WSM - Buy Alert: 3 Top Retail Dividend Growth Stocks For The Santa Rally

2023-12-04 12:02:36 ET

Summary

- Holiday spending shows consumer resilience despite inflation.

- Some retail stocks have shot up and are now overvalued.

- But here are 3 which present great opportunities for dividend investors.

Written by Sam Kovacs.

Introduction

The holiday season is well underway, with Black Friday and Cyber Monday having posted record numbers , which would be flat if adjusted for inflation.

Nonetheless, the fact that the dollar value of holiday spending is up shows that consumers have been more resilient than most expected, and have insisted on living the same quality life, despite the economic pressures of inflation.

We are now seeing certain retail stocks take off as strong Q3 results come in at the same time as optimism for the holiday season.

Williams-Sonoma ( WSM ), for instance, which we suggested investors purchase in April this year , and which we accumulated at an average cost of $120, has rapidly shot up to $195, up 62% in half a year.

WSM DFT Chart (Dividend Freedom Tribe)

{kind=link}

But, of course, in so doing, WSM has moved off our buy list onto our watch list and is closing in on our sell list now.

This doesn't mean there aren't other stocks out there who are seeing strong momentum and that could do very well in the upcoming holiday season.

Here are 3 retail related picks I think are brilliant buys right now.

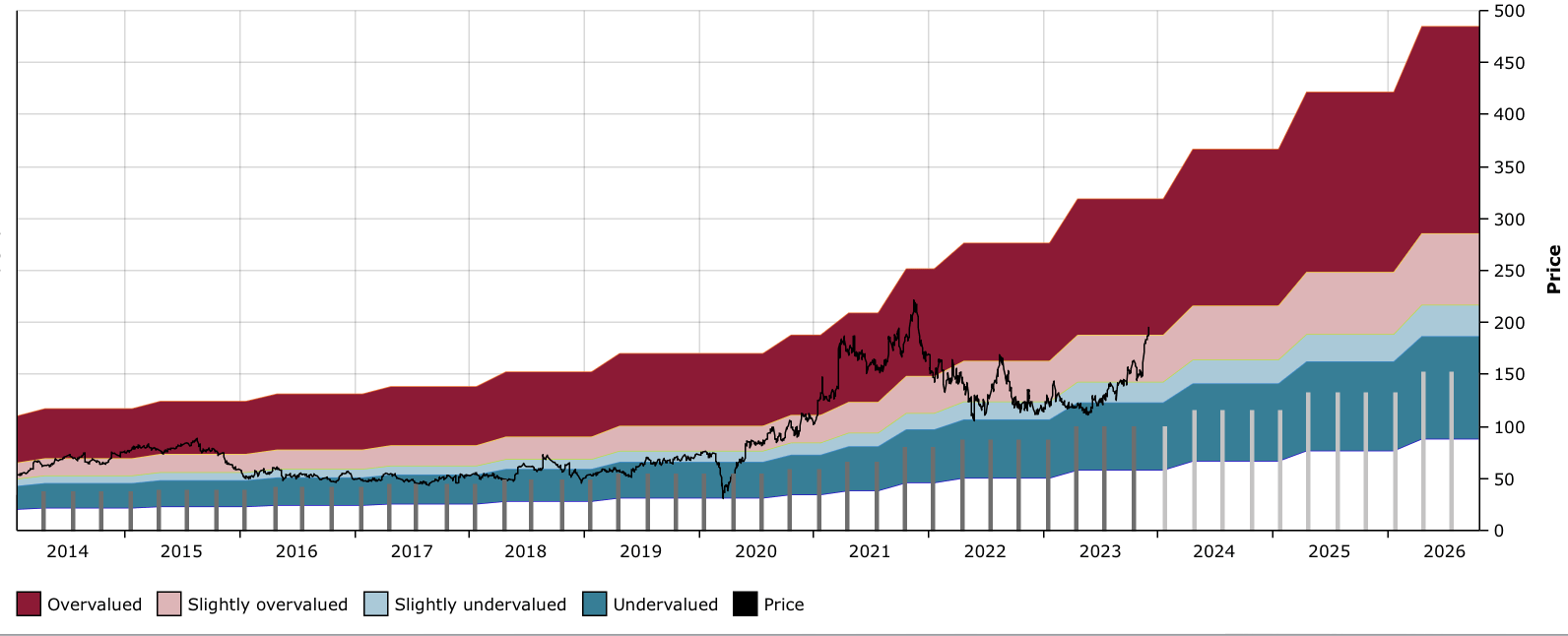

Buy Dicks Sporting Goods

On August 25th, I provided investors of our Investing Group an update on DICK'S Sporting Goods, Inc. ( DKS ), which at the time was trading at $113, after having posted somewhat underwhelming earnings and cutting its earnings guidance.

Bank of America analyst Robby Ohmes downgraded DKS. I dissected his analysis for members, which I suggested was full of "clear recency bias impacting poor analyst work."

I said that buying DKS at that price was a good idea, and that I'd be doubling down on DKS.

