CDLX - Cardlytics: Undervalued But Risky

2023-07-13 11:35:32 ET

Summary

- Cardlytics has faced a number of challenges over the past year, including customer/partner churn, weak demand, and high costs.

- There are signs that the advertising market has bottomed, which could lead to a return to growth in the second half of the year.

- Cardlytics' stock is inexpensive, but its business model is vulnerable for a number of reasons, making the stock risky.

After a strong run during the pandemic, Cardlytics ( CDLX ) has suffered from customer/partner churn, a weak demand environment and elevated costs. Some of these issues are now being resolved, but soft consumer spending could be a downside risk in the second half. Cardlytics' stock is objectively inexpensive though, and profitability and cash flow concerns should be reduced in coming quarters.

Market

Cardlytics offers a digital advertising platform which leverages consumer spending data and operates through its partners' digital channels. The company is differentiated by its visibility into spending behavior and could benefit from a number of trends going forward.

An increased focus on privacy over the past few years has made it more difficult for digital advertisers to perform targeting and attribution, increasing the value of purchase data. In addition, digital advertising has always had a visibility gap in regard to in-store purchases. Closing this information gap is potentially valuable, as the vast majority of consumer spending still occurs offline. The majority of US consumer payments are now electronic, and the percentage is increasing, making FIs a source of insights into consumer spending, providing the data can effectively be aggregated.

The digital channels of financial intermediaries also provide an attractive means for advertisers to reach potential customers, as they avoid many of the issues of other digital channels. For example, interactions are authenticated, and applications are protected by state-of-the-art security.

It is difficult for banks to capitalize on the digital advertising opportunity for a number of reasons though:

- Fragmentation - Purchase data is fragmented across thousands of FIs in the US. This data must be aggregated to provide an understanding of consumer spending. It should be noted that this issue is more prominent in the US.

- Scale - FIs generally do not have the ability to connect purchase data to their customers' online presence and most lack the scale to make this worthwhile.

- Privacy and Regulatory Concerns - FIs are highly regulated and must ensure they protect customer data.

- Data Complexity - There is no standard methodology for capturing and storing data, making data aggregation across FIs a complex process.

According to a Cardlytics estimate in 2016, the US native bank advertising opportunity was approximately 11 billion USD. This seems like a highly optimistic estimate based on the company's current market penetration and ARPU though.

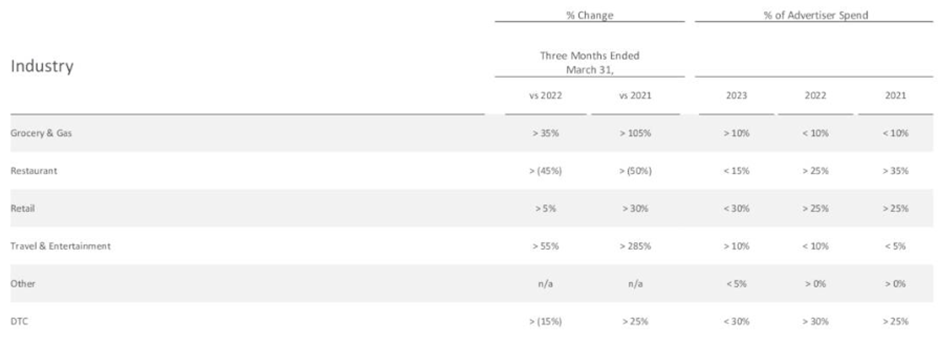

Despite the long-term opportunity, the macro environment has been a significant headwind to Cardlytics' business over the past 6-12 months. The first quarter of 2023 was particularly difficult, with YoY spend only growing by 1% versus 10% in Q1 of 2022. Restaurant and retail spend were both areas of weakness, growing 5% and -2% YoY. Travel spend continues to normalize though, increasing by 12% YoY in the first quarter.

Cardlytics

Cardlytics' provides a native ad platform in its partners' digital channels which enables advertisers to capitalize on insights from consumer spending data. The platform helps marketers both identify likely buyers and measure the impact of their marketing spend.

