EAF - Brookfield Business Partners: EAF Highlights The Challenging Environment

2023-07-11 14:46:59 ET

Summary

- Brookfield Business Partners is up about 5% since our last update.

- Q1-2023 numbers look ok on the surface.

- Corporate liquidity is adequate but some underlying holdings are likely feeling the stress from higher interest rates.

- We go over one publicly traded one that highlights how refinancings will drain cash flow.

It is easier to get the longer-term outlook on a stock correct than to pick out every peak and valley in the price movement. But even the former requires periodic follow-ups to make sure the course has not changed. Brookfield Business Partners L.P. ( BBU ) ( BBU.UN:CA ), is certainly one which we have got the longer term correct. While the public has been enamored with the Brookfield Corporation ( BN ) association and the private equity like setup, we saw this as a less-than-ideal setup. Last December, we highlighted once again how BBU kept disappointing its investors. The stock took off just after that update, but since then has given up 80% of peak gains.

We go over the Q1-2023 results and highlight what challenges are likely to weigh on the company for the rest of 2023.

Q1-2023

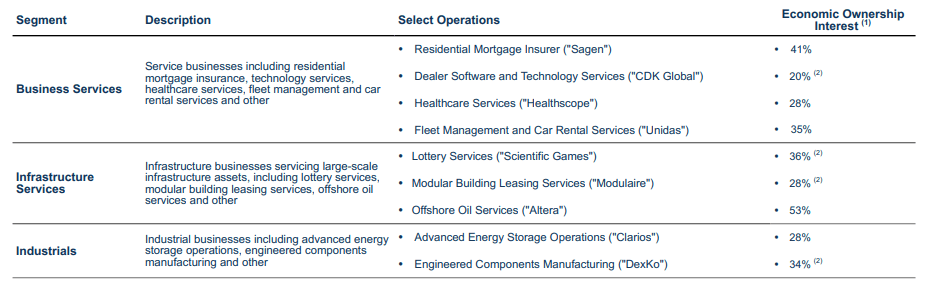

BBU is an amalgamation of many businesses, and the composite picture is usually hard to assimilate.

{kind=link}

On the widest and most generous metric out there, though (adjusted EBITDA), things looked relatively rosy for the company.

BBU Q1-2023 Presentation

Adjusted EBITDA was up across all lines and rose 28% year over year. The company's own secondary metric adjusted EFO did pretty well too, even though it was down sharply in the infrastructure segment. The one luxury the market gives companies like BBU is that they can focus on more lenient metrics like Adjusted EBITDA and Adjusted EFO. These generally have a low level of bearing for most other conglomerates, which turn their attention to earnings per share. On that earnings front, we see that BBU generally does not generate much on a consistent basis and only creates a meaningful number when there is an asset sale.

Balance Sheet

A key reason here to ignore the adjusted EBITDA numbers is because they of course exclude the "I" which is interest. BBU's balance is quite levered up, and you can see this by glancing at the consolidated total assets to total equity ratio approaching 5X.

BBU Q1-2023 Presentation

Consolidated levels here include even portions of these corporations not controlled by BBU. A different way to look at this is by examining the ratio of the equity market capitalization of BBU and proportionate non-recourse borrowings. This number is in a similar zone, and you can see the leverage levels dominating the picture.

BBU Q1-2023 Presentation

One other interesting way to examine the leverage is to look at the plain old income statement, without getting into all the "adjusted" stuff. Here you can see how the interest expense has almost doubled year over year to $865 million.

BBU 6-K

Outlook & Valuation

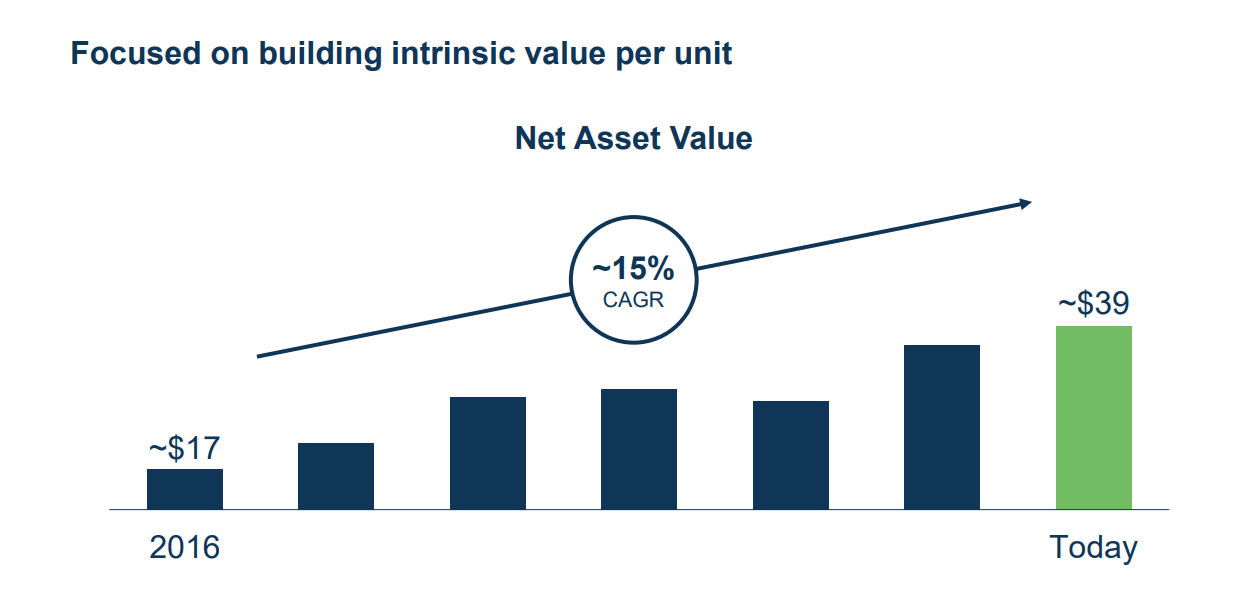

If you are a Brookfield fan, you ignore everything we say and just go with BBU's self-assessed net asset value for the September 2022 presentation.