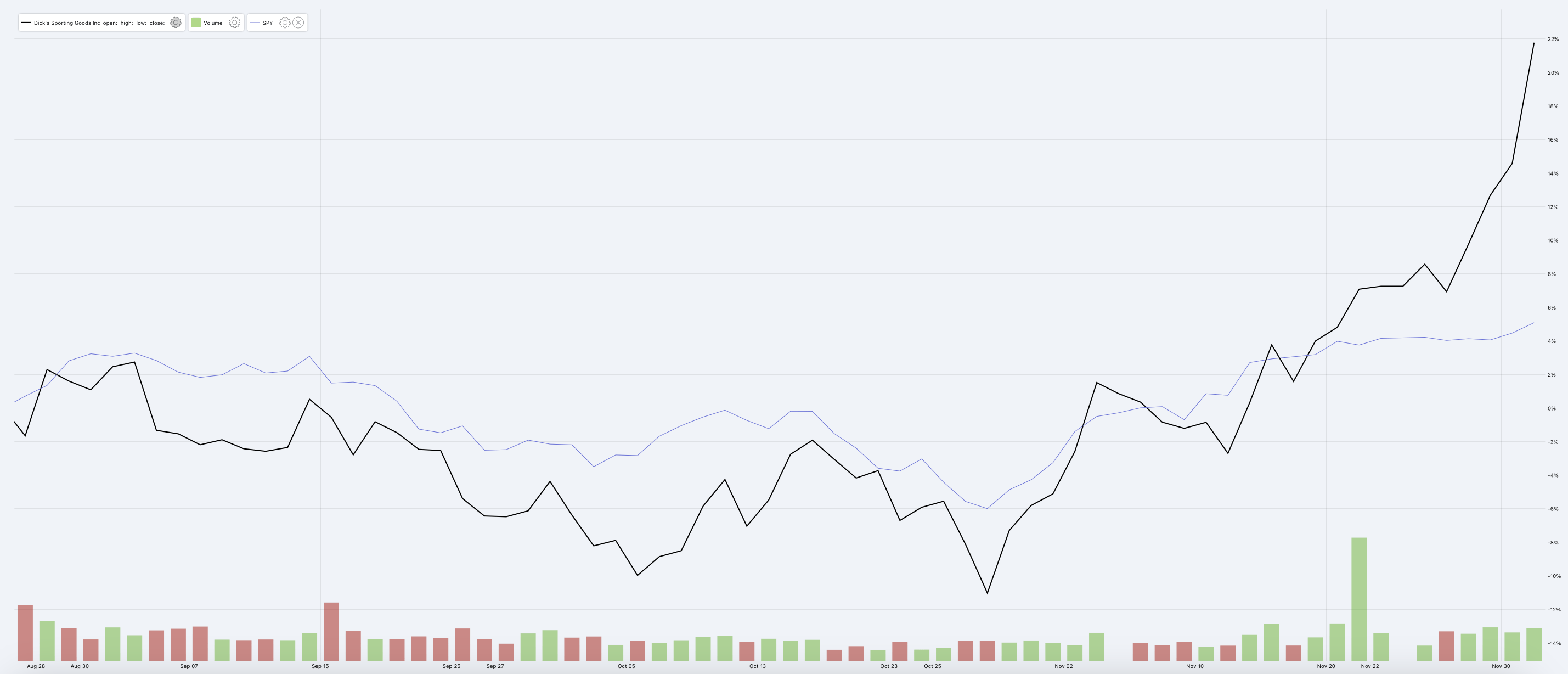

DKS vs SPY (Dividend Freedom Tribe)

{kind=link}

Since then, the stock is up 22%, more than 4x the return of the S&P 500 (SP500).

Sure the stock went a bit lower before recovering, but getting the exact bottom isn't nearly as important as consistently being close enough to the bottom.

After posting its Q3 results, and increasing its guidance back to where it was earlier this year, the share price recovered drastically.

DKS now trades at $138 and yields 2.9%.

DKS DFT Chart (Dividend Freedom Tribe)

{kind=link}

Next quarter, DKS will announce its dividend increase for 2024, and I expect a 10-12% increase, which will be in line with the level of buybacks DKS has enacted so far this year, and therefore will be permitted without increasing the total spend on dividends.