Cardlytics Direct is Cardlytics' native advertising channel and the company's primary source of revenue. Cardlytics Direct enables marketers to reach consumers across FIs through their digital banking accounts, and increasingly through email and various real-time notifications. The platform predicts where customers are likely to spend and presents them with offers to save money in these categories.

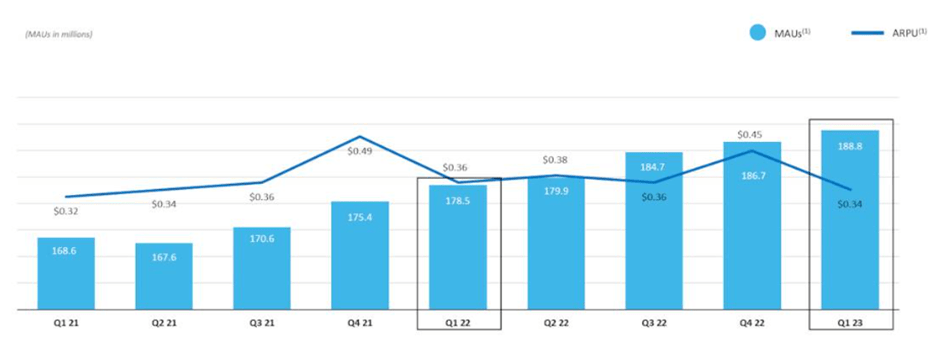

There are currently over 188 million monthly active users on Cardlytics' platform and user numbers are growing steadily. Annual spend covered by the platform is in excess of 4.1 trillion USD and Cardlytics has visibility into one in every two US purchase transactions. This ubiquity potentially makes Cardlytics' platform extremely valuable to advertisers.

{kind=link}

Cardlytics believes engagement with its advertisements is high as they reach customers in a trusted environment. Customers are at least nine times more likely to engage with Cardlytics' advertisements compared to digital display advertisements.

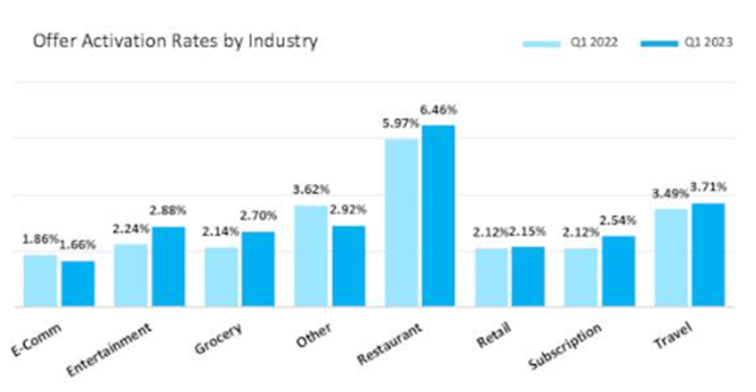

Unique consumers activating offers grew 4.4% YoY in the first quarter, even with the exit of a large restaurant client. Adjusting for this, total activations increased 19% YoY and total redemptions increased 74% YoY. Offer activation rates vary significantly by industry though, with restaurants and travel showing particularly high engagement.

Figure 2: Cardlytics Offer Activation Rates (Source: Cardlytics)

{kind=link}

While Cardlytics' platform clearly provides value to advertisers and FI partners. The company's ability to effectively monetize users is somewhat questionable. Users interact with banking apps / websites infrequently relative to many other internet surfaces, and interactions are generally short. Data shows that Cardlytics' MAUs logged in 10 days per month in Q4 2022. This provides Cardlytics with limited inventory, although this inventory is generally likely to be valuable. Cardlytics' ARPU was only 0.34 USD in the first quarter of 2023, down 5.6% YoY on the back of a weak demand environment. This is extremely low relative to ARPU for platforms like Meta ( META ) or even Twitter.

There is potential for ARPUs to move higher if Cardlytics can increase advertiser demand though. Studies have shown that return on ad spend on the platform is high. Advertisers received 6 USD in incremental return for every 1 USD spent on the platform, compared to 1.50 USD in incremental return for every 1 USD spent with traditional media.

