CA - Brookfield Property Preferreds: Resets As High As 19%

2023-11-21 10:00:00 ET

Summary

- Brookfield Property Partners Preferred shares were last rated Sell.

- Q3 2023 numbers show that Brookfield's expenses have risen sharply, causing negative funds from operations.

- We examine the distribution safety in light of the credit stresses and show you on which preferred the risk-reward is closer to being balanced.

The yield must always be measured in relation to the risk. So when we found that Brookfield Property Partners L.P. Preferred shares, i.e.:

1) Brookfield Property Partners L.P. 6.50 PF UNIT (BPYPP)

2) Brookfield Property Partners L.P. 6.375 CL A (BPYPO)

3) Brookfield Property Partners L.P. 5.75 CL A (BPYPN)

... were not giving the bang for the buck, we gave them Sell rating. Of course, it is considered blasphemy in real estate investment trust ("REIT") circles to say anything negative about the Brookfield Corporation ( BN , BN:CA ) empire, but the numbers were just too compelling. That decision has worked out so far, as the large yield was unable to offset the full impact of gravity.

Seeking Alpha

We review the Q3 2023 numbers today and update our view on the 3 preferreds listed on the U.S. side. We also highlight the one on TSX scheduled to be reset first and which will be yielding over 19%.

Q3 2023

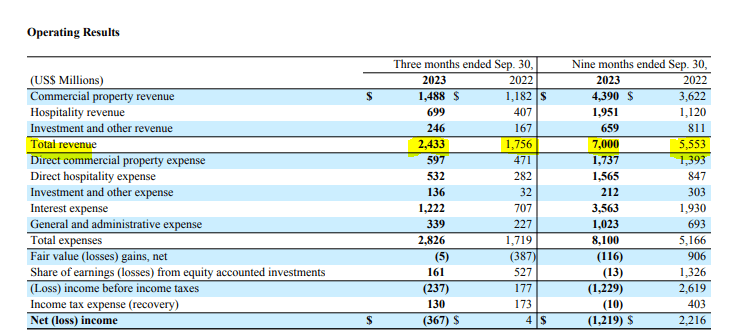

BPY's revenue streams continued to grow in 2023, and we saw that across all three reported segments. There was some bounce from the overall strength in the economy over the last 12 months, as well as some from acquisition activity that was completed. BPY does not break down same property numbers, so the exact impact for each is hard to decipher.

{kind=link}

BPY's expenses rose sharply as well and total expenses increased by 64%, outstripping the 38% revenue gain. The big kahuna there is the change in interest expense ($1.22 billion, up from $707 million), but we want to note here that all expenses were up quite substantially. This is an important distinction versus what we see in most other REITs, where expenses tend to stay relatively static.

Taking a closer look at the interest expense side, we can see that LP investment-related debt is what caused the biggest jump.

{kind=link}

What is causing such a rapid change though in interest expense? Well two things. The first being that BPY bought into "lower forever" and the ZIRP bubble, hook, line and sinker. So their debt came with dual flavor of being short maturity as well having a high amount of floating exposure. You can see below just how much the interest expense on all categories has changed over the last 9 months.

{kind=link}

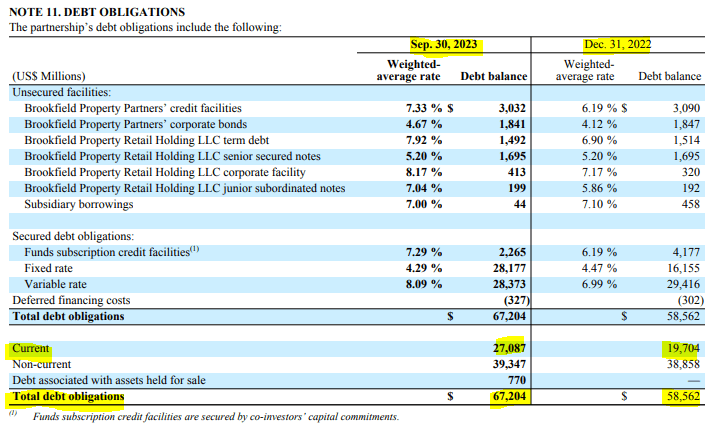

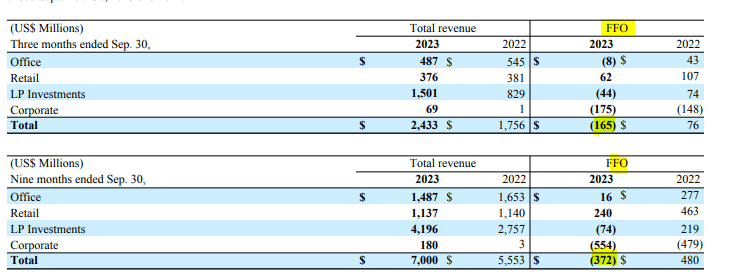

Of course the real fun aspect is the second part. Total debt obligations are higher to the tune of $8.7 billion. Fortunately that portion was "fixed," so the overall impact was still less than it could have been. With interest expenses going vertical it was only a matter of time that funds from operations ((FFO)) went negative. We saw that happen, and FFO came in at negative $165 million.

