SPWR - Canadian Solar: Renewable Energy Growth Story Priced Like A Value Stock?

2023-09-12 07:30:00 ET

Summary

- Canadian Solar's stock dropped 17% after weak guidance for the remainder of the year, but the earnings report wasn't bad overall.

- The company is well-positioned for future growth in the renewable energy sector, with a potential market size for solar energy expected to grow at a compound annual growth rate of 15.7%.

- CSIQ is currently trading at historically low valuations, making it an attractive buying opportunity with the potential for significant returns.

- As such, we currently rate CSIQ as a buy.

Introduction:

Canadian Solar (CSIQ) plummeted after its most recent earnings report at the end of August. The stock dropped close to 17% in the following days due to weak guidance for the remainder of the year. The stock is currently down over 40% since the beginning of June, with the stock now trading at a similar price as in 2019. We believe this provides an interesting opportunity to start a position in CSIQ, as the earnings report wasn't bad at all.

In this article, we will take a look at CSIQ's prospects for the future and how they are currently valued. We will not only compare them to competitors, but we will also take a look at their valuation compared to big tech companies. In addition, we will explore if an investor like yourself should consider CSIQ as an alternative investment in the renewable energy space.

Canadian Solar: Exponential Growth and Renewable Energy Tailwinds

Founded in 2001, Canadian Solar is a leading designer and manufacturer of silicon ingots, wafers, cells, solar modules (solar panels), and custom-designed solar power applications. Canadian Solar has active buying customers in over 160 countries and subsidiaries in 23 countries & regions on six different continents, according to their website .

Important to note is that Canadian Solar holds a majority ownership stake of 72% (or 62% after its most recent IPO) in CSI Solar Ltd, which conducted its initial public offering on the Shanghai Stock Exchange in June 2023. CSI Solar encompasses solar module and battery storage manufacturing, as well as the provision of comprehensive system solutions, including inverters, solar system kits, and EPC services.

{kind=link}

Renewable Energy is one of the sectors expected to grow significantly in the upcoming decade as we earlier discussed in our copper piece. In addition, we discussed the renewable energy sector as a whole in the second part of our high-growth series . The potential market size for solar energy is vast, and as per Grand View Research, it is anticipated to sustain a remarkable compound annual growth rate of 15.7%. This presents a substantial advantage for Canadian Solar in the foreseeable future.

The chart below shows that CSIQ has seen explosive growth over the last decade, especially in the last 3 years. We believe CSIQ is in a great position to continue on this trajectory.

{kind=link}

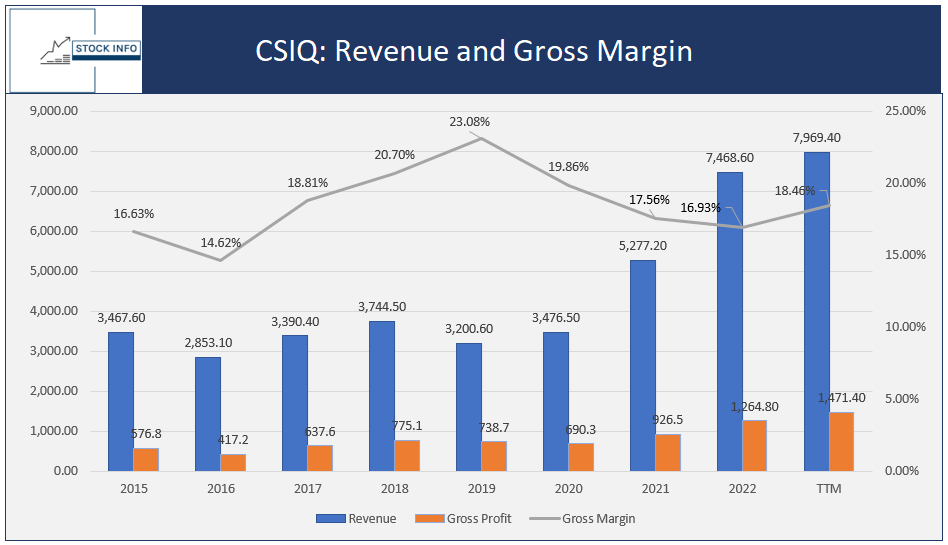

While the stock hasn't consistently been able to grow revenues and gross profit in the years prior to 2020, the company has been able to grow at a rapid pace over the last few years, as can be seen in the chart below.