{kind=link}

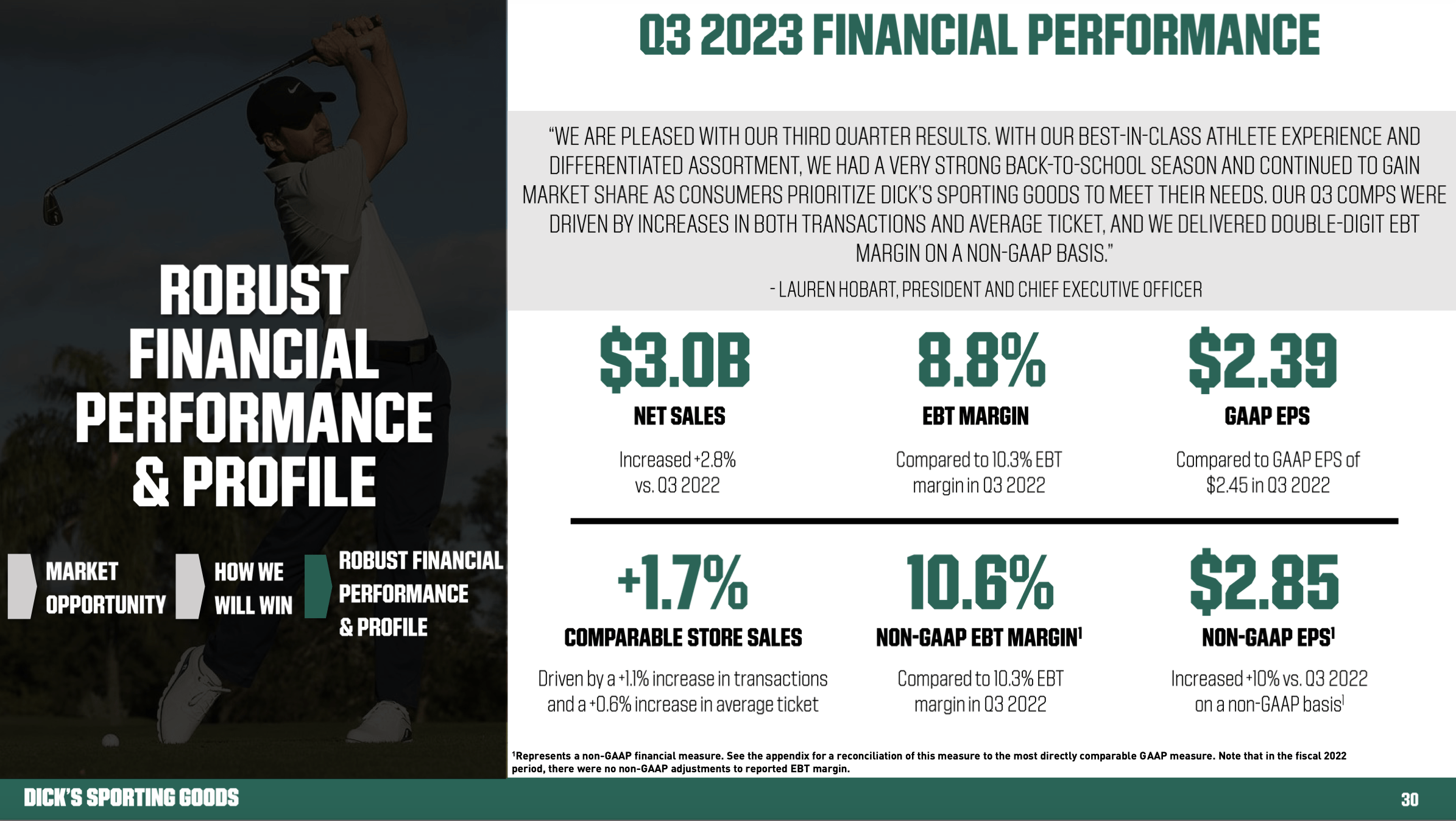

Below is a summary of DKS' 3rd quarter results :

- Net sales increased by 2.8% year-over-year to $3 billion.

- Comparable store sales were up by 1.7%.

- Adjusted EPS rose by 10% to $2.85.

- The company outperformed analysts' EPS expectations of $2.42, reporting $2.85 per share.

- Revenue reached $3.04 billion, exceeding analysts' estimates of $2.94 billion.

