APO - Buy The Dip: 2 REITs Getting Way Too Cheap

2023-08-10 08:05:00 ET

Summary

- REITs have crashed over the past year.

- Some of the most sensitive to interest rates offer the best opportunities.

- We present two of our favorite opportunities.

Interest rates are up...

... and real estate investment trusts, or REITs, are down.

This has been the story of the past one-and-a-half years for REITs.

Whenever interest rates go up, REITs sell off almost mechanically as if they were going to face severe and immediate pressure as a result of it.

Note that this is the average of the REIT (VNQ) sector, and so you can imagine that those REITs that are more heavily leveraged and/or own interest rate-sensitive assets must have dropped even more.

Quite a few of them are down 50, 60, or even 70%!

They are, of course, riskier, and so a steeper drop is certainly warranted. However, if, like me, you think that interest rates are headed to lower levels, then this is a fantastic opportunity.

It is important to remember that interest rates only surged to stop the high inflation. But this is now already happening and, therefore, I think that steep interest rate cuts will soon follow. This is precisely what has happened every single time over the past 40 years. Periods of rising rates have been followed by rapid interest rate cuts once the economy had cooled down:

{kind=link}

As interest rates again return to lower levels, some of these REITs could present >100% upside potential in a future recovery as the primary concern of the market is removed.

Below I highlight two of my top picks among such higher risk / higher (potential) reward plays:

Safehold Inc. ( SAFE )

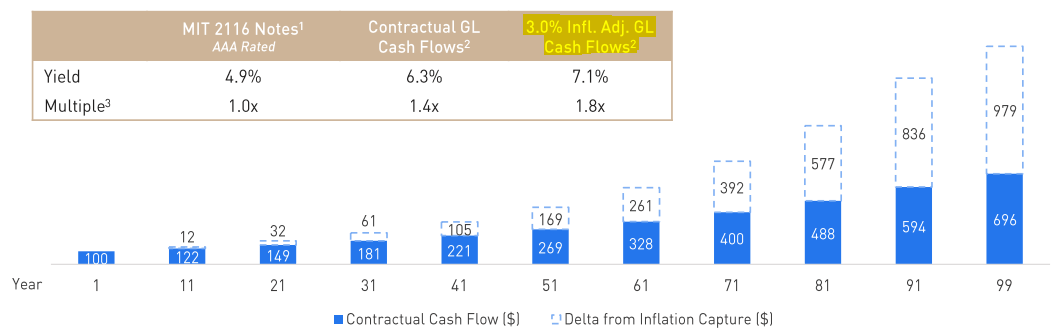

SAFE is arguably the most sensitive to interest rates of all REITs because it owns ground leases that have an initial lease term of 99 years with capped annual rent hikes.

A ground lease grants the use of a parcel of land to a tenant, very often for many decades, in exchange for rent payments, and at the end of the lease, the land and all structures upon it revert to the landowner at no cost. Moreover, under a ground lease, a lease default would also cause the control of the land and the ownership of all structures upon it to return immediately to the landowner. As such, they are very safe investments and defaults are extremely rare. This video will give you a good overview of ground leases:

But since they are so safe, their cap rates are also low and rent escalations are limited, making them more similar to very-long-duration bonds.

Therefore, the higher inflation and rising interest rates have a significant negative impact on the fair value of its ground leases and it explains why its valuation has collapsed.

But the flip side of things is that lower inflation and declining interest rates would have the exact opposite effect and we don't need interest rates to return to zero for SAFE to enjoy very substantial upside from here. Even if its share price rose by 50%, it would still trade at less than half of where it was back in early 2022 and that doesn't even account for the fact that its cash flow has grown since then, it has internalized its management, and improved its credit rating.

I think that when we look back 5 years from now, we will realize that the period of high inflation and interest rates in 2022/2023 was just a temporary hiccup in SAFE's growth path.

It caused its external growth to temporarily slow down because it couldn't access much new capital at a reasonable cost, but on the other hand, it will now also result in an acceleration in its organic growth going forward as CPI-based lookbacks will eventually kick in.