BBU September 2022 Presentation

{kind=link}

$39, ergo, buy at $17.70. We think those numbers are so far removed from reality that we would just throw them out and start fresh. Even for those that are inclined to believe the Brookfield presentations, keep in mind that they took Brookfield Property Partners L.P. private at a huge discount to the self-assessed NAV.

All the underlying subsidiaries carry a pretty substantial chunk of leverage and if you adjust exit EV to EBITDA multiples down 1-3X, you will find that even the $18 current stock price might be optimistic. We actually saw one case study for BBU play out last year where the sale of Westinghouse was assumed to occur at 14X EV to EBITDA and boost BBU's NAV by $7.00. The actual sale occurred at 10.5X EV to EBITDA and required another Brookfield entity to actually buy half the stake . We will add that all of those negotiations occurred at a time when everyone believed the terminal Fed Funds rate would be under 4%. So on the whole, we see a challenging set of conditions for BBU to monetize assets at anywhere close to its reported NAV. But that is not all. The existing businesses do have to refinance their debt, and we will see this play out over the next couple of years. In fact, BBU was asked about this and pointed to the fact that one company in their fold, extended its debt in a rather uneventful manner.

Geoff Kwan

Okay. Actually, maybe if I can ask one last question. You talked about doing debt refinancing at a number of your companies. When you take a look at the portfolios today, like, would there be other - how much more - do you think you might either have to do or where you think there's a window to opportunistically extend term at a reasonable cost?

Jaspreet Dehl

Yes. So Geoff, we're constantly kind of watching the market and we like to be opportunistic where we can. But just in terms of kind of our overall debt profile. So the weighted average maturity on the debt today is 5.5 years. Mark touched on the recent refinancing that we did at Clarios that actually extends our maturities now to 5.8 years. And in the next 12 months, we've got 5% debt maturing of our overall debt. So there's not a whole lot that's very imminent for us.

Source: BBU Q1-2023 Transcript

Well, that refinancing mentioned was for Clarios, probably one of BBU's most stable businesses. The cyclicals are not doing so well when it comes to refinancings. Let us show you GrafTech International Ltd. ( EAF ), a publicly traded company where BBU owns about 25% of the equity. EAF has some issues that go beyond just the cyclical nature of the business ( see this ). But the numbers are still eye-popping when it comes to debt refinancing.

BROOKLYN HEIGHTS, Ohio--(BUSINESS WIRE)-- GrafTech International Ltd. ("GrafTech") today announced that its indirect, wholly-owned subsidiary, GrafTech Global Enterprises Inc. (the "Issuer"), priced its private offering of $450 million aggregate principal amount of 9.875% Senior Secured Notes due 2028 (the "Notes"), including $11.4 million of original issue discount to yield 10.500% . The Notes will be issued at a price of 97.456% of their aggregate principal amount. The offering is expected to close on June 26, 2023, subject to customary closing conditions.

The proceeds from this offering are intended to be used to repay the debt outstanding under the secured term loan facility provided for by the credit agreement entered into by GrafTech in February 2018 (as amended, the "2018 Credit Agreement") and pay all related fees and expenses and, to the extent any proceeds remain, for general corporate purposes.

Source: Seeking Alpha

The press release is slightly garbled further down, but it appears that the issuance is being used to pay off debt at 4.625% . Even in isolation, pricing at 10.5% is hardly cheap. This is about half of their total net debt of $950 million, so interest costs are going through the roof for at least one BBU baby.

Verdict

Is BBU going to go under? No. They have maintained a clean balance sheet at the corporate level. Some of their more defensive names like Clarios are doing quite well.

As a reminder, Clarios is the world leader in low voltage batteries, powering one in three vehicles globally with unmatched scale and geographic reach. We are five to six times larger than any of our nearest competitors and we're the only true global player. We have the number one market position in the Americas and Europe and are currently number three in Asia. To put this in context, we ship over 150 million batteries per year. And when the business was acquired by Brookfield, EBITDA was approximately $1.6 billion. We set a record year of earnings in fiscal 2021 and we continue to make strong progress in fiscal 2023 and plan to exceed $2 billion of EBITDA over the next few years. And depending on how much we reinvest in the growth, the business should generate at least $500 million or more of free cash flow each year. Approximately 80% of the volume is driven by the high margin resilient aftermarket demand. We're also the go-to partner for virtually every automaker in the world, and in many cases have majority share, bringing the right levels of technology to solve for their challenges of today and the future.

Source: BBU Q1-2023 Transcript

This is balanced by most of their cyclical names being heavily leveraged and likely to face torturous refinancings. The performance since inception has been underwhelming and BBU has trailed the broader S&P 500 ( SPY ) and Industrial Select Sector SPDR ( XLI ) by more than 100%.

We don't expect BBU to repair this deficit any time soon. The stock might make sense for those that believe that the next rate cut cycle is about to begin and BBU's self-computed NAV is accurate. We don't buy either, and hence, we don't want to buy BBU.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Business Partners: EAF Highlights The Challenging Environment