{kind=link}

Outlook

So if this was publicly traded and you saw a negative FFO you would likely wonder where the money is coming from to pay those distributions. Since it is private with only the preferreds hanging in the public eye, investors have decided to continue holding till things actually break. When they will break is the big question. Here the forces converging are the expire of the interest rate swaps (shown below) and refinancing required on another $30 billion of debt within 1 year.

{kind=link}

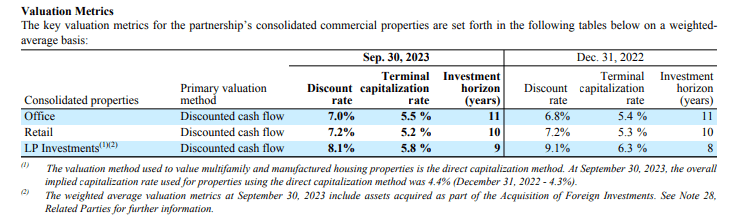

Sure, you might argue that there is still billions of dollars of equity on the balance sheet. That equity stands ahead of the preferred equity. Both good points. That equity, though, has been computed under IFRS using the capitalization rates shown below.

{kind=link}

5.5% terminal cap rates for office and 5.2% for retail. We really cannot write down here what we actually think about those numbers as this is a PG-13 website. But we can say that those cap rates are detached from reality. S&P had cut the ratings last for the debt in 2021 and now has threatened to push BPY into junk territory.

BPY's deteriorating credit protection measures are unlikely to recover materially over the next two years. As of June 30, 2023, BPY's adjusted debt to EBITDA increased to 17.3x from 15.2x at year-end 2022 while fixed-charge coverage ((FCC)) fell to 0.9x from 1.4x. A notable portion of the deterioration was caused by the consolidation of one of its funds' (BSREP IV) U.S. investments in December 2022 and foreign investments in January 2023, which added a material amount of new debt to BPY while EBITDA has not fully cycled through on our trailing-12 month adjusted metrics. BPY owns a 23% financial stake in the fund but fully consolidates it within its financial statements.

That said, interest rates have risen materially over the past year, and BPY's substantial exposure to floating-rate debt (45% net of interest rate hedges as of June 30, 2023) has rapidly deteriorated coverage metrics. S&P Global Ratings economists expect interest rates to remain higher for longer, with one additional rate hike expected in 2023. While we acknowledge that BPY's sizable liquidity position and consistent execution of asset sales mitigate the risk of the company not being able to pay its fixed charges over the near term, BPY has one of the weakest financial risk profiles within our North America real estate coverage given elevated leverage and thin interest coverage. We project adjusted debt to EBITDA to improve slightly to the low-16x area over the next two years but expect FCC to be sustained at about 1x. While we expect BPY to execute meaningful asset sales over the coming years, we anticipate that the majority of proceeds will continue to be distributed up to its parent Brookfield Corp. (BN; A-/Stable/A-1) rather than allocated for debt repayment.

Source: S&P (emphasis ours).

16X debt to EBITDA with a less than 1.0X fixed charge coverage is where this stands today. Of course you got that when you saw the negative FFO but it is always good to hear from S&P. They also touch on the weighted maturity of 3 years, which shows just how much refinancing you should expect in a hostile market. 3% of its mortgages are in default and occupancy levels are not looking too great on the office side.

{kind=link}

The declines have been steady though not too drastic. But that is what you expect when fundamentals are bad in REIT land. The declines occur as old leases roll off.

The TSX Issues

There are a ton of Brookfield preferred shares listed on the TSX. We want to focus on the two that are about to be reset shortly.

1) Brookfield Office Properties Inc. Class AAA Preference Shares Series AA ( BPO.PR.A:CA ) trading at $9.32 CAD. This one will reset on December 31, 2024 at Government of Canada 5 year yield (GOC-5)+3.15%. If the GOC-5 remains unchanged, till then, it would translate into a 19% yield on the current price. The current dividend is 29.4 cents a quarter and that creates a 12.65% yield on the current price.

2) Brookfield Office Properties Inc. Class AAA Preference Shares Series T (BPO.PR.T:CA) trading at $12.57 CAD.

This one will reset on December 31, 2023 at Government of Canada 5 year yield (GOC-5)+3.16%. The reset should be announced very shortly. If the GOC-5 remains unchanged, till then, it would translate into a 14% yield on the current price.

Verdict

There is a huge difference in yields for those resetting immediately and those resetting further out. With BPO.PR.A , you also get a huge discount to par value. So if you had to bet on one here, just like with debt, you would want to bet on the most discounted one.

On the US side the three preferreds yield about 12.3% each but they are fixed rate. Currently the BPY bonds are appearing distressed and trading fairly wide of SmartCentres REIT ( SMU.UN:CA ).

{kind=link}

We are currently staying out as we think there is a high chance that the debt blows through the equity and the preferred cushions as well.

For further details see:

Brookfield Property Preferreds: Resets As High As 19%