Typically, SAFE's leases include annual fixed bumps of 2%, but there are also periodic CPI-based lookbacks that provide inflation capture, typically up to 3-3.5% on a compounded basis.

This means that if the CPI exceeds 2% over a lookback period of 10 years as an example, then SAFE's rents will be adjusted upward in the future.

{kind=link}

Put differently, when we look back 5 years from now, I think that we will see 2022/2023 as a case of "short-term pain for long-term gain." It halted growth for a bit but will accelerate it in the following period.

Yet, its share price remains heavily discounted and this is perhaps why the company's insiders have been buying shares in recent months:

{kind=link}

For this reason, we think that SAFE is the king of all bets on lower inflation.

Just to return to half of its all-time highs, it would need to see its share price rise by 100% from here, and to return to its previous highs, it would need to rise by 300% from here.

The only thing holding it back is the fear of high interest rates.

DIC Corporation (DIC / DDCCF )

We recently also made a small addition to DIC, which is one of our favorite opportunities in Germany.

It owns a vast portfolio of industrial and office properties that generate steady cash flow from long-term leases and in addition to that, it also has a rapidly-growing asset management business that generates growing fee income.

DIC Asset

But here's the main reason for buying it today:

Its shares have crashed and are now priced at an 80% discount to their NAV, or put differently, just 20 cents on the dollar:

Why is it so heavily discounted by the market?

The answer is leverage.

The company has a 57% LTV and it is making the market very nervous because DIC needs to sell off some assets to deleverage.

Admittedly, DIC is in a risky position, but we remain optimistic because:

- 1) We talked to the management in early 2023 and they felt confident that they could structure JVs such as the one announced by VNA to raise equity and pay off debt. You can read our interview by clicking here.

- 2) DIC has an asset management business with relationships with 150+ institutional investors and about 40% of its portfolio is invested in highly desirable industrial properties with growing rents and near 100% occupancy. DIC could sell some of its assets at a slight discount if needed and make up for it by earning fees for managing the investment.

- 3) Blackstone just recently announced that it was going to buy out a European Industrial REIT at a share price near its net asset value for close to €1 billion. Moreover, Vonovia (VNA / VONOY ), the biggest landlord in Germany, recently announced 2 big transactions with CBRE ( CBRE ) and Apollo ( APO ) to sell assets near its NAV and it is in a similar situation.

- 4) They recently restructured their bridge loan in a way that instead of it all maturing on January 31st, 2024, it will now have half of it (€200m) mature on July 31st, 2024, and the other half on July 31st, 2025. This gives them more headroom with dispositions.

- 5) They have most other major debt maturities now covered until 2026, leaving them ample time to be opportunistic with asset sales.

- 6) The management recently said the following: "We expect transaction activities to start normalizing by mid-year. This year, the company's focus is on optimizing its financial structure, an effort that is progressing according to schedule." commented Sonja Wärntges, CEO of DIC.

- 7) They have not yet cut or suspended their dividend, which is one more lever that they could pull to retain cash flow and pay off debt. I think that a dividend suspension is likely and this could be beneficial to the company as it would increase its chances of eventually recovering from here.

DIC Asset

So risks are high, but I remain optimistic that the company will avoid a worst-case scenario, which is what the market has been pricing lately.

The stock is currently offered at a 80% discount to its net asset value, which clearly tells you that the market fears that this is going to zero.

But if I am right and they manage to sell some assets to pay off debt, DIC could rapidly double or even triple from here as market conditions normalize.

The risk-to-reward is compelling for more aggressive investors.

Bottom Line

The last time REITs were so cheap was early into the pandemic when the average of the REIT sector crashed by about 50%.

We bought a lot of REITs back then and made a little fortune in the following year as REITs recovered.

We don't think that this time will be any different. This is why we are now accumulating a lot of REITs at these historically low valuations.

For further details see:

Buy The Dip: 2 REITs Getting Way Too Cheap