CA - Brookfield Asset Management Should Prosper Despite Brookfield Property Partners

2023-06-04 08:00:43 ET

Summary

- Real estate and Infrastructure are the biggest sources of fees for the new BAM.

- Concerns about BPY's Real Estate may be negatively affecting BAM shares. Based on comps, BAM appears undervalued.

- Analysis of BPY makes these concerns hardly justified. BAM is likely to climb once the company starts increasing its dividends.

- Under the same BPY analysis, its four preferred issues appear less risky than it seems at first, and their distressed price may account for risks.

- Out of the four risky preferreds, BPYPN seems the most promising.

"Strange case of Brookfield Asset Management and Brookfield Property Partners" was my first title for this post alluding to the famous story by R.L. Stevenson. I do not think there are any doubts about who is Dr. Jekyll and who is Mr. Hyde in this couple of entities.

Brookfield Asset Management ( BAM )

Asset management is the crown jewel of Brookfield's empire generating ample and recurring cash flows. After December's spinoff, the business is split between BAM (25%) and Brookfield Corporation ( BN ) (75%). BAM's filings are the looking glass for this business.

{kind=link}

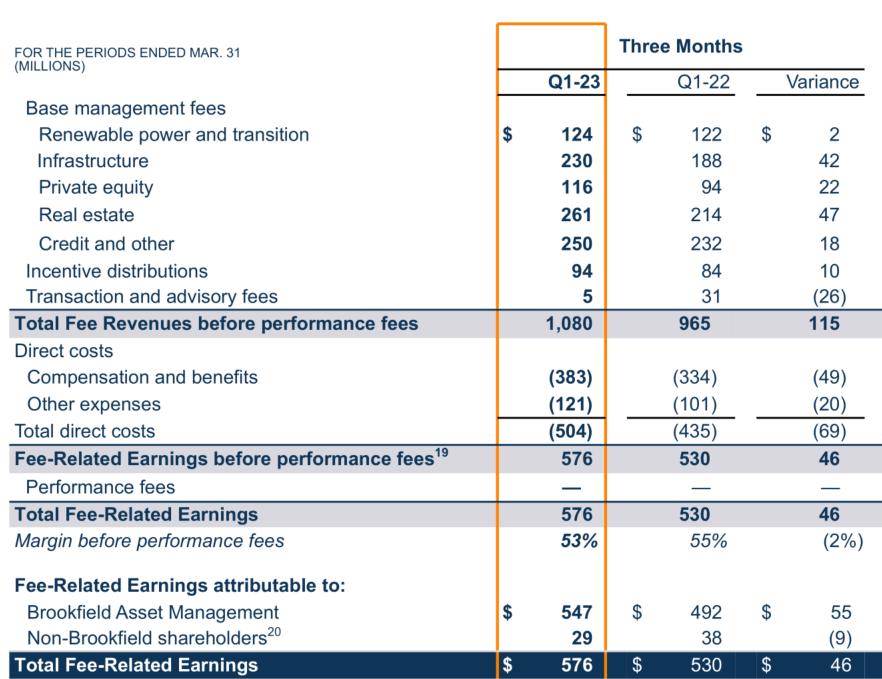

From the table above, Real Estate ("RE") generates higher fee-related earnings ("FRE") than any other business. Even though Credit fees are higher than from RE in the table, FRE from Credit are much lower. This is because Credit means mostly Oaktree with only 68% of BAM's ownership and margins almost twice below that of Brookfield's. Credit's FRE are only ~ $58M in Q1 (about twice of FRE going to Non-Brookfield shareholders in the table). RE generated close to 261*0.6 ~ $157M in FRE. Summing up, RE and Infrastructure are the two biggest sources of fees by far (Infrastructure also generates the lion's share of incentive distributions).

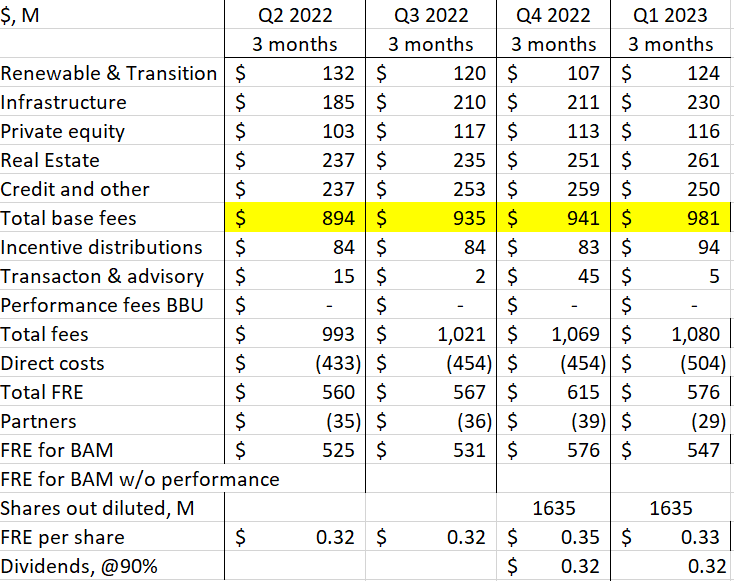

If we look at the time evolution of fees, only Infrastructure and RE are consistently growing with the former growing more quickly.

