UDR - Camden Property Trust: A High-Quality REIT On Sale That You Should Consider Going Into 2024

2023-12-21 14:00:00 ET

Summary

- Camden Property Trust is a beaten-down REIT trading at attractive valuations, making it a good investment opportunity.

- The company owns Class A properties in fast-growing markets and continues to grow its portfolio with acquisitions.

- Despite a drop in occupancy ratings, Camden Property Trust has a strong balance sheet, a growing FFO/AFFO, and a safe and increasing dividend.

- As rates decline in 2024, I expect CPT's share price to increase and have a price target of $117.

Introduction

Those who follow me here on SA have probably figured out that REITs are some of my favorite investments. And in 2023 I've come to love them even more. One reason is that many of them have been beaten down by the macro environment and now are trading at very attractive valuations. There is nothing I enjoy more than catching items/stocks that I consider to be high-quality trading at a discount. I mean, who doesn't love a good sale? I last covered Camden Property Trust ( CPT ) this past summer, where I said the stock was undervalued and then was a good time to buy. Well, the apartment REIT is an even better buy now, having declined an additional 7% since then. In this article, I get into why this REIT is one you should consider going into 2024.

Brief Overview

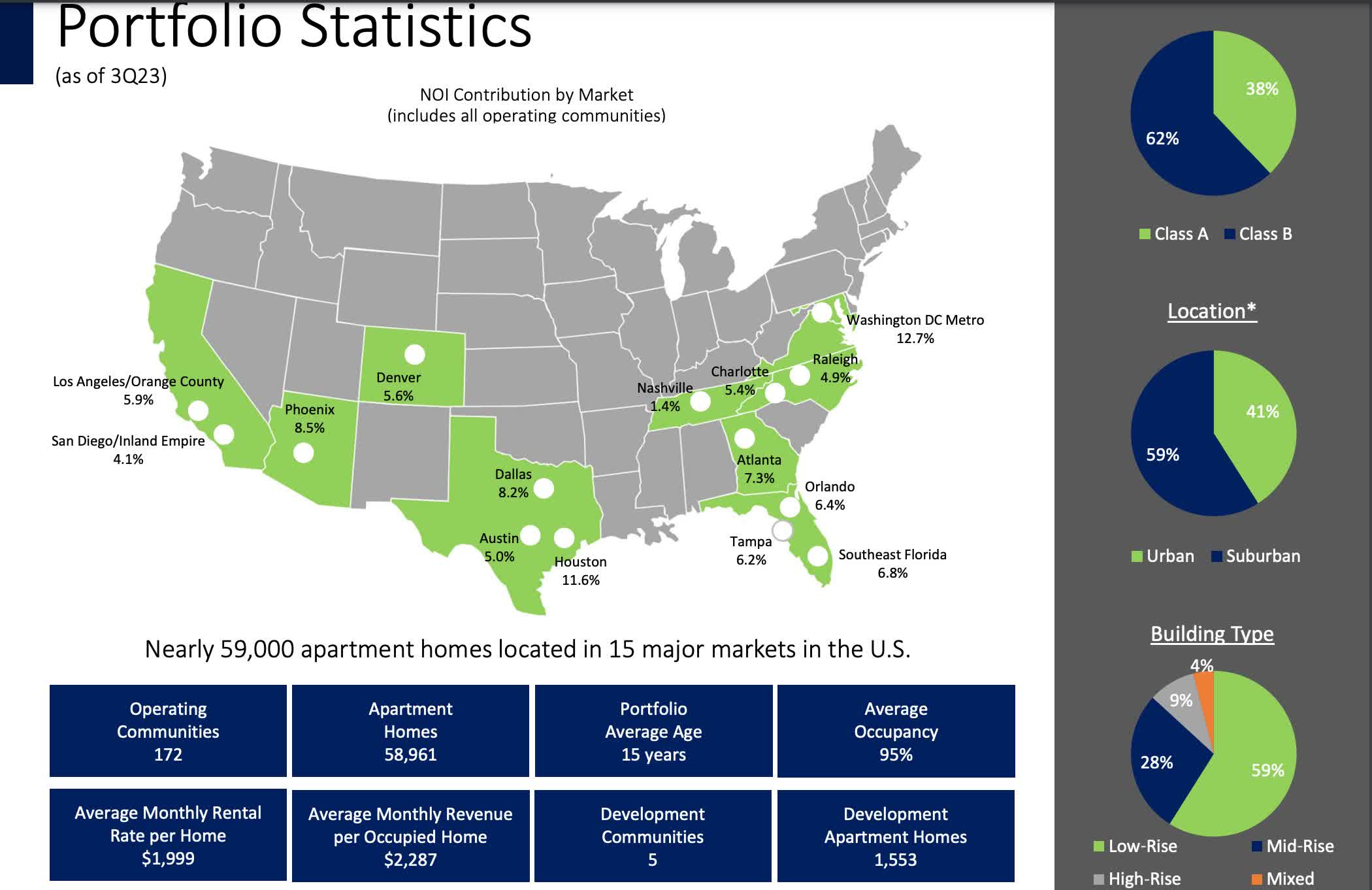

For those who are not familiar with Camden Property Trust, they are an apartment REIT who focuses on mostly Class A & B properties mostly in the Sun Belt region. They also are members of the S&P 500 and have been public since 1993. Additionally, they operate 172 properties comprising roughly 59,000 units in 15 markets. Some of these include fast-growing cities like Houston, Austin, Atlanta, and Charlotte.

{kind=link}

Price Decline

