ACTV - Buckle Up For 2 Weeks Of Wild Fed-Driven Volatility In Stocks

2023-03-06 15:06:13 ET

Summary

- Options markets are pricing some volatile days ahead.

- The core tension is around inflation and the future path of Fed policy.

- Many investors are still paying speculative valuations for stocks and housing, betting that a Fed pivot will bail them out.

- But if inflation doesn't cooperate (as it likely won't), investors will find that they overpaid for hot potato assets.

- All in the next 2.5 weeks, Powell testifies for Congress, nonfarm payrolls are released, CPI is released, and then the FOMC meets.

Just because they close the bars doesn't mean the party is over. The broad S&P 500 index ( SPY ) has rallied about 7% this year, with stocks led by massive rallies in speculative names such as Tesla ( TSLA ), Carvana ( CVNA ), and Nvidia ( NVDA ). Underpinning this rally has been a widespread belief by stock traders that the Federal Reserve will soon pivot and start sharply cutting interest rates at any sign of an economic slowdown. Jerome Powell's failure to challenge the speculative frenzy that formed in parts of the stock market early this year has traders hopeful that they can find buyers for their assets at ever-increasing valuations. On cue, pivot rumors ramped up Friday when hawkish Fed board member Christopher Waller had a Zoom speech hacked Friday by pranksters playing adult videos, while nonvoting member Raphael Bostic had his dovish sentiments spread far and wide by the financial press.

If inflation remains stubbornly high, the Fed may even have to go back to 50 bps hikes, taking interest rates to 6%, or even 7% to combat price inflation running over 5% annually. This would be crushing for stocks, which are priced for a return to sharply lower interest rates. The black swan hiding in plain sight is that the market could fall 10% or more in a matter of days if the CPI report next week comes in red hot.

What's The Outlook For Stocks?

Citigroup head of equity strategy Stuart Kaiser put out a helpful note for traders late last week on the implied volatility for stocks, by day. This was then shared by Bloomberg .

Implied volatility is quoted on an annualized basis, but we can use an old trader trick called the " square root rule " to boil it down to an expected daily move (here simply divide by 16 to get the daily expected move). This implies daily moves of 1.4% when Powell testifies before Congress, 1.6% when payrolls come out, 2% when CPI is released, and 2.3% on the day of the FOMC meeting.

Implied Volatility By Day (Citigroup via Bloomberg)

First off, nothing big is likely to happen in stocks until Powell's testimony. Today, some professional traders are likely to cover short positions, some others will take profits on the long side, and retail traders will likely continue pumping some money into meme stocks.

Here's a quick calendar for those interested:

- Powell testimony - Tuesday, March 7

- Nonfarm Payrolls - Friday, March 10 (yes, it's a week late because February is a short month)

- February CPI - Tuesday, March 14

- FOMC Decision & Press Conference, Wednesday, March 22

Powell's Testimony

Tomorrow, things start to get interesting. Powell will testify before Congress, and he's going to get drilled by questions about inflation and rates. Democrats have lined up behind wanting to cut Fed rates and keep them lower, while Republicans have lined up behind more hawkish policy. However, it's actually not so clear that the Democrat's constituency would be hurt by higher rates. Stoking the real estate bubble clearly harmed lower-income and middle-class renters, while higher rates are actually beneficial for unions, public pension funds, and other areas of Democrat support.

Trump famously goaded Powell to cut rates below appropriate levels for the economy, but Republicans now favor higher rates. For context historically, farmers and factory workers supported looser money to make debts easier to pay back (ex. the free silver movement in the US ), while the aristocracy favored the gold standard. Powell going to Congress and getting grilled is part of a long history of different interest groups seeking to sculpt monetary policy to benefit their own interests. Powell does have a tendency to say things that get the market riled up, which is why stocks are expected to move 1.4% tomorrow.

Nonfarm Payrolls

Nonfarm payrolls on Friday are the next big event, and this is another case where good news is actually bad news. If the report shows that hiring continues to be robust and that there are shortages of labor, it's a sign that monetary policy is still too loose. Interest rates are clearly starting to affect rate-sensitive sectors like housing and tech, but the amount of people employed in leisure and hospitality is still below pre-pandemic levels, while demand seems to be quite strong . This is likely where big hiring is likely to continue. Current estimates for nonfarm payrolls are above 200,000 new jobs added last month, which is more than the growth in the US population and would indicate a labor market that continues to get tighter in key areas.