{kind=link}

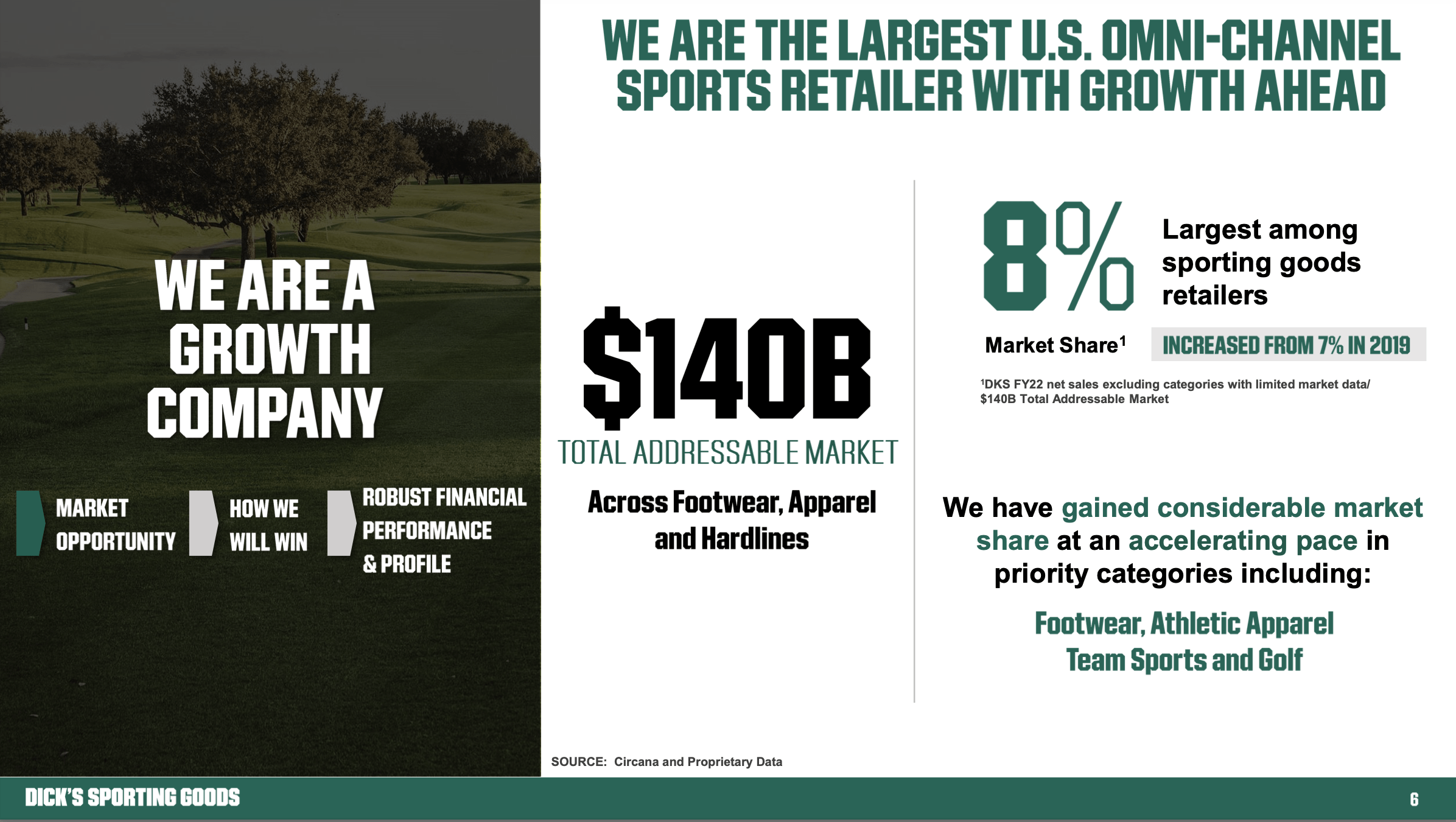

Analysts expected a drop year-over-year in total revenue, but strong performance in terms of both average spend and number of visits drove growth.

This is because DKS has invested heavily in improving customer experience, and they've been gaining market share within the sports retailer space, where they went from 7 to 8% of market share in the past 3 years.

{kind=link}

The revamped House of Sports locations, which provide an immersive and interactive sport experience for customers, provides double-digit growth in revenue within locations converted from the old model to the new model.

By 2027, over 10% of DKS stores will have been converted to House of sports concepts, from just 12 of the 800+ stores today.

Industry insiders have taken notice, with Nike's ( NKE ) CEO making the following comment

I was blown away at the store’s [House of Sport’s] unique service model, interactive sport experience and enhanced showcasing of product, which creates a true destination for consumers and will alter future expectations at retail. -John Donahoe, President and CEO of NIKE, Inc.

DKS is showing great momentum going into holidays, and I expect the stock to challenge its $150 high once again. If it breaks out, then the share price could go bananas.

Buy Target

While analyst Robert Ohmes and I didn't see eye to eye on DKS, we see eye to eye when it comes to Target Corporation ( TGT ).

We got bought buying Target on the way down, which has been beaten down to levels way below fair value.

Back in June, when I last wrote about Target , I said:

Its 3 month performance is among the 90% worst stocks, its 6 month performance is among the worst 82% of stocks, and its 12 month performance is among the worst 72% of stocks.

So the price action has been getting worse and worse.

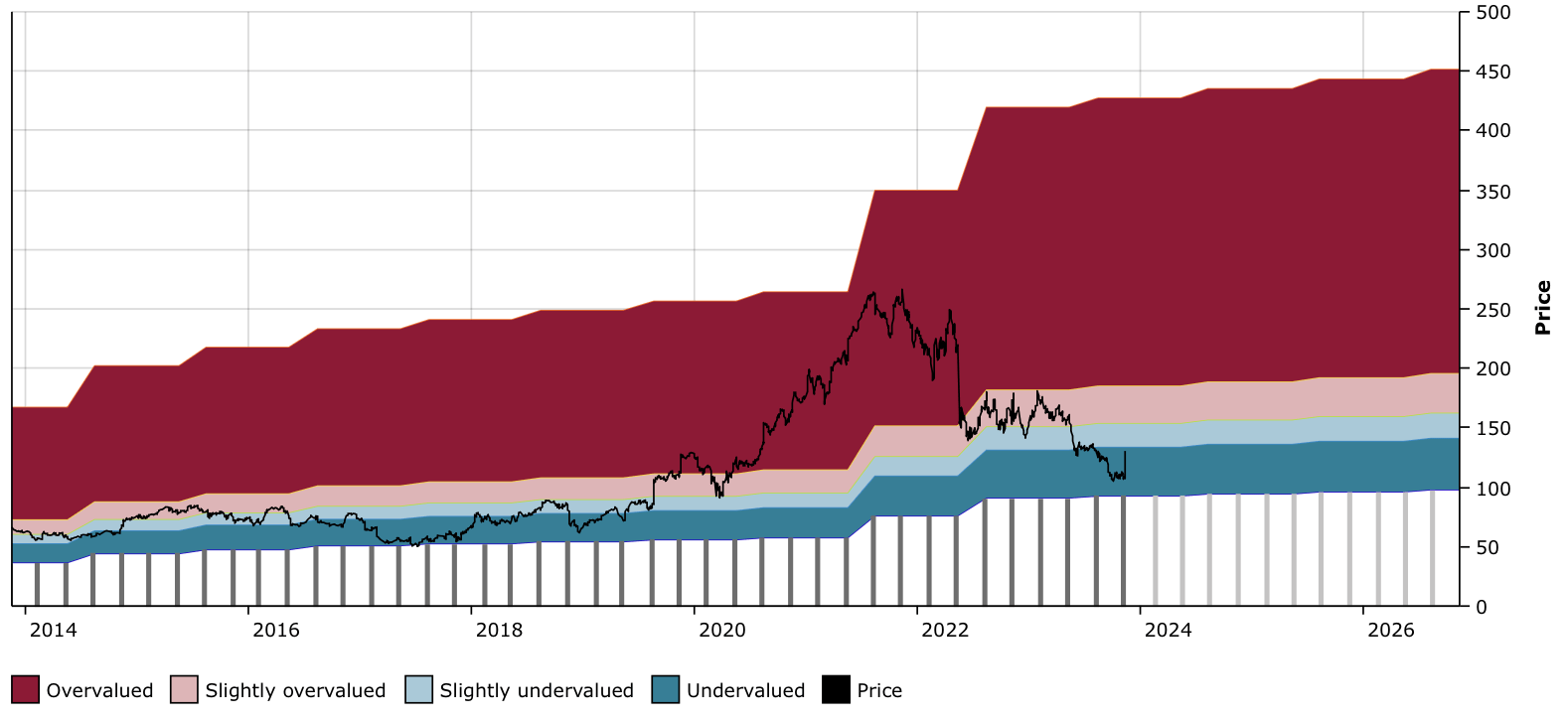

According to the DFT chart, TGT could go down all the way to $100 before finding a bottom.