You can see in the chart below, CPT's price has declined further since my last article published on August 25th of this year. Since then, the REIT has posted some solid Q3 earnings back in October. Both FFO of $1.73 and revenue of $390.78 million were in-line with analysts' estimates. This was an increase of $0.23 from Q2. Revenue grew slightly from $385.5 million as well. Some solid numbers, especially considering the macro environment. So, why has the price continued to decline?

Well, one reason may be because the stock was downgraded back in October because of their Sun Belt exposure, a confluence of rising rates, and pandemic-fostered bad debt according to some analysts. But with interest rates expected to decline next year, I think the fears are overblown. It also didn't help that September & October are historically some of the worst months for the market.

And now that rate hikes are seemingly behind us, 2024 is looking positive, especially for REITs. And I think investors should take advantage of the suppressed prices before share prices rise. Management now expects FFO for Q4 to be in a range of $1.70-$1.74. That's a growth of 3.6% if FFO comes in at the mid-point of $1.72. This would also represent a slight decline from the $1.74 in Q4 of 2022. Like I previously mentioned, 2023 has been a very challenging for a lot of companies, especially for REITs. I also discuss later in the article another reason FFO could have declined year-over-year.

And although they may continue in the coming months, I expect them to subside in the foreseeable future as rates continue to decline. As an investor, I typically have at least a 3-to-5-year window for my investments/holdings. Of course, this is unless the fundamentals of the business change. But that's why it's important to not only have a longer outlook, but to select quality companies to hold for the long-term. And Camden Property Trust fits the bill.