{kind=link}

The stock is now trading at the same level as in 2019, while gross profit has doubled since then. Nonetheless, revenue and gross profit have been growing nicely.

Nonetheless, we have to admit that growth is certainly slowing, and the transition to renewable energy will be harder than expected. The infrastructure needed for renewable energy requires significant investment, and especially in times of economic hardship, these investments might be pushed further down the line. This explains the recent guidance cuts and weaker-than-expected results by pretty much all the companies within the solar energy space.

Renewable Energy and Its Current State

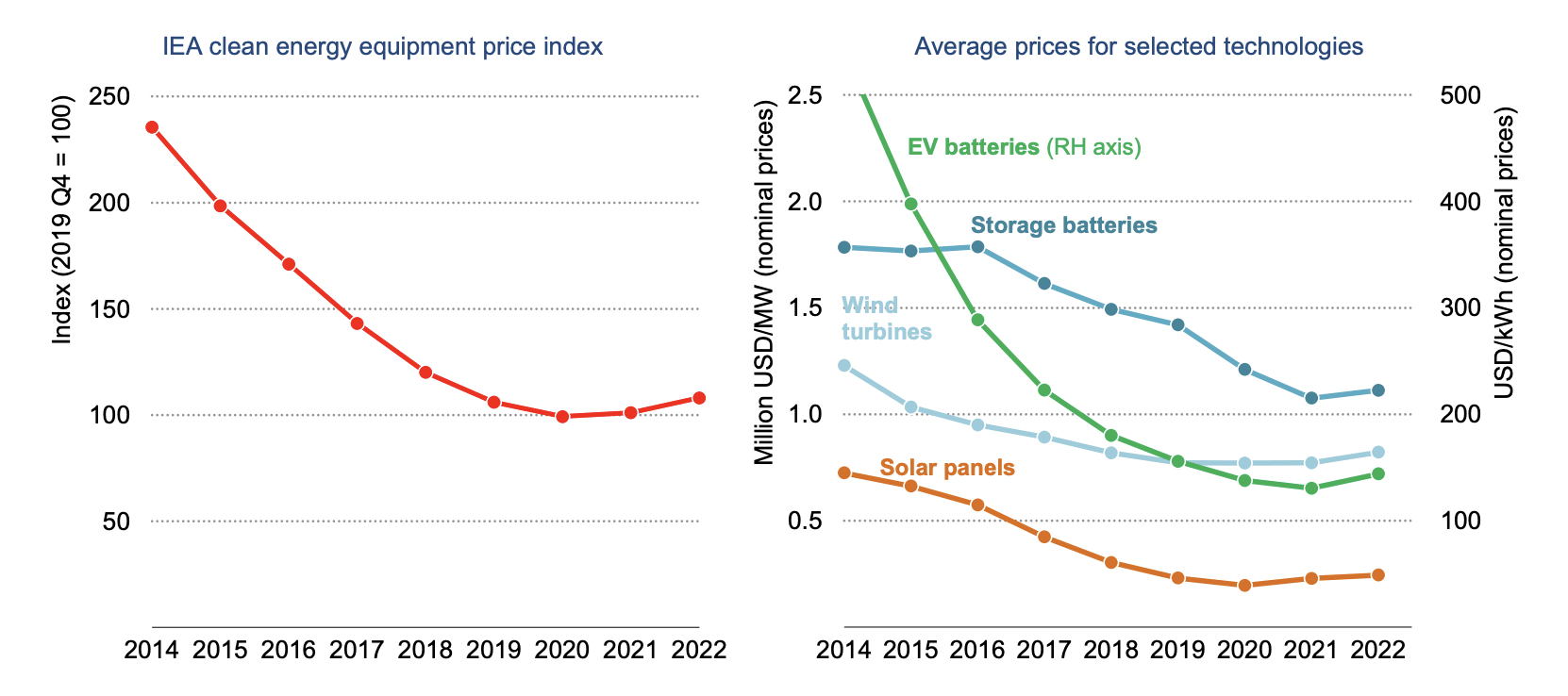

Still, it is expected that the prices of components for solar energy systems will continue to further reduce due to continuous improvements in technology. Down the line, it is expected that solar energy systems will become cheaper than the currently operating coal or gas power plants, but this is currently not the case yet. In addition, we believe nuclear energy will remain a key component of the overall energy supply for years to come.

The chart below from the U.S. Energy Information Administration ((IEA)) shows that the prices for clean energy overall and for solar panels is dropping over time. As mentioned above, a significant part of the decline in prices is due to investments in technology. That said, over the last 2 years the overall clean energy equipment price and the equipment for solar panels increased in price due to high inflation. But, this indicates that it is fairly likely that when inflation comes down the prices of the equipment will turn lower again as well.

{kind=link}