I believe the $100 mark would provide a strong level of support, if it were ever to get to that.

That would be another 25% downside from the current price.

This is the worst case scenario, which while it doesn't make sense to me based on fundamentals or where the market is heading in general, is definitely a possibility.

Well, the stock didn't quite get to $100 before bouncing, but it did go all the way down to $105.

TGT DFT Chart (Dividend Freedom Tribe)

{kind=link}

The stock currently yields 3.39%. Earlier this year, the dividend was increased by a measly 1.9%, way lower than the 10% CAGR the firm achieved over the past 10 years, in large part thanks to 2 big pandemic-induced dividend hikes in 2021 and 2022.

Let's take a look at the results.

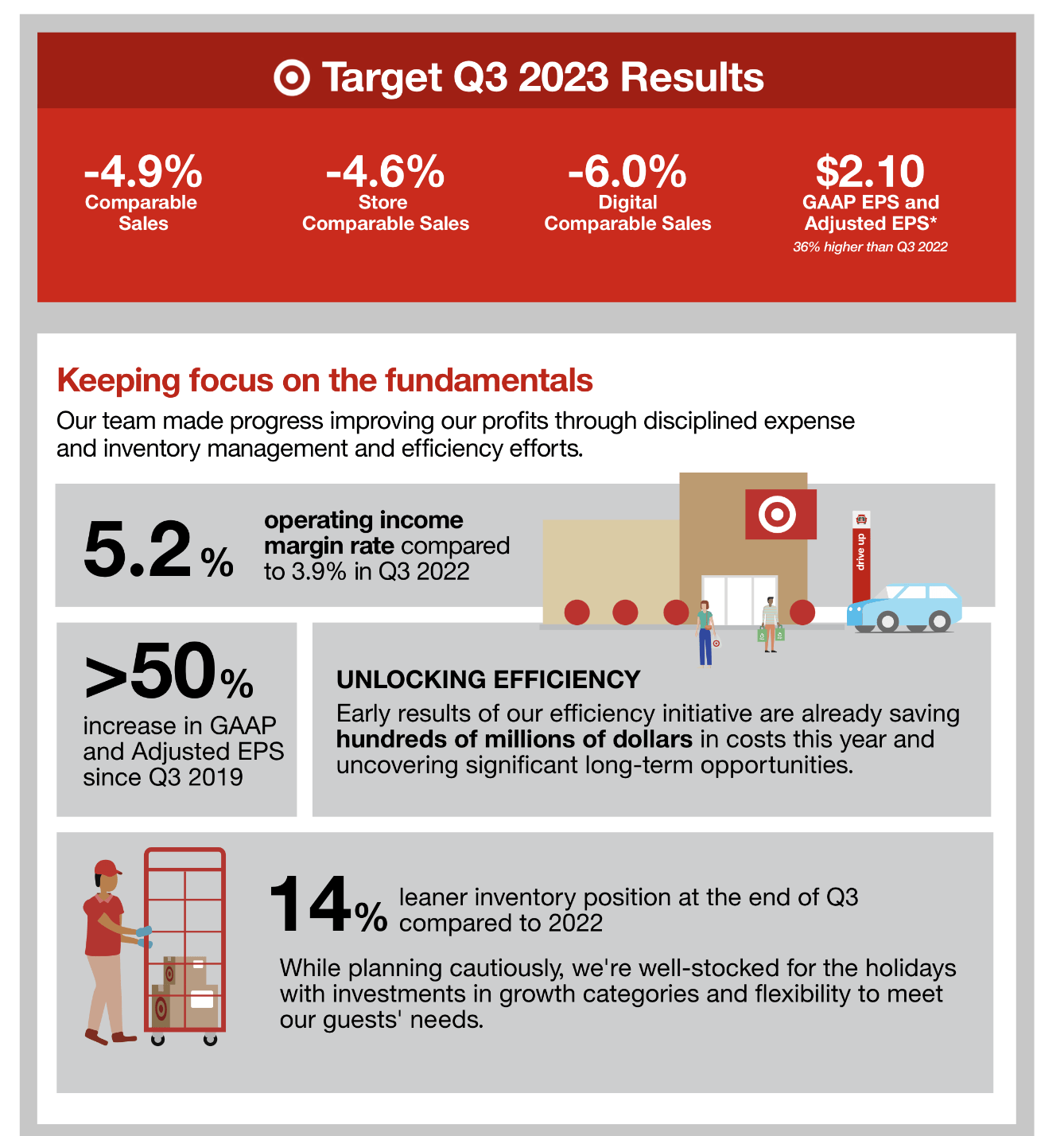

Sales declined by 4.9% in Q3 2023 somewhat as expected by analysts, but the bottom lined surprised most.

Target has achieved a significant inventory reduction of 14%, decreased freight costs, and made enhancements to its supply chain. These efforts resulted in an improved gross margin rate of 27.4%, a 270 basis points increase from the previous year. The operating income margin rate rose to 5.2% from 3.9% last year.

As a consequence, EPS of $2.1 beat by $0.6, and increased by 36% YoY.

{kind=link}

The market responded positively to Target's earnings report, with the stock price rising 9.9% to $121.7 per share post-reporting. Analysts were impressed by Target's performance, especially its ability to exceed EPS expectations significantly.

