TAST - Carrols Restaurant Group: Bad For Your Health And Your Portfolio

2023-05-28 05:01:10 ET

Summary

- Carrols Restaurant Group operates hundreds of Burger King franchises across the US.

- An investment in Carrols Restaurant Group would have lagged the S&P by 200% over the past decade.

- Operating in the restaurant industry is notoriously challenging and usually results in weak margins.

Introduction

Who doesn't like the occasional hamburger with a side of french fries?

You know it's probably not the best for your health, in fact, you probably know it's terrible for your health, but many of us still splurge on the occasional fast-food visit as a sort of guilty pleasure.

For many, the first of these fast food restaurants that come to mind is likely McDonald's ( MCD ), for others, its Wendy's ( WEN ), but in this article, I'll be talking about the other burger chain, specifically a sizeable US-based franchise operator of Burger Kings, Carrols Restaurant Group ( TAST ).

Carrols Restaurant Group operates hundreds of these popular fast-food franchises across the US. But despite the addictive qualities found in many of the products they sell: fatty meat, salty fries, and sugary soda, its stock price is clearly not as popular with investors as its food is with its customers...

Over the past decade, investors in CRG earned a total return of just 5.7% compared to a 202.1% return for S&P 500 investors. That meager 6% return would have actually been much worse if not for the sharp rally it benefited from in 2023.

So what gives? What is going on with this business?

Within this article, I'll examine the business performance of Carrols Restaurant Group, and its financial performance, and discuss where I believe the stock price may go from here.

The Restaurant Business: A Notoriously Competitive Industry

Before we get Carrols, let's take a step back and discuss the restaurant industry at a high level so we have some better context to frame CRG's operations.

Let's start with the positives of the restaurant industry, first of all, the product sold is a necessity to life itself, food, everyone must eat to survive. But restaurants are very different from grocery stores, which also sell food. Restaurants must also provide service, primarily in the form of cooking that food, thereby providing convenience to the consumer.

Once you have the food and the labor, all that's left is the real estate, while the best real estate usually comes at a high price to own/rent, there are usually many acceptable locations in any given town where a restaurant could perform well.

In short, it really does not take much to start a restaurant.

And for that very reason, many chose to start their own. According to Zippia , there are over 660K restaurants in the USA, and 70% percent of those are single-unit operations.

Peter Theil once wrote about the challenges of the industry at length in his book, From Zero to One. In his book, he mentioned that despite the majority of these restaurant ventures failing within one-two years, and entrepreneurs knowing that fact, many still chose to open believing their offering is unique.

Industry Challenges on Full Display

No more evident have the challenges of the restaurant industry been as during the COVID-19 pandemic which shuttered the doors to many restaurants and led to a radically changed labor market, and highly variable food commodity prices.

