BZFD - BuzzFeed Has Lost Its Buzz

Summary

- BuzzFeed's stock price has declined 84% in just nine months.

- Since coming into the spotlight between 2011 and 2015, BuzzFeed has steadily lost relevance over time.

- Even at 0.5x sales, BuzzFeed is not an attractive investment as future prospects remain weak.

BuzzFeed's ( BZFD ) stock price has experienced a free fall since its SPAC in November 2021 where it traded at ~$10 a share. Today, BuzzFeed trades at just $1.50.

Top-line growth is dwindling while net losses are widening - operating costs are rising more aggressively than sales. Even at current prices, I do not see BuzzFeed as an attractive investment. Future prospects look dim; new content isn't resonating with consumers, and the company is battling against a poor advertising backdrop.

BuzzFeed may appear cheap at 0.5x FY22 sales, but don't be fooled - margins are moving in the wrong direction, with little evidence that this will change as the company unsuccessfully tries to turn the ship around. Sell.

Why has BuzzFeed stock fallen?

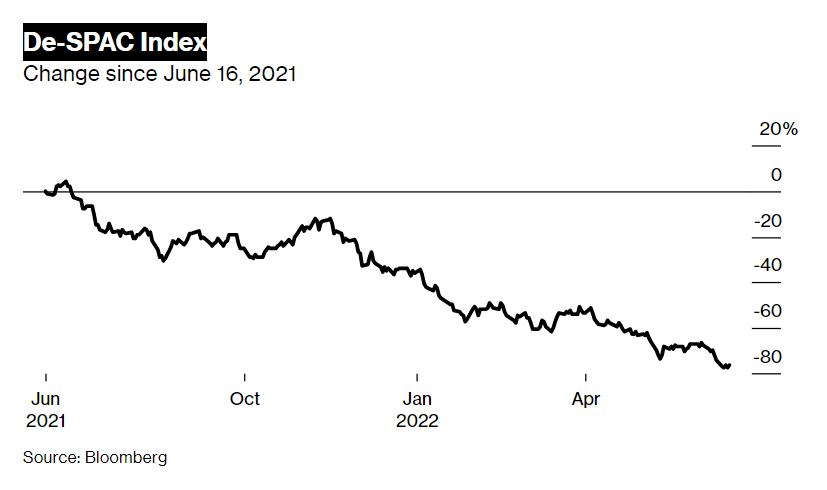

BuzzFeed's performance has fallen victim to the same fate as many other 2021 SPACs due to an over-optimistic (to put it lightly) initial valuation. Take a look at Bloomberg's De-SPAC index as a quick measure of what I mean by this SPAC 'fate'.

{kind=link}

It, therefore, isn't too surprising to see a significant slowdown in the SPAC activity in 2022; the number of SPAC IPOs dropped more than 80% in the first half of 2022 compared to the prior year.

For BuzzFeed's pre-IPO shareholders, it appears they got the merger away at a good time (before the big crumble). But even under more accommodating SPAC conditions, BuzzFeed had little demand from investors. When the company merged with blank-check company 890 Avenue Partners Inc, 94% of the money raised by the SPAC was withdrawn as investors started to rotate away from SPACs, leaving BuzzFeed with just $16M.

This general consensus move foreboded what was to come, just nine months later and the BuzzFeed stock price is down 84%. Like the initial valuation, BuzzFeed's guidance was likely aggressive. The firm expected a revenue CAGR of 25% annually through 2024. Just a year later and this expectation has been revised, the market now expects BuzzFeed to achieve a CAGR of just 10% through '24. This slower growth has come despite a stark increase in marketing spend. In Q2, BuzzFeed reported 20% revenue growth while sales and marketing expenses increased 61%. This was only slightly higher than the overall jump in total costs (47%). These higher costs drove BuzzFeed to a net loss of $23.7M.