Growth Outlook

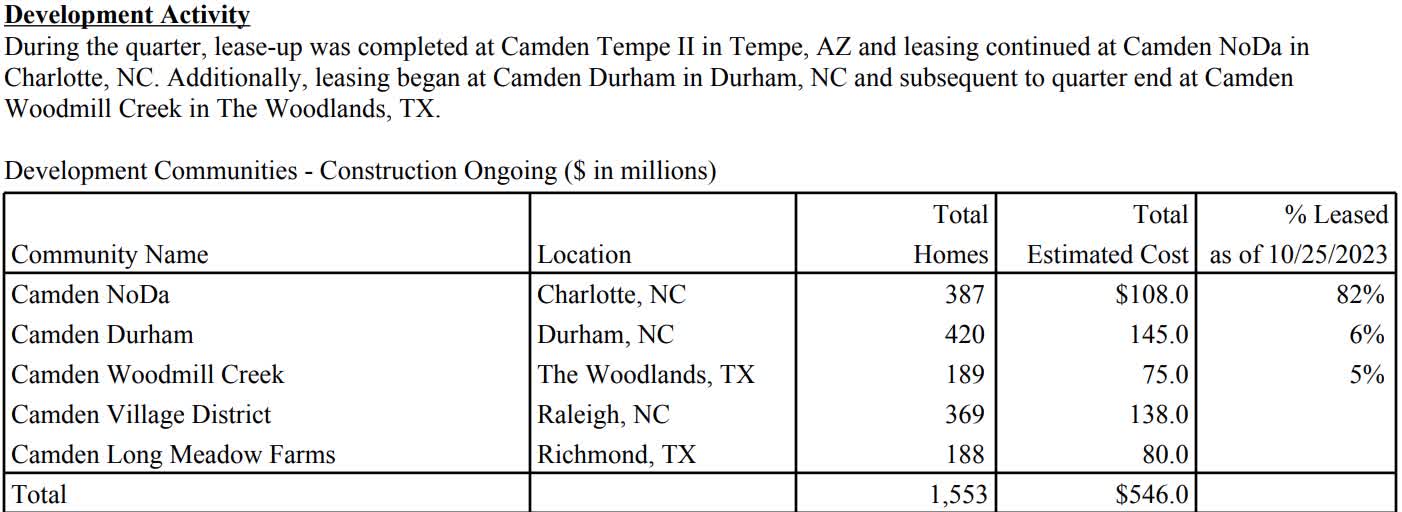

Although CPT owns Class A & B properties in attractive markets, the company continues to grow their portfolio. And these are strategically located in fast-growing places like Charlotte, Raleigh, and some cities in Texas. During their Q3 earnings call, management addressed that fundamentals for the business were good overall and that they were taking the challenges and opportunities together.

{kind=link}

On the call, their CEO stated:

On the demand side, job growth remains robust, U.S. consumer demographics continue to be supportive for apartment demand, the share of 25-to-34-year-olds is stable, the share of 34-to-48-year-olds is growing, and they have a high propensity to rent, given the record high costs of buying a home. The long-term trend to in-migration to our markets continues.

Something I think will continue to affect CPT positively for the foreseeable future, surging home prices. Times are changing and consumers are looking for value. And with homes at steep prices, this along with high mortgage rates will force them elsewhere like moving into apartments. There are also other alternatives, such as the RV life, which I am considering myself. Lower rates could potentially spur an increase in home sales activity again, but I think it will be some time before consumers are looking in that direction again. And according to Bank rate, home prices are expected to rise another 3% to 4% next year.

Solid Dividend Growth

Despite the dividend cut during the Great Financial Crisis, CPT has a pretty good dividend record. And although they don't have a long streak of increases because of COVID, their uninterrupted streak is impressive. Since coming out of the pandemic, the REIT has raised its dividend at a pretty rapid pace, increasing it from $0.83 to $1.00 currently. And these increases are well-supported by a conservative payout ratio.

With full-year FFO guidance expected to be in the range of $6.83 - $6.93, even if it comes in on the lower range of $6.83 this would still give them a very safe payout ratio of less than 59%. With a ratio this low, the REIT has plenty of room for additional increases, which I expect them to continue to do. So, investors get paid a safely-covered dividend while they wait for the price to recover, which I expect sometime next year. Furthermore, core AFFO & FFO in the first nine months of 2023 grew by 6.6% and 6.5% respectively.