{kind=link}

From this standpoint, everything seems fine except for an important detail: Infrastructure fees are more or less transparent as they come from publicly trading Brookfield Infrastructure Partners ( BIP ) ( BIPC ) and private funds under the watchful eyes of institutional investors. RE fees come from private funds and private Brookfield Property Partners ( BPY ) with the latter being rather opaque.

We do not know the details of how Brookfield is assessing fees on BPY but have every reason to believe that fees are related to the value of assets under management ("AUM") that probably consists of IFRS equity plus net recourse debt plus preferred stocks.

There is another important difference between Infrastructure and RE: from multiple sources (including BIP filings), we know that this business is performing fantastically well. In my opinion, if it were not for the high fees payable to BAM, BIP would be an outstanding investment (for details, please check my " Brookfield Infrastructure: checking numbers before rushing in").

BPY, on the other hand, is facing a lot of troubles, not unlike other CRE companies, but exacerbated by overleverage. If only investors start thinking that RE fees are arbitrary and shakier than from other sources, BAM shares may suffer. In its turn, BN will be hit twice as hard due to both value of its RE holdings and shakier RE fees.

Perhaps, it is already happening to some extent. For BN, I wrote about it in my recent "Brookfield Corporation is undervalued and so what" . Let us now turn to BAM.

At the time of writing, BAM is trading at ~$31 which corresponds to the dividend yield of 4.1%. As I indicated many times, the dividend yield is a good metric to value asset-light and management-fee-centric alt managers as they pay out 85-90% of their earnings. Among big alt managers, only Ares ( ARES ) represents a good but not perfect comp. Ares is not as diversified as BAM and not supported by BN but is trading at a lower yield of 3.5%. It should be the other way around. Concerns about BPY fees might explain the discrepancy.

Brookfield Property Partners

BPY is domiciled in Bermuda and was public until Brookfield privatized it two years ago. However, four preferred stocks linked to BPY remain public (there are many preferred issues linked to BPY subsidiaries but we will not discuss them).

{kind=link}

All are trading at a depressed level with high yields.

I published about them half a year ago ( "Brookfield Property Partners Preferreds..." ) when they were at $15-16. The issues have dropped further since and higher interest rates only partially explain it. RE concerns may affect BAM and BN, but due to public preferreds, BPY quarterly 6-K filings are the only direct window into RE.

BPY comprises three segments: LP Investments, Core Office, and Core Retail.

{kind=link}

ln BN's filings, RE is split differently: LP investments, Core RE that includes prime offices and prime malls, and Transitional & Development RE for everything else.

LP Investments represent Brookfield's capital in traditional private funds and should be of the least concern to us. Private funds buy opportunistic RE, fix or improve it, and sell upon rent stabilization at a higher price. At that point, BPY receives back its initial capital with profits. Over the long history through many cycles, these funds have delivered superior results and I do not see any reason to expect anything different this time. However, consolidating multiple private funds in different phases distorts the financial statements. Luckily, filings include segment results as well.

{kind=link}

FFO for both Office and Retail have dropped which BPY attributes primarily to higher interest rates on variable debt obligations.

At first sight, negative FFO seems deeply troubling as, besides $237M payable in fees to BAM (they are included in FFO), BPY also paid $145M in distributions to BN, and about $19M in preferred distributions. How safe are these payments?

Fees are by far the safest. There is a Management Agreement between BPY and BAM in place that stipulates that fees are payable (almost) always. Preferred distributions are the next, with common distributions being the most vulnerable.

But where is cash coming from with negative FFO? BPY has another source of financing not reflected in FFO - dispositions of Transitional & Development properties and selling interests in their attractive prime properties. Currently, BPY has $14.5B in their Core properties and $9.4B in Transitional & Development. Even though sales of Transitional & Development are progressing slower than investors would like, BPY can always speed up things by lowering ask prices. Their Core properties should remain rather lucrative and can be sold as a last resort.

Fees and distributions do not seem jeopardized for the next several years at least until the interest rate cycle turns around. IFRS values are likely to suffer which should cause some reduction in fees. However, arcane methods used and controlled by Brookfield to value its properties will prevent significant drops. Meanwhile, other big segments of Brookfield (Infrastructure, Renewables and Transition, Insurance, and Credit) will grow making RE fees less significant with time.