Wells Fargo upgraded Target to "Overweight" from "Equal Weight," raising the price target to $148.00 from $120.00. This upgrade was based on a margin inflection and a belief that the path of resistance for the stock seems higher??.

Bank of America analyst Robert Ohmes upgraded Target shares to a "Buy" rating from "Neutral" and increased the price target from $120 to $135 per share?.

Now these targets are quite reactive, which shows that analysts had followed the stock down with their price targets, making these things useless.

A price target is only good if associated with a timeframe anyway.

What good is saying "our price target is $148, and we expect it to reach this price anytime between tomorrow and 10 years from now"?

This is beyond me, and why we don't usually give price targets, but rather ranges to buy the stock below and sell above, with the direct implication that you might have to hold to wait.

While waiting, you'll get paid to wait.

Anyways, I digress.

Target's improvements on margins and reduced inventory show that they have been able to right-size their inventory and move towards categories which are less discretionary.

With the global retail sales growth dipping to under 1% year-over-year in 2023, Target, like other retailers, may continue to face challenges due to economic uncertainty. Consumers are becoming more selective in their spending, focusing on necessities due to the prolonged cost-of-living pressures and inflation.

But while consumers are cautious with their spending, there is still a willingness to splurge, especially among younger and higher-income groups. Target can focus on categories like fashion, groceries, and restaurants, which are popular splurge areas, while also catering to the necessities that dominate consumer spending??.

This for me has always been Target's edge, which is not considered by most analysts.

Target is effectively a consumer-staples business, with a discretionary option layered on top.

When discretionary spending goes up, Target can very quickly increase its sales, as it showed in 2021 and 2022. And when discretionary spending becomes more selective, they can shift back to staples, which provides the business with both downside protection and upside opportunity.

This is how the COO summarized this during the last earnings call :

Thanks, Christina. Over the last 3.5 years, our operations have continually faced unusual and rapidly changing external conditions. In 2020 and 2021, after the onset of the pandemic, we couldn't secure enough inventory to satisfy the explosion in demand for our products, and we saw operating margin rates grow well beyond normal levels. Then in early 2022, the period of rapid growth in discretionary categories suddenly reversed, and we quickly moved from having too little inventory to having way too much. As a result, both our distribution centers and store backrooms filled up well beyond optimal levels and operating margin rates quickly moved to historical lows.

So this year, as Brian mentioned, a key priority was to optimize our inventory position so it was better aligned to the current size and growth rate of our business. We were confident that if we were successful in that effort, our operations will become more efficient, markdowns will come back down, and we'd see our profit rate recover back toward more sustainable long-term levels. And through the first 3 quarters of the year, despite unexpectedly soft top line trends, the team has delivered a more rapid recovery in our profitability than we'd even planned at the beginning of the year.

Of course, because of all of this, Target is subject to the economic cycle. Nonetheless, it is clear to me that management has been doing a great job at managing what it could manage.

Yes I'd prefer if the company didn't meddle in politics, which I see as a divisive position which can only lead to negative outcomes given America's bipartisanship and increasing part of personal identity being attributed to political sides.

But at the end of the day, they've shown that in environments conductive to improving top line, they did that aggressively, and when that tide turned, they were able to increase profitability substantially.

I continue to be satisfied with the investment, and expect that the softer comps will set up 2024 to be a success to drive both top line and bottom line profitability

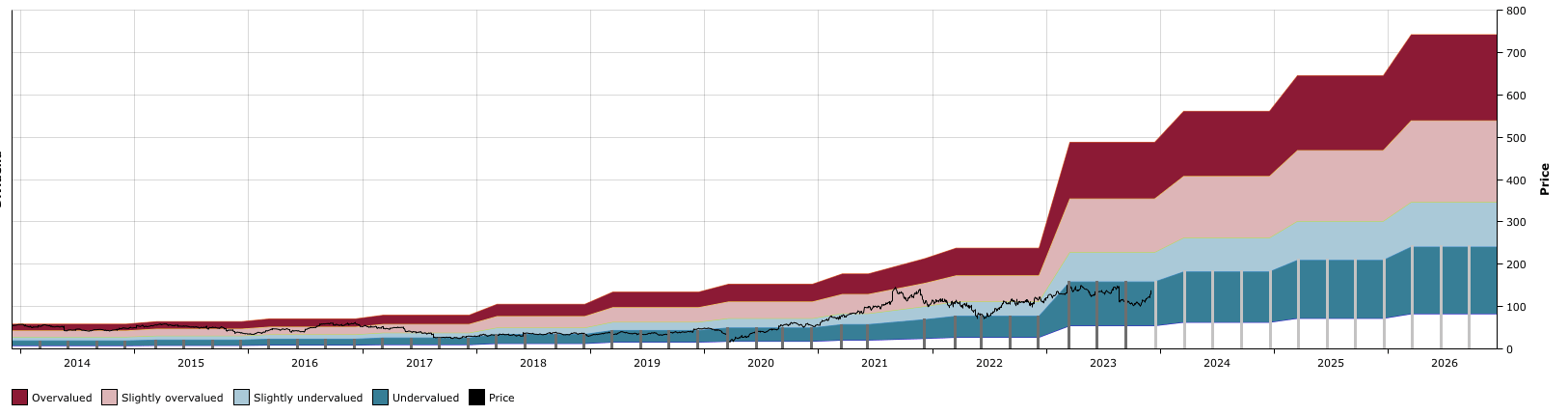

Buy Simon Property Group

The last stock we suggest buying isn't a retailer, but a real estate investment trust, or REIT, which operates high end malls.

