ENBA - British American Tobacco: 25 Hated Dividend Growth Stocks Compared

2023-04-15 07:33:28 ET

Summary

- British American Tobacco is currently "hated" by the market for a variety of reasons.

- We share data on 25 top dividend-growth stocks that are also currently hated by the market (considering they trade near the lower end of their 52-week price ranges).

- After reviewing the details on BTI (including business, valuation, big-dividend yield and risks), we conclude with our strong opinion on investing in BTI specifically and dividend growth stocks in general.

Following the incredible fiscal and monetary stimulus during the pandemic, the market is now reeling from high inflation and the threat of an ugly recession. However, one thing that helps many investors cope with market uncertainty is steady growing dividend income. In this report, we first share data on 25 top dividend growth stocks that currently trade well below their 52-week highs. Next, we dig into the details on one name in particular, British American Tobacco ( BTI ), including its business, the safety of its big dividend yield, valuation and risks. We conclude with our strong opinion on investing in BTI (and dividend-growth stocks in general) as well as a handful of alternative contrarian ideas worth considering.

25 "Hated" Dividend Growth Stocks, Compared

For starters, here is a look at the recent performance of 25 top dividend growth stocks. To make this list, we required at least 10 consecutive years of dividend growth (although many of them have been increasing their dividends for much longer). We also required the shares to be trading in the lower half of their 52-week price range (i.e. the stocks are "hated" by the market as the share prices are down big).

data as of 13-Apr-23 (StockRover)

{kind=link}

( JNJ ) ( HD ) ( PFE ) ( COST ) ( VZ ) ( ENB ) ( MO ) ( MMM ) ( USB ) ( QCOM ) ( IBM )

Note: an expanded (and downloadable) list of over 70 dividend-growth stocks is available here .

One name from the above list that we find particularly interesting is British American Tobacco, as described below.

British American Tobacco (BTI), Yield: 7.5%

{kind=link}

British American Tobacco is a UK-based company that sells tobacco and nicotine products to consumers worldwide. It trades in the US as an American Depository Receipt ("ADR"), and the shares are currently depressed (as we will explain throughout this report).

British American Tobacco

For a little perspective, BTI's largest operating segment by geography is the United States, as you can see in the following graphic. And there is some pressure for the company to move its primary listing to the US (because that could result in a higher valuation--a good thing for investors).

{kind=link}

And for reference, you may be familiar with some of BTI's products and brands, including combustible tobacco.

BTI Investor Presentation

And also including its newer, non-combustible, categories.

BTI Investor Presentation

Revenue Breakdown and Growth

Traditional tobacco (combustible) products still make up the lion's share of the business, as you can see in this revenue graphic below.

BTI Investor Presentation

And this next chart shows that the smaller "New Categories" are actually growing much faster, but of course they are still smaller by revenue than traditional combustible products.

BTI Investor Presentation

Business Strategy:

And this revenue breakdown (above) is consistent with the company's strategy to be a leader (and capture market share) in newer non-combustible categories, such as vaping, heating tobacco and oral products

Also important to note, BTI's products are diversified across premium products, mid-tier and low-cost products. This gives it some pricing power (in the premium space), but also helps diversify risks as consumer preferences can (and do) change over time.

BTI's Wide Moat:

BTI has a variety of "wide moat" competitive advantages. For example, regulations (especially in the US) make it virtually impossible for new entrants in the traditional combustible tobacco space. And BTI's large size also gives it competitive advantages through economies of scale. Not to mention, the nicotine in BTI's products is highly addictive (which helps ensure customers stick around).

Big Dividend Safety

From a high-level perspective, BTI is a very profitable company (as we will see in the valuation section of this report), but it's not growing rapidly (tobacco isn't exactly a popular product to market considering its addictive nature and side effects, as we will cover later in the risks section of this report). As such, BTI should return extra profits and cash flows to investors through dividends and share repurchases (because they don't have compelling high-growth opportunities to reinvest back into the company). And that is exactly what BTI does (especially the big dividend part).

BTI's current dividend yield is 7.5%, and the company has increased its dividend every year for over two decades straight. However, as a US investor, the dividend fluctuates because currency exchange rates (British Pound versus US dollar) also fluctuate. Importantly, as per the company :

The equivalent quarterly dividends receivable by holders of ADSs in US dollars will be calculated based on the exchange rate on the applicable payment date. A fee of US$0.005 per ADS will be charged by Citibank, N.A. in its capacity as depositary bank for the British American Tobacco American Depositary Receipt ("ADR") programme in respect of each quarterly dividend payment.

And here is a look at the company's cash flows as compared to the dividend payout (i.e. the dividend is very well covered).

BTI Investor Presentation

Specifically, as compared to free cash flows, BTI's dividend coverage ratio was recently over 163%. That is a very strong dividend coverage ratio.

And with regards to share repurchases (i.e. another way to return cash to shareholders), BTI made clear in its latest quarterly earnings announcement that it is currently prioritizing the dividend (and paying down debt) ahead of share buybacks (emphasis ours):

"Our business is highly cash generative; we achieved another year of excellent operating cash conversion, delivering 100%, well ahead of our 90% guidance and we expect as a Group to generate c.£40 billion of free cash flow before dividends over the next five years.