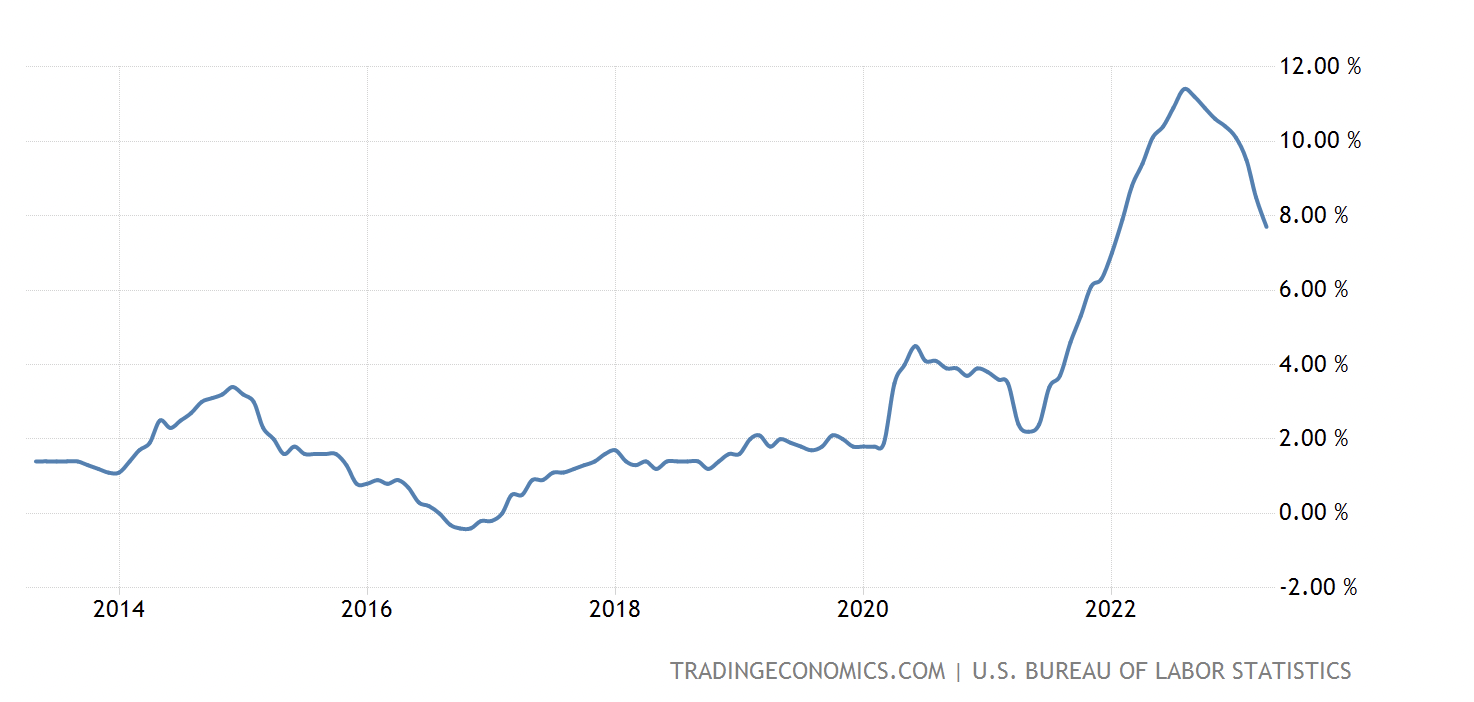

Food Price Inflation USA (US BLS: Trading Economics)

{kind=link}

Over the last decade, food prices remained relatively stable fluctuating between 0-3% increases per annum, which provided business owners with the flexibility to plan their menu prices, and more easily forecast business performance.

Ongoing inflation and supply chain worries make operating a restaurant much more challenging and unpredictable.