Data points towards growing advertiser adoption of the Cardlytics platform. The total number of advertisers in the channel increased by 8% in 2022. The number of advertisers spending more than 50,000 USD in the channel increased by 8% YoY in the first quarter. Advertisers with billings between 500,000 USD and 5 million USD increased by 11% in the same period.

{kind=link}

Increased advertiser adoption of the platform is also helping Cardlytics to reduce customer concentration. Cardlytics' top five customers accounted for 15% of revenue in the fourth quarter of 2022 compared to 23% a year earlier. This figure is down from 35% in 2020 .

Figure 4: Cardlytics Ad Spend by Vertical (Source: Cardlytics)

{kind=link}

Adoption also appears to be increasing across verticals, although campaign spend ratios indicate penetration is still generally low. Cardlytics defines campaign spend ratio as the amount of spend from MAUs that is associated with the campaigns in which they were targeted divided by the total amount of spend from MAUs in the industries in which MAUs were targeted.

Figure 5: Campaign Spend Ratios by Industry (Source: Cardlytics)

MAUs are a primary driver of revenue for Cardlytics and as a result, MAUs contributed by each FI partner is an important indicator of partner concentration. While Cardlytics is partnered with thousands of FIs, the size distribution of these partners is highly skewed. In 2016, Cardlytics largest FI partner (Bank of America) was responsible for 47% of total FI MAUs. In the same period, Cardlytics largest FI partner in the United Kingdom (Lloyds) was responsible for 10% of total FI MAUs. As of September 30, 2017, Cardlytics had direct contractual relationships with 17 of its FI partners. The other FI partners became part of the network through bank processors and digital banking providers, such as Digital Insight. Digital Insight contributed approximately 13% of total FI MAUs in 2016.

During 2022, Cardlytics' top three FI partners accounted for over 80% of the total Partner Share paid, with the top two FI partners each representing over 20% and third largest FI partner representing over 10%. Cardlytics FI partner concentration, and its reliance on bank processors and digital banking providers, is problematic as it makes it far easier for a competitor to scale its product. It also provides FIs with leverage when negotiating revenue-sharing agreements. The loss of one of the top-2 FI partners would be devastating for Cardlytics.

FI partners need to be compensated for providing access to their customers' payment data, and this is one of the weaknesses of Cardlytics' business model. Cardlytics shares its revenue with FI partners and claims it helps to improve customer engagement. This should be a high-margin source of revenue, but banks are likely to be sensitive to any potential negative impact on customers.

Many FIs operate in a competitive environment and the threat from alternative banking solutions is increasing. As a result, FIs need ways to ensure customers remain engaged. In 2022, data showed customers engaging with Cardlytics' program spent 1.2x more on their card and made 1.3x more shopping trips.

While Cardlytics has faced recent headwinds, management believes its pipeline is solid. The company is reportedly in discussions with multiple top 20 US banks and several high upside fintechs. At least one of these is expected to sign by the end of 2023.

Cardlytics has been working to improve its UI, although this is as much about increasing functionality as it is about improving the look of the product. For example, Cardlytics now provides more detailed descriptions of offers. Cardlytics has observed a 50% increase in impressions on the rewards summary with one bank partner.

Cardlytics has also been working to improve its machine-learning capabilities to drive higher monetization of users. The company is currently in the process of migrating banks to its ad decisioning engine, which is expected to be nearly complete by the end of the second quarter. Banks that have already upgraded are seeing around a 6% increase in activations. The impact of Cardlytics' ranking and budget pacing optimization is expected to be around 2.2 million USD in the second quarter.

New targeting features released in Cardlytics' Ads Manager include:

- The ability to target audiences who shop at competing brands.

- The ability to target based on minimum or maximum amounts of spend during the same period.