A Rated Balance Sheet

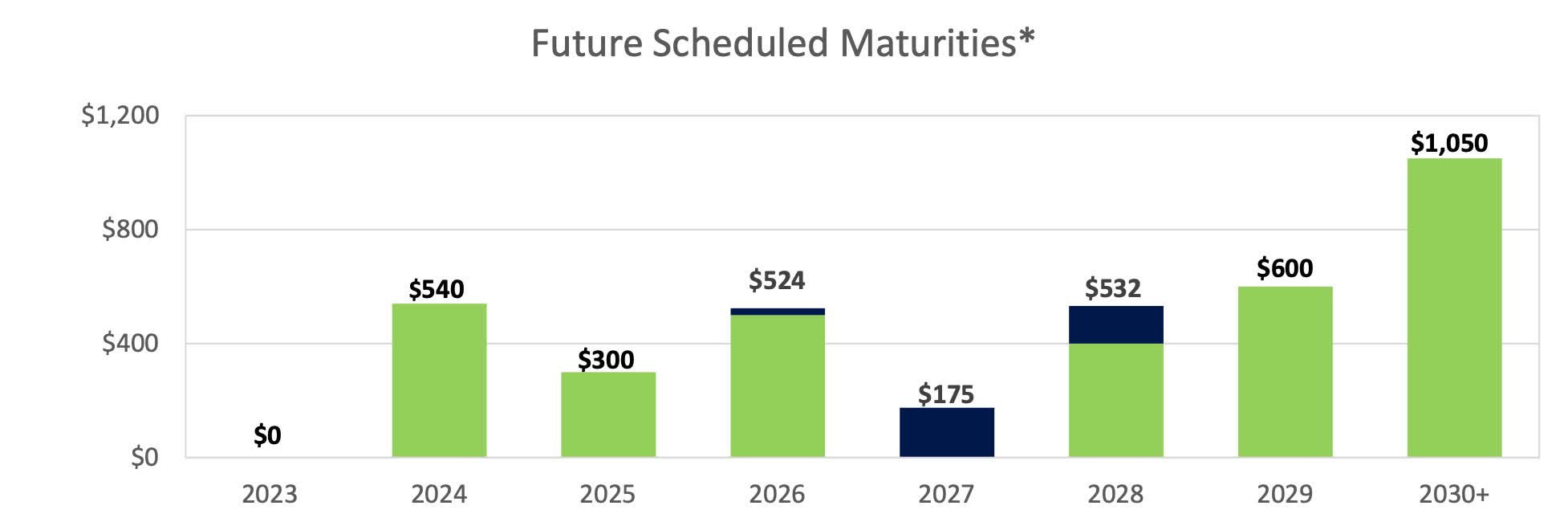

Camden Property Trust is also one of the few A rated REITs. They also have a very low net-debt-to-annualized adjusted EBITDA of 4.1x and a total fixed charge coverage ratio of 5.9x. This is in comparison to peers Essex Property Trust ( ESS ) & UDR's ( UDR ) 5.6x and 5.5x respectively. Furthermore, their debt maturities are very manageable, with only $540 million maturing in 2024 and even less in 2025. All of this, a weighted average interest rate of 4.2%. Additionally, they had $1.5 billion in available liquidity under the $1.2 billion unsecured credit facility. So, the REIT is in a comfortable financial position with available liquidity and manageable maturities due in the coming years.