Loss of reader traction

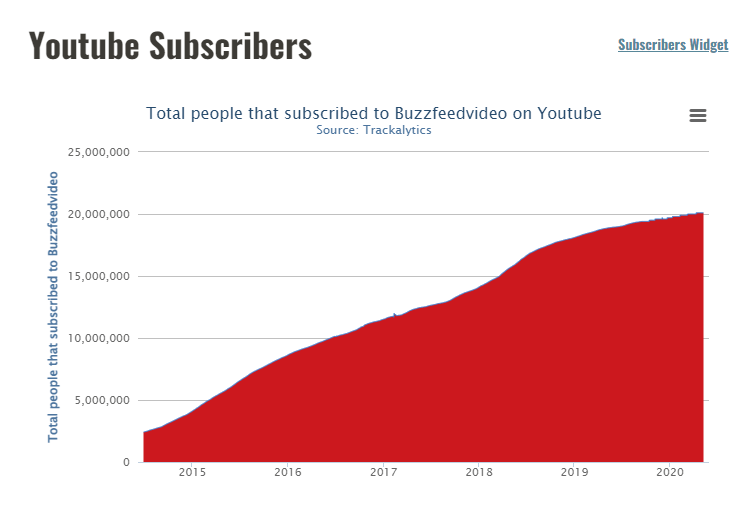

A key aspect of BuzzFeed's business is the YouTube channel, and the statistics on this account can provide a good insight into the overall performance and traction of BuzzFeed content. Purely looking at subscriber count, it's clear for a long period BuzzFeed experienced consistent exemplary channel growth.

{kind=link}

But there has been a notable slowdown in this growth since 2019. It appears the BuzzFeed channel is starting to reach maturity. 20 Million is a lot of subscribers, but it means very little without similar levels of engagement

{kind=link}

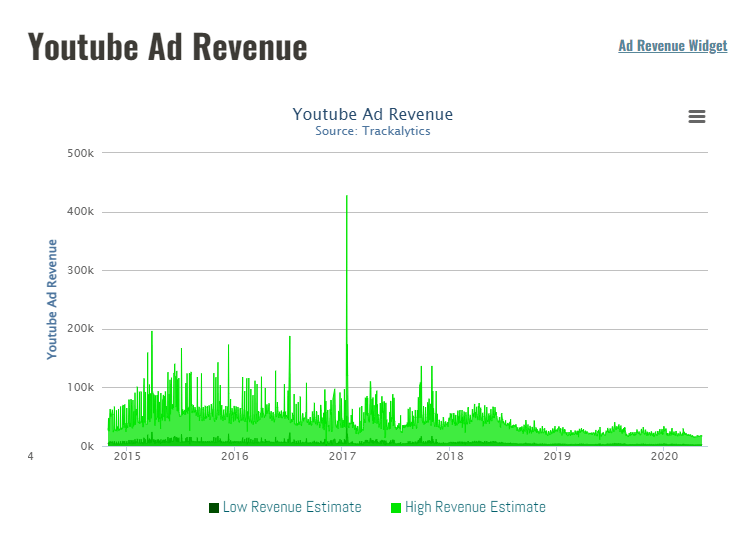

The above Trackalytics feature gives estimates of Ad revenue over time. The revenue estimates are very broad but do show a gradual decline in earnings since late 2018. Google trends paint a similar story.

{kind=link}

Of course, these stats aren't a complete reflection of BuzzFeed's performance but they do provide a good overview of the brand's potentially diminishing relevance.

Is BuzzFeed undervalued now?

The US and global economy are slowing down and that does not spell good news for BuzzFeed. Nearly half of Q2 revenue came from advertising, therefore weak guidance was expected against this poor backdrop (~6% growth expected in Q2 Y/Y).

BuzzFeed is expecting sequentially deeper losses in Q3. The company has guided for Adjusted EBITDA in the range of $5-10M. Investors should also strap in for greater net losses as stock-based compensation is expected to be between $3.5-$4.5M.

BuzzFeed had $68M cash on hand at the end of last quarter, which decreased by $6.35M from the quarter prior. This means the company is unlikely to completely burn through its cash any time soon, but it does have $150M in long-term debt which relates to the convertible note issued in June 2021. This note has an interest rate of 8.5%. This is due in 2026 and can be converted into common stock with an initial conversion price of $12.50 - making it very unlikely that it will be. BuzzFeed can meet the obligations under this note, but it does create a future roadblock if BuzzFeed is unable to become cash flow positive over the next few years. Operating cash flow was -$4.9M in Q2.

Considering this expensive debt, widening losses and an uncertain economic backdrop, even at 0.5x sales, I do not consider BuzzFeed undervalued at current prices.

The bottom line

BuzzFeed is facing considerable headwinds related to its advertising segment. A dangerous crossroads is fast approaching, sales and marketing investment is necessary to keep the brand pertinent in the media scene, but it would also be beneficial to adjust variable expenses to reduce losses in consideration of the headwinds. This is a difficult balancing act and I do not believe it's worth having exposure to BuzzFeed, Sell.

For further details see:

BuzzFeed Has Lost Its Buzz