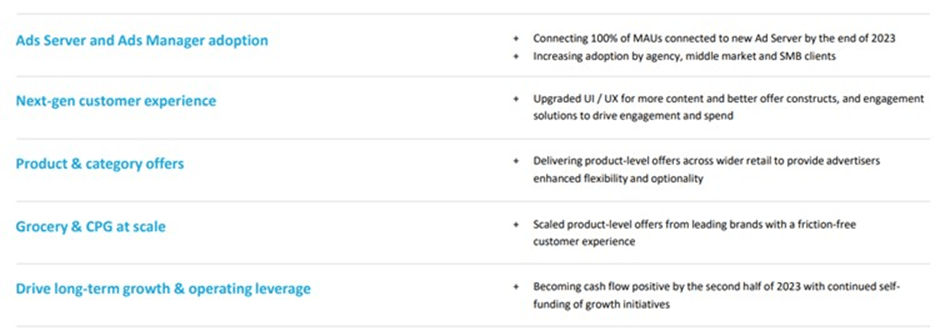

Figure 6: Cardlytics Strategic Initiatives (Source: Cardlytics)

{kind=link}

Cardlytics acquired Bridg in 2021 for its customer data platform. Cardlytics is transforming Bridg from a customer data platform into a retail media network for mid-market and regional retailers. This could be valuable as many smaller retailers lack the ability to do this themselves.

Retail Media Networks are digital ad platforms operated by retailers and are becoming an increasingly important part of adtech ecosystems. This is because they are able to provide valuable data, such as demographics and shopping behavior, based on actual known customers.

The Bridg acquisition aimed to give Cardlytics access to more granular data. Bridg can connect to 90% of PoS systems in the US and provide SKU level insights. This more comprehensive view of consumer purchase behavior is useful for retail media networks and CPGs. Cardlytics is currently in the process of building out its base of smaller retailers on the retail media network.

Cardlytics acquired Bridg for approximately 350 million USD in cash. The company also agreed to two potential earnout payments in cash and stock on the first and second anniversary of the deal, with the payout being determined by Bridg's annualized revenue run rate in the US. At the time, Cardlytics expected these payments to equate to roughly 100-300 million USD in total.

An independent accountant recently determined that the first-anniversary payout was 208.1 million USD. It is also now anticipated that there will be no second-anniversary payment. The total cash for both earn-outs is expected to be 72.6 million USD and 3.4 million shares are expected to be delivered for the equity portion of the earn-out. Cardlytics expects the equity portion to be independent of the current trading price of the stock, resulting in half the shareholder dilution originally anticipated.

Cardlytics also acquired Dosh in 2021 for its cash-back offers platform. The transaction was worth 275 million USD in cash and stock. Dosh provides Cardlytics with access to a younger user base, and fintech clients like Venmo. Dosh also has a stand-alone cash back app that helps it to understand what drives consumer engagement.

Financial Analysis

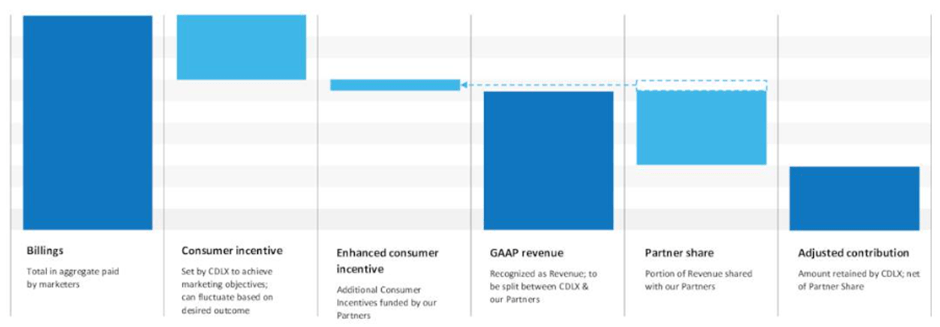

Cardlytics' billings decreased 2.6% YoY in the first quarter, while revenue decreased 5.3% YoY and Bridg revenue grew 34% YoY. Excluding the large clients that exited Cardlytics channel last year, revenue growth was 10% YoY and US billings growth was 21% YoY. Adjusted contribution decreased 5.6% YoY. Adjusted contribution is defined as revenue less the cost of obtaining purchase data and advertising space from partners.