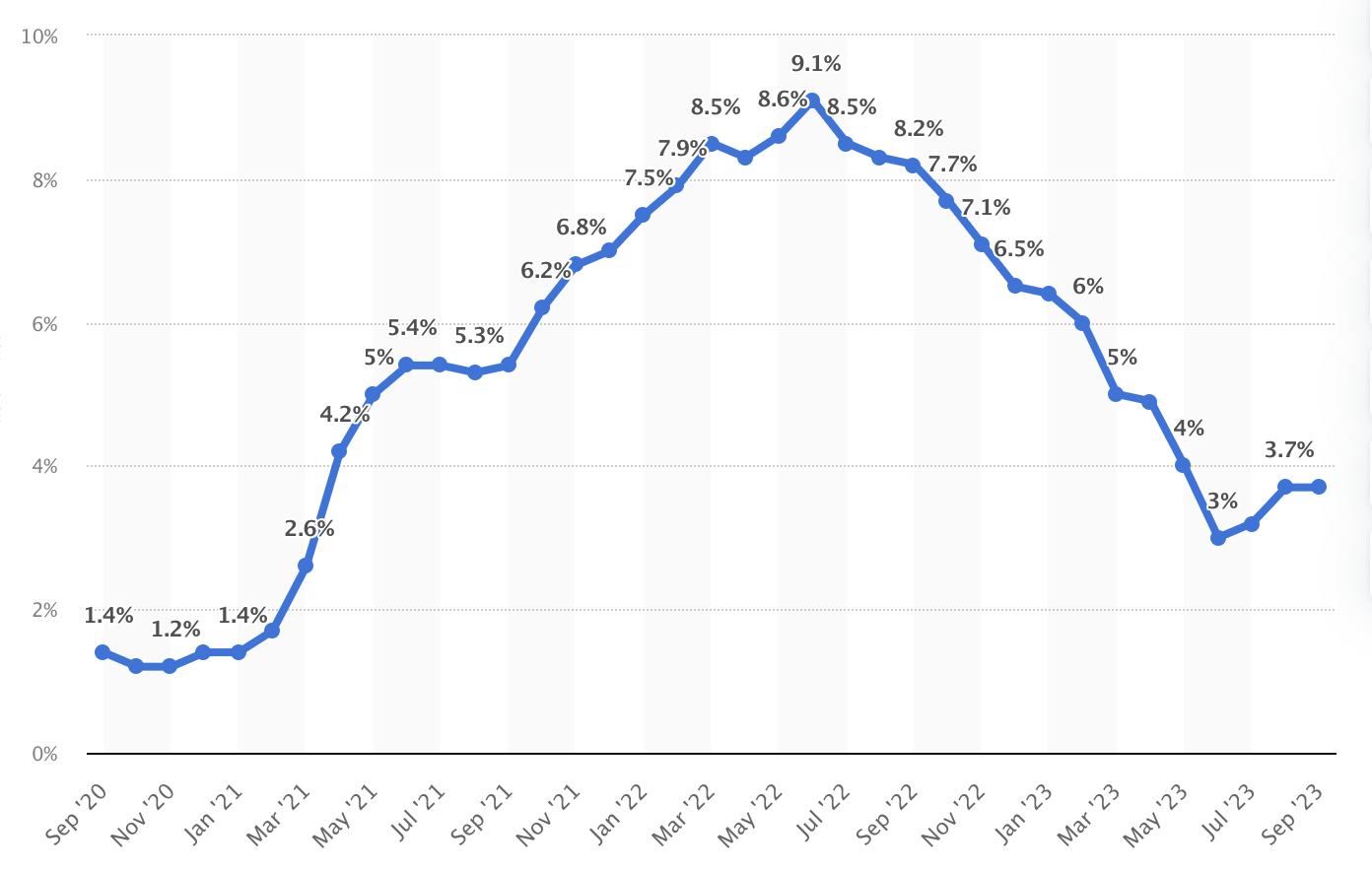

We last looked at Simon Property Group, Inc. ( SPG ) in July 2022, when inflation had just topped out at 9.1%.

{kind=link}

Since then, inflation has gone back down to 3.7%, the lowest level since May 2021.

In July '22, I said that :

SPG is undervalued.

REITs have all been repriced this year (which is the polite way of saying they're down bad).

A 7% yield makes it a bargain. If you buy the stock and the price goes nowhere, over the next year or two, your yield will go up to over 8% just from the dividend returning to its prepandemic level.

SPG should be trading between $140 and $160, not at the current level.

In 2023, The Federal Reserve's continued efforts to curb inflation by raising short-term rates created a challenging operating environment for real estate. The REIT sector's resilience was partially due to strong balance sheet positions, which helped in navigating the higher interest rate landscape?. We've seen many REITs beat expectations and do better than the headlines about REITs suggested.

This is also because REITs took a larger loss in 2022, and have declined 6.8% YTD.

SPG, on the other hand, is down just 2.5% YTD, as it has performed better than the sector.

It currently trades at $128, up 28% from when we last suggested to buy the stock, and yields 5.9%.

