ZION - Buy Zions Bancorp. Think 5 Years Ahead Not Just Next Quarter

2023-10-23 09:38:18 ET

Summary

- Zions reported Q3 earnings per share of $1.13, only 3 cents short of expectations, but it caused a 16% decline in market cap.

- The banking industry is currently facing challenges to its interest income, credit costs, and capital flexibility, but I expect them to fade over the next few years.

- Zions' current valuation is the cheapest it has been in a decade, making it an attractive investment for long-term investors.

Zions (ZION) reported Q3 EPS of $1.13 last week, three cents short of Wall Street expectations. That $5 million earnings shortfall took 16%, or $850 million, off Zions' market cap over the next two days. If the market is rational, investors decided that the news behind that three-cents shortfall seriously lowered Zions' earnings over the long run. Because after all, the value of a stock is the present value of all future earnings, right?

Or maybe the reaction was simply irrational, a fear of the banking industry's tough operating environment at present.

I'm going with the second choice. Banks are currently getting battered by a confluence of events. But the odds are that these events will fade over the next few years, making Zions' current $30 price quite a bargain if you are taking into account the present value of all future earnings. So if you are an investor and not a trader, consider this stock.

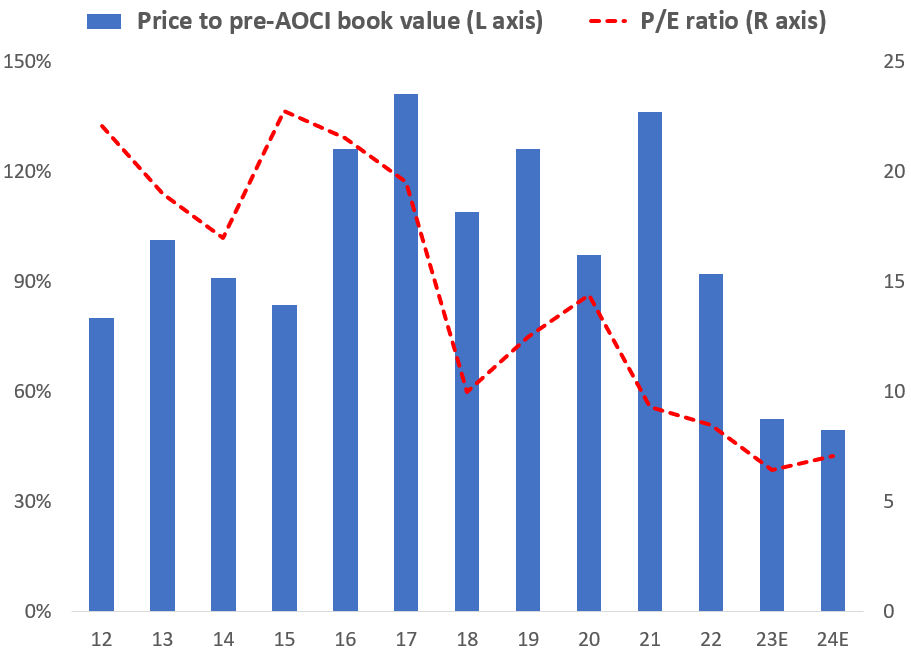

Zions' dirt-cheap valuation

Here is a history forecast of Zions' price-to-book value and P/E ratio:

{kind=link}

Note that I adjusted Zions' reported book value by adding back the $3 billion write-down of its securities portfolio. The reason is that Zions owns its $21 billion of fixed rate securities in order to hedge its non-interest-bearing deposits (0% cost), which currently total $27 billion. While Zions' book value marks-to-market the securities, it doesn't write up this very valuable asset.

That said, the chart shows that Zions' current valuation is by far its cheapest over the past decade. The stock price implies many, many years of bad news. Let's see if that dismal view makes sense, by reviewing these key risk areas for Zions:

- Interest rate risk

- Credit risk

- Capital risk

Interest rate risk part 1. Will interest rates rise forever?

It sure feels like it, doesn't it? But I offer three reasons why the Fed funds rate should be lower, and probably much lower, 5 years from now:

- The real Fed funds rate is already pretty high. The level of the Fed funds rate is best judged by comparing it to the inflation rate. The spread between the two is the "real" Fed funds rate. It is currently at 1.6%. That compares favorably to the median 1.1% real rate since 1954. And if the average economists' inflation forecast of 2.7% a year from now ( Philadelphia Fed ) is correct, the real Fed funds rate will widen to 2.6%. So it seems likely that the Fed is done, or nearly so.

- We can't afford the current interest rate levels. Five years from now federal government debt will exceed $40 trillion. And private sector debt won't be much below $50 trillion. Moving the cost of Treasury debt from its recent 2% average to 5% adds $1.2 trillion to the annual budget deficit. That is a crushing burden. Part of the Fed's unspoken mandate going forward is to limit the pain from our massive debt load.