Travel and entertainment and gas and grocery were strong verticals in the first quarter. US revenue declined by 0.9% YoY and UK revenue decreased by 48.2% in USD. The decrease in UK revenue is primarily due to the loss of a bank partner, highlighting the risk of customer concentration. Cardlytics is making progress in this regard though, with its top five customers accounting for 15.1% of revenue in the most recent quarter compared to 25% a year earlier.

For the second quarter, revenue growth is expected to be -7.8%. The decline of Cardlytics' UK business is expected to be responsible for a negative mid-single-digit impact on growth.

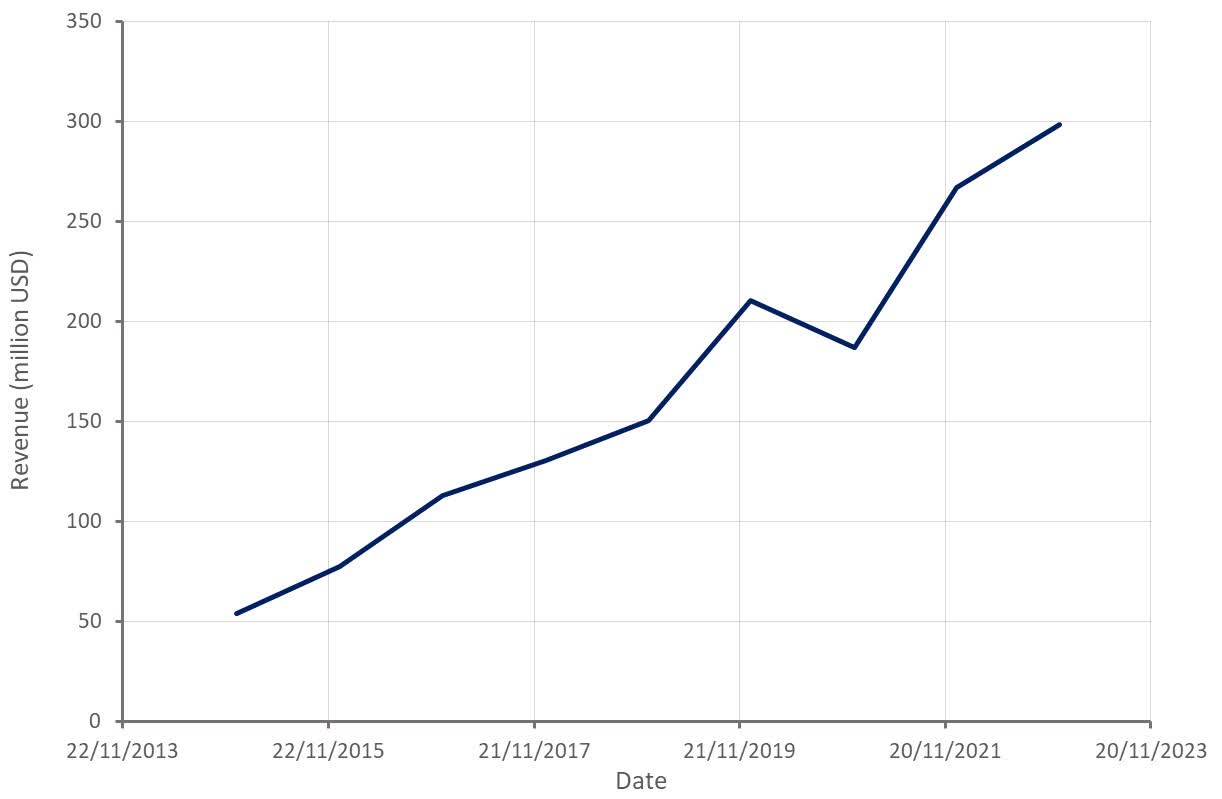

Figure 7: Cardlytics Revenue (Source: Created by author using data from Cardlytics) Table 1: Revenue Contribution by Country (Source: Cardlytics)

{kind=link}

Cardlytics gross profit margins are quite poor, which is a structural outcome of the fact that it has to share revenue with its FI partners. The stock would be far more attractive if Cardlytics could negotiate better revenue-sharing agreements, but given partner concentration, its negotiating position is likely quite weak.