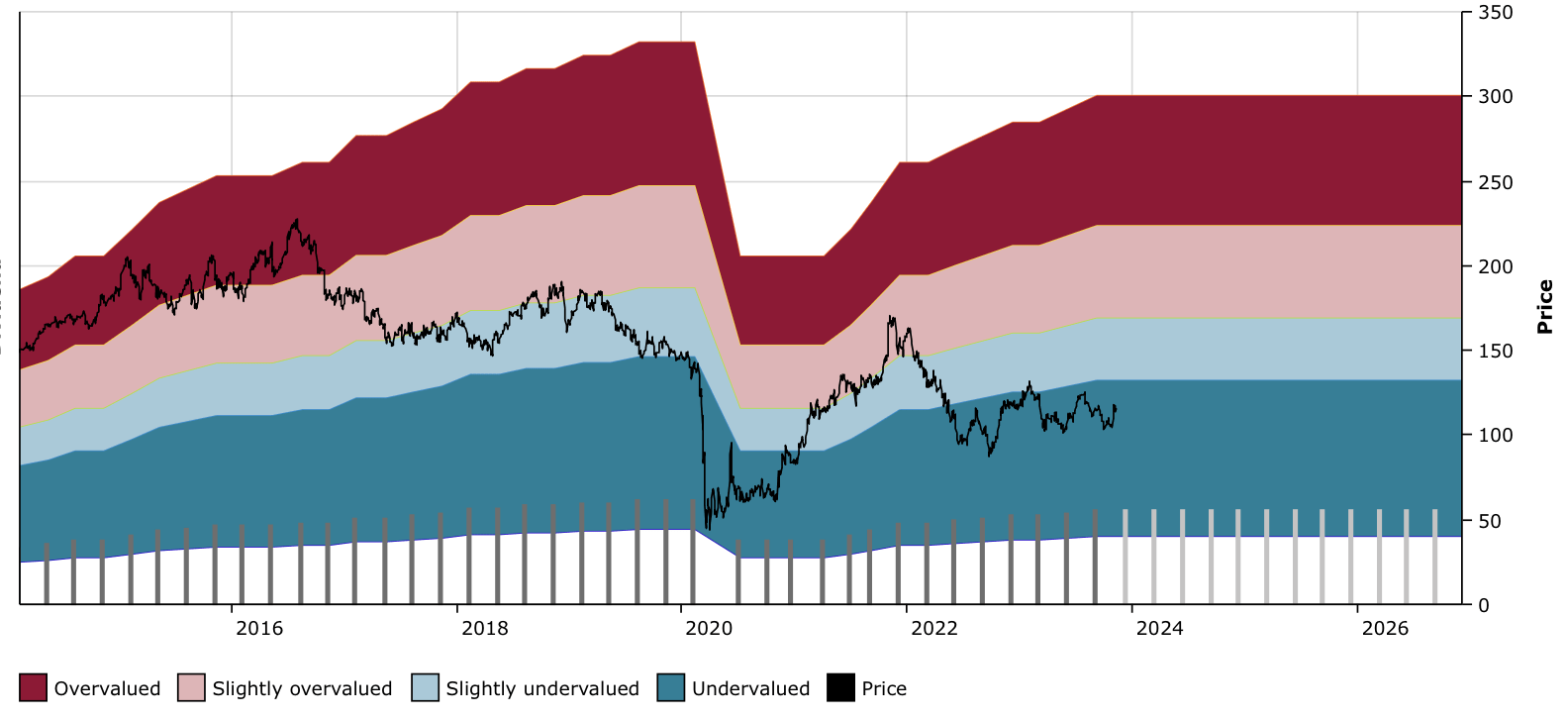

SPG DFT Chart (Dividend Freedom Tribe)

{kind=link}

When looking at the results from SPG, what we see is a clear superior retail REIT with a fantastic balance sheet , good payout ratios, and growing its operations and dividend as a consequence.

The dividend was reset during the pandemic, which was unfortunate but did vastly improve the payout ratio and gave us an opportunity to get in at attractive yields.

The 5.9% yield still seems rather high when we consider that

-

Domestic property NOI increased 4.2% year-over-year for the quarter and 3.8% for the first nine months.

-

The fourth-quarter dividend of $1.90 per share was announced, representing a year-over-year increase of 5.6%.

-

Full-year 2023 guidance was increased from $11.85-$11.95 to $12.15-$12.25 per share, an increase of $0.30 at the midpoint.

Even with a slight interest rate hit continuing in 2024, CEO David Simon still sees NOI growing at 3%.

The FFO payout ratio is about 70-75% which is reasonable, and the dividend is now just $0.2 away from returning to its pre-pandemic level.

I believe we'll continue to see 5% dividend growth until we return to that level, and 3% growth thereafter, which aligns with reasonable profitability increases for SPG.

Like Simon says, when you zoom out and look long term, they have outpaced the peer group, by focusing on quality, maintaining balance sheet superiority, and exerting expertise in their domain:

Balance sheet and quality of operations is a two-way street. It's both. As we look at retailers, we assess that. They certainly assess us. And I think that gives us an advantage that we've worked very hard, as you know, to achieve and, I mean, how do I say this? I mean, we've really outpaced our peer group dramatically in any measure you want, growth, earnings, dividend, quality of operations, scale, balance sheet, the -- I know we all focus quarter to quarter and this and that, but if you take a step back and you go, what do you got going for you? And again, we don't -- this sounds a little braggadocious. I don't want it to, but I mean, we've really outpaced, if you look over the last 10 -- 5, 10, 15, 20, 25 years, you know, we've dramatically outpaced our peer group.

The latest 5% dividend increase was satisfactory, and SPG remains a good quality high-yielding REIT to add to dividend portfolios.

Conclusion

All three of these stocks are run by competent management teams, and are trading at prices which support a healthy dividend yield relative to the dividend growth potential, which makes them great dividend buys.

For further details see:

Buy Alert: 3 Top Retail Dividend Growth Stocks For The Santa Rally