CDLX - Cardlytics: Minimal Catalyst With High Revenue Concentration Risk

2023-05-22 12:28:07 ET

Summary

- Ongoing macro headwind to continue pressuring ad spending and increase the risk of partner and client churns - two stakeholders driving revenue generation.

- Top 5 clients make up +15% of revenue, but top 3 partners account for +70% of the partnership revenue-share pool ("Partner Share").

- Auto-enrolling customers into targeted ad programs may unlock growth at better unit economics. But scale is needed to drive material impact.

Cardlytics ( CDLX ) is a digital advertising/ad and analytics platform focusing on leveraging transactional data from financial institutions/FI and merchants (with its Bridg platform) to provide targeted ad solutions to marketers.

Since the post-pandemic recovery which resulted in a +40% YoY growth in FY 2021, Cardlytics has been dealing with another significant headwind. The ongoing economic slowdown that has been pressuring ad spending continues to pose a big challenge to the growth outlook for FY 2023.

In this coverage, I give Cardlytics a hold rating. My view is that the macro-driven headwind is temporary. Yet, apart from that, I am not seeing any meaningful catalyst on the stock just yet, while the business continues to face a considerable risk due to the high revenue concentration.

Risk

I believe that there are two key risks the business is facing at present. While one of them is mostly macro-driven - and more immediate given the economic situation we are in today - the other one is rather company-specific in nature:

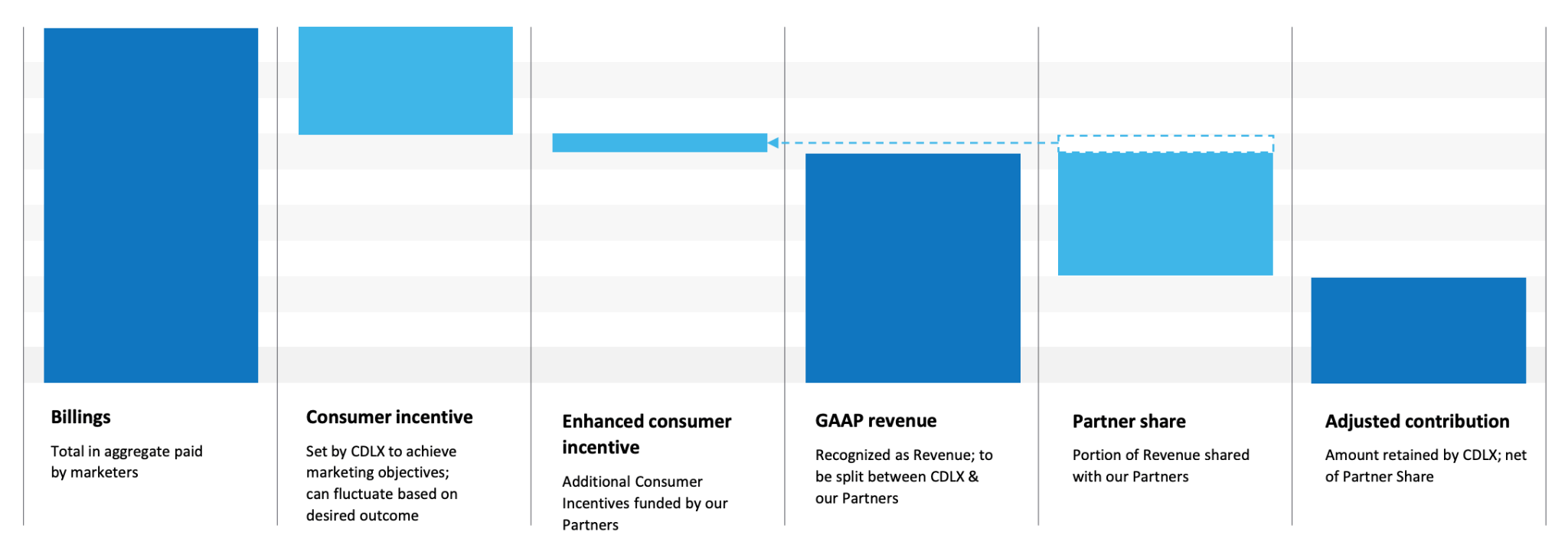

1). Ongoing macro headwinds will continue to pressure ad spending and increase not only the client (marketers/advertisers) but also partner churn risk (mostly FIs) - Cardlytics' business model relies on the revenue generated from the targeted ad campaign run within its partner's digital channels on behalf of the Cardlytics' clients. However, Cardlytics often collaborates with its partners to provide the so-called "Customer Incentives" to drive ad conversions on a revenue-sharing scheme termed "Partner Share", where they both pool incentive expenses together and share revenues, to deliver the expected ROI for its clients. As such, the reduced ad spending is putting pressure not only on its clients but also on its FI partners, risking churn from both sides.