"The Board reviews our capital allocation priorities taking into account the macro-economic environment and potential regulatory and litigation outcomes. At this time, the Board has decided to take a pragmatic approach. Given our incremental investment plans in 2023 to further accelerate our transformation, and in light of the uncertain macro environment, higher interest rates, outstanding litigation and regulatory matters, the Board has decided to prioritise strengthening the balance sheet. This will provide greater business resilience while continuing to support future financial agility, as we aim to reduce leverage more quickly towards the middle of our target 2-3x corridor.

In line with our progressive dividend policy, the dividend will increase by 6.0% to 230.9p . "We strongly believe that share buy-backs have an important role to play within our capital allocation framework, and we will continue to keep it under review as we progress through the year.

And for reference, the 2-3x corridor referenced above is debt to adjusted EBITDA. So it looks like there won't be much share repurchase activity in the near term, but BTI does expect to raise the dividend by 6.0%, again. Good for income-focused investors!

Valuation:

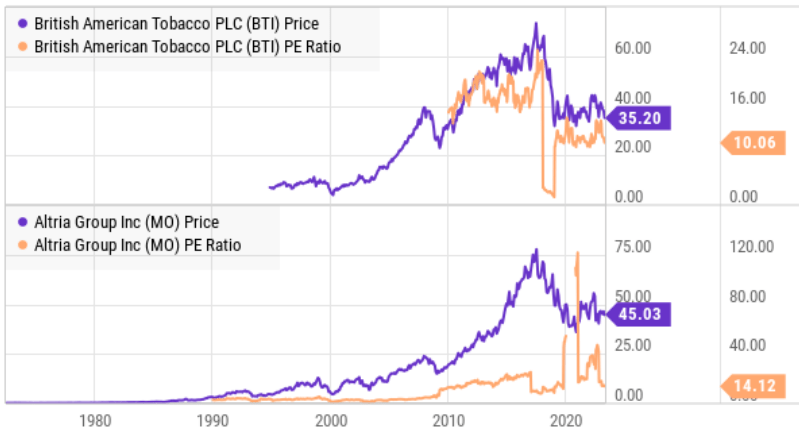

Typically, investors talk about price-to-earnings ratios, but the inverse of that is the "earnings yield." BTI's current P/E ratio is 10.1x, so its earnings yield (i.e. how much earnings you, as a shareholder, get in exchange for the price you pay per share) is 9.9%. That is a very high and attractive earnings yield, and an indication that BTI is trading at an attractive low price. And for perspective, here is a look at BTI's historical P/E ratio as compared to tobacco competitor Altria ( MO ).

{kind=link}

BTI is currently trading at an attractively low valuation, especially considering its strong cash flow and healthy (and improving) balance sheet (BTI has a BBB+ "investment grade" credit rating from S&P, and is actively using cash to strengthen the balance sheet (paydown debt) as described earlier).

BTI Investor Presentation

In a nutshell, BTI is a healthy, steady business with a well-covered safe dividend; and BTI also has a wide moat (as described earlier) to defend its very strong profit margins (as shown in the table below).

Seeking Alpha

Profit margins as high as BTI's are impressive, especially for a consumer staples stock.

Risks:

Of course BTI does face risks. For starters, it is a tobacco company. Tobacco/ nicotine products are addictive and its products can literally cause cancer. As such, the company is severely restricted in terms of advertising and it is constantly at risk of new damaging regulations and lawsuits. For example, the FDA recently issued a marketing denial order on certain BTI vape products. And for perspective, you can see how litigation impacted cash flow results in recent years in the table below.

BTI Investor Presentation

Another risk is that BTI may or may not get its growth strategy right. For example, there is a certain degree of experimentation (and research & development costs) associated with developing and releasing new products. Further still, BTI has made expensive inorganic acquisitions in the past that have negatively impacted its margins (such as its 2017 Reynolds acquisition ).

Further still, in its quarterly earnings release, BTI describes its own principal risks as follows: Competition from illicit trade; Geopolitical tensions; Tobacco, New Categories and other Regulation (that can interrupt the growth strategy); Litigation; Significant increases or structural changes in tobacco, nicotine and New Categories related taxes; Inability to develop, commercialise and deliver the New Categories strategy; Injury, illness or death in the workplace; Disputed taxes, interest and penalties; Foreign exchange rate exposures; Solvency and liquidity; Climate and circularity.

All things considered, BTI is a very healthy business from a profitability and dividend standpoint, but there are risks, particularly tail risks related to the challenges the entire tobacco industry faces.

The Bottom Line

If ever there was a company that should pay a big dividend, it is British American Tobacco. BTI is very profitable and highly cash generative, but it doesn't have a ton of long-term growth (i.e. this is the big dividend sweet spot). In fact, we like British American Tobacco enough to include it as one of four select ideas in our new free report 100 Hated Stocks: These 4 Worth Considering . However, at the end of the day, you need to select only investments that are right for you and your own personal situation. We believe disciplined goal-focused long-term investing will continue to be a winning strategy.

For further details see:

British American Tobacco: 25 Hated Dividend Growth Stocks Compared