In addition, CSIQ will significantly benefit from the tax credits that were issued by the United States through the Inflation Reduction Act (IRA), which was passed last year. As manufacturers get a significant tax credit for their investments in renewable energy, this should have a direct effect on the demand for solar energy, which will thus directly influence the demand for Canadian Solar as well.

The United States is not the only region that gives favorable tax advantages for investments in renewable energy. Europe has a goal to increase renewable energy sources to 45% of all of Europe's energy production by 2030, an initiative started by the Net-Zero Industry act .

CSIQ: Never Been This Attractive Since IPO

First of all, we have to acknowledge the current headwinds. The weaker guidance and, more specifically the slowing growth is a concern.

The major factor that caused this slowdown is the high-interest-rate environment. Even when taking the subsidies and tax cuts into account, investing in renewable energy, and in this case more specifically solar energy is still quite expensive. Such big investments are often financed with debt, which is making renewable energy solutions less and less viable in high-interest-rate environments.

Now let's take a look at the valuation. Due to the weaker guidance and the overall rough market outlook investors aren't willing to a high premium for growth anymore. This was the case for ENPH, but CSIQ is already at such low valuations that cuts make it a very attractive buying opportunity.

As can be seen in the charts below, Canadian Solar is now trading at historically low valuations, trading even below the stock market lows during the COVID-19 pandemic in March of 2020, when the stock was trading below $15 per share.

Ycharts

In addition, The EPS has never been this high, as can be seen in the chart below.