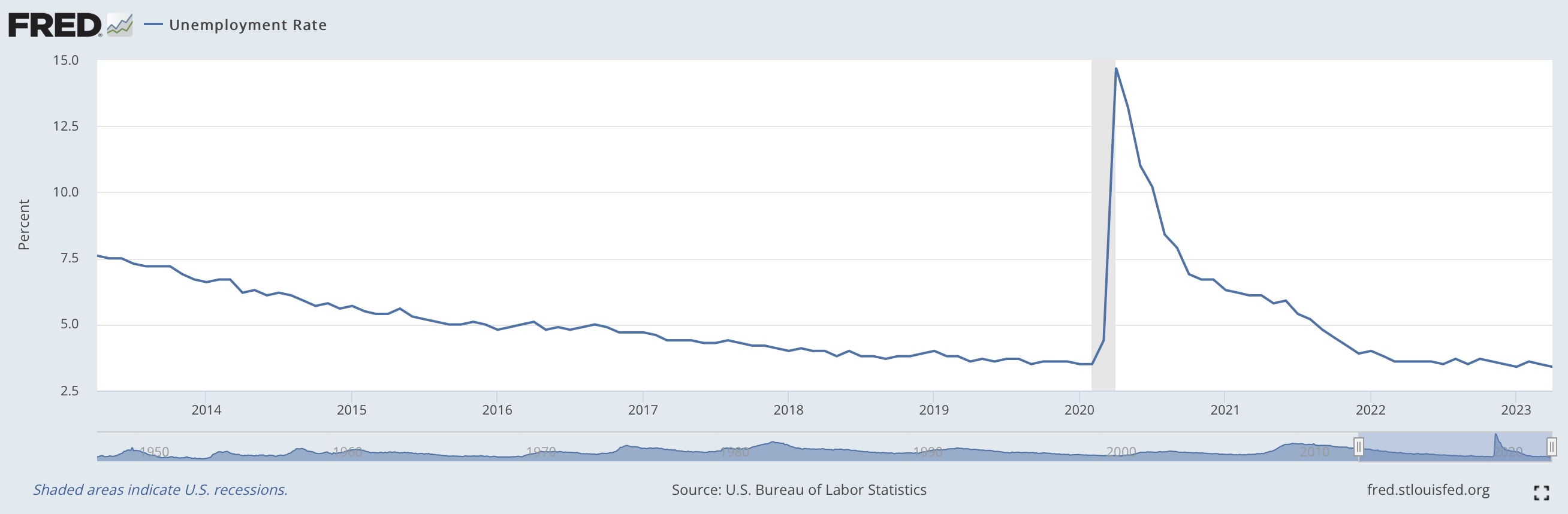

Adding on to the challenges brought on by food inflation is the labor pool in the USA which is at a near-all-time low in unemployment.

{kind=link}

How these numbers are so low right now, in the face of so many different economic challenges is perplexing to me, but regardless of the reason, such low unemployment will increase wage pressure on businesses and could further strain their margins.

Starbucks ( SBUX ) is witnessing this firsthand, as it battles an ongoing unionization effort that impacts several of its stores.

Weak Margins

Speaking of margins, according to Restaurant365, restaurants usually operate with a profit margin in the mid-low single digits.

Because consumers can choose between so many other options, including cooking their own food, prices are kept low. More entrants just exacerbate the problem.

Chains are able to leverage their brand to drive increased sales, something that Carrols benefits from, but that alone is not enough to keep a restaurant afloat.

Financials

Margins

Looking at Carrols margins a few insights emerge, they have a decent gross margin of 36%, but that's quite low compared to operators like McDonald's which are less exposed operationally to the restaurant business, instead licensing their brand to franchisors for a fee.

The problem extends to the bottom line as well, where the profit margin is in the red, at negative 3%. Looking back over the past decade and things are not much brighter, during its best year of the decade, 2017, the profit margin was still in the low single digits, albeit positive. Compare that to McDonald's which has a net profit margin of 30% and you can see why the franchise model is so favored.

Revenue and CFO

Looking at revenue and operating cash flow, on a per-share basis, we can see that CRG's business has been anything but predictable as cash flows and revenues have fluctuated so heavily.

Returns on Invested Capital

It's no surprise to me that such a variable business performance has resulted in such poor returns on invested capital. During a good year, CRG invests capital to earn a low single-digit return, in a bad year they are earning negative returns on capital (like this year so far).

Valuation and Conclusion

Compared to other franchisees, Arcos Dorados ( ARCO ), and Fiesta Restaurant Group ( FRGI ) Carrols is priced roughly in line at a 0.5x price to sales and 13x EV to EBITDA. While these ratios are low, in the context of its business model, I feel they may not be low enough.

If Carrols were to trade in line with Arcos Dorado's EV to EBITDA multiple of 7.3x that would mean shares would need to fall more than 40% from where they are today. I see that as a strong possibility given the challenges it's facing vis-a-vis labor, and food prices, as well as its market positioning.

I rate Carrols Restaurant Group a Sell.

For further details see:

Carrols Restaurant Group: Bad For Your Health And Your Portfolio