Since BAM's fees are not under pressure, the comparison with Ares indicates that shares may climb upon the start of dividend increases (as a reminder: it did not happen in Q1).

BPY Preferreds As An Investment

Our dive into BAM and BPY provides some conclusions about the latter's four preferred issues. I have seen some warnings about them that mention negative FFO, variable rate debt, and certain problems with Transitional & Development. This is all true but it misses the role of BPY within the broader Brookfield complex. By no means do I imply parent's support - it is unlikely to come.

Preferred issues are no doubt risky and should not be bought or even held because of yield only. Please find something safer for this purpose. However, the issues can appreciate within 2-3 years once interest rates start dropping. The drop in interest rates will make all preferred issues more attractive and drastically improve BPY FFO. It will be also easier for BPY to unload Transitional & Development. Meanwhile, the distributions will keep coming and the total return should be close to 100% within the same 2-3 years.

This picture may seem too rosy without analyzing the risks involved.

Interest rate risk is the first to mention. As long as rates keep climbing, preferreds will keep dropping but this is temporary. Once investors are ready to hold several years, the cycle should turn around. I would not be overly concerned about this risk.

Can BPY stop paying preferred distributions voluntarily to conserve cash? I think this risk is remote. In Q1, BPY paid $145M in distributions to BN. The combined quarterly distribution for all four issues is close to $19M. BPY distributions are vital for BN and they are conditioned on preferred distributions.

Can BPY be forced to stop paying preferred distributions because there will be not enough cash left? This is possible but not very likely. As we already know, FFO is not the only source of cash and dispositions provide a lot of liquidity as well. BPY has two levers to manage this source. It can either drop the price for Transitional & Development or consider selling prime properties or at least interest in them (they have already done the latter). In my opinion, BPY will sell as much RE as needed to continue paying both preferred and regular distributions for many years until interest rates start dropping.

Can BPY use some legal trick to strand preferred issues? For example, can they delist preferreds making their price artificially low, and then buy them back for pennies? Or somehow stop paying preferred distributions while keeping distributions to BN intact? This risk seems more realistic to me.

Certainly, any ethical or legal arguments against it do not stand. In the past, Brookfield stranded preferreds for their portfolio companies a couple of times. It is also difficult to sue BPY because of its Bermuda domicile.

However, BPY is not a portfolio company. It is an important fully owned subsidiary for the conglomerate that issues preferreds for strategic purposes to finance its other businesses such as Infrastructure and Renewables. If they discredit one set of their preferred issues, they may lose this source of financing for all segments.

But there is an even stronger argument. From our previous analysis, we know that BPY plays a vital role for both BAM and BN. On the last BN earnings call, management spent a lot of effort persuading investors of RE safety. The confidence in RE will be gone if Brookfield starts playing with preferreds tweaking something. Consequently, both BN and BAM should plunge. And all this to achieve rather meager gains. Seems unlikely.

That leaves the last risk. What if interest rates remain high for many years and Brookfield RE crumbles under their weight? Theoretically, it is possible but it represents a doomsday not only for Brookfield but also for many other entities, including the US government. But even under this grim scenario, preferreds may survive (or at least have some residual value) due to the non-recourse nature of most of BPY's debt. Transitional & Development (or at least a big part of it) will be gone together with the related debt. LP investments and prime properties have a good chance to keep functioning.

I do not want to be misunderstood. The preferred issues are risky due to the combination of the factors I described. Should only one risk materialize, preferreds might be ruined. The combination of risks is far more dangerous than any one of them individually. In the worst-case scenario, investors may lose about 70-80% of their capital (100% of investments less distributions for, say, 2-3 years). In the best-case scenario, they should gain about 100% over the same 2-3 years. We do not know which scenario will unfold, but the probability distribution seems skewed to favorable scenarios under our analysis.

The preferreds appear risky but investable as a part of a diversified portfolio.

Of the four issues, I like BPYPN the most. It is cheaper than others and consequently, has higher appreciation potential and lower risk for the same quantity of shares.

Conclusion

I wonder if it is justified to write so much about different pieces of Brookfield. Certainly, your positive responses encourage me. Without them, I would write less about Brookfield. There are plenty of other topics.

However, I believe it is very instructional to follow this company. Perhaps, deciphering Brookfield's maneuvers is as useful as analyzing Berkshire Hathaway ( BRK.A ) ( BRK.B ) and Buffett's moves. Investment rewards may follow as well.

If I decide to post timely updates on this and other publications, I will do it through pinned comments. You will not miss them if you follow me in real-time.

For further details see:

Brookfield Asset Management Should Prosper Despite Brookfield Property Partners