{kind=link}

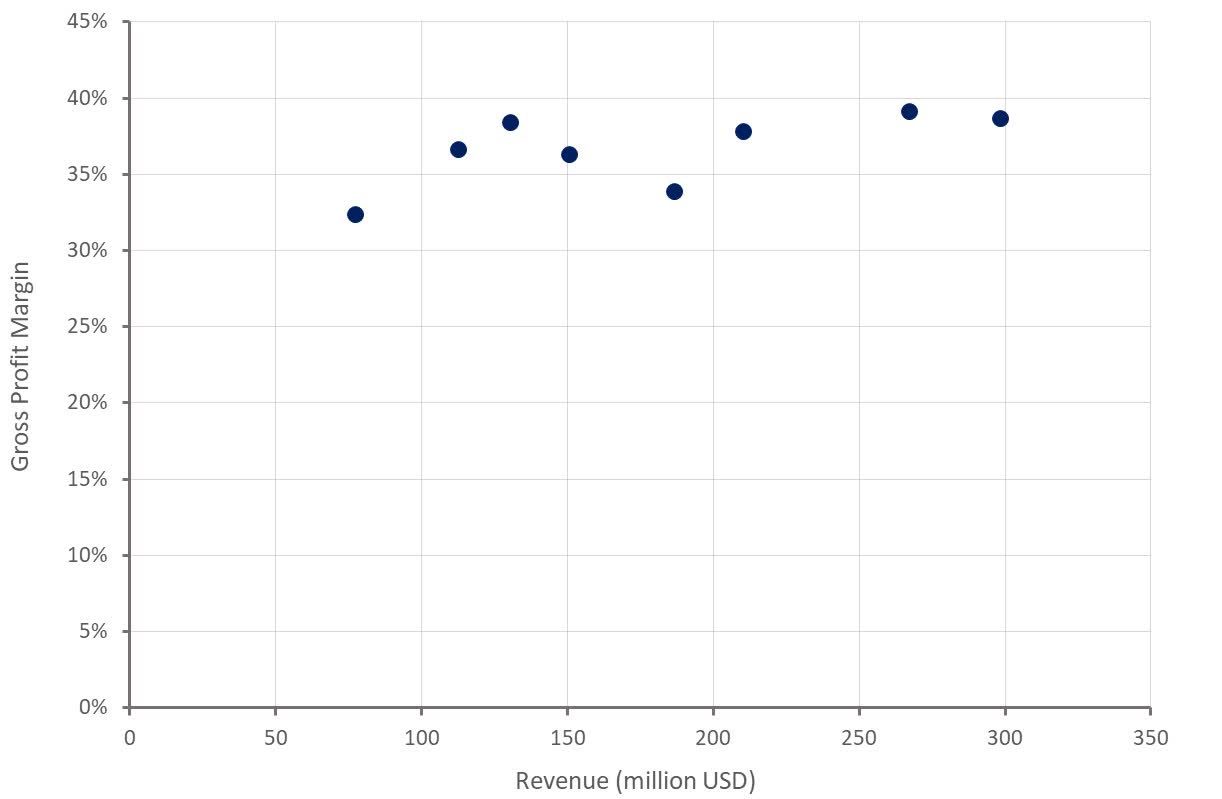

Outside of macro weakness, Cardlytics has shown some ability to drive higher gross profit margins with scale though. Gross margins should also be aided by Bridg's rapid growth as this business has higher margins.

Figure 9: Cardlytics Gross Profit Margins (Source: Created by author using data from Cardlytics)