We seem to be at least 1 million workers short of our pre-pandemic trend for leisure and hospitality workers, so my guess is that the jobs report will give the Fed no reason to slow down hiking. That, however, is very bad news for the housing and tech sectors that benefited so immensely from rock-bottom interest rates. Stock market investors are acting a bit wild here, but that's nothing compared to workers stretching big time to buy homes with the bet that they can "date the rate and marry the house" and lower their grim DTI ratios by refinancing to a lower interest rate in the future. Hundreds of thousands of people per month are making this bet!

CPI Could Get A Little Wild

The options market thinks the Fed meeting will be the most volatile day, but my intuition is that this CPI report on March 14 will be a firecracker. CPI nowcasts have core CPI rising at 0.45% month-over-month for February, which would indicate zero progress against inflation and Fed policy that isn't quite too restrictive territory yet.

To get a read on how CPI will come in, I recommend taking a look at the Mannheim used car report (this should come out tomorrow, as it's usually released on the fifth business day of the month). This gets released somewhat quietly, and it will take up to 24 hours for the mainstream media to report on it, but it's a key battlefield for the Fed's fight against runaway price increases. A bad number here dramatically raises the odds that CPI will come in hot. Wholesale used car prices have been shooting up in 2023. Used cars were driving the disinflation narrative since October. If they start going back up again then we have to go back to square one on inflation.

Additionally, countries that report before the US are useful for handicapping CPI at home. Swiss inflation was hotter than expected , and inflation in The Netherlands crested expectations , actually accelerating from January as well. Inflation indicators from Japan show that core prices are accelerating as well.

Overall, February CPI is shaping up to be another slap in the face for pivot-hungry bulls. It's never 100% certain, but the higher-frequency data is coming in poorly for inflation doves with zero exceptions so far this year.

The Fed May Be Behind The Curve Yet Again

Speaking of data revisions that came in poorly, the PCE numbers were revised up for Q4 2022, indicating that inflation had not come down as much as we thought. Then January PCE came in hotter than expected , indicating that whatever slowdown in inflation we had in Q4 of last year is now giving way to a reacceleration in price increases. This is important because core PCE is the main inflation input to Fed policy.