2). The fact that Cardlytics has a high revenue concentration worsens the situation further. In Q1 2023, we have learned that the top 5 clients make up ~15% of the revenue, while the top three FI partners combined made up +70% of "Partner Share" . The impact of partner churn would then be more severe for Cardlytics. In Q1, Cardlytics lost almost half of its UK business due to a loss of just a bank partner. UK revenue also makes up ~5% of Cardlytics' business.

I would imagine that losing another key partner or customer can certainly be very financially damaging for Cardlytics, and the risk is just getting higher the longer the macro slowdown. In that situation, the stock may potentially see at least a +10% decline, shattering the confidence for a rebound.

Catalyst

Based on the Q1 earnings call, there are a few initiatives launched by the management to put the company back on the right track in terms of growth and operational efficiencies that may potentially serve as catalysts for the stock. However, I feel that their impact on the overall business would probably be minimal until the management can replicate and scale them effectively across its partner ecosystem. Nonetheless, I see a potential for some of them to help reaccelerate growth once the economic slowdown softens and ad spend picks up. At scale, I think that they would also drive profitability by enabling Cardlytics to increase MAUs more efficiently.

Of all the recent initiatives, I would probably consider the auto-enroll program a catalyst to watch. In the Q1 earnings call, the management suggested that it will be launched by one of the company's UK FI partners . This is not a new practice in the targeted ad industry, with T-Mobile ( TMUS ) previously also implementing the same tactic .

{kind=link}

By auto-enrolling customers into the targeted ad program, Cardlytics and its partner should be able to grow its MAUs at lower Consumer Incentive, increased partner share, and higher adjusted contribution. This would not only help improve profitability but also drive revenue growth and retention across the board.

{kind=link}

{kind=link}

It is important to note that the management is likely prioritizing operational efficiency improvements at present, especially with the history of widened adjusted EBITDA loss in recent years . In Q1, we observed how billings experienced a decline while consumer incentives continued to rise. Though billings declined as % of revenue from 69% to 67% , it appears as if the management would need a more significant efficiency lever going forward. As the management continues to work towards reducing operating expenses to drive higher adjusted EBITDA, the program may just be the right lever that could help the management drive efficiency at the top-line level (adjusted contribution).

In Q2 and beyond, I believe that investors would probably want to keep an eye on the development of this initiative. A successful launch in the UK may encourage Cardlytics to launch similar programs in the US. I believe that scaling that program effectively across its partners should help Cardlytics improve partner retention, attract more marketers, and grow its revenue more sustainably. Overall, that should take the company closer to its goal of achieving positive OCF/Operating Cash Flow.

