BZFD - BuzzFeed: I Bought A Speculative Position

2023-07-03 07:49:37 ET

Summary

- BuzzFeed is now valued at $70.76 million, a far cry from its $1.7 billion valuation in 2015 and 2016.

- BZFD is laying off staff and shutting down its news unit in an attempt to turn its fortunes around.

- A gradual rightsizing of its operational footprint is supported by a cash position of $50 million and free cash outflows of $600,000 during its fiscal 2023 first quarter.

BuzzFeed's ( BZFD ) more than year-long selloff has overextended itself. The digital media company's price to trailing 12-month sales multiple at 0.17x presents a speculative entry point even against quarterly revenue in decline over its year-ago comp, a large total debt balance, and consistent net losses from operations. Common shares are currently swapping hands at the cheapest ever level since it went public. Indeed, it's likely trading at its cheapest-ever level since its founding in 2006 with its Series F and Series G funding rounds in 2015 and 2016 valuing it at $1.7 billion when its revenue was markedly lower. Hence, I've taken a small speculative position in the common shares with a view to holding for at least a year on the basis that the stock market appetite for loss-making companies will be greatly improved by a normalization of the current turbulent macroeconomic environment and that the management turnaround plan should be aggregated with this process.

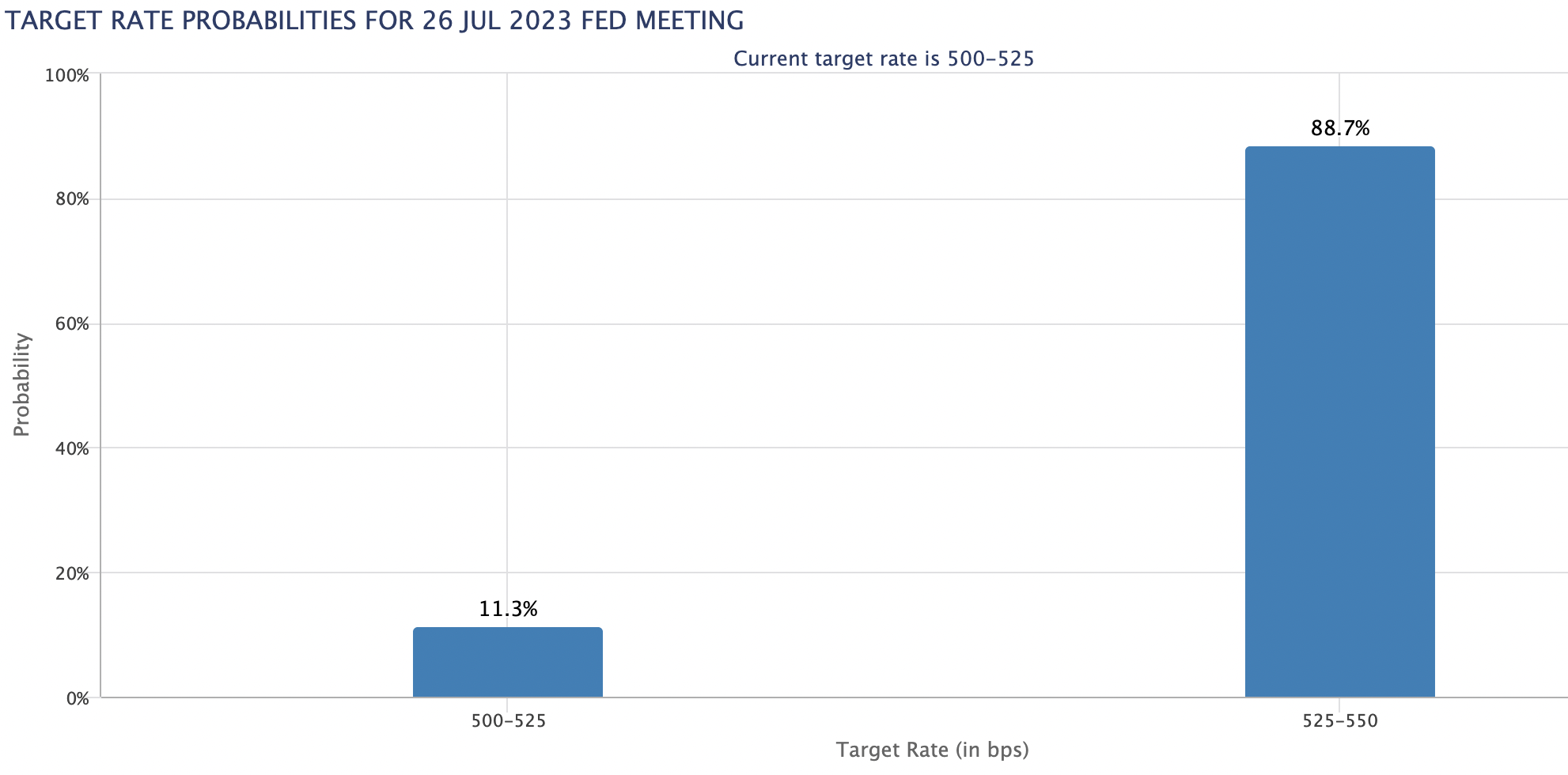

To be clear here, this is a trade that will be built on no more interest rate hikes this year and a potential cut in the first half of 2024. This is as BuzzFeed goes through major cost cuts to rightsize its operations and enhance profitability that's behind what it could be. However, it's important to flag that the Fed has openly stated they see themselves conducting more hikes in 2023 and the stock market is currently pricing in an 88.7% chance of a hike at the July 26th FOMC meeting, up from a 74.4% chance a week ago. However, as Powell has stated that the decision will be data dependent, headline inflation below market consensus of 3.6% at the upcoming July 12th inflation update will likely drive a second consecutive pause.

{kind=link}

The company only went public a few weeks before Christmas in 2021 via a merger with a special purpose acquisition company. Had this happened a year earlier and BuzzFeed would have seen its valuation skyrocket on the back of the unfettered euphoria that defined the brief pandemic period before what would be ten consecutive interest rate hikes. My bullish thesis is that whilst we are a long way away from the zeitgeist that defined the pre-rate hike period, the June FOMC rate pause could come to represent a watershed moment for long-suffering bulls.