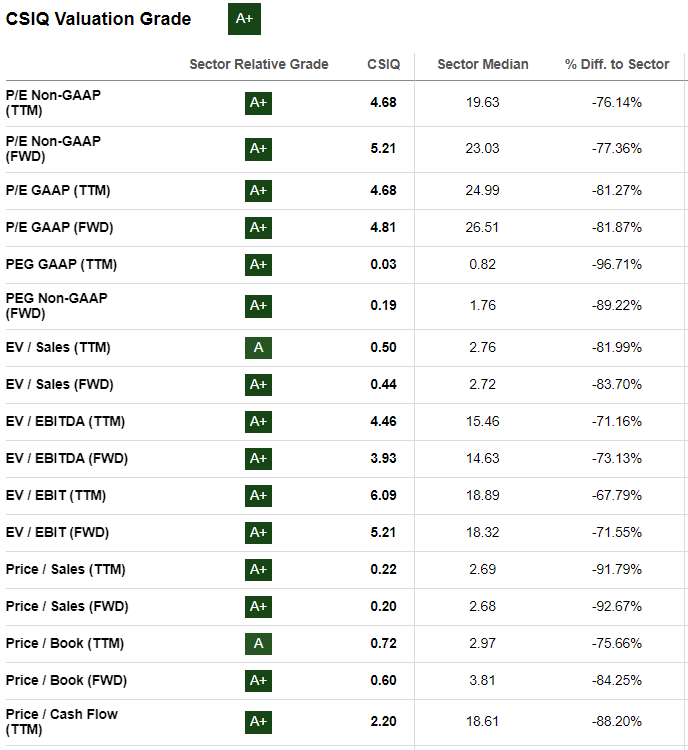

Before taking a look at their peers it is interesting to see that Seeking Alpha's quant rates CSIQ an A+ across all of its valuation metrics, as can be seen in the table below.

{kind=link}

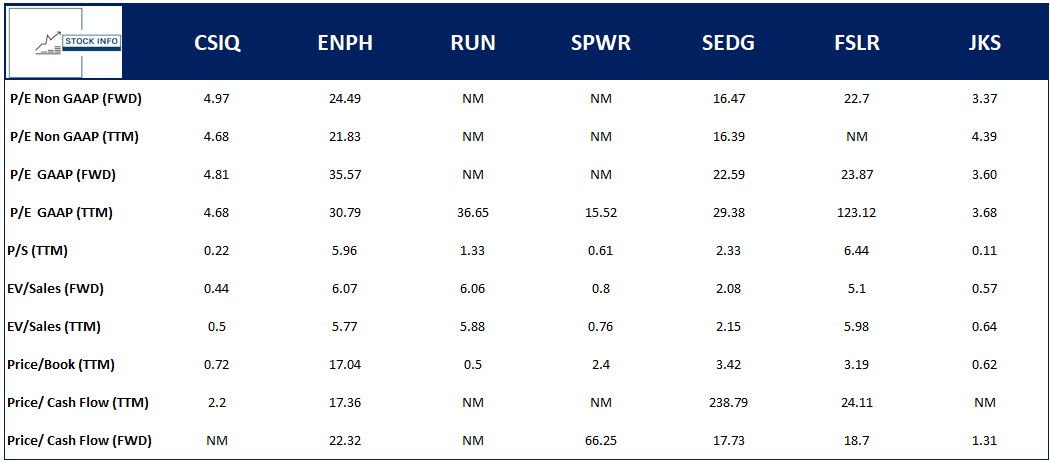

Now let's take a look at their peers. As can be seen in the table below, CSIQ is one of the cheapest when compared to its peers, only beaten by JinkoSolar ( JKS ). Nonetheless, one has to take profitability into consideration.

While JKS looks cheap and definitely is at an interesting valuation as well, the company is not cash flow positive. For example, in fiscal year 2022 JinkoSolar had a $2,617.4M negative cash flow, compared to a positive cash flow of $288.6M for CSIQ over the same period.

{kind=link}

In addition, the only businesses cash flow positive in this list are CSIQ, ENPH, and SEDG. All of the others are cash flow negative and thus currently not profitable investments. Nonetheless, these other businesses remain very interesting, in particular JKS as mentioned earlier.

Currently, the company has a 5Y Revenue CAGR of 20.02%. In addition, they have an FCF yield of around 17.18%, based on 2022 numbers, which indicates that the company is able to buy itself back in less than 6 years, this is very impressive. In addition, CSIQ has a ROIC of 20.46%, indicating that for each $100 the company is able to generate an additional $20.46 in operating income.

CSI Solar IPO Unlocking Value For Shareholders?

In June, CSIQ announced that its majority-owned subsidiary (72%) CSI Solar Co finalized its IPO process. The IPO generated approximately $6B RMB, which was around $850M at the time. Higher than expected by many analysts. This was based on a price of 11.10RMB at the time. Currently, CSI Solar Co Ltd (SHA: 688472) is trading at 14.16RMB.

In general, Chinese investors are more inclined toward manufacturing firms and willing to pay higher multiples compared to US and Europe-based counterparts. This dynamic likely played a role in the decision to list in China.

