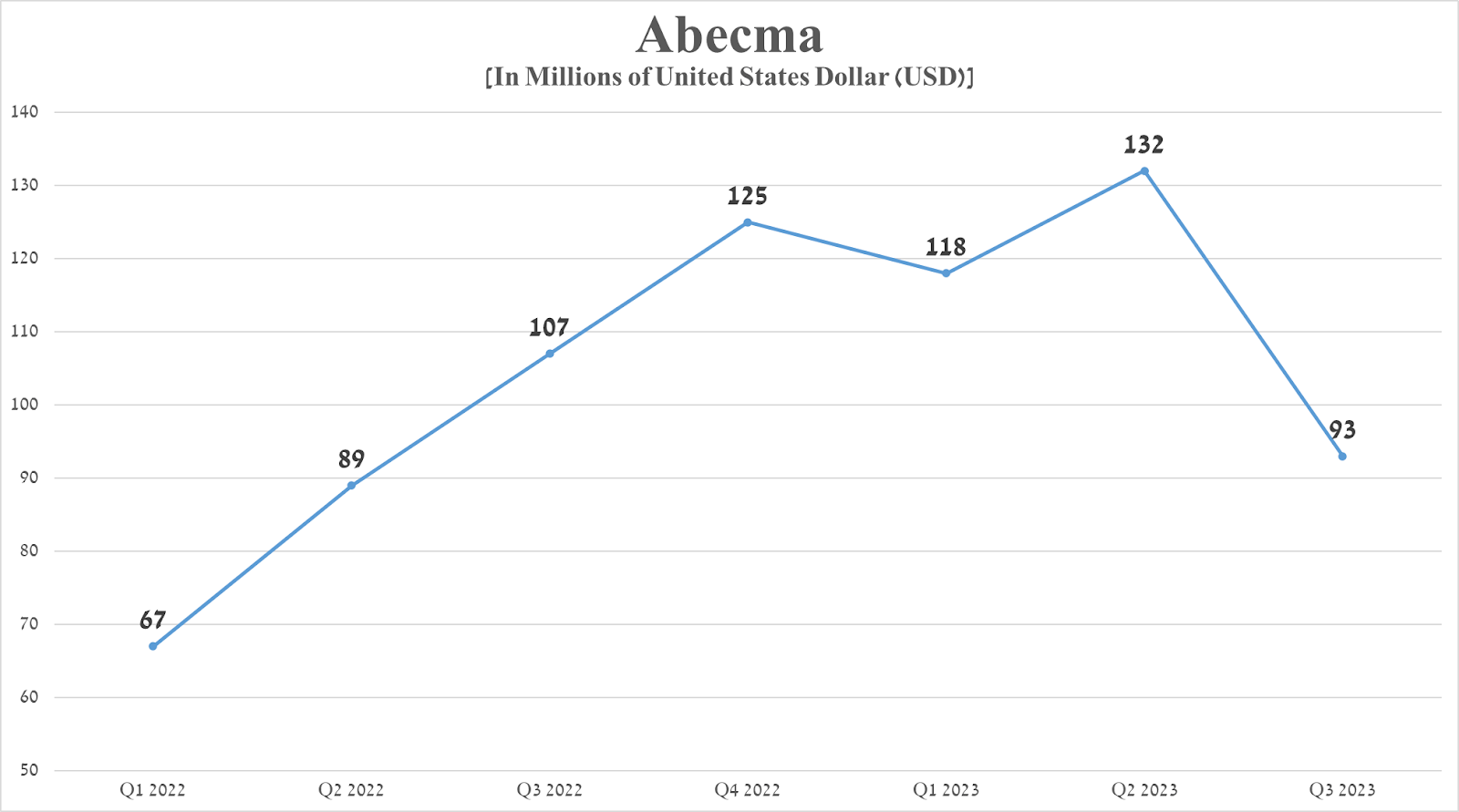

Weak sales of Abecma

Abecma (idecabtagene vicleucel) is a medicine developed in collaboration with 2seventy bio ( TSVT ) and approved by regulatory authorities for the treatment of patients with RRMM after 4 or more prior lines of therapy. Its sales were $93 million for the third quarter of 2023, down 13% year-over-year due to the higher efficacy of Legend Biotech/Johnson & Johnson's Carvykti, its key competitor.

{kind=link}

Conversely, readers of the article should note that Abecma was the first CAR T cell therapy to receive regulatory approval in Japan in early December 2023 for the treatment of patients with RRMM who have received at least two prior therapies.

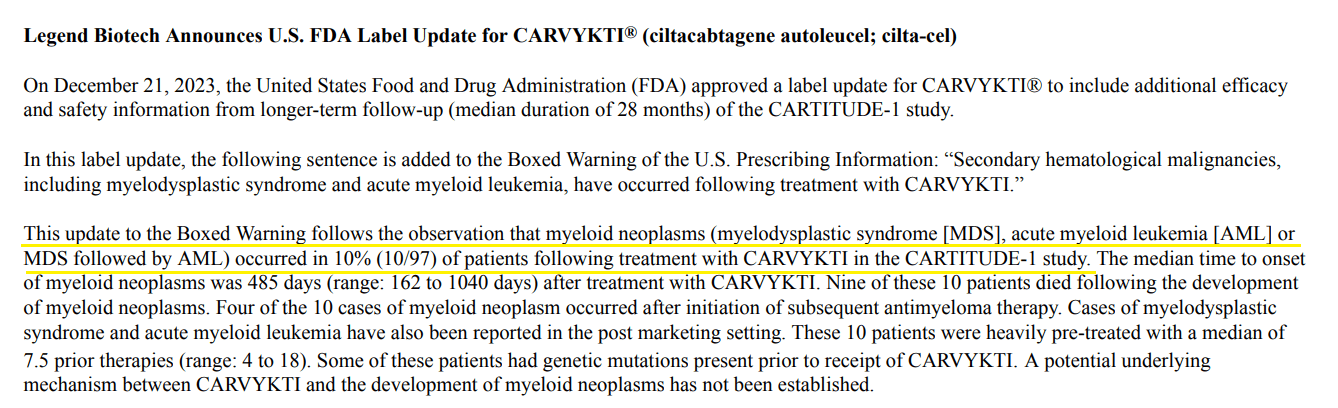

Also, on December 21 , Legend Biotech ( LEGN ) reported additional results from the CARTITUDE-1 study, according to which about 10% of patients taking Carvykti developed myeloid neoplasms, which are a group of rare types of blood cancer.

{kind=link}

In my assessment, this is positive news for 2seventy bio and Bristol-Myers Squibb ahead of the Oncologic Drugs Advisory Committee, which will discuss the results of the pivotal phase 3 KarMMa-3 trial.

Takeaway

Bristol-Myers Squibb is an American pharmaceutical company and one of the leaders in the oncology and cardiovascular markets.

Despite the decline in Revlimid's sales due to tighter competition with its generic versions and other financial risks noted in the article, I highlight several investment theses that make Bristol-Myers Squibb an appealing asset for conservative investors. These are the company's aggressive M&A policy, which allowed it to acquire best-in-class drugs, an extremely high dividend yield exceeding 4.6%, high rates of Opdivo's label expansion, and continued extremely high demand for Sotyktu and Camzyos.

I'm initiating coverage of Bristol-Myers Squibb with a "buy" rating.

For further details see:

Bristol-Myers Squibb's Winning Formula: Dividends, M&A, And Innovation