{kind=link}

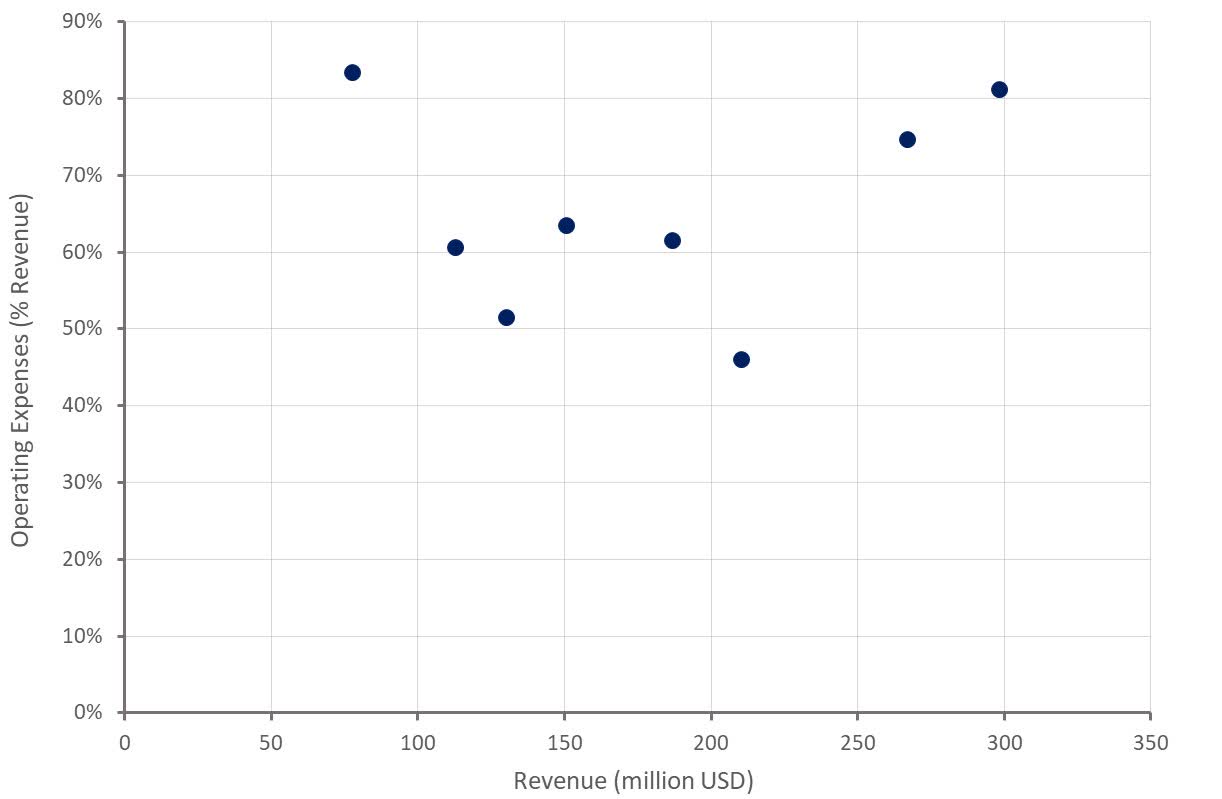

Cardlytics has been working to improve its cost base, including a 3.9 million USD one-time reversal of a bonus accrual and renegotiating the lease on its office space in Atlanta. The amended lease is expected to save the company a touch over 1 million USD annually over the next two years.

These types of efforts will not shift the company's bottom line significantly though. Cardlytics' will ultimately need to realize operating leverage through scale before it becomes profitable on a sustainable basis.

Figure 10: Cardlytics Operating Expenses (Source: Created by author using data from Cardlytics)