Risks

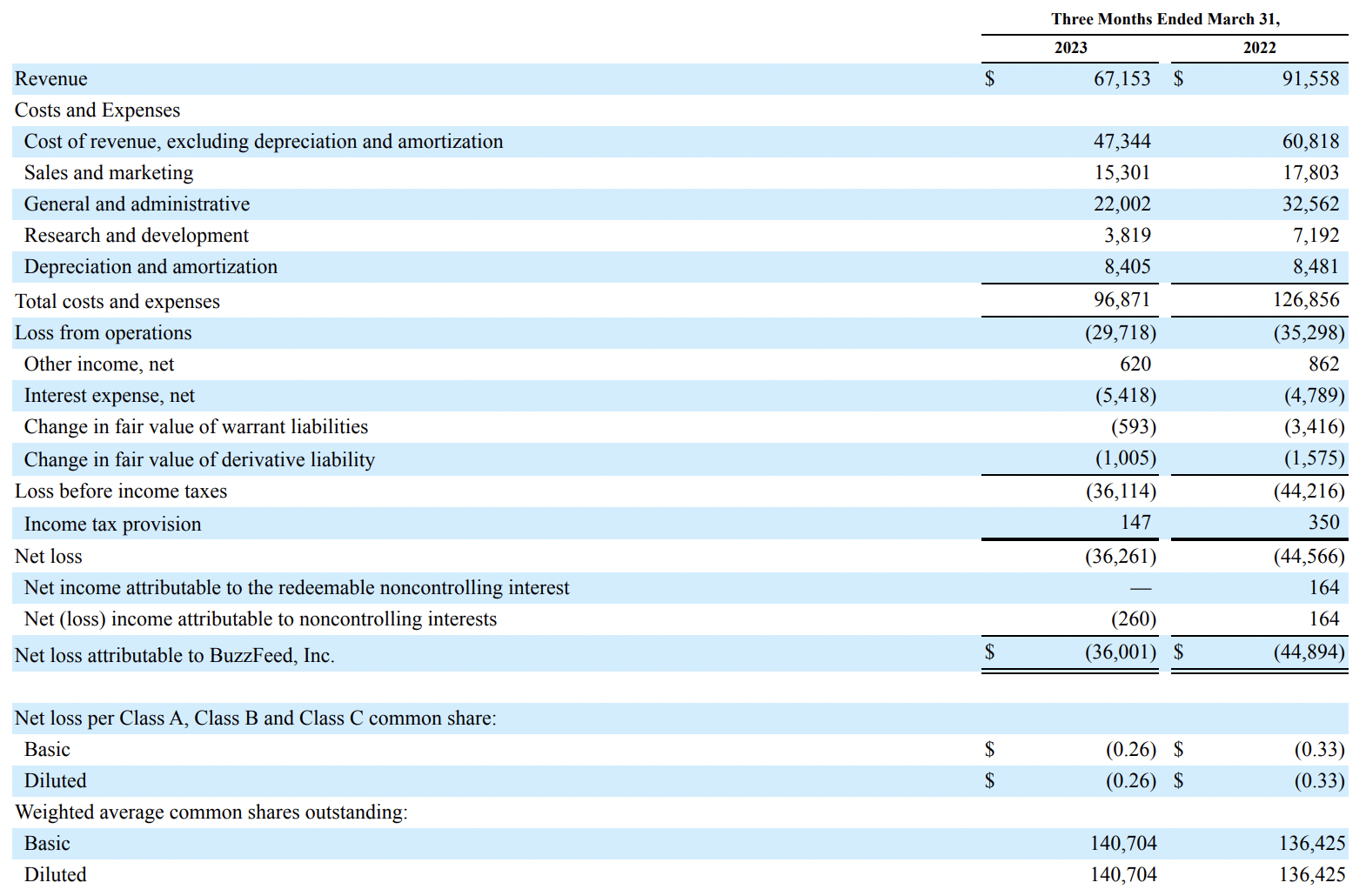

There are two core reasons to still avoid BuzzFeed. Firstly, the company recorded fiscal 2023 first-quarter revenue of $67.2 million , a 27% year-over-year decline but still a beat by $2.93 million on consensus estimates. There was a broad decline across all its three revenue segments with advertising revenues falling to $34.2 million from $48.6 million in the year-ago period. Why is this happening? US companies have been pulling back on ad spending against interest rate hikes and the rising specter of a recession. April marked the tenth straight month of ad spending declining . Further, companies could further cut back on their ad spend if the US economy deteriorates with PIMCO putting out some comments in early July that they expect a harder landing of the global economy that current market expectations.

Another reason to avoid the commons is BuzzFeed's outsized net losses. The company lost $36 million during its first quarter, down from $44.8 million in the year-ago comp but still forming 54% of revenue and 40% of its market cap. Bears, who form the 6.5% short interest, would be right to state that the company on a trailing-12-month basis as of the end of its first quarter lost the equivalent of 210% of its market cap. The trendline for losses is also going in the wrong direction.

BuzzFeed's total debt as of the end of the quarter stood at $229.2 million driving interest expenses to jump $630,000 from the year-ago period to $5.42 million. Hence, from a retrospective fundamental basis, BuzzFeed offers a few reasons to cheer. This is a loss-making company, built around selling ads, that is now seeing its revenue decline as net losses climb. Critically, there will be no pathway to valuation expansion if net losses continue to remain outsized even against better market appetite for previously 'risk-off' tickers. The company is also currently trading below Nasdaq's minimum listing requirement to open up a further risk of being moved to over-the-counter trading. This would require a reverse stock split as a remedy if the commons remain below the $1 listing minimum through 2023.

The Turnaround

BuzzFeed Fiscal 2023 First Quarter Form 10-Q

{kind=link}