For these reasons, we believe CSIQ could appreciate quite a bit in share price based on closing the value gap between the US and Chinese listings. After the IPO, CSIQ owns approximately 62% of CSI Solar, assuming that the over-allotment option is exercised in full. At the moment of writing this 62% stake is worth approximately $4.38B. This is over 2x the current market cap of CSIQ, while the valuation will never be on par, even with a discount of 25% CSIQ's stake would be worth $3.285B, which would mean a share price of around $50.91 or almost 2x the current share price.

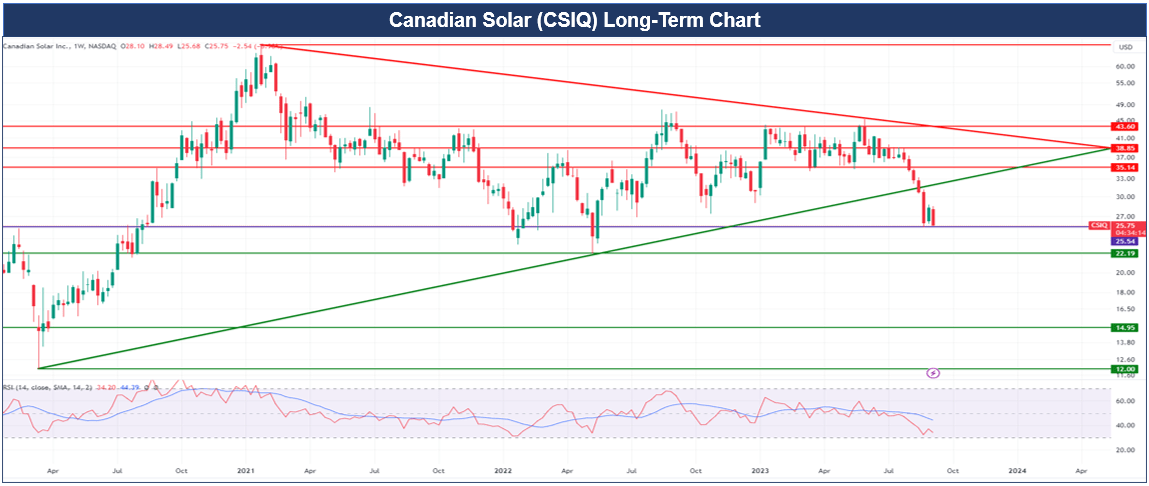

Technical Analysis

As can be seen in the chart below, CSIQ had a rough few weeks, breaking the green trendline support even before the guidance cut was announced. The stock fell right towards the $25.53 level that week, which is where the stock has been hovering around ever since. It will be important to see if the stock will hold here, otherwise, we could see a bit more downside in the short term, a correction towards the $22 level is the first support zone we would then need to look at.

The stock is currently trading below all of its EMA's on a daily basis as well, indicating that the bears are currently in control.

If we bounce here, the first resistance would be the green trendline, which has now become a resistance level. A break above this line could see us move quickly towards the $35 zone.

{kind=link}

Conclusion

In conclusion, Canadian Solar currently provides an interesting buying opportunity despite short-term headwinds and weaker-than-expected guidance. The company operates in the rapidly growing renewable energy sector, with solar energy expected to witness substantial expansion in the coming years.

Although the days of exponential growth might be behind us. I believe CSIQ will continue to grow and margins should increase once the macro outlook improves. In addition, technology advancements will continue to lower the cost of equipment.

CSIQ currently trades at historically low levels, presenting an attractive entry point for potential investors. A small investment in this company operating in an exciting sector might be able to generate significant returns in the future.

Taking into account that a closure of the value gap alone provides significant upside, without taking the other elements into account makes us bullish about this company and as such we rate CSIQ as a buy.

For further details see:

Canadian Solar: Renewable Energy Growth Story Priced Like A Value Stock?