{kind=link}

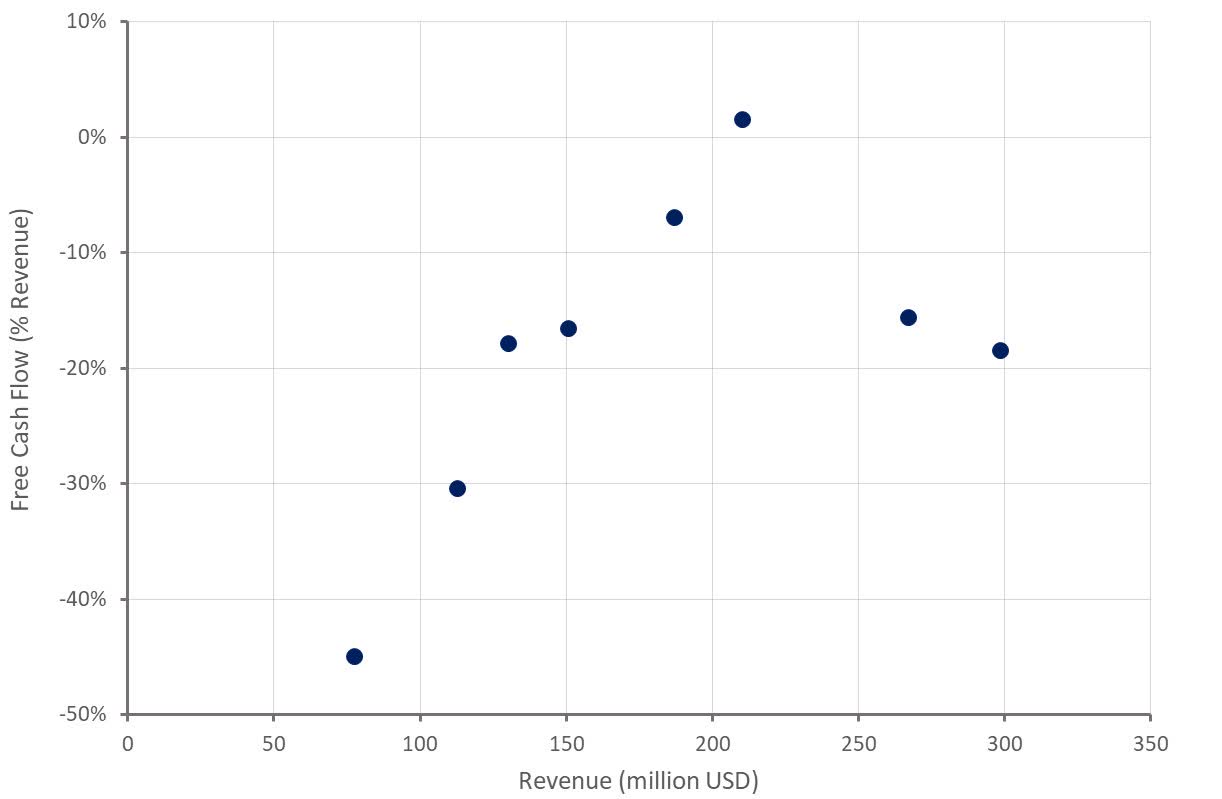

With a greater focus on costs and continued growth, Cardlytics expects positive cash flows later in 2023.

Figure 11: Free Cash Flow (% Revenue) (Source: Created by author using data from Cardlytics)

{kind=link}

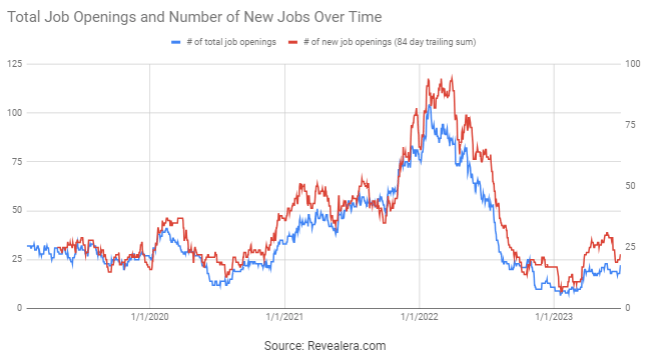

Hiring appears to have picked up in 2023, which supports the notion that the business has bottomed.

{kind=link}

Valuation

Despite the stock moving significantly higher in recent months, Cardlytics' valuation remains low, indicating investor skepticism about the ability of the company to sustainably generate free cash flows. While the near term is likely to remain volatile, and Cardlytics may need to raise capital, the company is progressing towards positive free cash flows.

The long-term strength of Cardlytics' business is questionable though. There are privacy concerns regarding accessing payments data and the fact that Cardlytics' doesn't control the payments data will likely ensure margins remain low. Customer/partner concentration also remains an ongoing concern, amplified by the fact that there have been problems with customer churn.

{kind=link}

For further details see:

Cardlytics: Undervalued But Risky