{kind=link}

Valuation

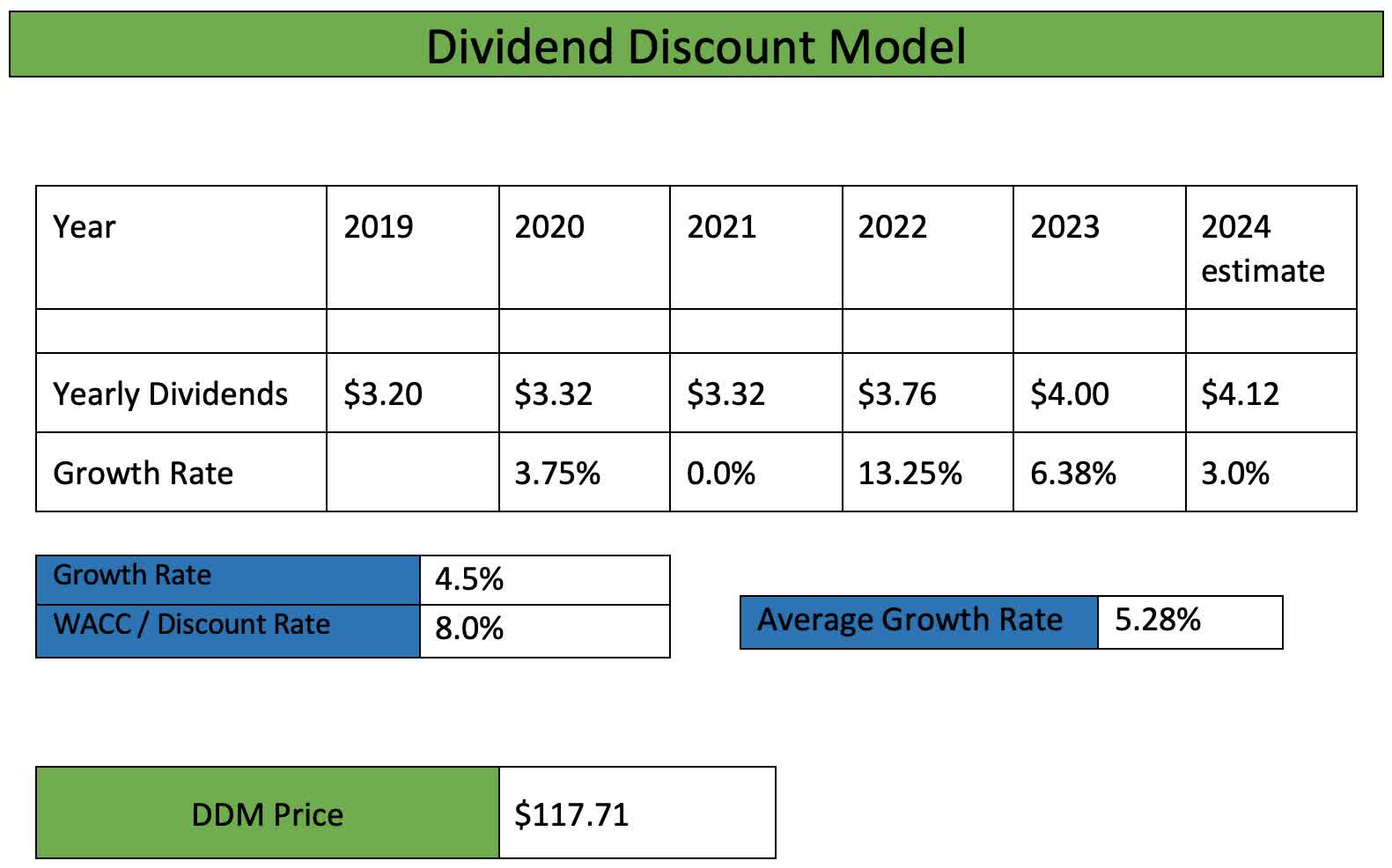

Seeing how much CPT has fallen in the last few months, it's no surprise the REIT is considered an attractive investment right now. At a price of $98.47 at the time of writing, I think it is a massive bargain. With a forward P/AFFO ratio of less than 17x, this is well-below their 5-year average of almost 23x. Using the Dividend Discount Model, I have a price target of roughly $117 for Camden Property Trust. So, investors get a well-covered dividend from an A rated REIT and also the potential for nearly 19% upside.

{kind=link}

Risks

Although I expect apartment REITs to benefit from higher home prices in 2024, a risk Camden Property Trust continues to face is a drop in their occupancy ratings. In Q3, the REIT reported a rating of 95.6%. This was a decrease from 96.6% in Q3 of last year, and management is projecting an average of 94.8% next quarter. And although same-property revenue growth was positive in most of their markets this year, this is something for investors to keep an eye on in the coming quarters. The REIT has proved to be resilient despite headwinds, but a continued drop in occupancy will likely affect rental revenues going forward. And this could cause further downward pressure on the share price.

Bottom Line

REITs have suffered in 2023 despite their strong balance sheets and growing FFO/AFFO. But with rates expected to decline in 2024 I suspect many will see their share prices move in a positive direction. Furthermore, REITs like CPT offer investors safely-covered, and growing dividends while they wait for prices to recover. That's why those with well-laddered debt maturities, strong credit ratings, and growing AFFO & revenues are important when dividend investing. While many are still fearful and have not yet rotated back into the sector from fixed-rate investments like CDs, I suspect this will change in the coming months. And those who are buying REITs will benefit with dividends and capital appreciation. Investors looking for slow & steady growth with potential double-digit upside, Camden Property Trust seems like a good fit.

For further details see:

Camden Property Trust: A High-Quality REIT On Sale That You Should Consider Going Into 2024