- Businesses will address the labor shortage. The current near-record labor shortage is a major reason for today's high inflation rate. Ask GM about that. Or Delta. But technology is providing more and more tools to replace labor, from robots to AI to autonomous driving. Businesses will almost certainly adopt these tools as fast as they can to preserve their profit margins, which should ease or even eliminate the labor shortage.

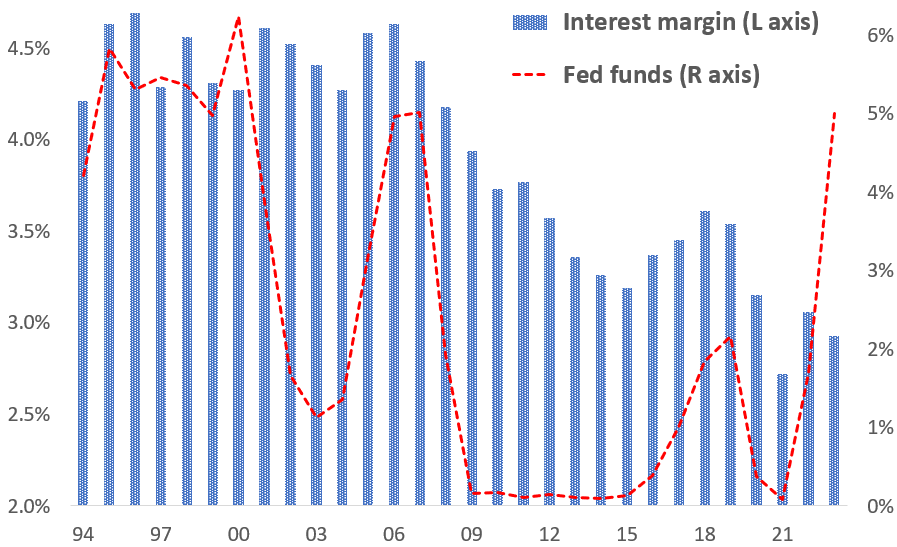

Interest rate risk part 2. Zions' interest margin is highly unlikely to drop sharply

To understand how Zions' interest margin moves, check out its history versus the fed funds rate:

{kind=link}

Zions' interest margin has done better over time with higher Fed funds than with lower Fed funds! Why? Because of the bank's non-interest-bearing deposits. By definition, they have zero cost. But the yields on the loans they fund rise as interest rates rise.

"But Gordon, Zions has lost a lot of those no-cost deposits." Yes, they did; they lost $12 billion, or 32% of them over the last year. But the anomaly is not this past Q3, but the year-ago Q3 when deposit yields were near zero and leaving money in checking accounts didn't cost us much. There is a natural trade-off between the percent of deposits that are no-cost and the spread benefit of those no-cost deposits, as this table shows:

Zions financial reports

So, yes, Zions' no-cost deposits are shrinking. But the benefit to earnings of those deposits is growing. Net/net, Zions had this to say in its Q3 earnings transcript : " Our outlook for net interest income in the third quarter of 2024 is stable relative to the third quarter of 2023."

Credit risk. Get over those office loans

Yes, the remote work phenomenon is emptying office buildings and creating bad loans. Yes, Zions announced that two office loans went non-performing during Q3. But:

- The two loans generated a whopping $3 million write-off, or 2 cents a share.

- Only 4% of Zions' loan portfolio is office loans. If Zions has to charge off 10% of that total loan portfolio over time, that is $1 a share. The stock dropped $6 late last week.

- The office loans have average loan-to-value ratios of less than 60%. And 70% are in suburban locations, where commutes are shorter and going to the office is less burdensome.

The rest of Zions' loan portfolio is pretty standard. Yes, Zions will get hurt in a recession, but so will the rest of Corporate America.

Capital risk. Will the government trap more capital?

In the four years from 2019-2022, Zions returned all of its earnings to shareholders as dividends or share repurchases. Over $20 per share. But this year, while maintaining its $1.64 dividend - a 5.5% yield! - Zions had to stop buying back stock to build its regulatory capital in response to regulators' nervousness after the Silicon Valley/First Republic bank failures. And it will have to build its capital ratio for the foreseeable future due to potential increased regulatory requirements.

But will Zions have to limit its returns to shareholders forever? No. If regulators increase bank capital requirements they do increase taxpayer protections. But they also limit banks' ability to fund spending and GDP growth. That's obviously a political risk.

My guess is that Zions' share repurchases will resume by 2025. And when they do return, returns to shareholders will approach or exceed 10% on today's $30 stock price.

The bottom line - At $30, Zions is a terrific value

Interest rate wiggles will drive Monday's trading. But investors should be more interested in what Zions looks like 5 years from now:

- Book value should be at least $60.

- EPS should be north of $5 and more likely north of $6.

- The dividend should be above $2 a share.

For further details see:

Buy Zions Bancorp. Think 5 Years Ahead, Not Just Next Quarter