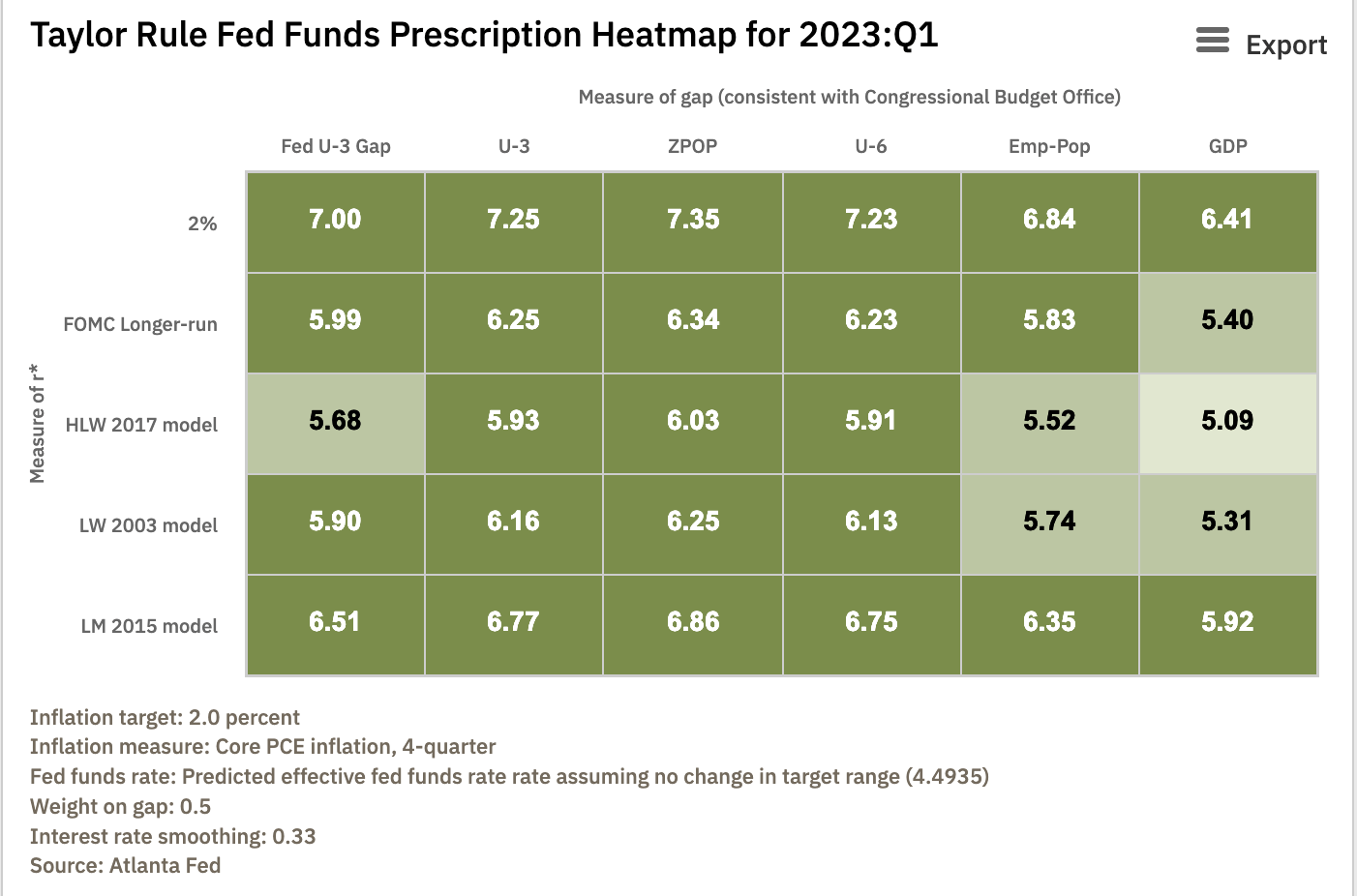

The data is ugly here. We can ballpark where Fed policy should be going forward with standard Taylor Rule-driven models . These starkly contrast the pivot hopes of bulls.

{kind=link}

Taylor Rule Heatmap (Atlanta Fed)

Running 30 models here and letting them compete, the lowest interest rate recommended is 5.1%, while most are over 6% and a few are over 7%. This isn't rocket science – if core inflation is running a bit over 5%, you need cash rates higher than the inflation rate to slow things down. Cranking rates up near 7% is not unreasonable if inflation gets more entrenched in the economy. However, that would take mortgages to 9% and virtually guarantee a recession. The Fed is caught between a rock and a hard place here. If they do nothing, inflation may accelerate from 5% annually to somewhere even worse, and rates would need to go higher still later. If they take rates to where they need them to balance the economy, it will hit housing and tech like a brick. In the end, it's almost impossible to get a soft landing when inflation is out of control because different areas of the economy have vastly different sensitivities to changing interest rates. A better solution would be to raise taxes, i.e. fix Social Security, but the White House and Congress are actually making the Fed's job harder by trying to run bigger deficits into an economic bubble via unfunded stimulus and student loan cancellation.

Another problem is that the Fed is starting to lose some credibility in the eyes of the bond market. 10-year TIPS inflation breakevens have steadily risen since December, meaning the market is starting to doubt that the Fed is capable of bringing inflation down to 2%. The longer inflation continues, the more the market starts to believe that it will continue, and the more the economy starts to price in large rates of inflation into expectations. If it's allowed to go on long enough, the whole economy changes so that people stop investing in organic growth and start investing to take advantage of misaligned government incentives.

The FOMC will meet a little over a week after the CPI report, so they'll have some time to think about how they want to respond. A minority of the market thinks that they may be forced to go 50 bps in response to a hot CPI. A 50 bps hike signals a Fed en route to a 6% cash rate, and I agree with the minority here based on the data I'm seeing. The alternative from some traders and parts of the blogosphere is the idea that the Fed is only pretending to care about inflation, but if the world subsequently loses confidence in the dollar, then the US is all but done as the premier world power.

Bottom Line

Powell's testimony, the nonfarm payrolls report, CPI, and the Fed meeting will put the stock market to a series of huge tests. Based on the way the market is priced, I don't think it will go too well. Large-cap stocks are trading above typical valuations from the 2010s when rates were 0%, and now rates are threatening to go above 6% on higher inflation – and stay there. This is an enormous disconnect. And the bigger this disconnect gets, the sharper the possible correction will be! The risk-reward looks terrible for large-cap stocks here.

For further details see:

Buckle Up For 2 Weeks Of Wild Fed-Driven Volatility In Stocks