BuzzFeed is shutting down its news division, has laid off 12 % of its workforce, and managed to reduce its sales and marketing expenses by $2.5 million year-over-year during its first quarter. The company also reduced R&D expenses to $3.82 million from $7.19 million with G&A expenses falling by $10.56 million year-over-year to $22 million. Management was upbeat on the potential of the company realizing further cost cuts during their first-quarter earnings call . They also provided a broad statement on their commitment to reaching and generating strong cash flows over time.

The company has a large Gen Z and Millennial audience base with millions of social media followers across its brands from Tasty , Hot Ones, and Complex. These are important intangible assets that will continue to be leveraged for revenue as US ad spending recovers. I'm not a fan of the AI content creation strategy as it seems as though management has jumped on a largely unproven technology to generate buzz. It harks back to the days when the metaverse was the lingua of stock market euphoria. The potential of this policy shift by BuzzFeed from an investment perspective remains a wait-and-see against what are bullish comments by management on the potential of AI in their earnings call.

This will be a highly speculative play, albeit one made less risky by a cash and equivalent position of $50 million as of the end of the first quarter. This is set against cash burn from operations of just $200,000 and a cash runway of more that's significant against first-quarter free cash outflow of $600,000. However, the trailing 12-month free cash flow of $12.7 million implies a lower cash runway if the company fails to control future costs. The company will likely not require external capital until fiscal 2025 against this. Critically, a failure to reduce cash burn would materially slim the time required until BuzzFeed does require what would be extremely dilutive capital against their current stock price with debt already significant. I think the company has time to fully realize its turnaround and I think the valuation here, especially against what looks set to be a more engaging market sentiment, makes for a decent medium-term but extremely speculative play.

For further details see:

BuzzFeed: I Bought A Speculative Position