Valuation/Pricing

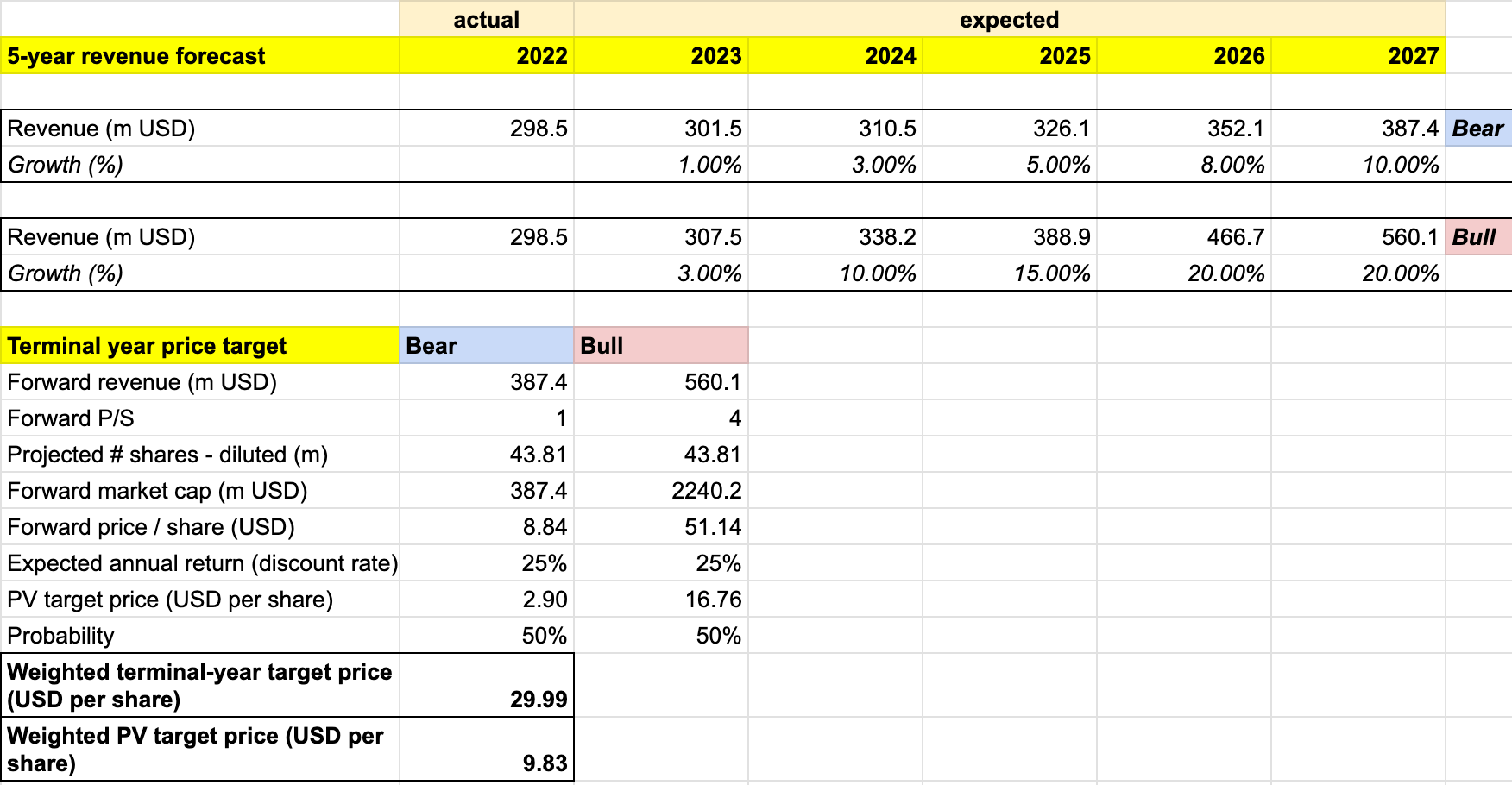

My target price for Cardlytics is driven by the following bull vs bear scenarios of the 5-year revenue forecast:

- Bull scenario (50% probability) - economic downturn to subside towards the end of FY 2023, and given no guidance, I would assume that Cardlytics will end the year with a ~3% growth - around a third of its previous FY's growth rate. Given the more disciplined growth approach under the new management, Cardlytics will probably experience slower growth than it did in recent years, but with better profitability and cash flow outlook. I expect Cardlytics to see growth gradually reaccelerate from 10% in FY 2024 to 20% in FY 2026 onwards, with OCF to continue trending upwards and finally reach breakeven in FY 2025, driven by the success of its growth and operational efficiency initiatives.

- Bear scenario (50% probability) - economic downturn to prolong into FY 2024. Cardlytics to see a merely 1% growth in FY 2023. Growth will continue to accelerate from 3% all the way to 10% into FY 2027 as the economic downturn subsides, but at a much slower rate than in the bull scenario, driven by the minimal success across its initiatives as well as some partner churns in between. The profitability outlook improves at a significant expense of growth, yet OCF generation will remain volatile and relatively weak.

In estimating the P/S ratio for the bull scenario, I consider Cardlytics' past performance during the bull market in 2018 and 2019, where the business maintained a steady +15% growth with a weak profitability profile - mostly negative OCF and FCF, as well as negative double-digit operating margin. During those times, the stock traded mostly at 2x - 3x P/S, though the P/S would gradually trend upward to reach +7x around the back half of 2019. With that in mind, I believe that a P/S of 4x could be fair for Cardlytics under the bull scenario in FY 2027, where I assume a 20% growth and positive profitability and cash flows. For the bear scenario, I would assume a P/S of 1x.

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2027 weighted target price of ~$30 per share in FY 2027. Discounting that target price with a 25% discount rate, I reached a Present Value/PV weighted target price of ~$10 per share. The 25% discount rate represents the expected annual return for holding Cardlytics.

In summary, ~$10 per share is the highest price point at which investors can purchase the stock to realize a projected 25% annual return should my FY 2027 target price of ~$30 be achieved. At ~$6 per share today, the stock trades at a +40% discount to the PV target price - suggesting that the stock is undervalued.

Conclusion

At this time, I assign a hold rating for Cardlytics. My target price model indicates that the stock is undervalued, while I also believe that the macro-driven headwind is temporary. Yet, apart from that, I am not seeing any meaningful catalyst on the stock.

On the other hand, I would continue to be cautious about Cardlytics' high partner and client concentrations, which put Cardlytics at a high risk of losing a significant amount of revenue in case of a churn from either side. Under such circumstances, I believe that the stock would see a deep correction.

It is more likely that the stock will trade sideways into the next quarter. I would probably advise investors to watch for further development of the macro situation, management's progress in reducing expenses across the board, and the potential catalyst I highlighted, before initiating a position.

For further details see:

Cardlytics: Minimal Catalyst With High Revenue Concentration Risk